|

시장보고서

상품코드

2063990

포도 수확기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Grape Harvesting Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

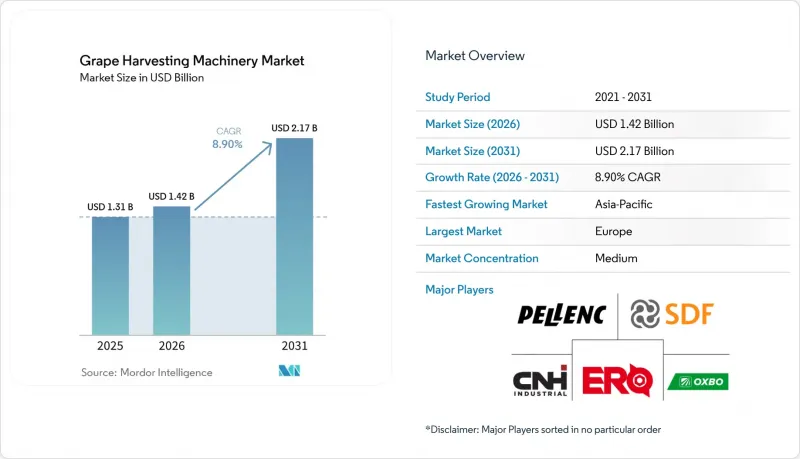

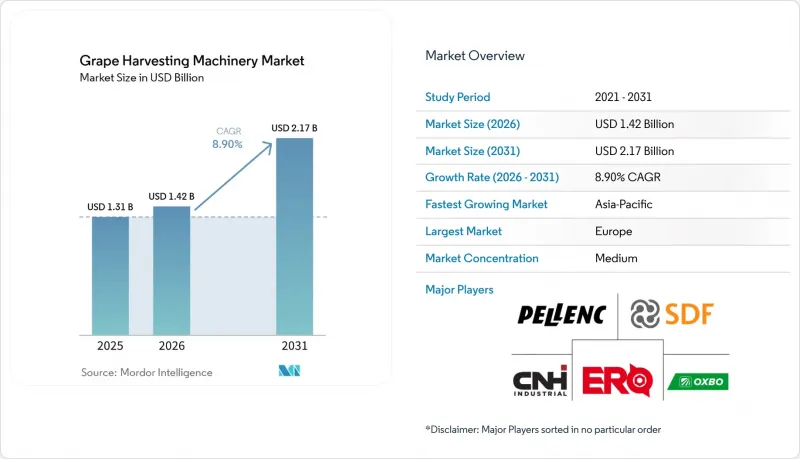

Mordor Intelligence에 의하면, 포도 수확기 시장 규모는 2025년 13억 1,000만 달러로 평가되었고, 2026년에는 14억 2,000만 달러로 추정되고, 2031년까지 21억 7,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 8.9%로 성장할 전망입니다.

본 보고서는 수확기 유형별(자주식, 견인식, 기타), 운용 모드별(수동, 보조식, 정밀 유도식, 기타), 동력원별(디젤, 하이브리드, 전기), 포도원 규모별(소규모 포도원(50헥타르 미만) 등), 지역별(북미, 남미, 유럽 등)로 분류되어 있습니다. 시장 전망치는 달러 기준 금액으로 제시되어 있습니다.

세계의 포도 수확기 시장 동향 및 분석

인력 부족으로 인한 기계화의 급증

포도원 운영에 따른 인력 부족은 주요 와인 생산 지역 전반에 걸쳐 뿌리 깊은 과제로 대두되고 있으며, 이는 기계화된 포도 수확 솔루션의 도입을 촉진하고 있습니다. 미국 농무부(USDA)는 2025년에 H-2A 비자 승인 건수가 증가했으며, 임금 상승률이 다른 농업 부문을 상회했다고 보고했습니다. 호주에서는 2025년, 계약 수확 비용이 시간당 345달러(525 호주 달러)에 달했고, 수작업 수확 비용을 크게 웃돌게 되자, 자동 수확기 구매가 가속화되었습니다. 독일에서는 2025년 수확량이 인력 부족으로 인해 지난 10년간의 평균보다 16% 감소했으며, 이는 전통적인 와이너리들이 기계화를 단행하는 계기가 되었습니다. 미국 캘리포니아주 나파 밸리의 고급 와이너리에서는 인력 부족 문제를 해결하고 과일의 산도를 유지하기 위해 2025년에 야간 기계 수확을 도입했습니다. 인건비가 포도 가격 상승률을 웃도는 상황에서 수익성을 확보하기 위해서는 자동화 솔루션이 필수적입니다.

대규모 생산자 간의 포도원 통합

통합에 따라 수요는 수천 명의 소규모 소유주에서 소수의 자본 집약적인 구매자로 이동하고 있습니다. 미국에서는 2025년 6월, 와인 그룹이 콘스텔레이션 브랜즈로부터 6,600에이커를 인수하면서 기계화 수확기 수요를 확대시켰습니다. 또한, 미국 캘리포니아주에 본사를 둔 아틀라스 빈야드 매니지먼트는 같은 달 미국 오리건주에 거점을 둔 리잘츠 파트너스를 인수했습니다. 이번 인수를 통해 오리건주 내 관리 면적이 9,000에이커로 확대되어, 여러 대의 수확기를 계약하는 것이 용이해졌습니다. 대규모 와이너리들은 브랜드 표준화에 주력하고 있으며, 통일된 데이터 인터페이스가 필요하고, 계절적 인력 수요를 줄이기 위해 자율 주행 기능 도입을 추진하고 있습니다. 합병이 진행됨에 따라 수주량은 첨단 센서를 탑재한 대용량 플랫폼에 점점 더 집중되고 있습니다.

막대한 초기 투자

막대한 초기 투자가 필요하기 때문에 특히 소규모로 세분화된 포도원 경영자들에게는 수확 기계 도입이 어려운 실정입니다. 초급형 자가주행 수확기는 약 8만 달러이지만, 고급 모델은 40만 달러를 초과하기 때문에 소규모 생산자들에게는 구입하기 어려운 실정입니다. 유럽에서는 포도밭의 절반 이상이 1헥타르 미만의 규모이며, 보조금 제도가 있음에도 불구하고 기계 이용률과 투자 수익률은 여전히 낮은 수준에 머물러 있습니다. 미국 캘리포니아주나 호주 등 기계화가 진전된 시장을 제외한 많은 지역에서는 임대 및 도급 서비스가 미비하기 때문에 도입이 더욱 더딘 임베디드니다. 높은 비용과 자금 조달의 제약으로 인해, 특히 소규모 포도밭이나 전통적인 와인 산지에서는 기계화 수확기의 사용이 여전히 제한되고 있습니다.

부문별 분석

2025년, 자가주행 기계는 포도 수확기 시장 점유율의 48.5%를 차지했으며, 200헥타르가 넘는 농장에서의 생산성 우위를 반영하고 있습니다. 2026-2031년 포도 수확기 시장 규모에서 트랙터 탑재형 유닛이 11.8%라는 가장 높은 연평균 성장률(CAGR)을 기록할 전망입니다. 이는 생산자가 기존의 마력을 활용하고 있기 때문입니다. 견인식으로 설계된 수확기는 현재 다양한 농장에서 활용되고 있으며, 여러 작물에 걸쳐 기계를 순환 투입할 수 있게 함으로써 포도 이외의 용도로도 그 유용성을 넓혀가고 있습니다. Pellenc OPTIMUM XXL80과 같은 대용량 자가 주행 모델에는 주행할 때마다 수확량 데이터를 기록하고 업로드하는 텔레메트리 기능이 탑재되어 있습니다. 한편, 고급 와이너리에서는 트랙터를 이용한 토양 다짐 작업을 줄이고 세척 모듈을 강화할 수 있다는 점을 높이 평가하여, 계속해서 자가주행식 기계를 선호하고 있습니다.

트랙터 탑재형 유닛의 급증에 박차를 가하고 있는 것은 자본 효율성에 대한 집중입니다. GREGOIRE를 비롯한 포도원용 장비 제조업체들은 ISOBUS를 지원하는 트랙터 탑재형 플랫폼을 통해 제품 라인업을 확대되고 있습니다. 이러한 플랫폼은 정밀 농업 및 디지털 모니터링에 대한 요구를 충족시킬 뿐만 아니라, 소유 비용 절감도 실현합니다. 각 제조업체들은 다양한 구성에 대응할 수 있는 모듈식 플랫폼과 호환성이 뛰어난 셰이커 기술에 주력하고 있습니다.

2025년에는 인간의 감시 기능을 보완하는 GPS 조향 시스템과 카메라 선별기를 통해 보조형 및 정밀 유도형 수확기가 54.2%라는 가장 높은 점유율을 차지했습니다. 수동식 기계는 유럽의 노후화된 장비군에 여전히 남아 있지만, 포도 수확기 시장 전체의 3분의 1 미만을 차지하는 데 그치고 있습니다. 자율형 및 반자율형 운영은 2026-2031년 연평균 성장률(CAGR) 13.2%라는 가장 높은 성장세를 보일 것으로 예측됩니다. 이는 수작업에 대한 의존도를 낮추는 센서 통합 시스템의 도입 확대가 원동력이 되고 있습니다. 2024년 2월, 호주 듀크스턴 빈야드(Duxton Vineyards)에서 실시된 시험에서 자율 주행 트랙터가 수관 데이터를 수확기의 제어 시스템에 효율적으로 전송하여 수확기를 최적의 경로로 유도할 수 있음이 입증되었습니다. 한편, 규제 체계도 변화하고 있어, 지오펜스가 설정된 사유지에서 무인 주행이 점차 허용되고 있습니다.

이러한 유망한 전망이 있는 반면, 전환 비용이 도입의 큰 걸림돌이 되고 있습니다. 자율 주행 시스템은 운전자 보조 시스템에 비해 가격이 비쌉니다. 그러나 캘리포니아주의 초과근무 수당을 고려하면, 24시간 무인 운행은 경제적으로 매력적입니다. 유럽연합(EU)에서는 엄격한 데이터 개인정보 보호 규정에 따라 안전한 클라우드 서비스 이용이 의무화되어 있습니다. 이에 따라 OEM(원청 브랜드 제조업체)은 지역별로 데이터센터를 구축하고 있습니다. 또한, 구매를 검토 중인 기업들은 구매를 결정하기 전에 배상책임보험료를 중요한 요소로 고려하고 있습니다.

지역별 분석

2025년, 유럽은 포도 수확기 시장에서 37.1%라는 압도적인 점유율을 차지했습니다. 이는 프랑스, 이탈리아, 스페인의 높은 기계화 수준에 힘입은 결과입니다. 이 지역은 연간 공동농업정책(CAP)을 통해 11억 2,000만 달러(10억 6,100만 유로)라는 막대한 자금을 지원받고 있으며, 주요 와인 생산 지역에서의 차량 교체 및 정밀 농업 추진이 강조되고 있습니다. 기후 변화의 영향을 여실히 드러내는 가운데, 2025년 독일의 수확량 감소는 전통적으로 보수적이었던 독일의 포도원 경영자들이 기계화 수확을 도입하도록 부추겼습니다. 근대화를 추진하기 위해 이탈리아는 2026년에 포도원 재편에 1억 5,200만 달러(1억 4,410만 유로)를 배정하고, 수확기 현대화에 중점을 두고 있습니다. 유서 깊은 제조업체들이 주도하는 유럽 시장에서는 특히 고급 포도원이나 알프스의 계단식 포도밭에서 경작할 때, 경량화되고 디지털 기술이 발전했으며 연비 효율이 뛰어난 수확기에 대한 수요가 뚜렷하게 증가하고 있습니다.

아시아태평양에서는 2026-2031년 포도 수확기 시장이 연평균 성장률(CAGR) 9.4%라는 견조한 성장세를 보일 것으로 예측됩니다. 중국에서는 닝샤(寧夏)의 와이너리들이 국내 와인 생산량 감소에 대응하기 위해, 기계 도입 비용을 경감해 주는 지역 보조금을 바탕으로 운영의 현대화를 추진하고 있습니다. 호주에서는 인건비 급등으로 인해 2025년에는 기계 대여료가 시간당 약 345달러에 달할 것으로 예상에 따라, 대규모 포도원들이 자율형 수확기의 시범 도입을 서두르고 있습니다. 한편, 인도에서는 마하라슈트라 주 정부가 기계화 보조금 대상에 포도 수확기도 포함시켰으며, 이는 신생 상업용 포도원에서 기계화에 대한 수용도가 높아지고 있음을 보여줍니다.

북미에서는 주요 와인 생산 주에서 포도원 통합이 진행되고 있는 것을 배경으로, 대용량 포도 수확기에 대한 수요가 급증하고 있습니다. 더 와인 그룹이 2025년에 6,600에이커에 달하는 광대한 포도원을 인수한 사례 등 주목할 만한 인수 사례들이, 노동력에 대한 의존도를 낮추는 효율적인 수확기 도입의 길을 열어주고 있습니다. 동시에, 각 제조업체들은 지역별 공급망을 강화하고, 애프터마켓 서비스를 확충하고 있습니다. 그 대표적인 예가 옥스보사의 뉴욕 지사입니다. 이 회사는 종종 간과되기 쉬운 동부 해안의 포도원에 대해 부품 조달의 편의성과 서비스 신속성을 높이고 있습니다. 남미에서는 칠레와 아르헨티나의 와인 생산자들이 모두 기계화에 대한 투자를 확대되고 있습니다. 그 목적은 생산 비용 절감, 안정적인 수확 확보, 그리고 특히 인건비 급등을 고려한 수출 경쟁력 강화에 있습니다. 한편, 도입이 아직 초기 단계에 있는 중동 및 아프리카에서는 선택적인 기계화가 진행되고 있습니다. 남아프리카의 서케이프 지역이나 튀르키예의 트라키아 지역 등, 여전히 노동력에 대한 의존도가 높은 지역에서는 상업용 포도원이 현대적인 수확 장비에 대한 투자를 확대하며, 업무 효율 향상과 수출 품질 유지를 목표로 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the grape harvesting machinery market size is anticipated to increase from USD 1.31 billion in 2025 to USD 1.42 billion in 2026 and reach USD 2.17 billion by 2031, growing at a CAGR of 8.9% during 2026-2031.

This report is Segmented by Harvester Type (Self-Propelled, Trailed or Towed, and More), by Mode of Operation (Manual, Assisted or Precision-Guided, and More), by Power Source (Diesel, Hybrid, and Electric), by Vineyard Size ( Small Vineyards (Below 50 Hectares), and More), and by Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value in USD.

Global Grape Harvesting Machinery Market Trends and Insights

Labor-Shortage Driven Mechanization Surge

Labor shortages in vineyard operations are becoming a persistent challenge across major wine-producing regions, driving the adoption of mechanized grape harvesting solutions. The United States Department of Agriculture (USDA) reported rising H-2A certifications in 2025 and wage inflation that outpaced other farm sectors. Australia experienced contract-harvesting fees of USD 345 (AUD 525) per hour in 2025, dwarfing hand-picking costs and accelerating the purchase of automated pickers. Germany's 2025 harvest fell 16% below the ten-year average due to crew shortages, prompting traditional estates to turn to machinery. Premium properties in Napa Valley, California, United States, adopted night mechanical picking in 2025 to address labor shortages and maintain fruit acidity. With labor costs rising faster than grape prices, automated solutions have become critical to ensuring profitability.

Vineyard Consolidation Among Large Producers

Consolidation shifts demand from thousands of small owners to a few capital-intensive buyers. In the United States, the Wine Group acquired 6,600 acres from Constellation Brands in June 2025, expanding its mechanized fleet requirement . Atlas Vineyard Management, headquartered in California, United States, acquired Results Partners, based in Oregon, United States, during the same month. This acquisition expanded its managed acreage in Oregon to 9,000, facilitating multi-unit harvester contracts. Larger estates are focusing on standardizing brands, requiring uniform data interfaces, and advocating for autonomous features to mitigate seasonal labor demands. As mergers progress, order volumes are increasingly concentrated on high-capacity platforms equipped with advanced sensors.

High Upfront Capital Expenditure

High capital requirements hinder the adoption of grape harvesting machinery, especially for small, fragmented vineyard operators. Entry-level self-propelled harvesters cost around USD 80,000, while advanced models exceed USD 400,000, limiting affordability for small-scale growers. In Europe, where over half of vineyards span less than 1 hectare, low machinery utilization and return on investment persist despite subsidy programs. Underdeveloped rental and contractor-based services in many regions outside mechanized markets, such as California, the United States, and Australia, further slow adoption. High costs and limited financing continue to restrict the use of mechanized harvesters, particularly in smaller vineyards and traditional wine regions.

Other drivers and restraints analyzed in the detailed report include:

- Government Mechanization Subsidies and Tax Credits

- Precision-Viticulture Adoption Requiring Data-Ready Machinery

- Operator-Skill and Maintenance Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Self-propelled machines captured 48.5% of the grape harvesting machinery market share in 2025, reflecting productivity advantages for estates above 200 hectares. Tractor-mounted units posted the fastest 11.8% CAGR over 2026-2031 in the grape harvesting machinery market size as growers leverage existing horsepower. Harvesters designed for trailing are now serving a diverse range of farms, enabling equipment rotation across various crops and broadening their utility beyond grapes. High-capacity self-propelled models, such as the Pellenc OPTIMUM XXL80, come equipped with telemetry features that record and upload yield data with every pass. Meanwhile, premium wineries continue to favor self-propelled machines, valuing their ability to reduce tractor compaction and enhance cleaning modules.

Driving the surge in tractor-mounted units is a focus on capital efficiency. Manufacturers, including GREGOIRE and other vineyard equipment providers, are broadening their offerings with ISOBUS-compatible tractor-mounted platforms. These platforms not only align with precision agriculture and digital monitoring needs but also offer lower ownership costs. Manufacturers are focusing on modular platforms and interchangeable shaker technologies compatible with various configurations.

Assisted and precision-guided harvesters held the largest share, 54.2%, in 2025, driven by GPS steering and camera sorters that augment human oversight. Manual machines linger in aging European fleets, yet account for less than one-third of the grape harvesting machinery market. Autonomous/Semi-Autonomous operations are projected to register the fastest CAGR of 13.2% during 2026-2031, driven by increasing adoption of sensor-integrated systems that reduce dependence on manual labor. In February 2024, trials at Duxton Vineyards in Australia demonstrated that autonomous tractors can efficiently transmit canopy data to harvester controls, guiding pickers along optimal paths. Meanwhile, regulatory frameworks are adapting to authorize driverless operations on geofenced private lands.

Despite the promise, transition costs pose a significant barrier to adoption. Autonomous systems come with a higher price tag than their assisted counterparts. Yet, California's overtime premiums render round-the-clock driverless operations financially appealing. In the European Union, stringent data privacy regulations mandate the use of secure cloud services. This has prompted Original Equipment Manufacturers (OEMs) to set up regional data centers. Furthermore, potential buyers are weighing liability insurance premiums as a crucial factor before finalizing their purchases.

Geography Analysis

In 2025, Europe commanded a dominant 37.1% share of the grape harvesting machinery market, bolstered by advanced mechanization in France, Italy, and Spain. The region benefited from robust funding of USD 1.12 billion (EUR 1.061 billion) from the Annual Common Agricultural Policy, underscoring its commitment to fleet renewal and precision agriculture in key wine-producing areas. Highlighting the impact of climate volatility, Germany's 2025 crop shortfall nudged its traditionally conservative vineyard estates towards embracing mechanized harvesting. In a bid to modernize, Italy earmarked USD 152 million (EUR 144.1 million) for vineyard restructuring in 2026, with a focus on harvester upgrades. The European market, dominated by established manufacturers, is witnessing a pronounced shift in demand towards lightweight, digitally advanced, and fuel-efficient harvesting units, particularly for premium vineyards and Alpine terrace cultivation.

Asia-Pacific is set to witness a robust 9.4% CAGR in the grapes harvesting machinery market between 2026 and 2031. In China, Ningxia estates are modernizing their operations to counteract a dip in national wine output, bolstered by regional subsidies that ease machinery costs. In Australia, wage pressures have driven machinery hire rates to nearly USD 345 per hour in 2025, spurring large vineyard estates to accelerate trials of autonomous harvesting. Meanwhile, in India, the Maharashtra government is expanding mechanization grants to include grape pickers, signaling growing acceptance of mechanization in emerging commercial vineyards.

North America is witnessing a surge in demand for high-capacity grape harvesting machinery, fueled by increasing vineyard consolidation in major wine-producing states. Notable acquisitions, such as The Wine Group's 2025 buyout of a sprawling 6,600-acre vineyard, are paving the way for efficient harvesting fleets that promise reduced labor reliance. Concurrently, manufacturers are bolstering regional supply chains and enhancing aftermarket services. A case in point is Oxbo's New York facility, which is amplifying parts accessibility and service responsiveness for the often-overlooked East Coast vineyards. In South America, both Chilean and Argentine wine producers are ramping up investments in mechanization. Their goal: to curtail production costs, ensure consistent harvests, and bolster their competitive edge in exports, especially in light of rising labor costs. Meanwhile, the Middle East and Africa, still in the nascent stages of adoption, are witnessing selective mechanization growth. Regions like South Africa's Westerreliance on labormore amidn Cape and Turkey's Thrace are seeing commercial vineyards invest in modern harvesting tools, aiming to boost operational efficiency and maintain export quality.

- Pellenc S.A.S.

- New Holland Agriculture - Braud (CNH Industrial N.V.)

- Oxbo International Corporation (Ploeger Oxbo Group B.V.)

- Gregoire S.A.S. (SDF S.p.A.)

- ERO GmbH

- Kubota Corporation

- Yanmar Holdings Co., Ltd.

- Alma S.R.L.

- CRF Costruzioni S.R.L.

- Blueline Manufacturing Company

- American Grape Harvesters Inc.

- Bobard S.A.S.

- Nairn Harvesters Limited

- Reese Group Ltd.

- Weremczuk FMR Sp. z o.o.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Labor-shortage driven mechanization surge

- 4.2.2 Vineyard consolidation among large wine producers

- 4.2.3 Government mechanization subsidies and tax credits

- 4.2.4 Precision-viticulture adoption requiring data-ready machinery

- 4.2.5 Emerging rental and subscription ownership models

- 4.2.6 Development of lightweight self-propelled micro-harvesters

- 4.3 Market Restraints

- 4.3.1 High upfront capital expenditure

- 4.3.2 Operator-skill and maintenance complexity

- 4.3.3 Quality concerns for premium hand-picked varietals

- 4.3.4 Limited suitability on extreme-slope vineyards

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Harvester Type

- 5.1.1 Self-Propelled Grape Harvesters

- 5.1.2 Trailed / Towed Grape Harvesters

- 5.1.3 Tractor-Mounted Grape Harvesters

- 5.2 By Mode of Operation

- 5.2.1 Manual Steering & Operation

- 5.2.2 Assisted / Precision-Guided Operation

- 5.2.3 Autonomous / Semi-Autonomous Operation

- 5.3 By Power Source

- 5.3.1 Diesel-Powered Harvesters

- 5.3.2 Hybrid Harvesters

- 5.3.3 Electric Harvesters

- 5.4 By Vineyard Size

- 5.4.1 Small Vineyards (Below 50 Hectares)

- 5.4.2 Medium Vineyards (51-200 Hectares)

- 5.4.3 Large Vineyards (Above 200 Hectares)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 France

- 5.5.3.2 Italy

- 5.5.3.3 Spain

- 5.5.3.4 Germany

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Australia

- 5.5.4.3 Japan

- 5.5.4.4 India

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Turkey

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Morocco

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Pellenc S.A.S.

- 6.4.2 New Holland Agriculture - Braud (CNH Industrial N.V.)

- 6.4.3 Oxbo International Corporation (Ploeger Oxbo Group B.V.)

- 6.4.4 Gregoire S.A.S. (SDF S.p.A.)

- 6.4.5 ERO GmbH

- 6.4.6 Kubota Corporation

- 6.4.7 Yanmar Holdings Co., Ltd.

- 6.4.8 Alma S.R.L.

- 6.4.9 CRF Costruzioni S.R.L.

- 6.4.10 Blueline Manufacturing Company

- 6.4.11 American Grape Harvesters Inc.

- 6.4.12 Bobard S.A.S.

- 6.4.13 Nairn Harvesters Limited

- 6.4.14 Reese Group Ltd.

- 6.4.15 Weremczuk FMR Sp. z o.o.