|

시장보고서

상품코드

2063993

노인 돌봄 AI 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In Elderly Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

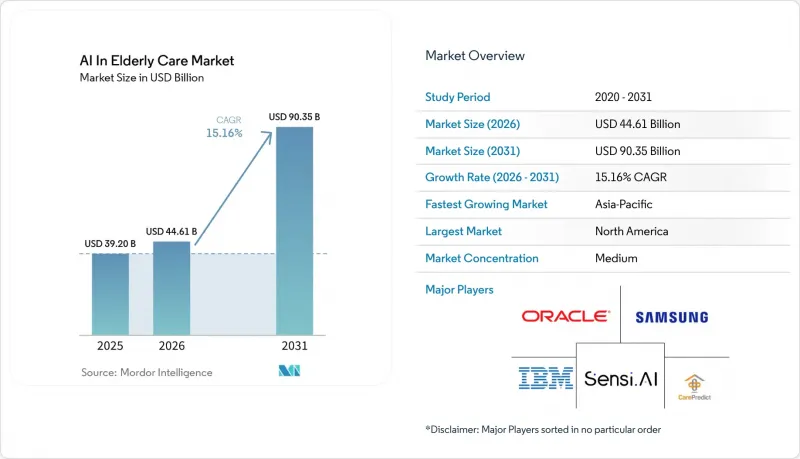

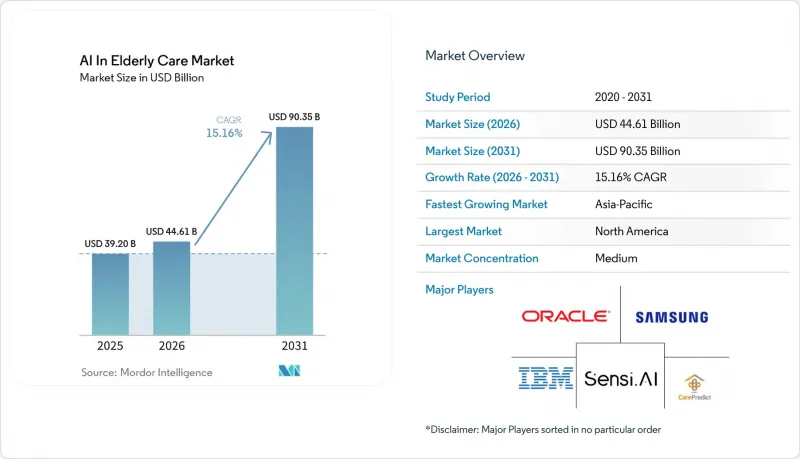

Mordor Intelligence에 의하면, 노인 돌봄 AI 시장 규모는 2025년에 392억 달러로 평가되었고, 2026년에 446억 1,000만 달러로 추정되며, 2031년까지 903억 5,000만 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 15.16%로 성장할 것으로 전망됩니다.

본 보고서는 제공 방식별(하드웨어, 소프트웨어, 서비스), 배포 방식별(클라우드, 온프레미스), 기술별(머신러닝 및 분석, 자연어 처리, 비전, 로봇공학, 기타), 용도별(낙상 감지, 원격 모니터링 등), 최종 사용자별(재택 간병, 간병 지원 주택, 특별양로원, 기타), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 노인 돌봄 AI 시장 동향과 인사이트

고령화와 평균 수명의 연장

노인 돌봄 AI 시장의 인구통계학적 기반은 돌봄이 가장 많이 필요한 연령대에서 가장 빠르게 확대되고 있습니다. 2024년 전 세계 출생 시 평균 기대수명은 73.3년에 달했으나, 이렇게 늘어난 수명은 장기간에 걸친 완전한 건강 상태라기보다는 만성 질환, 기능 저하, 그리고 반복되는 돌봄 필요와 관련이 있는 경향이 점점 더 강해지고 있습니다. 2025년 기준으로 전 세계 60세 이상 인구는 12억 2,000만 명에 달했으며, 2030년까지 14억 명으로 증가할 것으로 예측됩니다. 이에 따라 예측 기간 전반에 걸쳐, 고령자 돌봄용 AI 시장은 확대되는 돌봄 기반 시설과 밀접하게 연계된 상태가 지속될 것으로 전망됩니다. 80세 이상 인구는 이미 1억 400만 명이며, 2050년까지 2억 6,300만 명에 달할 것으로 예측됩니다. 이 계층은 돌봄, 약물 복용 지원, 이동 지원에 대한 수요가 가장 높기 때문에 중요한 의미를 지닙니다. 미국에서 80세 이상 인구는 2025년에 1,475만 명이었으나, 2030년까지 1,879만 명에 달할 것으로 예측되고 있으며, 이는 인력 배치 모델과 시설 운영에 대한 부담이 커지고 있음을 시사합니다. 2050년까지 중국과 인도의 고령 인구를 합친 비중이 전 세계 고령 인구에서 매우 큰 비중을 차지할 것으로 전망됩니다. 이는 노인 돌봄 AI 시장 제품 설계가 아시아의 저비용이며 자원이 제한된 돌봄 환경에 맞추어 점점 더 적응해 가고 있음을 의미합니다.

전체 노인 요양 시설의 요양사 부족

노인 돌봄 AI 시장은 단순히 공개된 구인 건수만으로는 파악할 수 없는 심각한 인력 부족에 의해서도 형성되고 있습니다. PHI의 예측에 따르면, 미국에서는 2024-2034년 직접 돌봄 종사자가 970만 개의 공석을 메워야 하며, 그중 77만 2,000명은 단순한 대체 수요가 아닌 순증분 신규 고용에 해당합니다. 이는 사업자에게 있어 인력 확보가 어려운 것은 물론, 신체적·정신적으로 혹독한 업무를 담당하는 다수의 신규 직원을 양성해 나가면서 서비스의 질을 유지하려 하고 있음을 의미합니다. 일본에서는 2026년도까지 필요한 요양 보호사 수가 240만 명에 달할 것으로 예상되지만, 고령화는 2040년을 향해 더욱 진행될 것으로 전망되어, 이로 인해 노동력 공급과 필요한 요양 능력 간의 격차는 더욱 확대될 것입니다. 이러한 상황에서 노인 돌봄 AI 시장은 기록 작성 시간 단축, 직원 간 협업 간소화, 입소자의 위험 요소를 조기에 파악하여 더 적은 인력으로 더 많은 입소자를 안전하게 관리할 수 있게 해주는 도구에 대한 수요 덕분에 혜택을 보고 있습니다. 수작업에 소요되는 시간을 1시간이라도 줄이는 것이 중요한 현장에서 기록 작성의 부담을 경감하고 경보의 정확도를 높이는 기술은 생산성과 직원 이직률 모두를 뒷받침할 수 있으므로, 그 운영상의 이점은 명백합니다.

개인정보 보호, 사이버 보안 및 규정 준수 부담

노인 돌봄 AI 시장에서 규정 준수 관련 장벽은 임상적 및 운영적 수요가 가속화됨에 따라 함께 높아지고 있습니다. EU AI법은 2024년 8월에 발효되며, 많은 의료 관련 모니터링 시스템이 2026년 8월부터 고위험 의무 적용 대상이 되므로, 도입 전 위험 관리, 데이터 거버넌스, 문서화 및 인적 감시의 필요성이 높아지고 있습니다. 미국에서는 HIPAA에 근거한 보호 대상 건강 정보(PHI)에 관한 규정에 따라, 입소자 수준의 건강 데이터를 취급하는 업체에 대해 별도의 보안 및 절차 요건이 부과되고 있습니다. 도쿄도립대학의 조사에 따르면, 고령자 피험자의 82%가 카메라 기반의 대안보다 개인정보 보호 기능을 갖춘 모니터링 시스템을 선호하는 것으로 나타났으며, 이는 개인정보 보호가 단순한 법적 문제가 아니라 노인 돌봄 AI 시장에서 사용자 수용성 문제이기도 함을 보여줍니다. 문제는 개인정보 보호 시스템에는 더 정교한 감지, 암호화 및 데이터 처리 아키텍처가 필요한 경우가 많아, 이로 인해 개발 비용이 증가하여 소규모 공급업체에게는 걸림돌이 된다는 점입니다. 이로 인해 자금력이 풍부한 대형 공급업체에게는 구조적인 우위가 생깁니다. 왜냐하면, 그들은 규정 준수 대응에 따른 부담을 더 수월하게 감당할 수 있고, 그 비용을 더 광범위한 도입 기반에 분산시킬 수 있기 때문입니다.

부문별 분석

2025년 기준으로, 소프트웨어는 노인 돌봄 AI 시장의 65.02%를 차지했으며, 이는 플랫폼 구독이 여전히 현재 도입 주기 내 지출의 핵심을 이루고 있음을 보여줍니다. 이러한 우위는 재택 및 시설 환경 모두에서 입소자 모니터링, 임상 워크플로우 지원, 분석, 경보 관리에 있어 소프트웨어가 수행하는 중요한 역할을 반영하고 있습니다. 센싱 및 로봇 공학 분야에서는 여전히 하드웨어가 필요하지만, 기기 간 경쟁이 치열하고 가격 압박도 심하기 때문에 소프트웨어와 동등한 이익률을 확보하지 못하고 있습니다. 서비스 분야는 2026년부터 2031년까지 연평균 성장률(CAGR) 16.17%로 확대될 것으로 예상되며, 이는 노인 돌봄 AI 시장이 단순한 제품 구매에서 도입 후의 전면적인 운영 지원으로 전환되고 있음을 의미합니다. 이러한 경향은 대개 구매자가 도구를 도입할지 여부를 결정하는 단계를 지나, 직원, 업무 흐름, 보고 체계 전반에 걸쳐 이를 어떻게 운영할지에 초점을 맞출 때 나타납니다.

서비스 확대가 중요한 이유는 도입, 교육, 워크플로우 재설계 및 관리형 지원이 도입 초기 단계에 비해 계약 금액에 직접적인 영향을 미치게 되었기 때문입니다. 여러 시설이나 돌봄 프로그램에 AI 도구를 도입하는 시설의 경우, 기존 돌봄 프로세스에 알림, 직원의 역할, 에스컬레이션 절차를 통합하기 위한 지원이 필요한 경우가 많습니다. 이로 인해 전문 서비스는 고객 유지에 있어 더욱 중요한 역할을 하게 될 것입니다. 왜냐하면 소프트웨어 자체가 뛰어나더라도 도입 시 지원이 미흡하면 성과가 저해될 가능성이 있기 때문입니다. Sage는 2026년 3월에 6,500만 달러를 조달하여, 총 조달액은 1억 2,400만 달러에 달했습니다. 이는 고령자 주거 시설 및 요양 시설 사업자를 대상으로, 예측 소프트웨어와 운영 지원을 결합한 통합 모델에 대한 투자자들의 신뢰를 보여주는 것입니다. 노인 돌봄 AI 시장이 성숙해짐에 따라, 소프트웨어와 지속적인 서비스 제공 능력을 결합한 공급업체는 단일 제품에 의존하는 기업보다 가격을 더 효과적으로 유지할 가능성이 높을 것입니다.

2026년 기준으로, 노인 돌봄 AI 시장 규모 중 클라우드 도입이 58.46%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 15.59%를 나타낼 것으로 예측됩니다. 현재의 규모와 미래의 성장 가능성을 모두 갖춘 이러한 상황은 통합된 가시성과 신속한 소프트웨어 업데이트가 필요한 다중 거점을 운영하는 사업자들에게 클라우드가 선호되는 운영 모델이 되고 있음을 보여줍니다. 노인 돌봄 AI 시장에서 사업자가 분산된 재택 돌봄, 돌봄형 주거 시설 및 돌봄 서비스를 단일 관리 체제 하에서 관리할 경우, 클라우드 아키텍처는 특히 매력적입니다. 경고, 문서화 도구 및 모델 개선에 대한 공동 접근 권한은 각 시설별로 개별적으로 도입하는 것보다 플랫폼을 일원화하여 관리하는 편이 더 용이합니다. 이러한 장점은 AI 도구가 단순한 모니터링에서 워크플로우 지원, 보고서 작성, 예측적 의사결정 지원으로 그 범위가 확대됨에 따라 더욱 중요해질 것입니다.

온프레미스형 시스템은 엄격한 데이터 상주 요건이나 엄격하게 관리되는 공공 부문 조달 규정이 적용되는 환경에서 여전히 일정한 위치를 차지하고 있습니다. 또한, 일부 유럽 및 아시아태평양 지역의 사업자들은 기밀성이 높은 신경학적 데이터나 장기적인 임상 데이터를 다룰 때 온프레미스형 또는 프라이빗 클라우드 구조를 선호하는 경향이 있습니다. 그렇긴 하지만, 로컬 시스템은 일반적으로 업데이트 속도가 느리기 때문에 공급업체가 감지 기능이나 언어 기능을 빠르게 개선하고 있는 경우, 모델 업데이트가 지연되어 성능이 저하될 가능성이 있습니다. 엔조 헬스(Enzo Health)는 2026년 5월, 재택의료 분야 전반에 걸쳐 클라우드 기반 AI를 확대하기 위해 2,600만 달러를 조달했습니다. 이 회사는 접수 업무의 자동화, 임상 기록, 품질 보증을 단일 워크플로우로 연계하고 있으며, 이는 노인 돌봄 AI 분야에서 자본이 어디로 흘러가고 있는지를 반영하고 있습니다. 구매자들이 신속하게 도입하고, 일원적으로 관리하며, 대규모 현지 인프라 구축 없이도 모든 케어 환경으로 확장할 수 있는 플랫폼을 점점 더 요구하고 있기 때문에 전반적인 방향성은 명확합니다.

지역별 분석

2025년, 북미는 노인 돌봄 AI 시장 규모에서 37.83%를 차지했으며, 여전히 이 분야에서 가장 큰 비중을 차지하는 지역으로서의 위상을 유지했습니다. 이 지역은 높은 요양 비용, 잘 갖춰진 디지털 인프라, 그리고 재택·지역·시설 요양 전 분야에서 업무 효율화 도구를 적극적으로 도입하려는 사업자 기반을 갖추고 있다는 이점을 누리고 있습니다. 미국에서는 2025년 80세 이상 인구가 1,475만 명이었으나, 2030년까지 1,879만 명에 달할 것으로 예측되고 있어, 노인 돌봄 분야에서 AI 서비스에 대한 장기적인 수요는 계속해서 증가하고 있습니다. CMS는 2024년 4월, 입소자 1인당 하루 3.48시간의 간호 시간을 최소 인력 기준으로 확정했습니다. 이러한 방침에 따라, 여전히 인력 확보가 어려운 상황에서 규정 준수를 지원하는 문서 관리 및 워크플로우 도구 도입에 대한 시설 측의 부담이 커지고 있습니다. 또한, 이 지역에 대한 투자 자금도 계속해서 확보되고 있습니다. Sage사의 2026년 3월 자금 조달 라운드와 Enzo Health사의 2026년 5월 자금 조달 사례가 보여주듯이, 두 사례 모두 노인 돌봄 및 재택치료 현장에서 AI 도구의 확대에 초점을 맞춘 것이었습니다. 남미에서는 도입이 아직 초기 단계에 있으며, 많은 지역에서 시설 전체에 광범위하게 도입되기 전에 스마트폰을 활용한 모니터링이나 음성 비서 이용이 나타나고 있습니다.

유럽은 노인 돌봄 AI 시장에서 규모는 크지만 지역마다 상황이 다른 시장입니다. 유럽연합(EU)의 65세 이상 인구는 2023년에 21%를 나타낼 것으로 예측되며, 2050년까지는 29%에 이를 것으로 전망됩니다. 이로 인해 수요는 단기적인 기술 주기가 아니라 장기적인 인구 동향의 변화에 의해 뒷받침되고 있습니다. EU AI법은 제품 요건을 재구성하고 있습니다. 2026년 8월부터는 의료 관련 모니터링 시스템에 대해 더욱 엄격한 의무가 부과됨에 따라 시장 진입 장벽이 높아져, 규정 준수 체계를 탄탄히 갖춘 공급업체에게 유리하게 작용할 것입니다. 영국은 독자적인 길을 걷고 있지만, 지역 돌봄 현장에서 진행 중인 AI 문서화 시범 운영을 통해 워크플로우 지원이 여전히 해당 지역의 노인 돌봄 제공업체들에게 가장 시급한 활용 사례 중 하나임이 드러났습니다.

아시아태평양은 노인 돌봄 AI 시장에서 가장 빠르게 성장하고 있는 지역으로, 2026-2031년 연평균 성장률(CAGR) 18.03%를 나타낼 것으로 전망됩니다. 일본은 여전히 주요 견인 역할을 하고 있으며, 고령화율은 2020년에 28.6%에 달했고, 2040년까지 35%에 이를 것으로 예상되는 반면, 간병인 수요는 2026년도까지 240만 명에 달할 것으로 전망됩니다. 또한, 일본 정부는 2024년도 추가경정예산에서 케어 DX 도입 패키지에 19억 엔(1,260만 달러)을 편성했습니다. 키타큐슈시에서 진행된 시범 사업에서는 기술의 연계 활용을 통해 요양 업무의 총 소요 시간이 35% 단축된 것으로 보고되었습니다. 중국도 AI 로봇 공학 및 노인 돌봄 인프라에 대한 투자를 확대하고 있으며, 한국과 호주는 디지털화 대비 및 노인 돌봄 개혁을 통해 지원을 강화하고 있습니다. 중동 및 아프리카는 여전히 소규모 지역 시장이지만, GCC 국가들의 고급 시설에 대한 도입과 아프리카 일부 지역에서의 지역 밀착형 모니터링 노력은 가장 성숙한 노인 돌봄 시스템이 구축된 지역 이외의 곳에서도 도입이 확대되기 시작하고 있음을 시사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the aI in elderly care market size is projected to be USD 39.20 billion in 2025, USD 44.61 billion in 2026, and reach USD 90.35 billion by 2031, growing at a CAGR of 15.16% from 2026 to 2031.

This report is Segmented by Service (Hardware, Software, Services), Deployment Mode (Cloud, On-Premise), Technology (ML & Analytics, NLP, Vision, Robotics, Other), Application (Fall Detection, Remote Monitoring, and More), End User (Home Care, Assisted Living, Nursing Homes, Others), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In Elderly Care Market Trends and Insights

Aging Population and Longer Life Expectancy

The demographic foundation of the AI in elderly care market is expanding most quickly in the age groups that consume the highest amount of care. Global life expectancy at birth reached 73.3 years in 2024, and the added years are increasingly associated with chronic disease, functional decline, and recurring support needs rather than long periods of full health. The global population aged 60 and above reached 1.22 billion in 2025, and that group is projected to rise toward 1.4 billion by 2030, which keeps the AI in elderly care market tied to an expanding care base for the full forecast period. The population aged 80 and above already stood at 104 million and is projected to reach 263 million by 2050, which matters because this group has the highest intensity of supervision, medication support, and mobility assistance needs. In the United States, the population aged 80 and above stood at 14.75 million in 2025 and is projected to reach 18.79 million by 2030, which points to rising pressure on staffing models and facility operations. China and India together are expected to hold a very large share of the global older population by 2050, which means product design in AI in elderly care market is increasingly being adapted for lower cost and resource-constrained care settings in Asia.

Caregiver Shortages Across Senior Care Settings

The AI in elderly care market is also being shaped by a labor shortage that is deeper than open vacancy numbers alone suggest. PHI projects that the United States direct care workforce must fill 9.7 million openings between 2024 and 2034, with 772,000 of those representing net new job growth rather than simple replacement demand. This means providers are not only struggling to hire, but they are also trying to maintain service quality while training large numbers of new workers into physically and emotionally demanding roles. In Japan, the required caregiver count reached 2.40 million by FY2026, while aging is projected to keep rising toward 2040, which widens the gap between labor supply and required care capacity. In this setting, the AI in elderly care market is benefiting from demand for tools that reduce charting time, simplify staff coordination, and identify resident risk earlier so fewer workers can manage more residents safely. The operational appeal is straightforward, because technologies that reduce documentation load and improve alert quality can support both productivity and worker retention in settings where every avoided hour of manual work matters.

Privacy, Cybersecurity, and Compliance Burden

The compliance barrier in the AI in elderly care market is rising at the same time that clinical and operational demand is accelerating. The EU AI Act entered into force in August 2024, and many healthcare related monitoring systems will face high risk obligations from August 2026, which increases the need for risk management, data governance, documentation, and human oversight before deployment. In the United States, protected health information rules under HIPAA add a separate layer of security and process requirements for any vendor working with resident level health data. Tokyo Metropolitan University research found that 82% of elderly subjects preferred privacy-protected monitoring systems over camera-based alternatives, which shows that privacy is not only a legal issue but also a user acceptance issue inside the AI in elderly care market. The challenge is that privacy preserving systems often require more advanced sensing, encryption, and data handling architecture, which raises development cost and slows smaller vendors. This gives larger and better funded suppliers a structural advantage because they can absorb compliance work more easily and spread those costs across a wider installed base.

Other drivers and restraints analyzed in the detailed report include:

- Aging-In-Place and Proactive Remote Monitoring Adoption

- Better AI Accuracy Across NLP, Vision, and Robotics

- Integration Cost and Legacy-System Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software captured 65.02% of the AI in elderly care market share in 2025, which shows that platform subscriptions still form the spending core of the current adoption cycle. This lead reflects the strong role of software in resident monitoring, clinical workflow support, analytics, and alert management across both home and facility environments. Hardware remains necessary for sensing and robotics, but it does not capture the same margin profile because device competition is broader and pricing pressure is more visible. Services are projected to expand at 16.17% CAGR from 2026 to 2031, which means the AI in the elderly care industry is moving from simple product purchase toward full deployment support. That pattern usually appears when buyers no longer ask whether to adopt a tool and instead focus on how to make it work across staff, workflows, and reporting structures.

The services expansion matters because implementation, training, workflow redesign, and managed support now influence contract value more directly than they did in the early phase of adoption. Facilities that deploy AI tools across multiple buildings or care programs often need help mapping alerts, staff roles, and escalation protocols into existing care processes. This makes professional services more central to retention because poor onboarding can weaken outcomes even when the software itself is strong. Sage raised USD 65 million in March 2026, bringing its total capital raised to USD 124 million, which points to investor confidence in integrated models that combine predictive software with operational support for senior living and skilled nursing providers. As the AI in elderly care market matures, vendors that pair software with recurring service capacity are likely to defend pricing more effectively than companies that rely on standalone products.

Cloud deployment accounted for 58.46% share of the AI in elderly care market size in 2026, and it is also projected to grow at 15.59% CAGR through 2031. This combination of current scale and future growth shows that cloud has become the preferred operating model for multi-site providers that need centralized visibility and rapid software updates. In the AI in elderly care market, cloud architectures are especially attractive when operators manage distributed home care, assisted living, and nursing services under one administrative structure. Shared access to alerts, documentation tools, and model improvements is easier when platforms are centrally managed rather than installed separately inside each building. This advantage becomes more important as AI tools expand from simple monitoring into workflow support, reporting, and predictive decision assistance.

On-premises systems still hold a place in settings with strict data residency demands or highly controlled public sector procurement rules. Some European and Asia-Pacific operators also prefer on-premises or private cloud structures when they handle sensitive neurological or long-term clinical data. Even so, local systems usually update more slowly, and slower model updates can weaken performance when vendors are improving detection or language features quickly. Enzo Health raised USD 26 million in May 2026 to scale cloud-based AI across home health, linking intake automation, clinical documentation, and quality assurance in one workflow, which reflects where capital is moving inside the AI in elderly care market. The broader direction remains clear, because buyers increasingly want platforms that can be rolled out quickly, managed centrally, and extended across care settings without major local infrastructure work.

Geography Analysis

North America accounted for 37.83% share of the AI in elderly care market size in 2025, which kept it as the largest regional contributor. The region benefits from high care costs, strong digital infrastructure, and a provider base that is actively seeking labor saving tools across home, community, and institutional care. In the United States, the population aged 80 and above stood at 14.75 million in 2025 and is projected to reach 18.79 million by 2030, which continues to strengthen the long term need for AI supported elderly care delivery. CMS finalized a minimum staffing standard of 3.48 nursing hours per resident day in April 2024, and that policy has increased pressure on facilities to use documentation and workflow tools that support compliance where hiring remains difficult. Capital also remains available for deployment in the region, as shown by Sage's March 2026 funding round and Enzo Health's May 2026 raise, which both focused on scaling AI tools across senior care and home health settings. South America remains earlier in adoption, with smartphone led monitoring and voice companion use appearing before broader institutional deployments in many areas.

Europe is a large but uneven regional opportunity inside the AI in elderly care market. The population aged 65 and above in the European Union reached 21% in 2023 and is projected to reach 29% by 2050, which keeps demand anchored in long duration demographic change rather than short term technology cycles. The EU AI Act is reshaping product requirements because healthcare-related monitoring systems will face stricter obligations from August 2026, which raises entry barriers and favors vendors with stronger compliance resources. The United Kingdom is moving on a separate path, but AI documentation trials in community care settings still show that workflow support remains one of the most immediate use cases for elderly care providers in the region.

Asia-Pacific is the fastest-growing region in the AI in elderly care market, with an expected CAGR of 18.03% from 2026 to 2031. Japan remains a key driver because its aging rate reached 28.6% in 2020 and is projected to move toward 35% by 2040, while caregiver demand reached 2.40 million by FY2026. Japan's government also committed JPY 1.9 billion, or USD 12.6 million, in its FY2024 supplementary budget for Care DX adoption packages, and a model project in Kitakyushu City reported a 35% reduction in overall care work time from coordinated technology use. China is also increasing its focus on AI robotics and elderly care infrastructure, while South Korea and Australia add support through digital readiness and aged care reform. The Middle East and Africa remain a smaller regional base, but premium facility deployments in GCC countries and community-oriented monitoring initiatives in parts of Africa suggest that adoption is beginning to widen beyond the most mature elderly care systems.

- Aiva Health

- Best Buy Health

- CarePredict

- Cera Care

- GrandCare Systems

- GrandPad

- IBM

- Intuition Robotics

- K4Connect

- Kami Vision

- Nobi

- Oracle

- Koninklijke Philips

- Reemo Health

- Resideo Technologies

- Samsung Electronics

- Sensi.AI

- SoftBank Robotics

- Tunstall Healthcare

- UBTECH Robotics

- Vayyar Care

- WellSky

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population and Longer Life Expectancy

- 4.2.2 Caregiver Shortages Across Senior Care Settings

- 4.2.3 Aging-In-Place and Proactive Remote Monitoring Adoption

- 4.2.4 Better AI Accuracy Across NLP, Vision, and Robotics

- 4.2.5 Privacy-Preserving Ambient Sensing Replacing Cameras and Wearables

- 4.2.6 Staffing-Rule and Documentation ROI Driving Workflow AI Uptake

- 4.3 Market Restraints

- 4.3.1 Privacy, Cybersecurity, And Compliance Burden

- 4.3.2 Integration Cost and Legacy-System Complexity

- 4.3.3 Surveillance Trust Gap Among Oldest-Old Users

- 4.3.4 Tariff And Component Volatility in Sensors and Robotics

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.3 By Technology

- 5.3.1 Machine Learning and Predictive Analytics

- 5.3.2 Natural Language Processing

- 5.3.3 Computer Vision

- 5.3.4 Robotics and Robotic Assistance

- 5.3.5 Other Technology (Smart Home Devices and IoT Solutions, Generative AI Care Assistants, etc.)

- 5.4 By Application

- 5.4.1 Fall Detection and Prevention

- 5.4.2 Remote Monitoring and Predictive Alerts

- 5.4.3 Medication Management

- 5.4.4 Cognitive Support and Dementia Care

- 5.4.5 Social Interaction and Companionship

- 5.4.6 Rehabilitation and Daily Living Assistance

- 5.5 By End User

- 5.5.1 Home Care Settings

- 5.5.2 Assisted Living Facilities

- 5.5.3 Nursing Homes

- 5.5.4 Other End Users (Hospitals and Clinics, etc.)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Aiva Health

- 6.3.2 Best Buy Health

- 6.3.3 CarePredict

- 6.3.4 Cera Care

- 6.3.5 GrandCare Systems

- 6.3.6 GrandPad

- 6.3.7 IBM

- 6.3.8 Intuition Robotics

- 6.3.9 K4Connect

- 6.3.10 Kami Vision

- 6.3.11 Nobi

- 6.3.12 Oracle Corporation

- 6.3.13 Philips

- 6.3.14 Reemo Health

- 6.3.15 Resideo Technologies

- 6.3.16 Samsung Electronics

- 6.3.17 Sensi.AI

- 6.3.18 SoftBank Robotics

- 6.3.19 Tunstall Healthcare

- 6.3.20 UBTECH Robotics

- 6.3.21 Vayyar Care

- 6.3.22 WellSky

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment