|

시장보고서

상품코드

2063994

소아 원격의료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Pediatric Telehealth - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

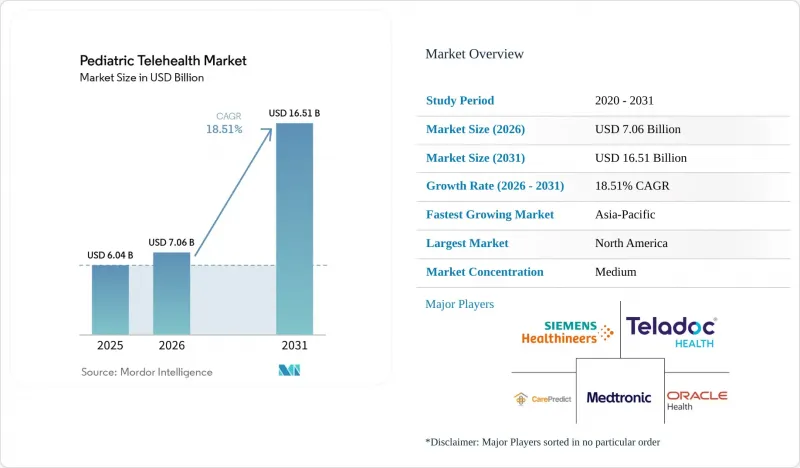

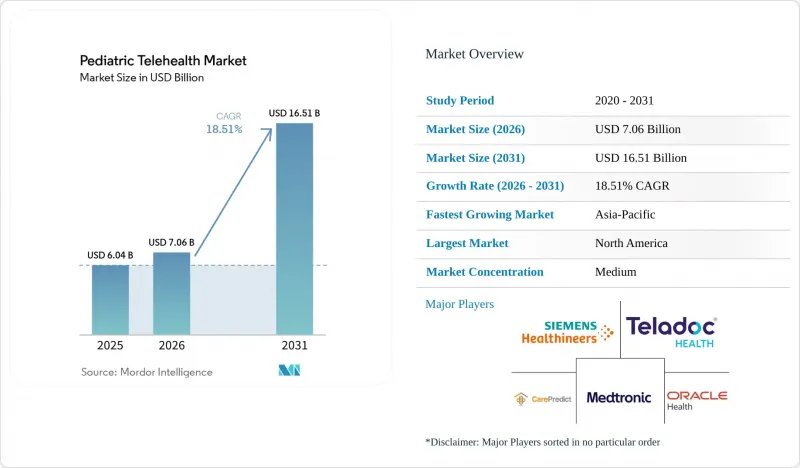

Mordor Intelligence에 의하면, 소아 원격의료 시장 규모는 2025년 60억 4,000만 달러에서 2026년에는 70억 6,000만 달러로 확대되어 2031년까지 165억 1,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 18.51%로 성장할 전망입니다.

본 보고서는 제품 유형(하드웨어, 소프트웨어, 서비스), 제공 형태(On-Premise, 웹 기반, 클라우드 기반), 질환 분야(정신과, 피부과, 신경과, 방사선과, 치과, 기타), 최종 사용자(의료 제공업체, 보험사, 환자 및 가족), 그리고 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 소아 원격의료 시장 동향과 인사이트

소아과 전문의 부족과 지방의 의료 접근성 격차

소아 원격의료 시장은 지방이나 인구 밀도가 낮은 지역에서 계속해서 확대되고 있는 의료 접근성 격차에 힘입어 성장하고 있습니다. 베일러 의과대학은 2025년에 미국 지방 카운티의 58.7%, 완전한 지방 카운티의 90.4%에 일반 소아과 의사가 없을 것이라고 보고했습니다. 지역 병원에서는 외래 및 급성기 의료 현장에서 소아과 체계가 충분히 갖춰지지 않아, 이러한 부담을 감당하기가 더욱 어려워지고 있습니다. UC 데이비스 헬스는 2024년 9월, 소아 재활의학과에서 학교를 거점으로 한 하이브리드형 원격 의료 진료와 관련해, 전문의의 출장비를 1회당 100달러 절감할 수 있었으며, 대면 진료와 비교했을 때 보호자의 만족도에 통계적으로 유의미한 차이는 나타나지 않았다고 밝혔습니다. 독일 북동부에서 실시된 RTP-Net 원격 소아 의료 네트워크의 조사 결과, 원격 상담을 통해 57.7%의 사례에서 임상 진단이 변경되거나 정밀화되었음이 밝혀졌습니다. 이는 가상 소아 진료가 단순한 선별 검사나 분류에 그치지 않고, 이미 실제 치료 결정에 영향을 미치고 있음을 보여줍니다.

소아 정신·행동 관리 수요 증가

소아 원격의료 시장에서 가장 강력한 수요 견인 역할을 하고 있는 분야는 정신·행동 관리 분야입니다. 미국 소아의 정신질환 진단 건수는 2016년부터 2023년 사이 35% 증가했으며, 이미 전문의 확보에 어려움을 겪고 있는 의료 시스템에 대한 부담을 더욱 가중시키고 있습니다. RAND는 2025년 보고서에서 정신건강 치료를 받고 있는 청소년의 45.3%가 원격의료 서비스를 이용하고 있으며, 진료소 기반의 전문 의료 분야에서 가상 진료 도입이 가장 집중되어 있다고 지적했습니다. 2025년 『JMIR Mental Health』지에 게재된 후향적 코호트 연구에 따르면, 소아 정신건강 분야의 원격 진료 횟수는 대면 진료에 비해 18% 적은 것으로 나타났습니다. 이는 돌봄의 효율성과 보험자 측의 경제성이라는 두 가지 측면에서 모두 중요한 의미를 지닙니다. 2024년 9월에 발표된 CMS 지침은 EPSDT를 통한 전문직 간 원격 상담을 지지하고 있으며, 이를 통해 1차 진료 현장은 전문의에게 의뢰하는 것만을 의존하지 않고 행동 건강 관리 제공 역량을 확대할 수 있게 되었습니다.

아동의 데이터 개인정보 보호 및 사이버 보안상의 위험

소아 원격의료 시장은 플랫폼이 미성년자의 의료 정보, 행동 정보, 생체 인증 정보를 다루기 때문에 의료 분야에서 가장 기밀성이 높은 데이터 환경 중 하나에서 운영되고 있습니다. FTC가 2025년에 시행한 COPPA 개정안에 따르면, 개인정보의 범위가 생체 인식 식별자까지 확대되었으며, 서비스에 필수적이지 않은 제3자에 대한 데이터 공개에 대해서는 별도로 검증 가능한 부모의 동의가 의무화되었습니다. 이로 인해, 아동용 플랫폼이 모델 학습, 분석 및 외부 공유를 위해 아동 데이터를 활용할 수 있는 방법이 직접적으로 제한됩니다. 학교에서 발급한 계정은 교육 목적으로 사용할 수 있지만, 해당 규정에 따르면 이러한 계정을 보다 광범위한 상실적 데이터 활용에 사용하는 것은 허용되지 않으며, 이로 인해 학교 중심 플랫폼의 수익화 선택지가 제한되고 있습니다. 2026년 4월 22일까지 완전한 규정 준수가 요구되며, 사업자는 현재 서면으로 된 정보 보안 프로그램의 유지, 연례 위험 평가 실시, 그리고 HIPAA 지침에 따른 부모의 접근권 관련 문제에 대해 보다 엄격하게 대응할 의무가 있습니다.

부문별 분석

2025년 기준으로 서비스 부문은 소아 원격의료 시장 규모의 48.66%를 차지하고 있으며, 이에 따라 의료 제공이 현재 지출의 중심을 이루게 되었습니다. 실시간 진료와 원격 환자 모니터링은 소아 원격의료 시장 전반에서 행동 의학, 만성 질환 관리, 퇴원 후 사후 관리를 지속적으로 뒷받침하고 있습니다. 이 서비스 계층은 특히 정신과나 치료 분야에서 확고히 자리 잡고 있으며, 치료의 지속성 측면에서 임상의와 가족 간의 지속적인 교류가 핵심적인 역할을 하고 있습니다. 2025년 네덜란드 연구에 따르면, 비침습적 재택 모니터링을 통해 소아 천식 조절 악화의 가장 강력한 수동적 지표로 야간 심박수 상승이 확인되었으며, 예후 악화의 오즈비는 2.1인 것으로 밝혀졌습니다.

소프트웨어는 소아 원격의료 시장에서 가장 빠르게 성장하고 있는 제품 유형으로, 2031년까지의 예상 연평균 성장률(CAGR)은 19.68%입니다. 의료 제공업체들이 EHR 연동, 원격 모니터링 데이터, 치료 조정을 단일 워크플로우로 구현하기를 원함에 따라, 통합 플랫폼이 소아 원격의료 업계에서 입지를 넓혀가고 있습니다. 독일의 Techped 프로젝트는 만성 질환을 앓고 있는 소아를 위한 다국어 모바일 헬스 플랫폼을 시범 운영 중이며, 연방 정부로부터 170만 유로(190만 달러)의 연구 보조금을 지원받았습니다. 하드웨어에 대한 수요는 증가하고 있지만, 기기 자체의 적용 범위가 확대되는 속도보다 임상 검증의 진전이 더 빠르기 때문에 그 성장세는 직선적이지 않습니다.

2025년에는 웹 기반 서비스가 44.87%의 점유율을 차지하며, 많은 대규모 학교 및 의료 제공업체 네트워크에서 여전히 기본 선택지로 자리 잡고 있습니다. 브라우저를 통한 접속은 관리 대상 기기에서 앱 설치가 제한되는 경우가 많은 학군의 IT 환경에 적합합니다. 보호 대상 건강 정보(PHI)를 보다 엄격하게 관리하고자 하는 대규모 소아병원에서는 On-Premise 도입이 여전히 중요합니다. 개정된 COPPA(아동 온라인 개인정보 보호법)의 틀에 따라, 소아 원격의료 시장 전반에서 공급업체가 관리하는 보안 및 문서화된 관리 체계의 중요성이 커지고 있습니다.

클라우드 기반 서비스는 소아 원격의료 시장에서 가장 빠르게 성장하고 있는 형태이며, 2031년까지 연평균 성장률(CAGR)은 20.03%를 나타낼 것으로 전망됩니다. 이러한 성장은 AI를 활용한 진단, 멀티모달 데이터 통합, 그리고 실시간 에스컬레이션 워크플로우에 대한 수요에 힘입어 이루어지고 있습니다. 2025년 10월에 도입되어 2026년에 상용화가 진행 중인 TytoCare의 ‘Smart Clinic Companion’은 연간 33%의 속도로 증가하고 있는 700만 건 이상의 검사 데이터 세트를 바탕으로 구축되었습니다. 또한, 클라우드 플랫폼은 보험사 및 의료 시스템에 2025년판 ‘Child Core Set’에 명시된 원격의료 품질 지표를 관리하는 데 필요한 분석 기반을 제공합니다.

지역별 분석

2025년 기준으로 북미는 소아 원격의료 시장 규모의 44.39%를 차지하며 여전히 가장 규모가 큰 지역 블록이었습니다. 미국은 메디케이드 및 CHIP을 통한 보상, 학교 기반 케어 패스웨이, 그리고 스타트업과 의료 서비스 제공업체의 활발한 활동을 통해 그 규모의 상당 부분을 주도하고 있습니다. 2024년 5월 현재, 미국에서는 3,800만 명의 어린이가 메디케이드 및 CHIP에 가입되어 있으며, 소아 원격의료 시장은 전 세계에서 가장 큰 규모의 공공 자금 지원 소아 의료 수요층을 보유하고 있습니다. 지역별 시장 규모는 여전히 불균등한 지급 정책으로 인해 제약을 받고 있습니다. 이는 48개 주와 워싱턴 D.C.가 원격의료 비용을 보상하고, 39개 주가 원격정신건강 서비스를 보상하고 있는 반면, 지급 격차 해소를 의무화하고 있는 주는 고작 23개 주에 불과하기 때문입니다.

유럽은 소아 원격의료 시장에서 2위의 점유율을 차지하고 있으며, 원격의료가 장기 요양 서비스의 재설계와 연계될 경우 이용이 어떻게 회복될 수 있는지를 보여주고 있습니다. 프랑스에서는 2024년에 1,390만 건의 원격 진료가 기록되어 전년 대비 20% 증가했습니다. 또한, 전문의에 의한 원격 진료는 정신과 의사의 진료 활동의 7%를 차지하고 있습니다. 2025년 1월에 시작된 독일의 ‘TelEmergency Kids’는 소아 응급 환자 분류가 전문센터에서 인근 병원 네트워크로 확대되고 있는 실제 사례를 보여주고 있습니다. 또한, 유럽에서는 GDPR(EU 개인정보보호규정)이나 영국의 ‘Children’s Code’에 따른 규정 준수 부담이 커서, 플랫폼에 이미 아동 데이터 거버넌스를 구축한 벤더가 유리한 입장에 있습니다.

아시아태평양은 소아 원격의료 시장에서 가장 빠르게 성장하고 있는 지역으로, 2031년까지 연평균 성장률(CAGR) 21.82%를 기록하며 확대될 것으로 전망됩니다. 이러한 성장은 중국, 인도, 일본, 한국의 전문의 부족, 디지털 인프라 확충, 그리고 국가 의료 시스템에 대한 투자에 힘입어 이루어지고 있습니다. 싱가포르에서는 국립대학병원이 2025년에 AeviceMD의 웨어러블 기기를 검증한 결과, 응급 의료 현장에서 85.3%의 민감도와 80.8%의 특이도를 확인했습니다. 또한, 재택 이용 시 성능은 92%를 초과합니다. 남미 시장은 규모는 작지만, 그 운영 사례는 점차 명확해지고 있습니다. 콜롬비아의 SPLA 모델에서는 소아 원격 상담의 70%를 대면 진료 없이 해결하고 있으며, 파라과이에서는 2026년 4월까지 500건 이상의 전문적인 소아 원격 상담이 이루어져 66,000킬로미터 이상의 이동을 줄일 수 있었다고 보고되고 있습니다. 중동 및 아프리카에서는 아직 도입 초기 단계이지만, GCC 시장의 공공 시스템 디지털화에 힘입어 소아과 분야의 가상 분류 및 후속 관리 활용이 꾸준히 확대되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the pediatric telehealth market size is expected to increase from USD 6.04 billion in 2025 to USD 7.06 billion in 2026 and reach USD 16.51 billion by 2031, growing at a CAGR of 18.51% over 2026-2031.

This report is Segmented by Product Type (Hardware, Software, Services), Delivery Mode (On-Premises, Web-Based, Cloud-Based), Disease Area (Psychiatry, Dermatology, Neurology, Radiology, Dental, Others), End User (Providers, Payers, Patients and Families), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Pediatric Telehealth Market Trends and Insights

Pediatric Specialist Shortages and Rural Access Gaps

The pediatric telehealth market is being pushed forward by a care access gap that keeps widening in rural and low-density areas. Baylor College of Medicine reported in 2025 that 58.7% of rural counties and 90.4% of fully rural counties in the United States had no general pediatrician. The pressure is even harder to absorb, as local hospitals no longer have strong pediatric coverage across outpatient and acute settings. UC Davis Health found in September 2024 that hybrid school-based telehealth visits for pediatric physiatry saved USD 100 per visit in specialist travel costs and showed no statistically significant difference in parent satisfaction compared with in-person care. In Northeast Germany, the RTP-Net tele-pediatric network found that teleconsultation changed or refined the clinical diagnosis in 57.7% of cases, which shows that virtual pediatric assessment is already influencing real treatment decisions rather than only screening or triage.

Rising Pediatric Mental and Behavioral Care Demand

The pediatric telehealth market is seeing its strongest demand pull from mental and behavioral care. Diagnosed mental health conditions among US children increased 35% between 2016 and 2023, which has raised pressure on a system that already struggles with specialist availability. RAND reported in 2025 that 45.3% of adolescents receiving mental health treatment used telehealth, with office-based specialty care showing the highest concentration of virtual delivery. A 2025 retrospective cohort study in JMIR Mental Health found that virtual pediatric mental health episodes involved 18% fewer visits than in-person episodes, which matters for both care efficiency and payer economics. CMS guidance issued in September 2024 supports interprofessional teleconsultation through EPSDT, which is helping primary care settings extend behavioral care capacity without relying only on specialist referral growth.

Child-Data Privacy and Cybersecurity Exposure

The pediatric telehealth market operates in one of healthcare's most sensitive data environments because platforms handle medical, behavioral, and biometric information from minors. The FTC's 2025 COPPA update expanded the scope of personal information to include biometric identifiers and required separate verifiable parental consent for third-party data disclosures that are not integral to the service. That directly limits how pediatric platforms can use child data for model training, analytics, and external sharing. School-issued accounts can support educational purposes, but the rule does not allow those accounts to be used for broader commercial data use, which narrows monetization options for school-centered platforms. Full compliance was required by April 22, 2026, and operators now have to maintain written information security programs, annual risk assessments, and tighter handling of parental access issues under HIPAA guidance.

Other drivers and restraints analyzed in the detailed report include:

- School-Based Reimbursement and Campus-Access Mandates

- Connected Peripherals that Improve Virtual Exam Closure

- Broadband, Device, and Digital Literacy Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services held 48.66% of the pediatric telehealth market size in 2025, which kept care delivery at the center of current spending. Real-time consultations and remote patient monitoring continue to support behavioral health, chronic condition management, and post-discharge follow-ups across the pediatric telehealth market. The service layer remains especially entrenched in psychiatry and therapy, where ongoing clinician and family contact is central to treatment continuity. A 2025 Dutch study found that non-invasive home monitoring detected nocturnal heart rate elevation as the strongest passive marker of worsening asthma control in children, with an odds ratio of 2.1 for worse outcomes.

Software is the fastest-growing product type in the pediatric telehealth market, with a forecast CAGR of 19.68% through 2031. Integrated platforms are gaining ground in the pediatric telehealth industry because providers want EHR links, remote monitoring data, and care coordination in one workflow. Germany's Techped project is testing a multilingual mobile health platform for children with chronic conditions and received EUR 1.7 million, or USD 1.9 million, in federal research funding. Hardware demand is rising, but growth is less linear because clinical validation is moving faster than reimbursement coverage for the devices themselves.

Web-based delivery held 44.87% share in 2025 and remains the default option for many large school and provider networks. Browser access fits school-district IT settings where managed devices often restrict app installation. On-premises deployment still matters in large children's hospitals that want tighter control over protected health information. The updated COPPA framework is making vendor-managed security and documented controls more important across the pediatric telehealth market.

Cloud-based delivery is the fastest-growing mode in the pediatric telehealth market, with 20.03% CAGR projected through 2031. Growth is being driven by AI-supported diagnostics, multi-modal data ingestion, and the need for real-time escalation workflows. TytoCare's Smart Clinic Companion, introduced in October 2025 and now in commercial rollout in 2026, was built on a dataset of more than 7,000,000 exams that is growing 33% annually. Cloud platforms also give payers and health systems the analytics backbone needed to manage telehealth quality measures in the 2025 Child Core Set.

Geography Analysis

North America held 44.39% of the pediatric telehealth market size in 2025 and remained the largest regional block. The United States drives most of that scale through Medicaid and CHIP reimbursement, school-based care pathways, and a large base of startup and provider activity. As of May 2024, 38 million children were enrolled in Medicaid and CHIP in the United States, giving the pediatric telehealth market the largest publicly financed pediatric demand pool in the world. Regional value is still constrained by uneven payment policy because 48 states and DC reimburse telemedicine, 39 states reimburse telemental health, and only 23 require payment parity.

Europe held the second-largest share in the pediatric telehealth market and shows how usage can rebound once telemedicine is tied to long-term care redesign. France recorded 13.9 million teleconsultations in 2024, up 20% from the prior year, and specialty teleconsultation represented 7% of psychiatrists' activity. Germany's TelEmergency Kids, launched in January 2025, shows how pediatric emergency triage is being extended from specialist centers into surrounding hospital networks. Europe also carries a high compliance burden under GDPR and the UK's Children's Code, which favors vendors that already built pediatric data governance into their platforms.

Asia Pacific is the fastest-growing region in the pediatric telehealth market and is projected to expand at 21.82% CAGR through 2031. Growth is supported by specialist shortages, expanding digital infrastructure, and national health system investment across China, India, Japan, and South Korea. In Singapore, National University Hospital validated the AeviceMD wearable in 2025 with 85.3% sensitivity and 80.8% specificity in emergency settings, with performance above 92% in home use. South America is smaller, but its operational case is becoming clearer, with Colombia's SPLA model resolving 70% of pediatric teleconsultations without in-person care and Paraguay reporting more than 500 specialized pediatric teleconsultations by April 2026 that avoided more than 66,000 kilometers of travel. The Middle East and Africa remain earlier in adoption, but public system digitalization in GCC markets is steadily widening the use of virtual pediatric triage and follow-up.

- Amwell

- Anytime Telecare

- Blueberry Pediatrics

- Brave Care

- Brightline

- CarePredict

- GlobalMed

- Hazel Health

- Kiddo Health

- Kismet Health

- Little Otter

- MDLIVE

- Medtronic

- Nicklaus Children's Health System

- Oracle Health

- PediaMetrix

- PM Pediatric Care

- Samsung Electronics

- Siemens Healthineers

- Summer Health

- Teladoc Health

- TytoCare

- Vayyar Care

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pediatric Specialist Shortages and Rural Access Gaps

- 4.2.2 Rising Pediatric Mental and Behavioral Care Demand

- 4.2.3 Remote Monitoring for Chronic Pediatric Conditions

- 4.2.4 Medicaid, CHIP, And Pediatric Telehealth Funding Support

- 4.2.5 School-Based Reimbursement and Campus-Access Mandates

- 4.2.6 Connected Peripherals that Improve Virtual Exam Closure

- 4.3 Market Restraints

- 4.3.1 Child-Data Privacy and Cybersecurity Exposure

- 4.3.2 Broadband, Device, and Digital Literacy Gaps

- 4.3.3 Adolescent Confidentiality and Proxy-Portal Leakage

- 4.3.4 Interpreter, Multi-Caregiver, and Pediatric Exam Workflow Friction

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Hardware

- 5.1.1.1 Monitors

- 5.1.1.2 Medical Peripheral Devices

- 5.1.2 Software

- 5.1.2.1 Standalone Software

- 5.1.2.2 Integrated Software

- 5.1.3 Services

- 5.1.3.1 Real-Time Interactions

- 5.1.3.2 Remote Patient Monitoring

- 5.1.3.3 Store-and-Forward

- 5.1.3.4 Other Services

- 5.1.1 Hardware

- 5.2 By Delivery Mode

- 5.2.1 On-Premises

- 5.2.2 Web-Based

- 5.2.3 Cloud-Based

- 5.3 By Disease Area

- 5.3.1 Psychiatry

- 5.3.2 Dermatology

- 5.3.3 Neurological Medicine

- 5.3.4 Radiology

- 5.3.5 Dental

- 5.3.6 Other Pediatric Indications

- 5.4 By End User

- 5.4.1 Providers

- 5.4.2 Payers

- 5.4.3 Patients and Families

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Amwell

- 6.3.2 Anytime Telecare

- 6.3.3 Blueberry Pediatrics

- 6.3.4 Brave Care

- 6.3.5 Brightline

- 6.3.6 CarePredict

- 6.3.7 GlobalMed

- 6.3.8 Hazel Health

- 6.3.9 Kiddo Health

- 6.3.10 Kismet Health

- 6.3.11 Little Otter

- 6.3.12 MDLIVE

- 6.3.13 Medtronic

- 6.3.14 Nicklaus Children's Health System

- 6.3.15 Oracle Health

- 6.3.16 PediaMetrix

- 6.3.17 PM Pediatric Care

- 6.3.18 Samsung Electronics

- 6.3.19 Siemens Healthineers

- 6.3.20 Summer Health

- 6.3.21 Teladoc Health

- 6.3.22 TytoCare

- 6.3.23 Vayyar Care

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment