|

시장보고서

상품코드

2063956

실험실 정보 관리 시스템(LIMS)용 AI 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Laboratory Information Management Systems (LIMS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

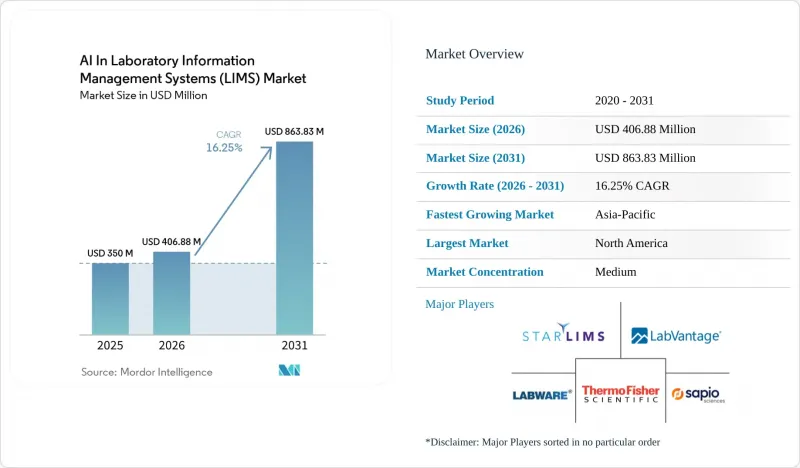

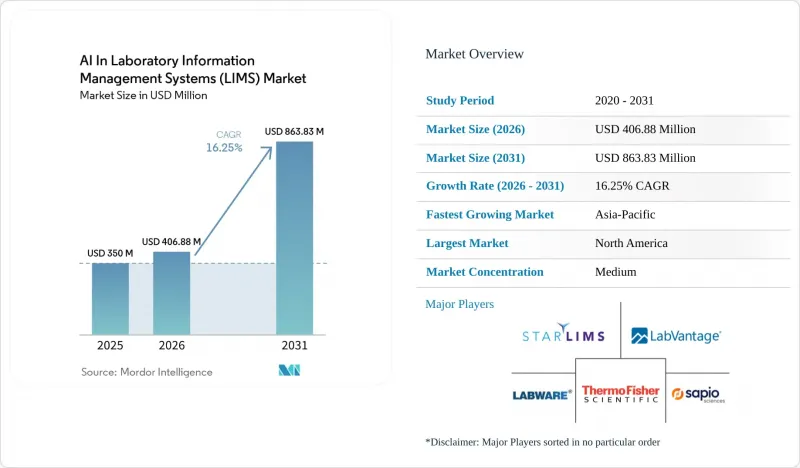

Mordor Intelligence에 의하면, 실험실 정보 관리 시스템(LIMS)용 AI시장 규모는 2025년 3억 5,000만 달러로 평가되었고, 2026년에는 4억 688만 달러로 추정되고, 2026-2031년 CAGR 16.25%로 성장을 지속할 전망이며, 2031년에는 8억 6,383만 달러에 이를 것으로 예측됩니다.

본 보고서는 AI 기능별(예측 분석, 이상 감지, 워크플로우 자동화, 기타), 컴포넌트별(플랫폼 소프트웨어, AI 모듈, 서비스), 도입 형태별(온프레미스, 프라이빗 클라우드, SaaS, 하이브리드), 연구소 유형별(제약 및 바이오기술, CRO/CDMO, 진단, 바이오뱅크, 학술 기관), 지역별(북미, 유럽, 기타)로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

세계 실험실 정보 관리 시스템(LIMS)용 AI 시장 동향 및 인사이트

예외 상황 처리 및 애널리스트의 생산성 향상을 위한 내장형 AI 코파일럿

LIMS 분야의 AI 시장에서는 과학자와 분석가들이 반복적인 검토 업무에서 예외 처리 업무로 전환할 수 있도록 돕는 ‘코파일럿’이 단기적으로 가장 빠른 수요 증가를 이끌고 있습니다. 이는 대량의 데이터를 다루는 품질 관리 실험실에서 여전히 기록 검색, 편차 확인, 서로 다른 정보 관리 도구 간 이동에 막대한 시간을 소비하고 있기 때문에 중요한 의미를 지닙니다. Sapio Sciences는 2026년 4월, Anthropic의 ‘Claude Cowork’를 Sapio Platform에 통합했습니다. 이를 통해 과학자들은 단일 대화형 인터페이스를 통해 추적 가능성과 사용자 속성 정보를 확보하면서, LIMS 및 ELN 데이터의 조회, 분석, 작업 실행이 가능해졌습니다.

LigoLab 역시 자사의 AI 에이전트 로드맵이 실험실 업무에서 자연어 기반 대화를 지원한다고 밝혔으며, 이는 평이한 언어를 통한 접근이 프리미엄 추가 기능이 아닌 제품의 표준 기능 중 하나로 자리 잡고 있음을 보여줍니다. LIMS 분야의 AI 시장 내 ‘코파일럿 계층’이 보급됨에 따라, 그 우위는 언어 인터페이스를 검증된 워크플로우 내의 구조화된 실험실 맥락, 감사 가능성 및 실행 가능성과 결합한 벤더에게로 이동할 가능성이 높습니다. 이는 구매자들의 기대도 변화시키고 있습니다. 왜냐하면 연구실에서는 더 이상 기록을 요약해 주는 AI를 원하는 것이 아니라, 적절한 맥락을 파악하고 일상 업무에서 규정 준수 행동을 지원할 수 있는 AI를 원하기 때문입니다.

점점 더 커지는 멀티오믹스와 고성능 데이터의 복잡성

또한, 멀티오믹스와 고성능 실험 데이터의 양과 다양성이 확대되면서 시장을 주도하고 있습니다. 기존의 LIMS 아키텍처는 시료 및 측정법의 추적을 목적으로 구축되었으나, 현재 국가 및 기업의 연구 프로그램을 통해 생성되는 규모의 전사체, 단백체, 후성유전체, 염기서열 분석 결과를 통합하도록 설계되지는 않았습니다. Illumina는 2026년 2월, 전문가가 구축한 파이프라인을 통해 학습한 AI 기반 워크플로우 제안 기능을 탑재한 ‘Connected Multiomics v1.1’을 출시했습니다. 이로 인해 메타분석을 설계할 때 고도의 생물정보학 지식이 필요했던 부담이 줄어들었습니다.

Sapio Sciences와 Ultima Genomics는 2025년 9월, 초고성능 시퀀싱과 AI 기반 LIMS 워크플로우를 결합하기 위한 제휴를 체결했습니다. 이는 확장성과 추적성을 확보한 멀티오믹스 분석에 대한 수요가 증가하고 있음을 반영합니다. 2025년 『Quantitative Biology』지에 게재된 논문에 따르면, 정규화, 보완, 모달리티 간의 조화가 여전히 멀티오믹스 통합의 주요 장애물로 남아 있는 것으로 밝혀졌습니다. 이는 임베디드형 분석 지원에 중점을 둔 LIMS 분야의 AI 시장 세분화와 잘 부합합니다. 싱가포르의 PRECISE-SG100K 프로그램 역시 LIMS를 통한 클라우드 파이프라인을 통해 약 5만 건의 전장 유전체 염기서열 분석 결과를 보고했으며, AI를 활용한 품질 관리를 통해 워크플로우 최적화 후 처리 시간을 3분의 1 이하로 단축하는 데 성공했습니다.

AI를 활용한 워크플로우에서 GxP 검증에 따른 부담

이 시장은 규제 대상인 실험실용 소프트웨어와 관련된 검증 부담이라는 장벽에 여전히 직면해 있습니다. 제약 제조 및 관련 분야의 실험실에서는 AI 기능을 단순한 사용자 인터페이스 업그레이드로만 볼 수 없습니다. 왜냐하면 이러한 기능들은 검토, 예외 처리, 안정성 해석, 릴리스 지원에 영향을 미칠 가능성이 있기 때문입니다. 주요 문제점은 적응형 또는 모델 주도형 동작이, 정적이고 결정론적인 소프트웨어를 위해 구축된 기존의 검증 절차에는 쉽게 부합하지 않는다는 점에 있습니다. 그 결과, 승인 절차가 지연되고 문서화 작업이 증가하며, AI 감독에 관한 성숙한 내부 거버넌스를 아직 확립하지 못한 품질 관리 팀에서는 보다 신중한 태도를 보이게 될 것입니다. 그 결과, LIMS 분야의 AI 시장은 위험이 낮은 워크플로우에서 먼저 도입이 진행되는 반면, 보다 중요한 이용 사례로의 전환은 지연되는 경향을 보이고 있습니다. 이러한 경향은 특히 위험을 회피하려는 구매자층에서 두드러지며, 특히 컴플라이언스 팀이 제한된 도입 범위를 넘어 확대를 진행하기 전에 모델 모니터링, 재검증 트리거, 지속적인 인적 검토에 관한 보다 명확한 규칙을 요구할 때 더욱 뚜렷하게 나타납니다.

부문별 분석

2025년, LIMS 분야의 AI 시장 점유율 35.16%를 차지한 것은 ‘예측 분석 및 예측’이었으며, 이는 다른 분야를 압도적인 차이로 앞지르며 가장 큰 기능 부문이 되었습니다. 이 리드는 품질 관리 동향 분석, 안정성 모델링, 장비 고장 예측이 이미 ‘업무 중단 감소’나 ‘검토 신속화’와 같은 측정 가능한 실험실 성과로 직접 이어지고 있다는 사실을 반영하고 있습니다. LIMS 분야의 AI 시장이 이 기능을 중시해 온 이유는 데이터 이력이 방대하고 예측 대상이 명확하게 정의된 경우, 지도 학습 모델이 뛰어난 성능을 발휘하기 때문입니다. 워터스사는 2025년, 텔레메트리 기반 예측을 통해 LC-MS의 유지보수를 사후 대응에서 계획적인 조치로 전환할 수 있음을 보여주었습니다. 이는 가동 시간과 자원 효율성을 모두 향상시킵니다. 따라서, 특히 신뢰성과 추적 가능성이 중시되는 규제 환경에서는 예측형 이용 사례가 자유도가 더 높은 생성형 이용 사례보다 도입의 정당성을 입증하기가 더 수월합니다.

지능형 워크플로우의 자동화 및 오케스트레이션은 LIMS 분야의 AI 시장에서 가장 빠르게 성장하고 있는 기능으로, 2031년까지 연평균 성장률(CAGR)이 18.88%를 나타낼 것으로 전망됩니다. 이러한 성장은 단순히 알림이나 개요를 생성하는 데 그치지 않고, LIMS, ELN, 장비, 연결된 실험실 기기에 걸친 단계를 조정할 수 있는 에이전트 기반 시스템에 대한 관심이 높아짐에 따라 주도되고 있습니다. LabVantage Cortex는 에이전트형 AI를 LIMS의 운영 계층에 통합함으로써 이러한 방향성을 구현하고 있습니다. 이를 통해 워크시트 지원, 샘플 관리, 안정성 검사 조정, 자동 모니터링과 같은 작업을 단일 플랫폼 환경 내에서 수행할 수 있게 됩니다. 또한, LIMS 분야의 AI 시장 전체를 보더라도 이상 감지, 지식 검색, 시맨틱 검색, 코파일럿 기능 부문에서 지속적인 성장이 나타나고 있습니다. 이는 과학 팀이 점점 늘어나는 데이터 자산 전반에 걸친 맥락 정보에 신속하게 접근하기를 원하기 때문입니다. 향후에는 운영 측면에서 심도 있는 기능이 없는 고립된 AI 기능을 제공하는 것이 아니라, 해석 가능한 예측, 워크플로우 액션, 거버넌스에 부합하는 도입을 결합할 수 있는 도구가 기능 선정 과정에서 우위를 점할 가능성이 높을 것으로 보입니다.

2025년 LIMS AI 시장 규모에서 AI 지원 LIMS 플랫폼 소프트웨어가 65.17%를 차지했으며, 이는 구매자들이 여전히 핵심인 인포매틱스 계층의 업그레이드를 가장 중요하게 여기고 있음을 보여줍니다. 이러한 경향은 AI가 단순한 부가 기능으로 구매되는 것이 아니라, 계약 가치와 벤더 종속성을 확대하는 광범위한 플랫폼 개편의 일환으로 구매되는 경향이 강해지고 있음을 시사합니다. LIMS 분야의 AI 산업에서는 이미 시료 기록, 감사 추적, 워크플로우 로직, 사용자 권한을 관리하고 있는 공급업체가 유리한 입장에 있습니다. 왜냐하면 이러한 자산이 AI를 얼마나 효과적으로 통합할 수 있는지를 좌우하기 때문입니다. Sapio Sciences는 실험실 데이터 전반에 걸친 대화형 상호작용을 핵심으로 하는 플랫폼을 구축한 반면, LabVantage는 핵심 실험실 업무에 에이전트 기능을 통합한 클라우드 네이티브 플랫폼을 도입했습니다. 이러한 움직임은 플랫폼 소유자가 장기적인 가치 창출의 중심이 될 것이라는 관점을 뒷받침하고 있습니다.

서비스 부문은 2031년까지 연평균 성장률(CAGR) 17.12%로 확대될 것으로 예상되며, LIMS 내 AI 시장에서 가장 빠르게 성장하는 부문이 될 것입니다. 이러한 성장은 구현, 검증, 워크플로우 재설계, 지속적인 모델 거버넌스에 여전히 전문적인 지원이 필요하며, 많은 연구소에는 사내에 그러한 자원이 없습니다는 현실을 반영하고 있습니다. 특히, 조직이 여러 거점에 걸쳐 운영되거나, 장비나 업스트림 시스템을 연동해야 하거나, 도입 시 명확한 규정 준수 증거를 확보하고자 할 경우, 서비스에 대한 수요가 특히 높아집니다. 따라서 LIMS 분야의 AI 시장은 단순한 소프트웨어의 규모 확대와 같은 양상을 보이지 않습니다. 왜냐하면 운영상의 성공은 여전히 데이터 준비, 적격성 평가 작업, 사용자 교육, 도입 후 모니터링에 달려 있기 때문입니다. 모델, 부조종사, 분석 모듈은 점차 보급되고 있지만, 고객이 체계적인 데이터 구조, 검증된 통합 패턴, 또는 AI가 규제 대상 업무에 어떤 영향을 미칠 수 있는지에 대한 명확한 규칙을 갖추지 못한 경우, 이러한 모듈의 활용은 제한된 상태로 남아 있게 됩니다.

지역별 분석

2025년, 북미는 LIMS 분야 AI 시장 점유율의 38.18%를 차지했으며, 이 시장의 최대 지역 기여 요인으로서의 위상을 유지했습니다. 이 지역은 제약사, CRO, 대규모 유전체학 프로그램, 그리고 잘 정립된 실험실 정보학 공급업체들이 밀집해 있다는 이점을 누리고 있습니다. LIMS 분야의 AI 시장은 특히 미국에서 깊이 뿌리내리고 있습니다. 이는 미국 구매자들이 강력한 구매력을 갖추고 있을 뿐만 아니라, 품질, 감사 가능성, 워크플로 관리에 대해서도 엄격한 기대치를 가지고 있기 때문입니다. 또한, 미국과 캐나다의 대규모 다지점 연구소 네트워크에서는 분산된 검사 환경 전반에 걸쳐 AI 주도 표준화의 가치를 더욱 높이는 표준화 프로젝트도 추진되고 있습니다. 규제가 가장 엄격한 이용 사례에서는 도입이 여전히 신중하게 진행되고 있지만, 이러한 요인들이 해당 지역의 우위를 계속해서 뒷받침하고 있습니다.

유럽은 독일, 영국, 프랑스를 중심으로 LIMS 분야의 AI 시장에서 여전히 중요한 비중을 차지하고 있습니다. 이 지역 수요는 규제된 의약품 데이터 관리와 엄격한 데이터 보호 요건을 모두 충족해야 할 필요성에 의해 형성되고 있으며, 명확한 데이터 저장 위치와 거버넌스 옵션을 갖춘 아키텍처가 선호되고 있습니다. LDB Labordatenbank는 EU 지역 내에 데이터를 저장하는 AI 모델의 선택지를 강조하고 있는 반면, dialog EDV는 안전하고 체계적인 도입 요구 사항에 부합하는 실험실용 소프트웨어를 추진하고 있습니다. 이는 현지 규정 준수 관련 선호도가 공급업체의 포지셔닝에 어떤 영향을 미치는지를 반영하고 있습니다. 따라서 유럽의 LIMS AI 시장에서는 AI 기능과 인프라의 신뢰성, 철저한 문서화, 마찰이 적은 검증 사이의 균형을 잘 맞출 수 있는 공급업체가 높이 평가됩니다. 이러한 균형 덕분에, 규제가 완화된 조사 환경에 비해 도입 속도는 느릴지라도 해당 지역은 상업적으로 중요한 위상을 계속 유지할 것으로 보입니다.

아시아태평양은 LIMS 분야의 AI 시장에서 가장 빠르게 성장하고 있는 지역으로, 2031년까지의 연평균 성장률(CAGR)은 17.36%로 전망됩니다. 이러한 성장은 인도의 제약 산업 확대, 중국과 한국의 유전체학 분야 투자, 일본과 호주의 정밀의료 및 자동화 노력에 힘입어 이루어지고 있습니다. 일본에서 시마즈 코퍼레이션(Shimadzu Corporation)이 추진하는 ‘Autonomous Labo’ 프로젝트는 해당 지역이 AI 지원 실험실 소프트웨어를 도입했을 뿐만 아니라, 장비, 로봇 공학, 최적화된 워크플로우 간의 연계를 강화하고 있음을 보여줍니다. 남미와 중동 및 아프리카는 도입 주기의 초기 단계에 있지만, 두 지역 모두 제약 제조의 성장, 임상 검사의 확대, 의료 디지털화 프로그램으로 인해 수요가 서서히 증가하고 있습니다. 현재 시장 규모는 작지만, 이 지역들에서는 검사실 현대화 계획이 견고한 디지털 인프라와 연계되어 있어, LIMS 분야의 AI 시장에 장기적인 기회를 제공합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the aI in Laboratory Information Management Systems (LIMS) Market size is expected to grow from USD 350 million in 2025 to USD 406.88 million in 2026 and is forecast to reach USD 863.83 million by 2031 at 16.25% CAGR over 2026-2031.

This report is Segmented by AI Capability (Predictive Analytics, Anomaly Detection, Workflow Automation, and More), Component (Platform Software, AI Modules, Services), Deployment (On-Premise, Private Cloud, Saas, Hybrid), Lab Type (Pharma/Biotech, CRO/CDMO, Diagnostics, Biobanks, Academic), and Geography (North America, Europe, and More). Forecasts are in Value (USD).

Global AI In Laboratory Information Management Systems (LIMS) Market Trends and Insights

Embedded AI Copilots for Review-by-Exception and Analyst Productivity

The AI in LIMS market is seeing its fastest near-term pull from copilots that move scientists and analysts away from repetitive review and toward exception handling. That matters because high-volume quality control laboratories still spend large amounts of time searching records, checking deviations, and moving across separate informatics tools. Sapio Sciences integrated Anthropic's Claude Cowork into the Sapio Platform in April 2026, which gave scientists one conversational interface to query, analyze, and act on LIMS and ELN data with traceability and user attribution.

LigoLab also states that its AI agent roadmap supports natural language interaction for laboratory operations, which shows that plain-language access is becoming part of the product baseline rather than a premium add-on. As the copilot layer spreads across the AI in LIMS market, the advantage is likely to shift toward vendors that pair language interfaces with structured laboratory context, auditability, and actionability inside validated workflows. This is also changing buyer expectations, because laboratories no longer want AI that only summarizes records, they want AI that can retrieve the right context and support compliant action inside routine work.

Growing Multi-Omics and High-Throughput Data Complexity

The market is also being pushed forward by the growing volume and diversity of multi-omics and high-throughput laboratory data. Classical LIMS architectures were built to track samples and methods, but they were not designed to harmonize transcriptomic, proteomic, epigenomic, and sequencing outputs at the scale now being generated by national and enterprise research programs. Illumina launched Connected Multiomics v1.1 in February 2026 with AI-guided workflow suggestions learned from expert-created pipelines, which reduced the need for deep bioinformatics knowledge when designing integrated analyses.

Sapio Sciences and Ultima Genomics formed a partnership in September 2025 to combine ultra-high-throughput sequencing with AI-driven LIMS workflows, which reflects growing demand for scalable and traceable multi-omics execution. A 2025 paper in Quantitative Biology found that normalization, imputation, and cross-modality harmonization remain the central barriers in multi-omics integration, which aligns well with the parts of the AI in LIMS market that focus on embedded analytical assistance. Singapore's PRECISE-SG100K program also reported nearly 50,000 whole-genome sequences through a LIMS-mediated cloud pipeline, with AI-driven quality control helping reduce turnaround time by more than 3-fold after workflow optimization.

GxP Validation Burden for AI-Enabled Workflows

The market continues to face resistance from the validation burden tied to regulated laboratory software. Laboratories in pharmaceutical manufacturing and related settings cannot treat AI functions like ordinary user-interface upgrades because these functions can influence review, exception handling, stability interpretation, and release support. The main difficulty is that adaptive or model-driven behavior does not fit as neatly into legacy validation routines that were built for static and deterministic software. That creates slower approval cycles, more documentation work, and more caution from quality teams that do not yet have mature internal governance for AI oversight. The result is that the AI in LIMS market often advances first in lower-risk workflows, while more critical use cases move more slowly into production. This effect is strongest in risk-averse buyers, especially where compliance teams want clearer rules on model monitoring, revalidation triggers, and sustained human review before scaling beyond limited deployments.

Other drivers and restraints analyzed in the detailed report include:

- Smart Lab Automation and Closed-Loop Workflow Orchestration

- Predictive Quality Monitoring and Compliance Automation

- Legacy LIMS, LIS, and Instrument Integration Debt

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Predictive Analytics and Forecasting held 35.16% of the AI in LIMS market share in 2025, which made it the largest capability segment by a clear margin. Its lead reflects the fact that quality control trending, stability modeling, and instrument failure prediction already map to measurable laboratory outcomes such as fewer disruptions and faster review. The AI in LIMS market has favored this capability because supervised models perform well when data histories are large and prediction targets are clearly defined. Waters showed in 2025 that telemetry-based forecasting can shift LC-MS maintenance from reactive interventions to planned action, which supports both uptime and resource efficiency. That makes predictive use cases easier to justify than more open-ended generative use cases, especially in regulated settings where credibility and traceability matter.

Intelligent Workflow Automation and Orchestration is the fastest-growing capability in the AI in LIMS market, with an 18.88% CAGR projected through 2031. Growth is being driven by rising interest in agentic systems that can coordinate steps across LIMS, ELN, instruments, and connected lab devices rather than only generate alerts or summaries. LabVantage Cortex illustrates this direction by embedding agentic AI into the LIMS operating layer so that tasks such as worksheet support, sample management, stability study coordination, and automated monitoring can happen within one platform context. The broader AI in LIMS market is also seeing continued growth in anomaly detection, knowledge retrieval, semantic search, and copilot functions because scientific teams want faster access to context across expanding data estates. Over time, capability selection is likely to favor tools that can combine interpretable prediction, workflow action, and governed deployment rather than offering isolated AI features without operational depth.

AI-Enabled LIMS Platform Software accounted for 65.17% of the AI in LIMS market size in 2025, which shows that buyers still place the highest value on upgrading the core informatics layer. This pattern suggests that AI is being purchased less as a separate bolt-on and more as part of a broader platform refresh that expands contract value and vendor lock-in. In the AI in LIMS industry, that favors suppliers that already control sample records, audit trails, workflow logic, and user permissions because those assets shape how effectively AI can be embedded. Sapio Sciences positioned its platform around conversational interaction across laboratory data, while LabVantage introduced a cloud-native platform that embeds agentic functions into core laboratory operations. Those moves reinforce the idea that platform ownership remains central to long-term value capture.

Services is forecast to expand at 17.12% CAGR through 2031, which makes it the fastest-growing component in the AI in LIMS market. That growth reflects the practical reality that implementation, validation, workflow redesign, and ongoing model governance still require specialist support that many laboratories do not have internally. Service demand is especially strong when organizations are deploying across multiple sites, linking instruments and upstream systems, or trying to maintain clear compliance evidence during rollout. The AI in LIMS market therefore does not behave like a simple software scaling story, because operational success still depends on data preparation, qualification work, user training, and post-deployment oversight. Models, copilots, and analytics modules are gaining traction, but they remain constrained when customers lack clean data structures, validated integration patterns, or clear rules for where AI may influence regulated actions.

Geography Analysis

North America held 38.18% of the AI in LIMS market share in 2025, which kept it as the largest regional contributor. The region benefits from a dense concentration of pharmaceutical manufacturers, CROs, large genomics programs, and established laboratory informatics suppliers. The AI in LIMS market is especially deep in the United States because buyers there combine strong spending capacity with strict expectations around quality, auditability, and workflow control. Large multi-site laboratory networks in the United States and Canada are also pushing standardization projects that make AI-driven harmonization more valuable across distributed testing environments. These factors continue to support the region's lead even as deployment still moves carefully in the most regulated use cases.

Europe remained a significant part of the AI in LIMS market, led by Germany, the United Kingdom, and France. Regional demand is shaped by the need to satisfy both regulated pharmaceutical data controls and strong data protection requirements, which favors architectures with clear residency and governance options. LDB Labordatenbank highlights EU-resident AI model choices, while dialog EDV promotes laboratory software aligned with secure and structured deployment needs, which reflects how local compliance preferences influence vendor positioning. The AI in LIMS market in Europe therefore rewards suppliers that can balance AI functionality with infrastructure confidence, documentation discipline, and lower-friction validation. That balance should keep the region commercially important even if adoption remains more measured than in less regulated research settings.

Asia-Pacific is the fastest-growing geography in the AI in LIMS market, with a 17.36% CAGR projected through 2031. Growth is being supported by pharmaceutical expansion in India, genomics investment in China and South Korea, and precision medicine and automation initiatives in Japan and Australia. Shimadzu's Autonomous Labo work in Japan shows how the region is not only adopting AI-enabled laboratory software but also building tighter links among instruments, robotics, and optimization workflows. South America and the Middle East and Africa are still earlier in the adoption cycle, yet both regions are seeing incremental demand from pharmaceutical manufacturing growth, clinical trial expansion, and healthcare digitalization programs. Even with a smaller current base, these regions add long-term opportunity for the AI in LIMS market where laboratory modernization agendas align with stronger digital infrastructure.

- Agaram Technologies

- Agilent Technologies

- Benchling

- Clinisys

- CloudLIMS

- Dassault Systemes BIOVIA

- Dotmatics

- eLabNext

- Illumina

- L7 Informatics

- Labguru

- LabLynx

- LabVantage Solutions

- LabWare

- QBench

- Revvity Signals

- Sapio Sciences

- Scispot

- STARLIMS Corporation

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Embedded AI Copilots for Review-By-Exception and Analyst Productivity

- 4.2.2 Cloud-Native LIMS Modernization for AI-Ready Data Workflows

- 4.2.3 Growing Multi-Omics and High-Throughput Data Complexity

- 4.2.4 Smart Lab Automation and Closed-Loop Workflow Orchestration

- 4.2.5 Predictive Quality Monitoring and Compliance Automation

- 4.2.6 Multi-Site Standardization Across Pharma, CRO, and Diagnostics Networks

- 4.3 Market Restraints

- 4.3.1 GxP Validation Burden for AI-Enabled Workflows

- 4.3.2 Legacy LIMS, LIS, and Instrument Integration Debt

- 4.3.3 Weak Metadata Provenance and Model Drift Risk

- 4.3.4 Restricted Use of Adaptive and Generative AI in Regulated Decisions

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By AI Capability

- 5.1.1 Predictive Analytics and Forecasting

- 5.1.2 Anomaly Detection and Review-by-Exception

- 5.1.3 Generative AI Copilots and Natural Language Assistance

- 5.1.4 Intelligent Workflow Automation and Orchestration

- 5.1.5 Knowledge Retrieval and Semantic Search

- 5.1.6 Quality Signal Detection and Risk Scoring

- 5.2 By Component

- 5.2.1 AI-Enabled LIMS Platform Software

- 5.2.2 AI Models, Copilots, and Analytics Modules

- 5.2.3 Services

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Private Cloud / Single-Tenant

- 5.3.3 Public Cloud / Multi-Tenant SaaS

- 5.3.4 Hybrid

- 5.4 By Laboratory Type

- 5.4.1 Pharmaceutical and Biotechnology Laboratories

- 5.4.2 CROs and CDMOs

- 5.4.3 Clinical Diagnostics and Molecular Laboratories

- 5.4.4 Biobanks and Genomics Laboratories

- 5.4.5 Academic and Translational Research Laboratories

- 5.4.6 Other Laboratories

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Agaram Technologies

- 6.3.2 Agilent Technologies

- 6.3.3 Benchling

- 6.3.4 Clinisys

- 6.3.5 CloudLIMS

- 6.3.6 Dassault Systemes BIOVIA

- 6.3.7 Dotmatics

- 6.3.8 eLabNext

- 6.3.9 Illumina

- 6.3.10 L7 Informatics

- 6.3.11 Labguru

- 6.3.12 LabLynx

- 6.3.13 LabVantage Solutions

- 6.3.14 LabWare

- 6.3.15 QBench

- 6.3.16 Revvity Signals

- 6.3.17 Sapio Sciences

- 6.3.18 Scispot

- 6.3.19 STARLIMS Corporation

- 6.3.20 Thermo Fisher Scientific

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment