|

시장보고서

상품코드

2063980

직접 급여 미생물(DFM) 시장: 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Direct-Fed Microbials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

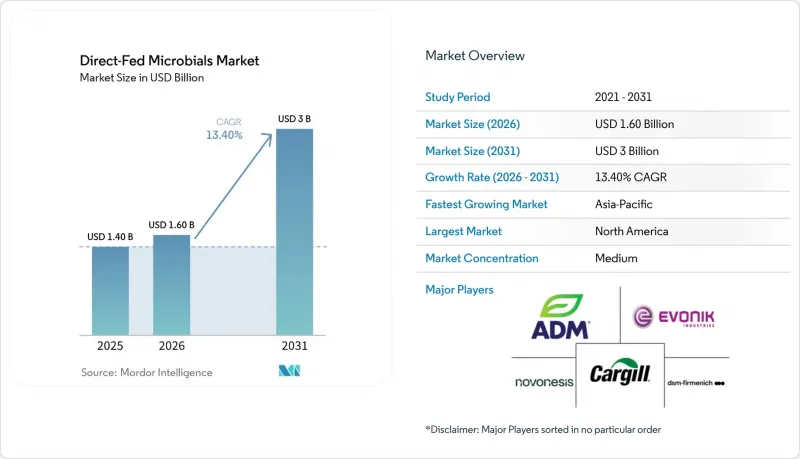

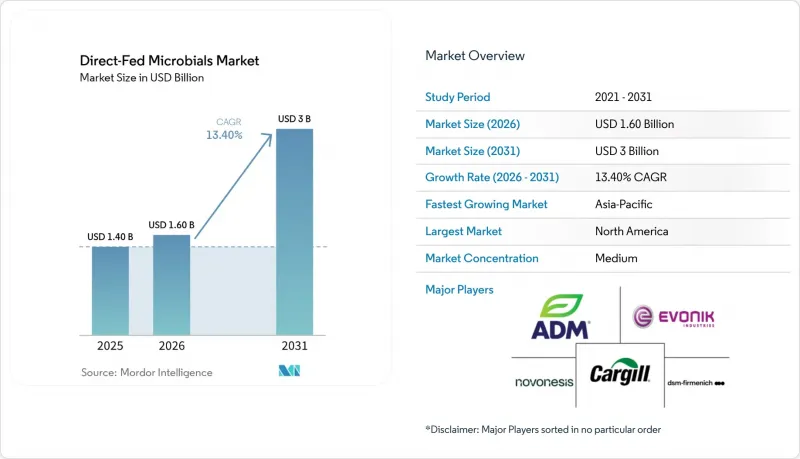

Mordor Intelligence에 의하면, 직접 급여 미생물 시장 규모는 2025년에 14억 달러로 평가되었고, 2026년에 16억 달러로 추정되며, 2031년까지 30억 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 13.40%로 성장할 것으로 전망됩니다.

본 보고서는 제품 유형별(유산균, 바실러스, 기타), 가축별(가금류, 돼지, 소, 수산 양식, 기타), 형태별(건조, 액상) 및 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 직접 급여 미생물 시장 동향 및 인사이트

항생제를 사용하지 않은 동물성 단백질에 대한 수요의 급증

가금류 생산 시스템에서 항생제 사용량이 꾸준히 감소하고 있는 것으로 보아, 항생제를 사용하지 않는 동물성 단백질 생산으로의 뚜렷한 전환이 나타나고 있습니다. 미국 가금류 및 계란 협회(US Poultry and Egg Association)의 ‘항생제 적정 사용 보고서(2025년)’에 따르면, 지난 10년 동안 미국 육계 중 부화장에서 항생제를 투여받는 비율은 약 90%에서 2024년에는 1% 미만으로 감소했습니다. 국내 생산의 대부분을 대상으로 한 종합적인 분석을 바탕으로 한 이 데이터는 특히 북미에서 상업적 가금류 사육 과정에서 항생제의 일상적인 사용이 사실상 중단되었음을 뒷받침하고 있습니다. 그 결과, 생산자들은 동물의 건강 유지, 사료 효율 향상, 그리고 변화하는 소매업체와 소비자의 요구에 부응하기 위해 직접 급여 미생물 등의 대체 수단에 대한 의존도를 높이고 있습니다.

항생제를 이용한 성장 촉진제에 대한 엄격한 규제

축산업에서 항생제 사용에 대한 엄격한 규제가 대체 사료 솔루션으로의 전환을 촉진하고 있습니다. 미국 식품의약국(2024년)에 따르면, 가축용 의학적으로 중요한 항생제는 모두 현재 ‘수의사 처방 사료 지침(VFD)’에 따라 수의사의 승인이 필요합니다. 이러한 규제 변경으로 인해 일상적 및 예방적 항생제 사용이 대폭 제한되었으며, 생산자에 대한 규정 준수 요건이 강화되었습니다. 그 결과, 가축 사육 농가들은 규제 기준을 충족하면서 동물의 건강 유지, 장 기능 향상, 생산성 유지를 도모하기 위해 직접 급여 미생물 등의 대체 수단을 도입하고 있습니다.

농장 환경에 따른 제품 효과의 편차

실제 농장 환경에서 나타나는 효과의 편차는 직접 급여 미생물의 도입에 있어 여전히 큰 과제로 남아 있습니다. 유럽식품안전청(2024년)은 사료 첨가제의 유효성은 특정 동물 종 및 사용 조건에 맞추어 설계된 여러 대조 시험을 통해 입증되어야 하며, 이때 명확하게 정의된 축산 기술적 매개변수와 시험 요건이 필요하다고 밝혔습니다. 이는 결과가 실험 설계나 운영 조건에 크게 좌우된다는 것을 보여주며, 다양한 농장 환경에서 결과를 재현하기 어렵다는 점을 시사합니다. 관리 기법, 사료 조성, 생물안전 대책 및 환경 조건의 편차가 농장별 결과의 편차를 초래하는 요인 중 하나이며, 이는 광범위한 도입을 저해하고 신뢰할 수 있는 성능 결과를 기대하는 생산자들 사이에서 신뢰를 떨어뜨리고 있습니다.

부문별 분석

2025년 기준으로 유산균은 직접 급여 미생물(DFM) 시장 점유율 43%를 차지해 가장 큰 비중을 차지했습니다. 이러한 우위는 강력한 정착 효율과, 장내 미생물 군집의 신속한 안정화가 필수적인 가금류 및 돼지 사육 시스템과의 적합성에서 비롯됩니다. 이러한 균주는 소화 기능에 대한 효과가 입증되었으며, 배합이 용이하기 때문에 사료 프리믹스에 널리 사용되고 있습니다. 마이크로캡슐화 및 공과립화와 같은 안정화 기술의 혁신으로 인해 사료 가공 공정에서의 생존율이 향상되고 있습니다. 이러한 발전 덕분에 제조업체들은 펠릿화 공정에서 발생하는 열 민감성 문제를 해결하면서도 효능을 유지할 수 있게 되었습니다.

바실러스 속은 2026-2031년 연평균 성장률(CAGR) 15.2%라는 가장 높은 성장률을 보일 것으로 예측됩니다. 이러한 성장은 뛰어난 내열성에 힘입은 것으로, 포자는 생존 능력을 잃지 않은 채 고온의 펠릿화 공정을 견딜 수 있습니다. 또한, 바실러스 균주는 프로테아제나 셀룰라제 등의 효소를 생성하여 다양한 가축 종에서 영양소의 분해를 촉진하고 사료 효율을 향상시킵니다. 가금류, 돼지, 수산 양식 시스템에서 그 범용성 덕분에 도입이 확대되고 있습니다. 균주 공학의 발전과 다중 균주 배합의 개발로 인해 성능의 일관성이 더욱 향상되었으며, 바실러스 균을 기반으로 한 솔루션은 산업 규모의 사료 생산에서 선호되는 선택지가 되고 있습니다.

지역별 분석

2025년, 북미는 직접 급여 미생물 시장에서 32%로 가장 높은 점유율을 차지했습니다. 이는 견고한 규제 체계와 항생제를 사용하지 않는 생산 시스템의 광범위한 도입에 힘입은 결과입니다. 이 지역의 축산업에서는 규제 요건을 준수하면서도 생산성을 유지하기 위해 미생물 솔루션을 일상적인 사료 전략에 도입하고 있습니다. 첨단 사료 생산 인프라에 힘입어 대규모 가금류 및 돼지 사육 사업이 계속해서 수요를 주도하고 있습니다. 동물의 건강과 생산성 최적화에 대한 관심이 높아지면서, 도입이 더욱 가속화되고 있습니다. 확립된 유통 네트워크와 강력한 조사 지원을 통해 지역 전체에서 일관된 제품 검증과 상품화가 촉진되고 있습니다.

아시아태평양은 가축 사육의 급속한 확대와 항생제 사용을 제한하는 규제 변경에 힘입어, 2026-2031년 14.8%라는 가장 높은 연평균 성장률(CAGR)을 기록하며 성장할 것으로 전망됩니다. 중국이나 인도 등에서는 사료 효율을 높이고 대규모 생산 시스템을 뒷받침하기 위해 미생물 사료 솔루션의 도입이 점점 더 확대되고 있습니다. 수산물 양식 생산량 증가와 수출 지향적 요인이 미생물 기반 사료 첨가제의 도입을 가속화하고 있습니다. 상업적 축산 사업의 확대와 항생제 대체 수단에 대한 인식 제고가 지역 성장을 더욱 촉진하며, 다양한 가축 부문에서 미생물 솔루션에 대한 수요를 끌어올리고 있습니다.

사료 첨가물에 관한 유럽의 고도로 체계화된 규제 체계는 축산 시스템 내 미생물 기반 솔루션의 도입을 주도하고 있습니다. 이 지역의 생산자들은 사료에 사용할 때 일관된 성능과 안전성을 확보하기 위해, 과학적으로 검증되고 규정을 준수하는 제품을 우선적으로 선택하고 있습니다. 이러한 엄격한 규제는 특히 젖소와 돼지 사육 분야에서 확립된 품질 및 유효성 기준을 충족하는 직접 급여 미생물(DFM)의 사용을 촉진하고 있습니다. 남미에서는 수출 지향적인 축산업이 확대되고 있으며, 중동 및 아프리카에서는 사료 인프라가 점차 강화되고 있습니다. 이러한 동향은 지역 전체에 걸쳐 미생물 사료 솔루션의 보급을 촉진하고, 직접 급여 미생물 시장의 세계적 성장에 기여하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the direct-fed microbials market size is projected to be USD 1.40 billion in 2025, USD 1.60 billion in 2026, and reach USD 3.00 billion by 2031, growing at a CAGR of 13.40% from 2026 to 2031.

This report is Segmented by Product Type (Lactic Acid Bacteria, Bacillus, and Others), by Livestock (Poultry, Swine, Cattle, Aquaculture, and Others), by Form (Dry and Liquid), and by Geography (North America, South America, Europe, Asia-Pacific, The Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Direct-Fed Microbials Market Trends and Insights

Surging Demand for Antibiotic-free Animal Protein

A notable shift toward antibiotic-free animal protein production is evident from the consistent decline in antibiotic usage within poultry systems. The United States Poultry and Egg Association Antibiotic Stewardship Report (2025) indicates that the percentage of broiler chickens in the United States receiving antibiotics at hatcheries has decreased from approximately 90% to less than 1% in 2024 over the past decade . This data, derived from a comprehensive analysis of the majority of national production, underscores the near elimination of routine antibiotic use in commercial poultry production, particularly in North America. Consequently, producers are increasingly relying on alternatives such as direct-fed microbials to support animal health, enhance feed efficiency, and meet evolving retailer and consumer demands.

Stringent Regulations on Antibiotic Growth Promoters

Stringent regulations on antibiotic usage in livestock production are driving a shift toward alternative feed solutions. According to the United States Food and Drug Administration (2024), all medically important antibiotics for livestock now require veterinary authorization under the Veterinary Feed Directive (VFD) . These regulatory changes significantly limit routine and prophylactic antibiotic use, increasing compliance requirements for producers. Consequently, livestock operators are adopting alternatives such as direct-fed microbials to support animal health, enhance gut function, and maintain productivity while meeting regulatory standards.

Variable Product Efficacy Across Farm Conditions

Inconsistent performance in real-world farming environments remains a significant challenge for the adoption of direct-fed microbials. The European Food Safety Authority (2024) states that the efficacy of feed additives must be demonstrated through multiple controlled studies designed for specific animal species and conditions of use, with clearly defined zootechnical parameters and trial requirements. This highlights that outcomes are heavily influenced by trial design and operational conditions, making it challenging to replicate results across diverse farm settings. Variations in management practices, feed composition, biosecurity measures, and environmental conditions contribute to inconsistent on-farm results, limiting widespread adoption and reducing confidence among producers seeking reliable performance outcomes.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Commercial Poultry and Swine Industries

- Shift Toward Functional Feed Additives Focusing on Gut Health

- Higher Cost Versus Conventional Feed Additives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lactic acid bacteria accounted for the largest 43% of the direct-fed microbials market share in 2025. Their dominance is attributed to their strong colonization efficiency and compatibility with poultry and swine systems, where rapid stabilization of gut microbiota is essential. These strains are commonly used in feed premixes due to their proven digestive benefits and ease of formulation. Innovations in stabilization techniques, such as microencapsulation and co-granulation, are enhancing survivability during feed processing. These advancements enable manufacturers to maintain efficacy while addressing thermal-sensitivity challenges during pelleting operations.

Bacillus is projected to grow at the fastest 15.2% CAGR from 2026 to 2031. This growth is driven by its superior thermal resistance, allowing spores to withstand high-temperature pelleting processes without losing viability. Bacillus strains also produce enzymes such as protease and cellulase, which improve nutrient breakdown and feed efficiency across various livestock categories. Their versatility in poultry, swine, and aquaculture systems supports increasing adoption. Advancements in strain engineering and the development of multi-strain combinations are further enhancing performance consistency, making Bacillus-based solutions a preferred choice for industrial-scale feed production.

Geography Analysis

North America accounted for the largest 32% of the direct-fed microbials market share in 2025, driven by robust regulatory frameworks and the widespread adoption of antibiotic-free production systems. The region's livestock industry has incorporated microbial solutions into routine feed strategies to maintain productivity while adhering to regulatory requirements. Large-scale poultry and swine operations continue to fuel demand, supported by advanced feed manufacturing infrastructure. The increasing emphasis on animal health and performance optimization further strengthens adoption. Established distribution networks and strong research support facilitate consistent product validation and commercialization across the region.

The Asia-Pacific region is projected to grow at the fastest CAGR of 14.8% from 2026 to 2031, driven by rapid livestock expansion and regulatory changes restricting antibiotic use. Countries such as China and India are increasingly adopting microbial feed solutions to enhance feed efficiency and support large-scale production systems. Rising aquaculture production and export-oriented requirements are accelerating the adoption of microbial-based feed additives. The expansion of commercial farming operations and the growing awareness of antibiotic alternatives further drive regional growth, boosting demand for microbial solutions across various livestock segments.

Europe's highly structured regulatory framework for feed additives is shaping the adoption of microbial-based solutions in livestock systems. Producers in the region prioritize products that are scientifically validated and compliant to ensure consistent performance and safety in feed applications. This regulatory rigor promotes the use of direct-fed microbials that meet established quality and efficacy standards, particularly in dairy and swine production. South America is expanding its export-oriented livestock production, while the Middle East and Africa are gradually strengthening their feed infrastructure. These developments collectively support the broader regional adoption of microbial feed solutions, contributing to the global growth of the direct-fed microbials market.

- Archer-Daniels-Midland Company

- Novonesis A/S

- DSM-Firmenich AG

- International Flavors & Fragrances Inc.

- Lallemand Inc.

- Kemin Industries, Inc.

- Evonik Industries AG

- Cargill, Incorporated

- Bio-Vet, Inc.

- Huvepharma EOOD

- Provita Eurotech Limited

- Asahi Biocycle Co., Ltd.

- Synbio Tech Inc.

- Phibro Animal Health Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for antibiotic-free animal protein

- 4.2.2 Stringent regulations on antibiotic growth promoters

- 4.2.3 Rapid expansion of commercial poultry and swine industries

- 4.2.4 Shift toward functional feed additives focusing on gut health

- 4.2.5 Heat-stable spore-forming probiotic strains enabling pelleted feed

- 4.2.6 On-farm precision dosing systems integrating live microbials

- 4.3 Market Restraints

- 4.3.1 Variable product efficacy across farm conditions

- 4.3.2 Higher cost versus conventional feed additives

- 4.3.3 Supply-chain bottlenecks for freeze-dried cultures

- 4.3.4 Regulatory uncertainty for engineered microbial strains

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Lactic Acid Bacteria

- 5.1.2 Bacillus

- 5.1.3 Others

- 5.2 By Livestock

- 5.2.1 Poultry

- 5.2.2 Swine

- 5.2.3 Cattle

- 5.2.4 Aquaculture

- 5.2.5 Others

- 5.3 By Form

- 5.3.1 Dry

- 5.3.2 Liquid

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 United Kingdom

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Archer-Daniels-Midland Company

- 6.4.2 Novonesis A/S

- 6.4.3 DSM-Firmenich AG

- 6.4.4 International Flavors & Fragrances Inc.

- 6.4.5 Lallemand Inc.

- 6.4.6 Kemin Industries, Inc.

- 6.4.7 Evonik Industries AG

- 6.4.8 Cargill, Incorporated

- 6.4.9 Bio-Vet, Inc.

- 6.4.10 Huvepharma EOOD

- 6.4.11 Provita Eurotech Limited

- 6.4.12 Asahi Biocycle Co., Ltd.

- 6.4.13 Synbio Tech Inc.

- 6.4.14 Phibro Animal Health Corporation