|

시장보고서

상품코드

2063999

클라인펠터 증후군 치료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Klinefelter Syndrome Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

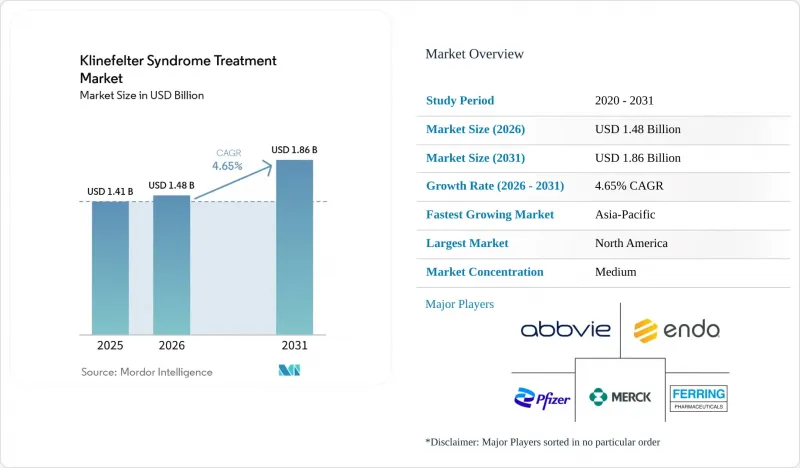

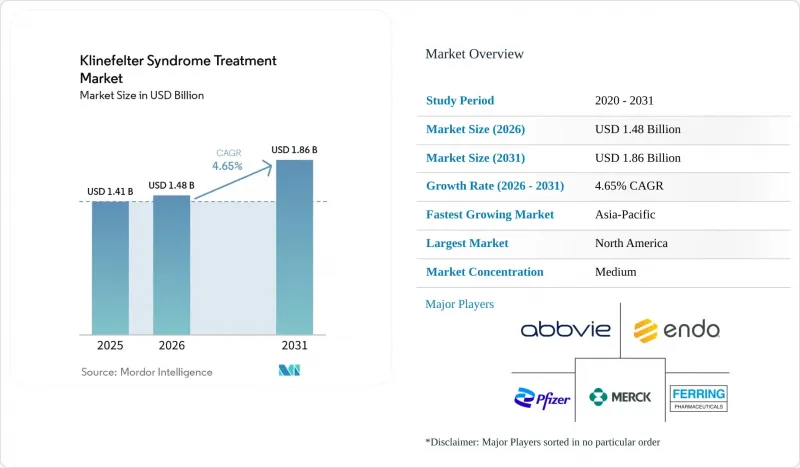

Mordor Intelligence에 의하면, 클라인펠터 증후군 치료 시장 규모는 2025년에 14억 1,000만 달러로 평가되었고 2026년 14억 8,000만 달러에서 2031년까지 18억 6,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.65%를 나타낼 전망입니다.

본 보고서는 치료 유형(TRT, 불임 치료, 지지 요법, 외과적 치료), 투여 경로(주사제, 경피제, 경구/구강 점막제, 비강제, 이식형), 최종 사용자(병원, 내분비 클리닉, 불임 치료 클리닉, 재택 간호, 기타), 연령대(소아, 청소년, 성인), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)에 따라 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

전 세계 클라인펠터 증후군 치료 시장 동향 및 인사이트

의료 종사자 및 환자의 인식 제고를 통한 조기 진단

클라인펠터 증후군 치료 시장은 최근 일반적인 질환치고는 비정상적으로 큰 진단 격차에 의해 계속해서 형성되고 있습니다. 평생 동안 이 질환으로 진단받는 환자는 50% 미만이며, 진단 시기의 중앙값은 여전히 28세에서 31세 사이에 집중되어 있습니다. 이 진단 지연은 심각한 문제입니다. 왜냐하면 많은 남성이 불임 검사 과정에서 처음으로 치료를 받게 되며, 그로 인해 호르몬 요법, 골 보호, 대사 경과 관찰, 그리고 불임 치료 계획과 같이 본래라면 수년 전에 시작할 수 있었을 조치들이 지연되기 때문입니다. 2024년 이후, 전자 진료 기록과 호르몬 프로파일을 활용한 머신러닝 접근법이 일반 진료 현장에서 실용적인 조기 발견에 한 걸음 더 가까워짐에 따라, 진단 툴킷이 개선되었습니다. 이로 인해, 증례 발견 시기가 전문의에게 늦게 의뢰되던 것에서 초기 단계로 점차 옮겨가고 있습니다.

클라인펠터 증후군의 치료 시장은 진단이 조기에 이루어질수록 더 큰 혜택을 얻습니다. 왜냐하면 조기에 진단받은 환자는 혈당 및 지질 조절이 양호하고, 뼈 건강 상태가 더 좋으며, 생식 가능 기간이 더 길게 확보되므로, 장기간에 걸쳐 보다 집중적인 치료를 지속할 수 있기 때문입니다. 일본의 소아용 지침 개정과 유럽 의료기관에서 불임 관련 증상에 대한 관심이 높아지고 있는 점도 환자의 치료 과정을 진전시키고 있습니다. 특히, 과거에는 치료 시작이 상당히 늦어졌던 사춘기 환자들에게서 이 현상이 두드러집니다. 이러한 추세는 태아기 및 소아기 유전자 선별 검사의 확대에 힘입어 더욱 강화되고 있습니다. 왜냐하면 진단을 받은 소아 및 사춘기 환자들은 성인이 되어 불임이 발생한 후에야 클라인펠터 증후군 치료 시장에 진입하는 것이 아니라, 체계적인 모니터링을 거쳐 평생에 걸친 관리로 전환될 가능성이 높기 때문입니다.

경구용 및 지속형 테스토스테론 제제를 통한 복약 순응도 향상

이 시장은 테스토스테론 요법이 오랫동안 안고 있던 상업적 과제 중 하나인, 즉 치료가 불편하거나 의료기관 방문에 의존해야 하는 경우 발생하는 치료 지속성 저하 문제를 해결하는 제제의 발전 덕분에 혜택을 보고 있습니다. 2025년 7월, FDA는 KYZATREX의 처방 정보를 개정하여 혈압 상승과 관련된 박스 경고를 삭제했습니다. 이로써 성인 성선 기능 저하증 관리에 있어 광범위한 처방에 대한 큰 장벽이 제거되었습니다. XYOSTED 역시 재택 치료로의 전환을 보여주는 중요한 사례로 자리매김하고 있습니다. 해당 피하 자가주사제의 제형은 주 1회 자가 투여를 가능하게 했으며, 첨부 문서의 갱신을 통해 진료소에서의 정기적인 주사 절차를 피하고자 하는 환자에게 바람직한 치료 프로파일이 유지되었기 때문입니다. 이러한 변화는 상업적으로 중요한데, 이는 재택에서 복용할 수 있는 경구제나 자가 주사제의 제형이 전문 내분비 센터 이외의 처방 의사층을 확대하고, 상태가 안정된 환자에게 원격 진료를 통한 사후 관리를 보다 현실적으로 만들어 주기 때문입니다.

클라인펠터 증후군 치료 시장은 여전히 장시간 작용형 주사제에 크게 의존하고 있으며, 덴마크의 처방 추적 데이터에 따르면 비경구 제제가 테스토스테론 사용의 주류를 이루고 있습니다. 이는 새로운 제형이 공백인 카테고리에 진입하는 것이 아니라, 뿌리 깊은 습관에 도전하고 있음을 의미합니다. 그럼에도 불구하고, 병원 방문이나 진료 예약, 치료 계획의 복잡성을 줄이기 위한 모든 노력은 복약 순응도 향상으로 이어지며, 복약 순응도의 향상은 클라인펠터 증후군 치료 시장에서 평생에 걸친 호르몬 요법의 상업적 가치를 직접적으로 높이는 결과를 가져옵니다.

불임 치료 및 다직종 연계 치료에 따른 고액의 본인 부담 비용

환자가 불임 치료, 전문의 진찰, 장기적인 모니터링 비용을 스스로 부담해야 하는 경우, 시장은 여전히 잠재적 수요를 잃게 됩니다. 왜냐하면, 반복 주기를 고려하기 전부터 종합적인 치료 모델은 비용이 많이 들기 때문입니다. 강력한 상환 제도가 없는 시장은 가장 큰 제약에 직면해 있습니다. 마이크로 TESE, ICSI, 호르몬 요법, 영상 진단 및 다학제적 진료는 중산층 가정이 장기적으로 감당하기 어렵기 때문입니다. 이는 특히 큰 제약이 됩니다. 왜냐하면 현재 임상적으로 권장되는 모델은 단순한 처방전 발급에 그치지 않고, 내분비학, 비뇨기과, 유전학, 심리학, 그리고 심대사계의 추적 관찰까지 포괄하고 있기 때문입니다. 그 결과, 종합적인 치료는 여전히 3차 의료기관에 집중되어 있으며, 많은 환자들이 대사증후군, 골다공증, 생식 관련 문제에 대해 연계된 관리가 아닌 단편적이거나 일시적인 치료만 받고 있는 것이 현실입니다.

또한, 이 시장은 불임 치료와 테스토스테론 투여 순서와 관련된 문제로 인해 제약을 받고 있습니다. 조기 테스토스테론 사용은 잔존하는 정자 형성을 억제할 가능성이 있기 때문에 임상의와 가족은 특정 치료를 유지하기 위해 다른 치료를 미루어야 하는 시점을 결정해야 하는 상황에 직면하게 됩니다. 게다가, 질환 특이적인 파이프라인은 여전히 부족한 상황이기 때문에 대부분의 상업적 활동은 보험사와의 보다 강력한 협력을 정당화할 수 있는 광범위한 전용 혁신의 물결이 아니라, 적응형 테스토스테론 제제나 불임 치료 기술에 의존한 채로 남아 있습니다.

부문별 분석

2025년 기준으로 테스토스테론 대체 요법(TRT)은 클라인펠터 증후군 치료 시장의 45.1%를 차지하고 있으며, 진단받은 환자의 대부분이 장기적인 성선 기능 저하증을 관리하기 위해 결국 호르몬 치료를 필요로 하기 때문에 TRT는 주요 치료 범주로서의 위상을 유지했습니다. TRT 분야에서는 장시간 작용형 주사용 테스토스테론이 여전히 임상에서 중심적인 위치를 차지하고 있지만, 경구 및 피하 투여 옵션이 늘어남에 따라 처방 의사의 범위가 확대되고, 의료기관에 의존하여 투여해야 할 필요성이 줄어들고 있습니다. 경피 흡수형 겔은 사춘기 시작에 있어 계속해서 중요한 역할을 하고 있습니다. 이는 유연한 용량 증량이 다량의 저장형 제제를 통한 노출보다 사춘기 호르몬 유도의 점진적인 특성에 더 적합하기 때문입니다. 비강용 테스토스테론 및 이식형 펠릿은 여전히 틈새 시장에 머물러 있지만, 다양한 투여 방식이나 복약 순응도 지원이 필요한 환자들에게 치료 선택의 폭을 넓히는 데 기여하고 있습니다. 클라인펠터 증후군 치료 시장에는 환자의 치료 과정 전반에 걸쳐 언어 및 신경 발달상의 문제가 여전히 흔히 나타나기 때문에 지속적인 수요를 창출하는 지지 요법 및 발달 지원 요법도 포함되어 있습니다.

불임 치료 시장 규모는 2026년부터 2031년까지 연평균 성장률(CAGR) 7%로 확대될 것으로 예상되며, 수익 기반은 작지만 가장 빠르게 성장하는 치료 분야가 될 것입니다. 이러한 성장은 마이크로 TESE와 ICSI의 보급, 정자 채취 전 호르몬 최적화의 광범위한 시행, 그리고 치료 과정의 초기 단계에서 이루어지는 보다 충실한 불임 상담과 밀접한 관련이 있습니다. 동일 주기 내 신선한 정자 사용에 대한 임상적으로 실용 가능한 대안으로서 냉동 보존을 뒷받침하는 근거는 일정 조정에 따른 마찰을 줄여주며, 불임 치료 프로그램이 시술의 시급성이 낮은 환자를 더 많이 수용할 수 있게 해줍니다. 외과적 치료 및 동반 질환 관리는 특히 불임 검사를 통해 광범위한 내분비 및 생식 관련 요구 사항이 드러나 협동적인 개입이 필요한 경우, 시술에 기반한 수익원을 한층 더 확대합니다. 그 결과, 클라인펠터 증후군 치료 시장에서 불임 치료가 TRT를 대체하는 것이 아니라, 지속적인 호르몬 치료에 앞서 또는 이와 병행하여 고부가가치 단계를 추가함으로써 평생에 걸친 치료의 연속성을 확대하게 됩니다.

2025년 클라인펠터 증후군 치료 시장 규모에서 주사제는 49.2%를 차지했습니다. 이는 병원 방문 횟수를 줄이면서도 안정적인 호르몬 노출을 실현하는 운데카노에이트형 테스토스테론 및 기타 데포 제제에 대한 오랜 선호도를 반영한 것입니다. 이 투여 경로는 특히 북미와 유럽에서 장기 작용형 근육 내 주사 요법의 처방 실적이 오래되었고, 명확한 모니터링 절차가 확립되어 있어 의료기관의 내분비 진료에 깊이 뿌리내리고 있습니다. 이 투여 경로의 지속성은 의사의 숙련도에 기인하기도 합니다. 왜냐하면, 데포 요법으로 상태가 안정된 환자의 경우, 편의성이나 내약성이 문제가 되지 않는 한 치료법을 변경해야 할 압박은 줄어들기 때문입니다. 따라서 클라인펠터 증후군 치료 시장에서는 많은 성인 환자, 특히 전문의의 진료 경로를 통해 치료 시작이 늦어진 환자의 경우, 여전히 주사제가 기본적인 투여 경로로 자리 잡고 있습니다. 이러한 확고한 기반이 마련되어 있기 때문에 새로운 환자층이 재택 치료 옵션에 큰 관심을 보인다고 하더라도 투여 경로의 구성은 급격하게 변화하기보다는 서서히 변화해 나갈 것입니다.

경구 및 구강 점막 흡수형 테스토스테론 제제는 2031년까지 연평균 성장률(CAGR) 6.5%를 나타낼 것으로 예측되며, 이는 클라인펠터 증후군 치료 시장에서 가장 빠르게 성장하고 있는 투여 경로가 될 것입니다. KYZATREX는 이러한 변화를 뒷받침했습니다. 2025년 적응증 확대에 따라 해당 제품의 처방 패턴이 개선되어, 보다 폭넓은 임상 현장에서 경구 요법을 고려하기가 쉬워졌기 때문입니다. 경피 흡수형 제품은 소아에서 성인으로의 전환기 관리에서 확고한 입지를 유지하고 있습니다. 이 분야에서는 더 세밀한 용량 조절이 유용하며, 치료 시작도 더 신중하게 이루어지는 경향이 있습니다. 비강 내 투여용 테스토스테론 제제는 서방형 제제에 노출되거나 주사로 인한 불편함을 피하고자 하는 환자들에게 선호되고 있습니다. 한편, 투여 간격이 매우 길어 치료의 지속성을 높이는 측면에서 이식형 펠릿 제제는 여전히 중요한 위치를 차지하고 있습니다. 향후 편의성, 유연성 및 가정 내 사용이 클라인펠터 증후군 치료 시장에서 더 큰 점유율을 차지하게 될 가능성이 있지만, 이러한 성장은 주사제의 우위를 배제하는 것이 아니라 이를 기반으로 이루어질 것으로 보입니다.

지역별 분석

2025년 기준으로 북미는 클라인펠터 증후군 치료 시장의 45.2%를 차지하며, 이 시장에서 가장 큰 비중을 차지하는 지역입니다. 이는 미국에서 테스토스테론 사용률이 높고, 불임 치료 인프라가 잘 갖춰져 있으며, 새로운 경구제나 자가 주사제의 도입이 조기에 이루어지고 있기 때문입니다. 2025년 KYZATREX에 대한 FDA의 적응증 확대 및 XYOSTED의 지속적인 위상은 처방에 대한 신뢰도를 높여주며, 특정 성인 환자에게 있어 재택 중심의 사후 관리를 보다 실용적으로 만들어 주고 있습니다. 미국은 제품 공급이 가장 충실하고, 내분비학, 생식 의학, 원격 의료 각 분야가 가장 견고하게 연계되어 있어 클라인펠터 증후군 치료 시장에서 핵심 국가로서의 위상을 유지하고 있습니다. 캐나다는 체계적인 소개 제도를 통해 시장을 뒷받침하고 있는 반면, 멕시코는 희귀질환에 대한 지원이 제한적이고 치료 빈도도 낮기 때문에 시장 점유율은 비교적 낮은 임베디드니다.

유럽은 확립된 임상 지침, 엄격한 추적 관찰 기준, 그리고 진단을 받은 환자를 지속적으로 돌보는 보험 급여 제도에 힘입어 클라인펠터 증후군 치료 시장에서 두 번째로 큰 규모를 자랑하는 지역입니다. 프랑스와 독일은 호르몬 요법의 보험 적용과 전문의 진료 접근성이 장기 관리 과정에서 발생할 수 있는 치료 중단 위험을 줄여주어, 이 지역에 보다 예측 가능한 치료 기반을 마련해 주고 있다는 점에서 특히 두드러집니다. 또한, 무정자증을 동반한 클라인펠터 증후군 환자들에게 마이크로 TESE 시술이 점점 더 보편화됨에 따라, 독일, 영국, 프랑스, 이탈리아, 스페인의 각국 불임 치료 센터들도 해당 지역에서의 역할을 강화하고 있습니다. 조기 생식 능력 평가와 장기적인 내분비 모니터링에 대한 지속적인 관심이 유럽의 임상적 입지를 강화하고 있으며, 이 모든 요소가 클라인펠터 증후군 치료 시장에서 평생 치료의 깊이를 더하고 있습니다.

아시아태평양은 2026년부터 2031년까지 연평균 성장률(CAGR) 5.8%를 나타낼 것으로 예측되며, 클라인펠터 증후군 치료 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 일본은 그 성장의 중심적인 역할을 담당하고 있습니다. 2025년 소아 내분비 지침에 따라 체계적인 사춘기 모니터링과 호르몬 요법의 조기 시작이 공식적으로 규정됨에 따라, 기존의 진료 관행에 비해 수년 더 빨리 환자를 치료로 이끌 수 있게 되었기 때문입니다. 동아시아 전역에서는 태아기 및 소아기 선별검사의 확대에 따라 조기 치료가 점차 확대되고 있습니다. 한편, 진단을 충분히 받지 못한 수많은 성인 환자가 존재하며, 향후 치료로 넘어갈 여지는 여전히 많이 남아 있습니다. 중동 및 아프리카은 클라인펠터 증후군 치료 시장에서 아직 발전 단계에 있지만, GCC 국가들에서 불임에 대한 인식이 높아지고 전문 의료 센터가 확대됨에 따라 조기 치료에 대한 수요가 발생하고 있습니다. 남미에서는 브라질과 아르헨티나의 도시 지역을 중심으로 여전히 비용 문제와 정책 지원 부족에 직면해 있으며, 생식 의료 체계는 개선되고 있지만 치료의 보급에는 한계가 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the klinefelter syndrome treatment market size was valued at USD 1.41 billion in 2025 and is estimated to grow from USD 1.48 billion in 2026 to reach USD 1.86 billion by 2031, at a CAGR of 4.65% during the forecast period (2026-2031).

This report is Segmented by Treatment Type (TRT, Fertility, Supportive, Surgical), Route of Administration (Injectable, Transdermal, Oral/Buccal, Intranasal, Implantable), End User (Hospitals, Endocrinology Clinics, Fertility Clinics, Home Care, Others), Age Group (Children, Adolescents, Adults), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts are in Value (USD).

Global Klinefelter Syndrome Treatment Market Trends and Insights

Earlier Diagnosis via Rising Clinician and Patient Awareness

The Klinefelter syndrome treatment market continues to be shaped by a diagnosis gap that remains unusually wide for a condition this common, with fewer than 50% of affected males identified during their lifetime and median diagnosis still concentrated between ages 28 and 31. That late timing matters because many men only enter care during infertility workups, which delays hormonal support, bone protection, metabolic follow-up, and fertility planning that could have started years earlier. Since 2024, the diagnostic toolkit has improved as machine-learning approaches using electronic health records and hormone profiles moved closer to practical early identification in general practice, which shifts case finding away from late specialist referral.

The Klinefelter syndrome treatment market benefits when diagnosis happens earlier because earlier-identified patients have better glycolipid control, stronger bone health, and more usable fertility windows, which supports longer and more intensive treatment use over time. Updated pediatric guidance in Japan and stronger attention to fertility-related presentation in European centers are also moving the patient journey forward, especially for adolescents who would previously have entered treatment much later. The same trend is reinforced by expanding prenatal and pediatric genetic screening, because diagnosed children and adolescents are more likely to move into structured monitoring and then lifelong care rather than entering the Klinefelter syndrome treatment market only after adulthood infertility appears.

Better Adherence from Oral and Long-Acting Testosterone Formats

The market is gaining from formulation progress that addresses one of testosterone therapy's oldest commercial problems, which is poor persistence when treatment is inconvenient or clinic dependent. In July 2025, the FDA revised the prescribing information for KYZATREX and removed the boxed warning for blood pressure increases, which lowered a meaningful barrier to broader prescribing in adult hypogonadism management. XYOSTED also remained an important example of the home-based shift, because its subcutaneous autoinjector format supports weekly self-administration and its label update preserved a favorable treatment profile for patients who prefer to avoid clinic injection routines. These changes matter commercially because at-home oral and self-injected formats expand the prescriber base beyond specialist endocrinology centers and make telehealth follow-up more practical for stable patients.

The Klinefelter syndrome treatment market still relies heavily on long-acting injectables, and Danish prescription tracking showed that parenteral formulations remained the dominant mode of testosterone use, which means new formats are challenging a strong installed habit rather than entering an empty category. Even so, every step that reduces travel, clinic scheduling, and regimen complexity supports better adherence, and better adherence directly increases the commercial value of lifelong hormonal care in the Klinefelter syndrome treatment market.

High Out-of-Pocket Cost of Fertility and Multidisciplinary Care

The market still loses potential demand when patients must pay for fertility procedures, specialist consultations, and long-term monitoring out of pocket, because the full care model is expensive even before repeated cycles are considered. Markets without strong reimbursement structures face the greatest limitation, since micro-TESE, ICSI, hormonal treatment, imaging, and multispecialty reviews are difficult to sustain for middle-income households over time. This is especially restrictive because the clinically preferred model now spans endocrinology, urology, genetics, psychology, and cardiometabolic follow-up rather than a single prescription encounter. The commercial effect is that comprehensive care remains concentrated in tertiary centers, while many patients receive fragmented or episodic treatment for metabolic syndrome, osteoporosis, and reproductive issues instead of coordinated management.

The market is also restrained by the fertility and testosterone sequencing problem, because early testosterone use can suppress residual spermatogenesis and forces clinicians and families to make timing decisions that may delay one part of care to preserve another. On top of that, the disease-specific pipeline remains thin, so most commercial activity still depends on adapted testosterone formats and fertility technologies rather than a broader wave of dedicated innovation that could justify stronger payer engagement.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Fertility Success through Micro-TESE plus ICSI

- Broader Reimbursement and Rare-Disease Policy Support

- Persistent Underdiagnosis and Late Referral in Primary Care

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Testosterone replacement therapy held 45.1% of the Klinefelter syndrome treatment market share in 2025, which kept it as the leading treatment category because most diagnosed patients ultimately require hormone support for long-term hypogonadism management. Long-acting injectable testosterone remained the clinical anchor within TRT, but oral and subcutaneous options are expanding the prescriber base and lowering the need for clinic-dependent administration. Transdermal gels keep an important role in pubertal initiation because flexible dose escalation fits the gradual nature of adolescent hormonal induction better than large depot exposure. Intranasal testosterone and implantable pellets remain smaller niches, but they help broaden the treatment toolkit for patients who need different dosing patterns or adherence support. The Klinefelter syndrome treatment market also includes supportive and developmental therapies that generate recurring demand because language and neurodevelopmental issues remain common across the patient journey.

The market size for fertility treatment is projected to grow at 7% CAGR from 2026 to 2031, which makes it the fastest-expanding treatment category even though it starts from a smaller revenue base. That growth is tied to the normalization of micro-TESE plus ICSI, wider use of hormonal optimization before sperm retrieval, and stronger fertility counseling earlier in the patient pathway. Evidence supporting cryopreservation as a clinically workable alternative to same-cycle fresh use reduces scheduling friction and helps fertility programs serve more patients with less procedural urgency. Surgical care and comorbidity management add another layer of procedure-based revenue, especially when fertility workups uncover broader endocrine and reproductive needs that require coordinated intervention. The result is that fertility care is not replacing TRT within the Klinefelter syndrome treatment market, but instead extending the lifetime sequence of care by adding a high-value phase before or alongside ongoing hormonal treatment.

Injectables accounted for 49.2% of the Klinefelter syndrome treatment market size in 2025, reflecting the long-standing preference for testosterone undecanoate and other depot formulations that deliver stable hormonal exposure with less frequent clinic visits. This route remains deeply embedded in institutional endocrinology practice, especially in North America and Europe where long-acting intramuscular therapy has a long prescribing history and clear monitoring routines. The route's staying power also comes from physician familiarity, because once stable patients are established on depot therapy there is less pressure to change unless convenience or tolerability becomes a concern. The Klinefelter syndrome treatment market therefore still relies on injectables as the default route for many adult patients, particularly those entering care late through specialist channels. That entrenched base means route mix will change gradually rather than abruptly, even as new patient cohorts show stronger interest in home-based options.

Oral and buccal testosterone is forecast to grow at 6.5% CAGR through 2031, which makes it the fastest-rising administration route in the Klinefelter syndrome treatment market. KYZATREX has helped that shift because label refinement in 2025 improved the product's prescribing profile and made oral therapy easier to consider in broader practice settings. Transdermal products keep a stable place in pediatric-to-adult transition care, where smaller dose steps are useful and treatment initiation is often more cautious. Intranasal testosterone appeals to patients who want to avoid depot exposure and injection discomfort, while implantable pellets remain relevant where very long dosing intervals improve persistence. Over time, convenience, flexibility, and home use are likely to take a larger share of the Klinefelter syndrome treatment market, but that growth is building on injectable primacy rather than removing it.

Geography Analysis

North America held 45.2% of the Klinefelter syndrome treatment market share in 2025, making it the largest regional contributor because the United States combines high testosterone use, advanced fertility infrastructure, and early uptake of new oral and self-injection formats. The 2025 FDA label refinements for KYZATREX and the continued positioning of XYOSTED support broader prescribing confidence and make home-centered follow-up more practical for selected adult patients. The United States remains the core national engine inside the Klinefelter syndrome treatment market because it has the deepest product availability and the strongest mix of endocrinology, reproductive medicine, and telehealth channels. Canada adds support through structured referral systems, while Mexico contributes a smaller share due to more limited rare-disease support and lower treatment intensity.

Europe is the second-largest region in the Klinefelter syndrome treatment market, supported by established clinical guidance, disciplined follow-up norms, and reimbursement structures that keep diagnosed patients in care. France and Germany stand out because reimbursed hormonal treatment and specialist access reduce interruption risk in long-term management, which gives the region a more predictable treatment base. Fertility centers across Germany, the United Kingdom, France, Italy, and Spain are also strengthening the region's role as micro-TESE becomes more routine in azoospermic Klinefelter syndrome patients. Europe's clinical position is reinforced by continued attention to early fertility evaluation and long-term endocrine surveillance, both of which raise lifetime treatment depth inside the Klinefelter syndrome treatment market.

Asia-Pacific is projected to grow at 5.8% CAGR from 2026 to 2031, making it the fastest-growing region in the Klinefelter syndrome treatment market. Japan is central to that growth because the 2025 pediatric endocrine guidance formalized structured puberty monitoring and earlier hormonal initiation, which can bring patients into care years ahead of prior practice. Across East Asia, wider prenatal and pediatric screening is gradually improving early entry, while large adult underdiagnosed populations still leave meaningful room for future conversion into treatment. The Middle East and Africa remains a nascent part of the Klinefelter syndrome treatment market, although fertility awareness and specialist center expansion in GCC countries are creating early procedure demand. South America, led by urban centers in Brazil and Argentina, continues to face cost barriers and weaker policy support, which limits treatment penetration despite improving reproductive healthcare capacity.

- Abbvie

- Antares Pharma

- Besins Healthcare

- Cook Group

- The Cooper Companies

- Endo International

- Ferring Pharmaceuticals

- FUJIFILM

- Hamilton Thorne Ltd.

- Hikma Pharmaceuticals

- Lupin

- Marius Pharmaceuticals, Inc.

- Merck KGaA / EMD Serono

- Organon

- Pfizer

- Sun Pharmaceuticals Industries

- Tolmar Inc.

- Vitrolife

- XY Therapeutics ApS

- ZEISS Microscopy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Earlier Diagnosis via Rising Clinician and Patient Awareness

- 4.2.2 Better Adherence from Oral and Long-Acting Testosterone Formats

- 4.2.3 Expanding Fertility Success Through Micro-TESE Plus ICSI

- 4.2.4 Broader Reimbursement and Rare-Disease Policy Support

- 4.2.5 Prenatal and Pediatric Genetic Screening Widening Lifetime Treatment Pools

- 4.2.6 Cardiometabolic and Bone-Health Surveillance Increasing Long-Term Care Intensity

- 4.3 Market Restraints

- 4.3.1 High Out-Of-Pocket Cost of Fertility and Multidisciplinary Care

- 4.3.2 Persistent Underdiagnosis and Late Referral in Primary Care

- 4.3.3 Testosterone-Fertility Sequencing Dilemma

- 4.3.4 Thin Disease-Specific Innovation Pipeline

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Supplier Power

- 4.7.2 Buyer Power

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Treatment Type

- 5.1.1 Testosterone Replacement Therapy

- 5.1.1.1 Injectable Testosterone

- 5.1.1.2 Transdermal Testosterone

- 5.1.1.3 Oral / Buccal Testosterone

- 5.1.1.4 Intranasal Testosterone

- 5.1.1.5 Implantable Testosterone

- 5.1.2 Fertility Treatment

- 5.1.2.1 Pre-treatment hormonal optimization

- 5.1.2.2 Surgical sperm retrieval

- 5.1.2.3 Assisted reproductive technology

- 5.1.2.4 Donor sperm pathway

- 5.1.3 Supportive and Developmental Therapies

- 5.1.4 Surgical and Comorbidity Management

- 5.1.1 Testosterone Replacement Therapy

- 5.2 By Route of Administration

- 5.2.1 Injectable

- 5.2.2 Transdermal

- 5.2.3 Oral / Buccal

- 5.2.4 Intranasal

- 5.2.5 Implantable

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Endocrinology clinics

- 5.3.3 Fertility and urology centers

- 5.3.4 Home-based care and telehealth monitoring

- 5.3.5 Other End Users

- 5.4 By Age Group

- 5.4.1 Children

- 5.4.2 Adolescents

- 5.4.3 Adults

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Antares Pharma, Inc.

- 6.3.3 Besins Healthcare

- 6.3.4 Cook Medical

- 6.3.5 CooperSurgical, Inc.

- 6.3.6 Endo Pharmaceuticals Inc.

- 6.3.7 Ferring Pharmaceuticals

- 6.3.8 FUJIFILM Irvine Scientific, Inc.

- 6.3.9 Hamilton Thorne Ltd.

- 6.3.10 Hikma Pharmaceuticals PLC

- 6.3.11 Lupin Limited

- 6.3.12 Marius Pharmaceuticals, Inc.

- 6.3.13 Merck KGaA / EMD Serono

- 6.3.14 Organon & Co.

- 6.3.15 Pfizer Inc.

- 6.3.16 Sun Pharmaceutical Industries Ltd.

- 6.3.17 Tolmar Inc.

- 6.3.18 Vitrolife AB

- 6.3.19 XY Therapeutics ApS

- 6.3.20 ZEISS Microscopy

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

(주말 및 공휴일 제외)