|

시장보고서

상품코드

2064008

고효능 API 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)High Potency APIs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

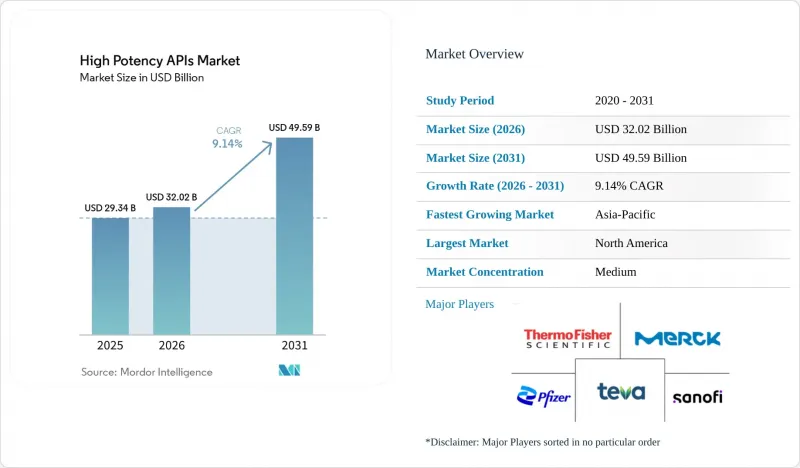

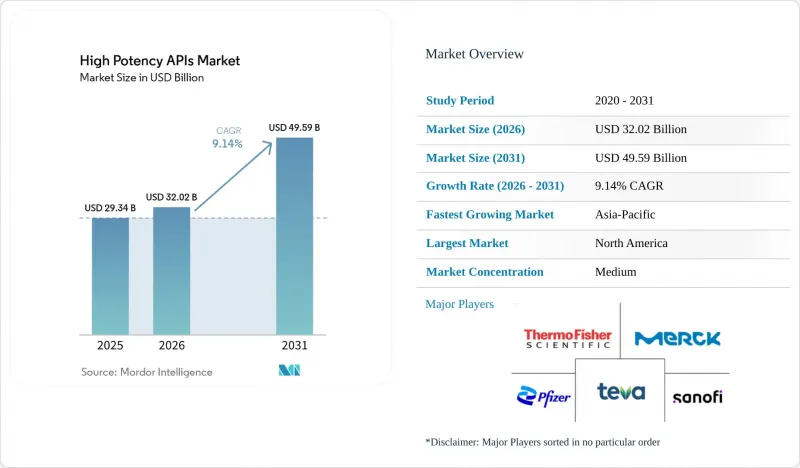

Mordor Intelligence에 의하면, 고효능 API 시장 규모는 2025년에 293억 4,000만 달러, 2026년에 320억 2,000만 달러, 2031년까지 495억 9,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 9.14%로 성장할 전망입니다.

본 보고서는 제품 유형(혁신적인 고효능 API 및 제네릭 고효능 API), 용도(종양학, 호르몬 장애 등), 합성 경로(합성 고효능 API 및 생명공학 고효능 API), 제조업체 유형(자체 제조업체 및 수탁 제조업체), 그리고 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 고효능 API 시장 동향 및 인사이트

만성 질환 및 종양성 질환의 유병률 증가

암 관련 API는 이미 전체 수요의 73.23%를 차지하고 있으며, 2024년 FDA의 신규 분자 실체(NME) 승인 건 중 28%가 고효능 범주에 분류되었습니다. 세마글루티드와 같은 신흥 대사성 질환 치료용 블록버스터는 2024년에 1억 3,890만 달러의 매출을 기록하며, 종양학 이외의 분야에서도 상업적인 성장세를 보였습니다. 항체-약물 복합체(ADC)에 포함된 세포 독성 페이로드의 경우, 10µg/m3 미만의 직업적 노출 한계치가 요구되므로, 소규모 공장에서는 대응할 수 없는 고밀폐 시설이 필수적입니다. 세계적인 고령화로 인해 만성 질환의 유병률이 더욱 높아지고, 치료 기간도 길어짐에 따라 API의 기초 수요량은 증가하고 있습니다. 신속 승인 절차의 도입으로 개발 주기가 단축됨에 따라, 후원사는 임상 계획의 초기 단계에서 적절한 생산 용량을 확보해야 합니다.

위탁 개발·제조 기관(CDMO)의 확대

고위험 공정을 외부에 위탁하는 것을 선호하는 스폰서의 경향에 힘입어, 전 세계 CDMO 부문은 성장이 예상됩니다. 사내에 격리 인프라를 갖추지 않은 중소 바이오기술 기업들이 현재 HPAPI 아웃소싱 물량의 대부분을 차지하고 있어, 서비스 제공업체의 수주 잔고를 더욱 끌어올리고 있습니다. 『BIOSECURE법』은 미국 기업들에게 2032년까지 중국의 CDMO와의 관계를 단절할 것을 의무화하고 있으며, 이로 인해 인도 및 유럽공급업체들에게 새로운 수요가 창출되고 있습니다. Aurigene와 Aragen Life Science와 같은 인도 기업들은 2024년에 두 자릿수 증가율을 기록한 문의 급증을 보고했습니다. 따라서 전문 CDMO는 세포 독성 시험 시설, 연속 유동 유닛 및 산업보건연구소를 동시에 확충해야 합니다. Lonza는 이러한 추이에 맞추어 자원을 조정하기 위해 전문 모달리티 부문을 포함한 3개의 사업 부문으로 재편했습니다.

세계 각국의 엄격한 규제 및 산업안전 기준

2025년 1월에 발효될 EMA의 개정된 ‘변경 규정’에 따라, 승인 후 변경 사항에 대한 보다 상세한 검증 기록이 요구됨에 따라 문서 작성에 소요되는 시간이 길어지고 있습니다. 미국 OSHA의 위험 물질 관련 지침에 따라 다단계 에어록 및 전용 개인보호장비(PPE)의 사용이 의무화되어 있어, 기존 의약품에 비해 생산 효율이 최대 15% 저하되고 있습니다. 2024년 8월부터 시행되는 PIC/S 부속서 1은 무균 격리 공정에 품질 위험 관리를 도입하는 것으로, 기존 공장에서의 개조 프로젝트를 불가피하게 만들고 있습니다. 중국의 스파이 방지법 확대에 따라 일부 유럽 검사 기관이 현지 감사를 중단함에 따라, 중국산 중간체의 출하 지연 위험이 발생하고 있습니다. 이러한 요인들이 복합적으로 작용하여 규정 준수 예산이 늘어나고, 확립된 규제 대응 팀을 보유한 기존 기업들이 유리한 입장에 서 있습니다.

부문별 분석

2025년 매출의 대부분은 혁신적인 화합물에 의해 창출되었으며, 이는 전체의 61.89%를 차지했습니다. 이는 높은 고정비를 상쇄할 수 있는 높은 수익을 창출하는 특허 보호 자산 덕분입니다. FDA 승인이 지속적으로 이어지고 있어(2024년에는 50건의 신규 분자(NME)가 승인되었으며, 그중 91%가 저분자 화합물), 혁신 파이프라인이 유지되고 있습니다. 최고 수준의 자산을 지원하는 CDMO는 수년에 걸친 독점권 패키지를 협상함으로써 생산 능력의 수익화를 확실하게 하고 있습니다.

제네릭 HPAPI 시장은 규모는 작지만, 블록버스터급 항암제의 특허 만료에 따라 2031년까지 연평균 성장률(CAGR) 11.18%를 기록하며 성장할 전망입니다. Aarti Pharmalabs와 같은 전문 제조업체는 2023-24 회계연도에 54종의 API를 상용화했으며, 이는 격리 성능을 저해하지 않으면서도 복잡한 공정을 재현할 수 있는 역량이 점차 성숙해지고 있음을 보여줍니다.

2025년 지출의 72.53%를 차지한 것은 종양학 분야였으며, 이는 본질적으로 철저한 격리가 필요한 세포독성 약물의 투여 요건을 반영한 것입니다. 론자의 스위스 슈타인 캠퍼스에서는 후원사 수요에 부응하기 위해 ADC 생산 능력 확장이 지속적으로 이루어지고 있습니다.

녹내장 및 더 광범위한 안과 분야는 규모는 비교적 작지만, 2031년까지 연평균 성장률(CAGR)이 12.61%로 가장 높은 성장세를 보이고 있습니다. 이는 2025년 10월 PDUFA(신약 심사료법) 기한을 앞두고, FDA로부터 신약 승인 신청(NDA) 접수를 확보한 Glaukos사의 Epioxa와 같은 차세대 서방형 임플란트에 힘입은 결과입니다.

지역별 분석

북미는 총 매출에서 압도적인 점유율을 차지하고 있으며, 탄탄한 혁신 기업 생태계와 선진적인 규제 환경을 바탕으로 2025년 수요의 39.62%를 차지하고 있습니다. 화이자가 4억 6,500만 달러 규모로 진행하는 칼라마주 공장 확장 사업은 국내 API 생산 능력에 대한 화이자의 확고한 의지를 입증하고 있습니다. CARES법에 따른 자금 지원과 주 차원의 인센티브가 자본 부담의 일부를 상쇄하는 한편, BIOSECURE법의 2032년이라는 기한이 생산의 국내 복귀를 더욱 가속화하고 있습니다. 캐나다가 FDA의 CGMP 기준을 준수하고 있어 국경을 초월한 원활한 유통이 가능해졌으며, 피라마르 파마 솔루션즈는 최근 오로라 사업장의 HPAPI 생산 능력 확대를 위해 2,500만 캐나다 달러를 투자했습니다. 고효능 API 시장에서는 북미의 기존 시설을 Annex 1 및 OSHA의 개정 기준에 부합하도록 하기 위한 브라운필드 개보수 작업이 계속해서 진행되고 있습니다.

아시아·태평양 지역은 2031년까지의 연평균 성장률(CAGR)이 10.32%로, 지역별로는 가장 높은 성장세를 보이고 있습니다. 인도의 CDMO 부문은 유럽 및 미국 스폰서의 다각화에 힘입어 성장하고 있습니다. 하이데라바드와 비샤카파트남에서의 시설 확충은 인도의 생산 연계형 인센티브 제도의 지원을 받아, 세포독성 약물 및 펩타이드 합성을 주축으로 하고 있습니다. 중국은 비용 면에서 우위를 유지하고 있지만, ‘반스파이법’ 시행에 따라 규정 준수 측면에서 과제에 직면해 있으며, 일부 다국적 기업들은 공급처 다각화를 추진하고 있습니다. 싱가포르의 바이오의약품 이니셔티브와 한국의 규제 조화를 통해 아시아태평양(APAC)은 다중 모드 HPAPI 허브로서의 입지를 더욱 공고히 하고 있습니다.

유럽은 특히 복잡한 바이오의약품이나 접합체 분야에서 여전히 매우 중요한 제조 거점입니다. EMA(유럽의약품청)의 ‘변경 규정’은 절차를 명확히 함으로써 EU 전역에 걸친 제품 수명 주기 관리를 용이하게 하고 있습니다. EU 역외에 위치하면서도 깊이 통합된 스위스에는 유럽의 항체-약물 복합체(ADC) 생산의 핵심을 담당하는 론자(Lonza)사의 주력 거점이 있습니다. 유럽연합 집행위원회의 ‘중요 의약품법’은 전략적 지원 대상인 270종의 원료를 지정하고 있으며, 공장 개보수 및 생산 능력 확대를 위한 보조금 지원의 길을 열어주고 있습니다. 매력적인 전력 가격 헤지와 풍부한 인력을 바탕으로, 서유럽의 시설들은 운영 비용이 높음에도 불구하고 경쟁력을 유지하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the high potency aPIs market size is projected to be USD 29.34 billion in 2025, USD 32.02 billion in 2026, and reach USD 49.59 billion by 2031, growing at a CAGR of 9.14% from 2026 to 2031.

This report is Segmented by Product Type (Innovative HPAPIs and Generic HPAPIs), Application (Oncology, Hormonal Disorders, and More), Synthesis Route (Synthetic HPAPIs and Biotech HPAPIs), Manufacturer Type (Captive Manufacturers and Merchant Manufacturers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global High Potency APIs Market Trends and Insights

Increasing Prevalence of Chronic and Oncologic Diseases

Cancer-related APIs already constitute 73.23% of overall demand, and 28% of FDA new molecular entity approvals in 2024 fell into the highly potent category. Emerging metabolic-disorder blockbusters such as semaglutide generated USD 138.90 million in 2024 sales, demonstrating commercial traction beyond oncology. Cytotoxic payloads within antibody-drug conjugates require occupational exposure limits below 10 µg/m3, thereby mandating high-containment installations that smaller plants cannot support. An aging global population further increases chronic-disease prevalence and extends therapy durations, lifting baseline API volumes. Accelerated-approval pathways compress development cycles, compelling sponsors to secure capable manufacturing slots early in clinical planning.

Expansion of Contract Development and Manufacturing Organizations

The global CDMO segment is projected to grow, propelled by sponsors' preference to externalize high-risk processes. Smaller biotech firms lacking internal containment infrastructure now represent a majority of HPAPI outsourcing volume, deepening order books for service providers. The BIOSECURE Act obliges US firms to sever Chinese CDMO links by 2032, directing fresh mandates toward Indian and European vendors; Indian outfits such as Aurigene and Aragen Life Science reported double-digit inquiry spikes in 2024. Specialized CDMOs must therefore scale cytotoxic suites, continuous-flow units, and occupational-hygiene labs in parallel. Lonza has reorganized into three divisions, including a dedicated Specialized Modalities arm, to align resources with this trajectory.

Stringent Global Regulatory and Occupational Safety Standards

EMA's updated Variations Regulation effective January 2025 demands deeper validation records for post-approval changes, lengthening documentation lead-times. OSHA's hazardous-drug directives in the United States oblige multi-stage air-locking and specialized PPE, cutting production efficiency by up to 15% relative to conventional pharmaceuticals. PIC/S Annex 1, enforced from August 2024, embeds quality-risk management into sterile containment, compelling retrofit projects at legacy plants. China's broadened Anti-Espionage Law has prompted some European inspectorates to halt on-site audits, risking delayed release for Chinese-sourced intermediates. Collectively, these layers inflate compliance budgets and favor incumbents with established regulatory affairs teams.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Targeted and Personalized Therapies

- Technological Advancements in High-Containment Manufacturing

- High Capital and Operational Expenditure Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Innovative compounds generated the bulk of 2025 revenue, capturing 61.89% owing to patent-protected assets that deliver premium returns capable of offsetting high fixed costs. Continuous inflows of FDA approvals-50 NMEs in 2024, 91% of which were small molecules-maintain the innovation pipeline. CDMOs supporting first-in-class assets negotiate multi-year exclusivity packages, assuring capacity monetization.

Generic HPAPIs, though smaller, are set to grow at 11.18% CAGR through 2031 as blockbuster oncology agents face expirations. Specialized manufacturers such as Aarti Pharmalabs commercialized 54 APIs in FY 2023-24, signaling maturing capability in replicating complex processes without compromising containment.

The oncology franchise accounted for 72.53% of 2025 spend, reflecting cytotoxic dosing requirements that inherently demand robust containment. Lonza's Stein, Switzerland campus has seen repeated ADC capacity expansions to meet sponsor demand.

Glaucoma and broader ophthalmology segments, though comparatively small, exhibit the fastest momentum at 12.61% CAGR through 2031, aided by next-generation controlled-release implants such as Glaukos's Epioxa, which secured FDA NDA acceptance with an October 2025 PDUFA date.

Geography Analysis

North America dominates gross revenue, absorbing 39.62% of 2025 demand on the back of a dense innovator ecosystem and an advanced regulatory environment. Pfizer's USD 465 million Kalamazoo expansion underscores its entrenched commitment to domestic API capability. CARES-Act funding and state-level incentives offset a portion of the capital burden, while the BIOSECURE Act's 2032 deadline expedites further reshoring. Canada's alignment with FDA CGMP standards allows seamless cross-border distribution, and Piramal Pharma Solutions recently committed CAD 25 million to expand its Aurora HPAPI output. The high-potency APIs market continues to see additional brownfield retrofits that bring legacy North American sites into compliance with Annex 1 and OSHA revisions.

Asia-Pacific registers the highest regional CAGR at 10.32% through 2031. India's CDMO sector is driven by Western sponsor diversification. Facility additions in Hyderabad and Visakhapatnam gear toward cytotoxic and peptide synthesis, supported by India's Production Linked Incentive scheme. China retains a cost-lead position but faces compliance headwinds following the Anti-Espionage Law, leading some multinationals to dual-source. Singapore's biologics initiative and South Korea's regulatory harmonization further cement APAC's stature as a multi-modality HPAPI hub.

Europe remains a pivotal manufacturing node, especially for complex biologics and conjugates. EMA's Variations Regulation harmonizes procedural clarity, easing pan-EU lifecycle management. Switzerland, outside the EU but deeply integrated, hosts Lonza's flagship sites that anchor European antibody-drug conjugate output. The European Commission's Critical Medicines Act lists 270 APIs for strategic support, opening grant pathways for plant retrofits and capacity expansions. Attractive electricity-price hedging and experienced labor pools keep Western European facilities competitive despite higher operating costs.

- Abbvie

- Merck

- Corden Pharma

- Pfizer

- Sanofi - EUROAPI

- SK Biotek

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

- Thermo Fisher Scientific

- Viatris

- Lonza Group

- WuXi App Tec

- Cambrex

- Dishman Carbogen Amcis

- Piramal Group

- Sterling Pharma Solutions

- Siegfried Holding

- Evonik Health Care

- Novasep (Seqens)

- Delpharm

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope Of The Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Chronic and Oncologic Diseases

- 4.2.2 Growing Biopharmaceutical Research and Development Investments

- 4.2.3 Expansion of Contract Development and Manufacturing Organizations

- 4.2.4 Rising Demand for Targeted and Personalized Therapies

- 4.2.5 Technological Advancements in High-Containment Manufacturing

- 4.2.6 Government Incentives and Reshoring Initiatives for Domestic API Production

- 4.3 Market Restraints

- 4.3.1 High Capital and Operational Expenditure Requirements

- 4.3.2 Stringent Global Regulatory and Occupational Safety Standards

- 4.3.3 Dependence on Limited Suppliers for Specialized Raw Materials and Equipment

- 4.3.4 Shortage of Skilled Workforce in High-Potency Manufacturing Facilities

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Buyers

- 4.5.3 Bargaining Power Of Suppliers

- 4.5.4 Threat Of Substitutes

- 4.5.5 Intensity Of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Innovative HPAPIs

- 5.1.2 Generic HPAPIs

- 5.2 By Application

- 5.2.1 Oncology

- 5.2.2 Hormonal Disorders

- 5.2.3 Glaucoma

- 5.2.4 Other Applications

- 5.3 By Synthesis Route

- 5.3.1 Synthetic HPAPIs

- 5.3.2 Biotech HPAPIs

- 5.4 By Manufacturer Type

- 5.4.1 Captive Manufacturers

- 5.4.2 Merchant Manufacturers

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 AbbVie

- 6.3.2 Merck KGaA

- 6.3.3 Corden Pharma

- 6.3.4 Pfizer, Inc.

- 6.3.5 Sanofi - EUROAPI

- 6.3.6 SK Biotek

- 6.3.7 Sun Pharma

- 6.3.8 Teva

- 6.3.9 Thermo Fisher Scientific, Inc.

- 6.3.10 Viatris

- 6.3.11 Lonza

- 6.3.12 WuXi AppTec

- 6.3.13 Cambrex

- 6.3.14 Dishman Carbogen Amcis

- 6.3.15 Piramal Pharma Solutions

- 6.3.16 Sterling Pharma Solutions

- 6.3.17 Siegfried Holding

- 6.3.18 Evonik Health Care

- 6.3.19 Novasep (Seqens)

- 6.3.20 Delpharm

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment