|

시장보고서

상품코드

2064018

아시아태평양의 자동차용 LED 패키지 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific Automotive LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

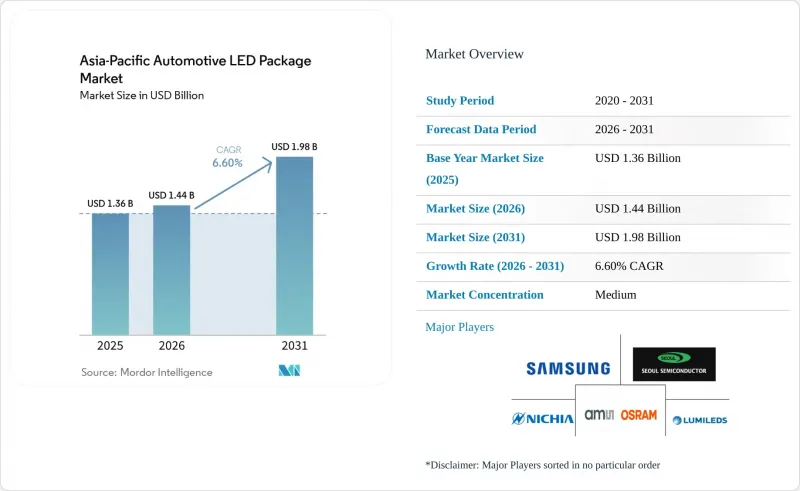

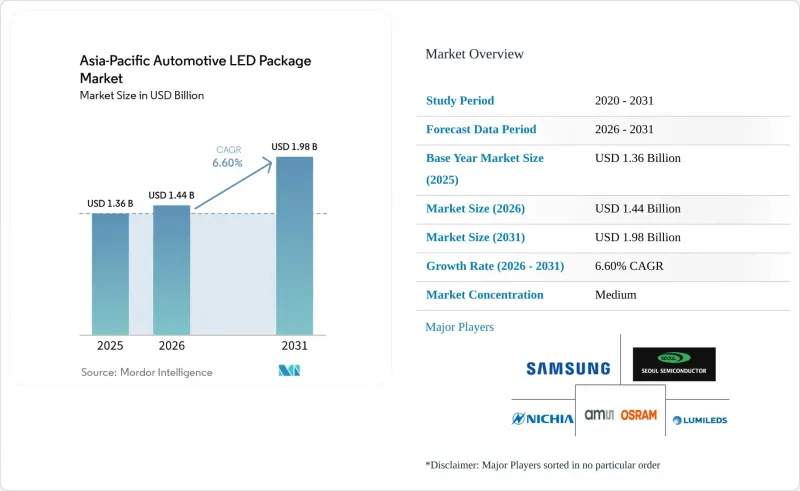

Mordor Intelligence에 의하면, 아시아태평양의 자동차용 LED 패키지 시장 규모는 2025년 13억 6,000만 달러로 평가되었고, 2026년에는 14억 4,000만 달러로 추정되고, 2026-2031년 CAGR 6.60%로 성장을 지속할 전망이며, 2031년에는 19억 8,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 패키지 구조별(SMD, CSP, 플립칩 LED 패키지, COB), 출력 등급별(저출력, 중출력, 고출력), 용도별(외장 조명, 내장 조명, 센싱/IR 용도 등), 차종별(승용차, 상용차), 국가별(중국, 일본, 인도 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 자동차용 LED 패키지 시장 동향 및 분석

에너지 효율이 높은 자동차용 조명에 대한 수요 증가

아시아태평양의 전기차(EV) 프로그램은 주행 거리 극대화에 중점을 두고 있으므로, 조명 서브시스템에서 전력 소비를 1와트라도 줄일 수 있다면 그만큼 주행 거리가 직접적으로 늘어납니다. 2024년 중국에서 생산된 1,286만 대의 신에너지차(NEV)는 할로겐 램프에 비해 전력 소비량이 30-50% 낮은 LED 패키지를 중시하는 대규모 도입 기반을 마련했습니다. 이를 통해 소형 배터리식 전기차의 주행 거리가 5-10킬로미터 향상됩니다. 하이브리드 차량 플랫폼에서도 알터네이터에 가해지는 부하가 줄어들어 이점을 얻게 되며, 이는 인도와 태국에서 보조금 수령 자격의 기준이 되는 연비 평가 향상으로 이어집니다. 미국 에너지부가 예측한 발광 효율 향상(2035년까지 1와트당 249루멘에 달할 전망)은 향후 패키지 개발 로드맵의 기반이 될 것입니다. 할로겐 램프의 수명이 1,000-2,000시간인 반면, LED는 25,000-50,000시간에 달하는 긴 수명과 뛰어난 신뢰성 덕분에, 서비스 네트워크가 미비한 동남아시아의 차량 운영 업체들에게 보증 위험을 줄여줍니다.

승용차에 LED 헤드램프의 보급 확대

2025년에는 패키지 LED의 단가가 1킬로루멘당 0.50달러 미만으로 떨어지면서, 자동차 제조업체들은 중형 세단과 스포츠 유틸리티 차량(SUV)에 LED 헤드램프를 기본 사양으로 장착할 수 있게 되었습니다. 서울세미컨덕터의 WICOP 칩 스케일 디바이스는 100종 이상의 승용차에 채택되어 있으며, 양산을 위한 비용 목표의 타당성이 입증되었습니다. 인도의 Bharat NCAP 평가 기준에 따르면, 주간 주행등(DRL)을 장착한 차량에 높은 안전 점수가 부여되기 때문에 각 OEM 업체들은 풀 LED 헤드램프와 DRL을 세트로 도입하는 방향으로 나아가고 있습니다. 2024년 중국의 승용차 생산 대수는 2,000만 대를 넘어섰으며, LED 헤드램프 보급률은 60%를 넘어섰습니다. 이는 국내 공급업체가 밝기나 열 성능 면에서 일본의 동종 업체에 필적하는 성능을 구현하면서도, 기존 제조업체의 가격보다 20-30% 낮은 가격을 책정했기 때문입니다.

할로겐 솔루션에 비해 높은 초기 비용

인도나 가격을 중시하는 아세안 시장의 보급형 모델은 여전히 개당 5-8달러짜리 할로겐 어셈블리에 의존하고 있지만, 기본적인 LED 헤드램프의 부품 원가는 15-25달러 범위입니다. 소매 가격이 약 1만-1만 2,000달러인 소형 세단의 경우, 램프 1개당 10달러의 추가 비용은 자동차 제조업체의 이익률을 크게 압박합니다. 중출력 표면 실장형 LED의 가격은 현재 1킬로루멘당 0.50달러 미만이지만, 드라이버, 방열판, 광학 시스템 등으로 인해 시스템 전체 비용은 할로겐 램프의 3-4배로 치솟습니다. 이륜 전기자동차의 경우, 에너지 효율이 향상되었음에도 불구하고 구매 결정 시 단가 경제성이 우선시되기 때문에 단일 칩 LED나 할로겐 램프가 계속해서 채택되고 있습니다.

부문별 분석

2025년, 표면 실장 소자는 아시아태평양의 자동차용 LED 패키지 시장 점유율의 43.39%를 차지했으며, 검증된 신뢰성과 확립된 공급망이 가장 중요하게 여겨지는 후미등, 번호판 조명, 실내등 분야에서 주도적인 위치를 유지했습니다. 그러나 연평균 성장률(CAGR) 7.06%로 성장하고 있는 칩 스케일 패키지는 광학 시스템 전체의 높이를 불과 10mm까지 낮춤으로써 헤드램프의 디자인을 혁신하고 있습니다. 서울세미컨덕터의 WICOP 구조는 베어 다이를 회로 기판에 직접 접합하여 기판이나 세라믹 프레임을 배제하고 있습니다. 중국과 일본의 OEM 업체들이 공기 저항을 줄이고 독특한 주간 가시성을 실현하는 초박형 램프 설계를 추구함에 따라, 칩 스케일 디바이스와 관련된 아시아태평양의 자동차용 LED 패키지 시장 규모는 가속화될 전망입니다.

플립칩 방식도 이러한 추세에 발맞추어, 금속 패드 접합을 활용하여 열전도율과 전류 분산성을 향상시키고, 적응형 구동 빔 어레이를 구현하고 있습니다. 특허를 둘러싼 공방이 격화되고 있는 가운데, 에버라이트가 2026년 2월 서울세미컨덕터를 상대로 미국에서 출원한 특허는 플립칩의 전극 형상에 대한 침해를 주장하고 있으며, 이는 CSP 수요 증가에 따라 법적 마찰이 발생하고 있음을 시사합니다. 칩 온 보드(COB)는 상용차용 보조 스팟 램프 분야의 틈새 시장으로 남아 있습니다. 여기에서는 단일 알루미늄 기판 위에 여러 개의 다이를 집적함으로써 높은 루멘 밀도를 실현하고 있습니다. 이러한 동향을 종합해 보면, 중국의 현지 공급업체들이 웨이퍼 레벨 패키징 생산 라인을 확대함에 따라 칩 스케일 및 플립 칩이 기존 SMD 시장 점유율을 계속해서 잠식해 나갈 것으로 보입니다.

1와트를 초과하는 고출력 패키지는 2025년 매출의 57.89%를 차지했습니다. 이는 눈부심 없는 하이빔을 구현하기 위해 200 cd/mm² 이상의 휘도가 필요한 어댑티브 드라이빙 빔 시스템의 급속한 보급을 반영한 것입니다. 이 등급에 기인한 아시아태평양의 자동차용 LED 패키지 시장 규모는 2028년까지 중형 세단에 픽셀형 헤드라이트가 도입됨에 따라 확대될 전망입니다. 중출력 소자는 열적 제약이 비교적 완화된 주간 주행등이나 차량 내부용 RGB 조명 용도로 채택되고 있습니다. 저출력 표시기는 중국 공급업체들이 개당 0.10달러 미만으로 제시하고 있어 상품화가 진행되고 있으며, 이로 인해 이익률이 압박받고 업계 재편이 촉진되고 있습니다.

니치아 화학공업의 마이크로PLS 마이크로 LED 라이트 엔진은 그 방향성을 보여주고 있습니다. 50-100mW의 고출력 마이크로 LED 1만 6,384개를 조합함으로써 1,000루멘을 넘는 광량을 실현하고, 노면에 투사하는 것도 가능하게 했습니다. GB 4599-2021 및 UNECE R112의 눈부심 제어 관련 규제 요건에 따라, 각 OEM 업체들은 이러한 어레이를 채택해야 하는 상황에 놓여 있습니다. 중출력 RGB LED는 전기차 실내에서 빠르게 보급되고 있으며, 50-100개의 주소 지정 가능한 LED가 무드 조명, 내비게이션, 충전 상태 알림 등의 역할을 담당하고 있습니다. 스마트 헤드라이트용으로 차량당 100-300픽셀이 추가됨에 따라, 고출력 부문이 계속해서 시장 가치의 대부분을 차지할 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the asia-Pacific automotive LED package market size is expected to grow from USD 1.36 billion in 2025 to USD 1.44 billion in 2026 and is forecast to reach USD 1.98 billion by 2031 at a 6.60% CAGR over 2026-2031.

This report is Segmented by Package Architecture (SMD, CSP, Flip-Chip LED Packages, COB), Power Class (Low Power, Mid Power, and High Power ), Application (Exterior Lighting, Interior Lighting, Sensing/IR Applications, and More), Vehicle Type (Passenger Vehicles, and Commercial Vehicles), and Country (China, Japan, India, and More). Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Automotive LED Package Market Trends and Insights

Increasing Demand for Energy-Efficient Automotive Lighting

Electric vehicle programs across Asia-Pacific center on maximizing range, so every watt shaved from lighting subsystems translates directly into extra driving kilometers. China's 12.86 million new-energy vehicles built in 2024 created a large installed base that values LED packages delivering 30-50% lower power draw than halogens, translating to 5-10 kilometer range gains in compact battery-electric cars. Hybrid platforms also benefit when alternator load falls, improving fuel-economy scores used for subsidy qualification in India and Thailand. Efficacy gains projected by the U.S. Department of Energy, reaching 249 lumens per watt by 2035, underpin future package roadmaps. Reliability advantages, with lifetimes of 25,000-50,000 hours compared with 1,000-2,000 hours for halogens, cut warranty risk for fleet operators in Southeast Asia where service networks are sparse.

Growing Penetration of LED Headlamps in Passenger Vehicles

Packaged LED cost fell below USD 0.50 per kilolumen in 2025, allowing automakers to list LED headlamps as standard equipment on mid-tier sedans and sport-utility vehicles. Seoul Semiconductor's WICOP chip-scale devices underpin more than 100 passenger models, validating cost targets for mass production. India's Bharat NCAP protocol attaches higher safety scores to daytime-running-lamp equipped cars, nudging OEMs toward full LED headlamp-DRL bundles. China's passenger car production exceeded 20 million units in 2024, with LED headlamp penetration crossing 60% as domestic suppliers matched Japanese peers on luminance and thermal performance while pricing 20-30% below incumbent quotes.

High Initial Cost Compared to Halogen Solutions

Entry-level cars in India and cost-sensitive ASEAN markets still rely on halogen assemblies costing USD 5-8 each, whereas a basic LED headlamp bill of materials sits in the USD 15-25 range. For compact sedans retailing at roughly USD 10,000-12,000, the extra USD 10 per lamp materially erodes automaker margin. Although mid-power surface-mount LED prices are now under USD 0.50 per kilolumen, drivers, heat sinks, and optics push full-system cost three-to-four times higher than halogen. Two-wheel EVs, despite energy-efficiency gains, continue opting for single-chip LEDs or halogens because unit economics dominate purchase decisions.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Automotive Lighting Safety Regulations

- Rapid Expansion of Electric Vehicle Production in Asia-Pacific

- Thermal Management Challenges in High-Power LED Packages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surface-mount devices captured 43.39% of the Asia-Pacific automotive LED package market share in 2025, maintaining leadership in rear lamps, license-plate illumination, and dome lights where proven reliability and entrenched supply chains matter most. Yet chip-scale packages, expanding at a 7.06% CAGR, are redefining headlamp styling by trimming total optical height to as low as 10 millimeters. Seoul Semiconductor's WICOP structure bonds the bare die directly to the circuit board, eliminating substrates and ceramic frames. The Asia-Pacific automotive LED package market size attached to chip-scale devices is set to accelerate as OEMs in China and Japan seek razor-thin lamp designs that lower drag and enable distinct daytime signatures.

Flip-chip formats ride the same trend, leveraging gold-pad bonding to improve thermal conductivity and current spreading for adaptive driving beam arrays. Patent crossfire is intensifying; Everlight's February 2026 U.S. filing against Seoul Semiconductor alleges infringement on flip-chip electrode geometry, signaling legal friction as CSP demand grows. Chip-on-board remains a niche for auxiliary spot lamps in commercial vehicles where clustering multiple dies on a single aluminum substrate gives high lumen density. Combined, these dynamics indicate that chip-scale and flip-chip will keep eroding legacy SMD share as local Chinese suppliers scale wafer-level packaging lines.

High-power packages above 1 watt delivered 57.89% of 2025 revenue, mirroring rapid uptake of adaptive driving beam systems that require 200-plus cd mm-2 luminance for glare-free high beam. The Asia-Pacific automotive LED package market size attributable to this class will expand alongside pixelated headlights entering mid-tier sedans by 2028. Mid-power devices fill daytime running lamp and interior RGB roles where thermal constraints are modest. Low-power indicators are commoditizing as Chinese vendors quote sub-USD 0.10 per part, squeezing margins and prompting consolidation.

Nichia's µPLS micro-LED light engine shows the trajectory: 16,384 high-power micro-LEDs, each at 50-100 mW, combine for over 1,000 lumens while enabling road-surface projections. Regulatory glare-control requirements in GB 4599-2021 and UNECE R112 push OEMs toward such arrays. Mid-power RGB usage is surging in electric-vehicle cabins where 50-100 addressable LEDs handle mood, navigation, and state-of-charge alerts. The high-power segment will continue to dominate value as each vehicle adds 100-300 pixels for smart headlights.

List of Companies Covered in this Report:

- Nichia Corporation

- OSRAM GmbH (Ams-OSRAM AG)

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding B.V.

- Samsung Electronics Co., Ltd.

- Cree LED (SGH Group)

- LG Innotek Co., Ltd.

- Everlight Electronics Co., Ltd.

- Lite-On Technology Corporation

- Dominant Opto Technologies Sdn. Bhd.

- Stanley Electric Co., Ltd.

- Rohinni LLC

- Lextar Electronics Corporation

- Toyoda Gosei Co., Ltd.

- EPISTAR Corporation

- TOSPO Lighting Co., Ltd.

- Refond Optoelectronics Co., Ltd.

- ProLight Opto Technology Corporation

- MLS Co., Ltd. (Forest Lighting)

- Lumens Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions And Market Definition

- 1.2 Scope Of The Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand For Energy-Efficient Automotive Lighting

- 4.2.2 Growing Penetration Of LED Headlamps In Passenger Vehicles

- 4.2.3 Stringent Automotive Lighting Safety Regulations

- 4.2.4 Rapid Expansion Of Electric Vehicle Production In Asia-Pacific

- 4.2.5 Localized Supply Chains Reducing LED Package Costs In ASEAN

- 4.2.6 Integration Of Smart Pixel LED Arrays For Advanced Driver Assistance Systems (ADAS)

- 4.3 Market Restraints

- 4.3.1 High Initial Cost Compared To Halogen Solutions

- 4.3.2 Thermal Management Challenges In High-Power LED Packages

- 4.3.3 Volatility In Automotive Sales Due To Macroeconomic Uncertainties

- 4.3.4 Patent Litigation Risks Limiting New Entrant Innovation

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact Of Macroeconomic Factors On The Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power Of Suppliers

- 4.8.2 Bargaining Power Of Buyers

- 4.8.3 Threat Of New Entrants

- 4.8.4 Threat Of Substitutes

- 4.8.5 Intensity Of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Package Architecture

- 5.1.1 SMD (Surface Mount Device)

- 5.1.2 CSP (Chip Scale Package)

- 5.1.3 Flip-Chip LED Packages

- 5.1.4 COB (Chip-On-Board)

- 5.2 By Power Class

- 5.2.1 Low Power ( Less Than 0.5 W)

- 5.2.2 Mid Power (0.5 to 1 W)

- 5.2.3 High Power (More Than 1 W)

- 5.3 By Application

- 5.3.1 Exterior Lighting

- 5.3.2 Interior Lighting

- 5.3.3 Sensing / IR Applications

- 5.3.4 Others - Applications

- 5.4 By Vehicle Type

- 5.4.1 Passenger Vehicles

- 5.4.2 Commercial Vehicles

- 5.5 By Country

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 Southeast Asia

- 5.5.5 Rest Of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share, Products And Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 OSRAM GmbH (Ams-OSRAM AG)

- 6.4.3 Seoul Semiconductor Co., Ltd.

- 6.4.4 Lumileds Holding B.V.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 Cree LED (SGH Group)

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Lite-On Technology Corporation

- 6.4.10 Dominant Opto Technologies Sdn. Bhd.

- 6.4.11 Stanley Electric Co., Ltd.

- 6.4.12 Rohinni LLC

- 6.4.13 Lextar Electronics Corporation

- 6.4.14 Toyoda Gosei Co., Ltd.

- 6.4.15 EPISTAR Corporation

- 6.4.16 TOSPO Lighting Co., Ltd.

- 6.4.17 Refond Optoelectronics Co., Ltd.

- 6.4.18 ProLight Opto Technology Corporation

- 6.4.19 MLS Co., Ltd. (Forest Lighting)

- 6.4.20 Lumens Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space And Unmet-Need Assessment