|

시장보고서

상품코드

2064017

플렉서블 LED 모듈 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Flexible LED Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

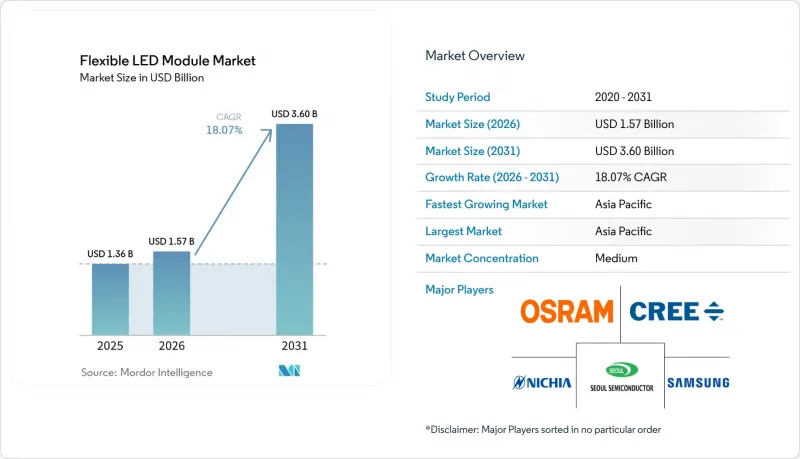

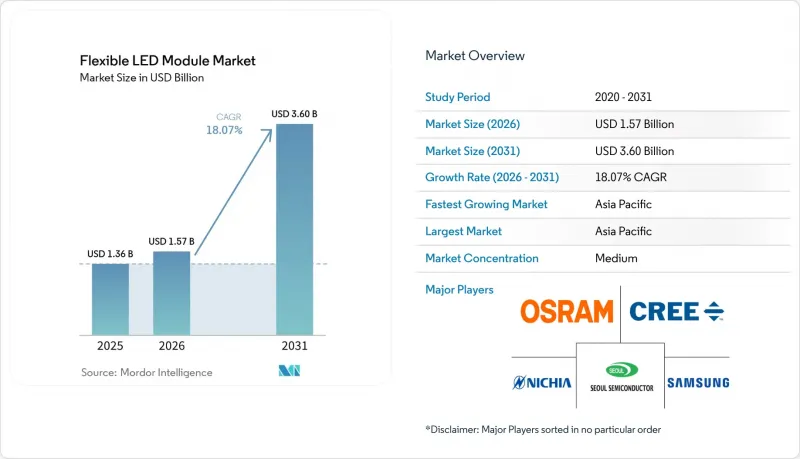

Mordor Intelligence에 의하면, 플렉서블 LED 모듈 시장 규모는 2025년 13억 6,000만 달러에서 2026년에는 15억 7,000만 달러로 확대되어 2031년까지 36억 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 18.07%로 성장할 전망입니다.

본 보고서는 기판 유형(플라스틱계 플렉서블 모듈, 폴리이미드계 모듈 등), 폼 팩터(스트립/선형형 플렉서블 모듈 및 패널/시트형 플렉서블 모듈), 용도(사이니지 및 광고, 자동차용 조명, 웨어러블 및 소비자용 전자기기 등), 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 플렉서블 LED 모듈 시장 동향 및 분석

건축 및 장식 조명 프로젝트에서 플렉서블 LED 스트립의 급속한 보급

플렉서블 스트립은 현재 곡선형 코브, 기둥, 액센트 벽 등에서 기존의 경질 압출 성형 제품을 대체하여, 반경이 불과 10mm에 불과한 곳에서도 이음매 없는 조명을 구현하고 있습니다. 2026년에 발효될 미국 에너지부(DOE)의 고체 조명(SSL) V6.0 규격에서는 150루멘/와트의 광속 효율과 스마트 조광 기능이 의무화되어 있으며, 이에 따라 호텔 및 레스토랑 업계 및 소매 업계에서의 업그레이드 속도가 가속화되고 있습니다. 유럽 표준 EN IEC 60598-1:2024에서는 플리커 및 광생물학적 임계값이 더욱 엄격해졌으며, 인증 취득까지 소요되는 기간은 길어지겠지만, 설계자들은 장기적인 신뢰성에 대한 확신을 더욱 굳히고 있습니다. 칩 온 보드 방식의 네온 대체 스트립은 기존 네온에 비해 전력 소비를 40% 절감하고 50,000시간 이상의 수명을 실현하여, 이러한 변화로 인해 유지보수 예산을 절감할 수 있습니다. -40℃에서 105℃에 이르는 넓은 작동 온도 범위 덕분에 북유럽의 스키 리조트부터 해안 지역의 쇼핑몰에 이르기까지 설치가 가능해져, 유연성이 뛰어난 LED 모듈 시장의 적용 범위를 확대되고 있습니다.

에너지 효율이 높은 간판 및 광고 솔루션에 대한 수요 증가

지자체의 밝기 규제와 전기 요금 급등으로 인해, 사업자들은 태양광 발전 셀을 내장하고 실시간 전력 기록 기능을 갖춘 고효율의 플렉서블 패널로 전환해야 하는 상황에 직면해 있습니다. 캘리포니아주의 ‘Title 24 2025’에 따르면, 옥외 간판의 자동 밝기 조절이 의무화됨에 따라, 150루멘/와트를 초과하는 발광 효율과 일조 센서가 내장된 모듈에 대한 수요가 증가하고 있습니다. 소매업체에 따르면, 곡면 비디오월을 타일 형태의 경질 캐비닛이 아닌 구부릴 수 있는 패널 형태로 출하함으로써 설치 공수가 30% 감소하고, 주요 상권에 위치한 매장의 경우 투자 회수 기간이 2년 미만으로 단축된다고 합니다. CES 2025에서 공개된 4,000니트의 곡면 마이크로 LED 디스플레이 덕분에, 브랜드는 OLED에서는 가시성이 떨어지는 햇빛이 강한 야외에서도 관객에게 다가갈 수 있게 됩니다. 플렉서블 모듈을 통해 구현된 원통형 키오스크나 기둥을 감싸는 듯한 구조는 교통 허브에서 새로운 광고 공간을 개척하여 광고 수익 증대를 촉진합니다.

고가의 첨단 플렉서블 LED 모듈과 경질 대체품의 초기 비용 비교

폴리이미드 모듈은 롤-투-롤 생산 라인이 소량 생산 방식으로 가동되고 고온 폴리머에 의존하고 있기 때문에 FR-4 기판에 비해 여전히 40-60% 정도 비싼 임베디드니다. 곡면 클러스터용 자동차용 미니 LED 백라이트의 비용은 80-120달러로, 이는 경질 LCD 백라이트의 약 2배에 달하고, 가성비 중심 차량에서의 채택을 제한하고 있습니다. 신흥국의 디지털 사이니지 사업자의 경우, 1제곱미터당 300달러가 넘는 설비 투자가 필요하며, 전기 요금이 1kW시당 0.10달러 미만에 그치는 상황에서는 투자 회수 기간이 길어집니다. 1라인당 500만 달러를 초과하는 대량 이송 장치는 자금력이 있는 기업만 진입할 수 있도록 제한함으로써 가격 경쟁의 압력을 약화시키고 있습니다. JEDEC와 같은 실적 규격이 확립되기 전까지는 프로젝트 간 장비 재사용이 제한적이며, 비용 절감 속도는 둔화될 것입니다.

부문별 분석

폴리이미드 모듈 시장은 -40°C에서 125°C의 온도 범위를 견디면서도 180도를 초과해 구부러지는 조종석 디스플레이 및 웨어러블 기기 수요에 힘입어 연평균 성장률(CAGR) 18.56%로 성장하고 있습니다. 폴리이미드 용액용 플렉서블 LED 모듈 시장은 300°C를 넘는 유리전이온도라는 특징을 활용하여, PET나 폴리카보네이트로는 구현하기 어려운 리플로우 프로파일을 실현하고 있습니다. 연속 레이저 전사 기술을 통해 마이크로 LED를 ±10 마이크로미터의 정밀도로 배치할 수 있어, 곡면 대시보드 전체에 걸쳐 밝기 균일성이 확보됩니다. 비용을 중시하는 건축용 조명 분야에서는 플라스틱 계열 기판이 여전히 주류를 이루고 있습니다. 이는 금형 비용이 30% 저렴하고, 굽힘 반경이 20mm 이상이면 기계적 응력이 완화되기 때문입니다. 음성 제어 스마트 홈 시스템이 보급됨에 따라, 더 작은 굽힘 반경과 높은 열 부하에 대한 수요가 증가함에 따라 시장 점유율은 점차 폴리이미드로 이동할 것입니다.

자동차용이 아닌 스트립 조명의 경우, 주변 온도가 60°C 미만이고 기계적인 굽힘이 적은 상황에서는 플라스틱이 여전히 충분한 성능을 발휘합니다. 그러나 수천 개의 구역으로 나뉜 로컬 디밍 기능을 갖춘 미니 LED 백라이트는 플라스틱으로는 효율적으로 방열할 수 없는 핫스팟 전류를 발생시키기 때문에 고급 간판 구매자들은 폴리이미드로 전환하고 있습니다. 하이브리드 금속 코어 플렉스 및 세라믹 충전 폴리머는 2 W m-K를 초과하는 열전도율이 필요한 산업용 하이베이 조명 기구와 같은 틈새 시장을 충족시키고 있습니다. 롤-투-롤 방식의 수율이 향상되고 수지 가격이 하락함에 따라, 2028년 이후에는 비용이 비슷한 수준이 될 것으로 예상되며, 플렉서블 LED 모듈 시장의 더 큰 점유율이 고성능 기판으로 이동할 것입니다.

지역별 분석

아시아태평양은 2025년 매출의 67.89%를 차지해 1위를 기록하고, 중국의 적극적인 생산 능력 확충과 한국 정부의 스마트 LED 분야 3억 5,000만 달러 규모의 경기 부양책에 힘입어 연평균 성장률(CAGR) 18.81%를 나타낼 것으로 예측됩니다. 천셴 광전(Chenxian Optoelectronics)이 유리 기판용 마이크로 LED 생산 능력을 30억 위안(4억 1,700만 달러) 규모로 확장하는 등의 투자는 이 지역의 성장세를 뒷받침하고 있습니다. 대만의 ±1 마이크로미터 이내의 고정밀 양산 기술은 이 섬을 차세대 디스플레이의 수탁 생산 거점으로 확고히 자리매김하게 하고 있습니다.

북미에서는 ‘Title 24 2025’나 ‘IECC 2024’와 같은 엄격한 에너지 규제가 고효율 모듈을 활용한 개조를 촉진하고 있는 반면, 주요 엔터테인먼트 시설에서는 방문객의 참여도를 높이기 위해 곡면형 8K 사이니지가 도입되고 있습니다. 유럽에서는 EN IEC 60598-1 표준을 준수하는 저플리커 및 플리커 프리 플렉서블 스트립을 선호하는 건축 리모델링이 진행되고 있으며, 독일의 고급 자동차 제조업체는 디지털 대시보드의 차별화를 꾀하기 위해 마이크로 LED 클러스터를 탑재하고 있습니다.

남미, 중동 및 아프리카의 점유율은 작지만, 사우디아라비아의 8,770억 달러 규모 인프라 계획이나 대륙 규모의 스포츠 행사를 앞두고 있는 브라질의 새로운 스마트 스타디움 건설과 같은 메가 프로젝트에 힘입어 국지적인 고성장이 나타나고 있습니다. 이 지역에 진출하는 공급업체들은 고온 환경에서의 작동 및 다중 전압 그리드에 대응할 수 있도록 패키지를 맞춤화하고 있으며, 플렉서블 LED 모듈 시장은 장기적인 지역 분산화의 기반을 마련하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the flexible LED module market size is expected to increase from USD 1.36 billion in 2025 to USD 1.57 billion in 2026 and reach USD 3.60 billion by 2031, growing at a CAGR of 18.07% over 2026-2031.

This report is Segmented by Substrate Type (Plastic-Based Flexible Modules, Polyimide-Based Modules, Nd More), Form Factor (Strip/Linear Flexible Modules and Panel/Sheet Flexible Modules), Application (Signage and Advertising, Automotive Lighting, Wearables and Consumer Electronics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Flexible LED Module Market Trends and Insights

Rapid Adoption of Flexible LED Strips in Architectural and Decorative Lighting Projects

Flexible strips now replace rigid extrusions on curving coves, columns, and feature walls, delivering seam-free illumination at radii as small as 10 millimeters. The U.S. Department of Energy's Solid-State Lighting V6.0 specification, effective in 2026, mandates 150 lumens-per-watt efficacy and smart dimming, accelerating upgrades in hospitality and retail. European regulation EN IEC 60598-1:2024 tightens flicker and photobiological thresholds, lengthening certification lead times but boosting designer confidence in long-term reliability. Chip-on-board neon-replacement strips cut power draw by 40% compared to legacy neon while lasting beyond 50 000 hours, a shift that trims maintenance budgets. Wide thermal envelopes from -40 °C to 105 °C enable installations from Nordic ski resorts to Gulf shopping malls, thereby broadening the flexible LED module market footprint.

Increasing Demand for Energy-Efficient Signage and Advertising Solutions

Municipal luminance caps and rising electricity tariffs push operators toward high-efficiency, flexible panels with integrated photovoltaic cells and real-time power logging. California Title 24 2025 compels outdoor billboards to auto-dim, reinforcing demand for modules with luminous efficacy exceeding 150 lumens-per-watt and embedded daylight sensors. Retailers report 30% lower installation labor when curved video walls ship as bendable panels rather than tiled, rigid cabinets, shortening payback to less than 2 years in prime storefronts. 4 000-nit curved micro-LED displays launched at CES 2025 let brands reach sunlit outdoor audiences where OLED fades. Cylindrical kiosks and wrap-around pillars made viable by flexible modules unlock new rentable surface area in transit hubs, driving incremental advertising yields.

High Initial Costs of Advanced Flexible LED Modules Versus Rigid Alternatives

Polyimide modules still carry 40%-60% premiums over FR-4 boards because roll-to-roll lines operate at smaller volumes and rely on high-temperature polymers. Automotive mini-LED backlights for curved clusters cost between USD 80 and USD 120, roughly double rigid LCD backlights, constricting adoption in value-segment vehicles. Signage operators in emerging economies see capex exceeding USD 300 per square meter, lengthening payback periods when power tariffs remain below USD 0.10 per kilowatt-hour. Mass-transfer equipment costing more than USD 5 million per line limits entry to cash-rich firms, dampening competitive pricing pressure. Until JEDEC-like footprint standards emerge, tool reuse across projects remains limited, slowing cost-down curves.

Other drivers and restraints analyzed in the detailed report include:

- Automotive OEM Integration of Interior Ambient Lighting for Differentiation

- Mini-LED And Micro-LED Backlighting Driving High-Density Flexible Modules for Curved Cockpit Displays

- Supply Chain Price Volatility for Key Semiconductors and Rare Earth Phosphors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyimide modules are advancing at a 18.56% CAGR, driven by cockpit displays and wearables that flex beyond 180 degrees while withstanding temperatures from -40 °C to 125 °C. The flexible LED module market for polyimide solutions benefits from glass-transition temperatures above 300 °C, enabling reflow profiles that are unsuitable for PET or polycarbonate. Continuous laser-assisted transfer places micro-LEDs within +-10 micrometers, securing luminance uniformity across curved dashboards. Plastic-based substrates still dominate cost-sensitive architectural lighting because their tooling is 30% cheaper, and bend radii above 20 millimeters relax mechanical stress. As voice-controlled smart-home systems proliferate, demand for tighter radii and elevated heat loads should gradually shift volume toward polyimide.

In non-automotive strip lighting, plastics remain adequate where ambient temperatures stay below 60 °C and mechanical flexing is infrequent. Yet mini-LED backlights with thousand-zone local dimming create hotspot currents that plastics cannot dissipate efficiently, nudging premium signage buyers toward polyimide. Hybrid metal-core flex and ceramic-filled polymers fill niches, such as industrial high-bay luminaires that need thermal conductivity above 2 W m-K. Cost parity is expected after 2028 as roll-to-roll yields climb and resin prices fall, pivoting a larger slice of the flexible LED module market toward high-performance substrates.

Geography Analysis

Asia Pacific led with 67.89% of 2025 revenue and is set to grow at an 18.81% CAGR, anchored by China's aggressive capacity adds and South Korea's USD 350 million government stimulus for intelligent LEDs. Investments such as Chenxian Optoelectronics' RMB 3 billion (USD 417 million) expansion of its glass-substrate micro-LED capacity underscore regional momentum. Taiwan's mass-transfer precision within +-1 micrometer cements the island as a hub for next-gen display subcontracting.

North America benefits from stringent energy codes such as Title 24 2025 and IECC 2024, which catalyze retrofits with high-efficiency modules, while leading entertainment venues install curved 8K signage to heighten visitor engagement. Europe follows with architectural refurbishments that favor low-flicker, flicker-safe flexible strips under EN IEC 60598-1, and premium automakers in Germany integrate micro-LED clusters to differentiate digital dashboards.

South America, the Middle East, and Africa hold smaller shares, but exhibit pockets of high growth tied to megaprojects such as Saudi Arabia's USD 877 billion infrastructure pipeline and Brazil's new smart-stadium builds ahead of continental sporting events. Suppliers entering these regions tailor packages for high-ambient-temperature operation and multi-voltage grids, positioning the flexible LED module market for long-term geographic diversification.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Nichia Corporation

- Seoul Semiconductor Co., Ltd.

- OSRAM GmbH

- CreeLED Inc.

- Signify N.V.

- Everlight Electronics Co., Ltd.

- Lumileds Holding B.V.

- Lite-On Technology Corporation

- Luminus Devices, Inc.

- Bridgelux, Inc.

- Nationstar Optoelectronics Co., Ltd.

- Shenzhen Kingsun Optoelectronic Co., Ltd.

- Leyard Optoelectronic Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Flexible LED Strips in Architectural and Decorative Lighting Projects

- 4.2.2 Increasing Demand for Energy-Efficient Signage and Advertising Solutions

- 4.2.3 Automotive OEM Integration of Interior Ambient Lighting for Differentiation

- 4.2.4 Rising Popularity of Wearables and Flexible Consumer Electronics Displays

- 4.2.5 Emergence of Ultra-Thin Polyimide Substrates Enabling Foldable Lighting in Smart Textiles

- 4.2.6 Mini-LED and Micro-LED Back-Lighting Driving High-Density Flexible Modules for Curved Cockpit Displays

- 4.3 Market Restraints

- 4.3.1 High Initial Costs of Advanced Flexible LED Modules vs Rigid Alternatives

- 4.3.2 Heat Management Challenges Limiting Lifespan at Tight Bending Radii

- 4.3.3 Supply Chain Price Volatility for Key Semiconductors and Rare Earth Phosphors

- 4.3.4 Lack of Uniform Global Bend-Testing Standards Complicating OEM Qualification Cycles

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Substrate Type

- 5.1.1 Plastic-Based Flexible Modules

- 5.1.2 Polyimide-Based Modules

- 5.1.3 Other Substrate Type

- 5.2 By Form Factor

- 5.2.1 Strip / Linear Flexible Modules

- 5.2.2 Panel / Sheet Flexible Modules

- 5.3 By Application

- 5.3.1 Signage and Advertising

- 5.3.2 Automotive Lighting (Interior and Ambient)

- 5.3.3 Wearables and Consumer Electronics

- 5.3.4 Architectural and Decorative Lighting

- 5.3.5 Other Applications (Medical, Specialty)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.2 Europe

- 5.4.3 Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 LG Innotek Co., Ltd.

- 6.4.3 Nichia Corporation

- 6.4.4 Seoul Semiconductor Co., Ltd.

- 6.4.5 OSRAM GmbH

- 6.4.6 CreeLED Inc.

- 6.4.7 Signify N.V.

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Lumileds Holding B.V.

- 6.4.10 Lite-On Technology Corporation

- 6.4.11 Luminus Devices, Inc.

- 6.4.12 Bridgelux, Inc.

- 6.4.13 Nationstar Optoelectronics Co., Ltd.

- 6.4.14 Shenzhen Kingsun Optoelectronic Co., Ltd.

- 6.4.15 Leyard Optoelectronic Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

(주말 및 공휴일 제외)