|

시장보고서

상품코드

2064019

COB LED 모듈 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)COB LED Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

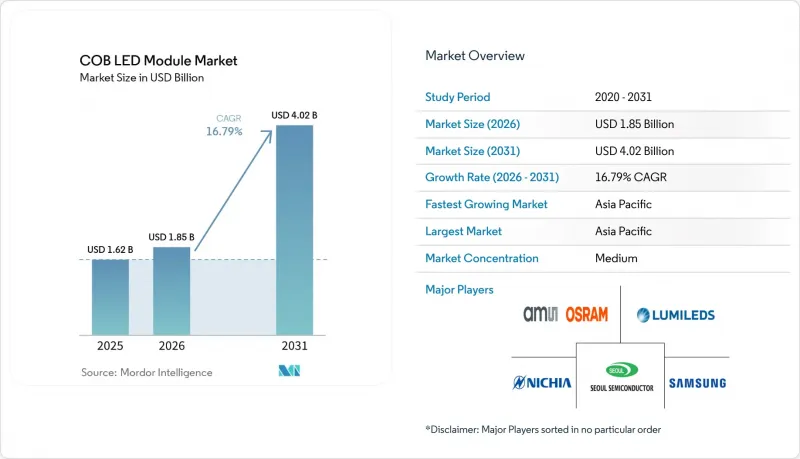

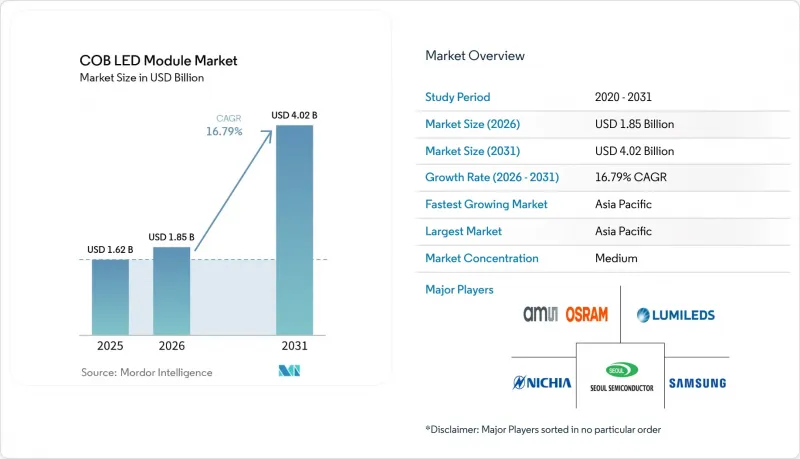

Mordor Intelligence에 의하면, COB LED 모듈 시장 규모는 2025년에 16억 2,000만 달러로 평가되었고, 2026년에 18억 5,000만 달러로 추정되고, 2031년까지 40억 2,000만 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 16.79%로 성장할 것으로 전망됩니다.

본 보고서는 출력 범위별(저출력 COB 모듈, 중출력 COB 모듈 등), 용도별(일반 조명, 자동차용 조명, 산업용 조명, 건축용 및 실외 조명 등), 지역별(북미, 남미, 유럽, 아시아태평양 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 COB LED 모듈 시장 동향 및 분석

전 세계 에너지 효율 규제 강화

EU의 2019/2020 에코디자인 규정 및 미국의 유사한 규정에 따른 규제 강화로 인해, 공급업체들은 모듈의 효율 향상, 루멘 유지율 연장, 그리고 플리커 억제를 꾀해야 하는 상황에 놓여 있습니다. 광원으로 분류되는 COB 제품은 유럽 시장에 진출하기 전에 EPREL 등록을 취득해야 합니다. 이러한 요건은 규정 준수 비용을 증가시키는 한편, 인증을 받지 않은 소규모 제조업체 시장 진입을 제한하게 됩니다. 2026년 12월부터 ‘지속 가능한 제품을 위한 에코디자인 규정’에 따라 순환형 경제와 관련된 요건이 추가되며, Zhaga Book 12 홀더를 준수하고 소켓 연결이 가능하며 유지보수가 용이한 설계가 권장됩니다. 제3자 시험, IEC 62031 준수, 그리고 광생물학적 안전성 확보라는 부담으로 인해, 적합성 선언서를 발급할 수 있는 인증 시험소를 보유한 제조업체들 간의 통합이 가속화되고 있습니다.

중출력 모듈의 1루멘당 단가 급락

2022년부터 2025년에 걸쳐 중출력 COB LED 모듈의 가격은 대폭 하락했습니다. 이러한 가격 하락은 주로 국내 MOCVD 생산 능력을 활용한 중국 공급업체들에 의해 주도되었습니다. 그러나 이러한 디플레이션 추세로 인해 포장 업체들의 매출총이익률은 절반으로 크게 줄었습니다. 2026년 초까지 귀금속 가격의 급등에 따라, 밸류체인 전반에 걸쳐 50개 이상의 기업이 손실된 이익률을 회복하기 위해 가격 인상을 단행했습니다. 이러한 가격 회복으로 인해 경쟁 구도가 변화하면서, 초점은 단순한 가격 경쟁에서 차별화로 옮겨갔습니다. 현재 주요 차별화 요인으로는 색 안정성, 고연색성(고CRI) 형광체, 드라이버 내장 기능 등이 있으며, 이 모든 요소가 평균 판매 가격 상승을 정당화하는 근거가 되고 있습니다. 독자적인 형광체 배합을 강점으로 삼고 있는 유럽, 미국 및 일본공급업체들은 단순한 광속을 넘어선 부가가치를 제품에 부여하고 있기 때문에 이러한 변화하는 시장 환경에서 가장 큰 혜택을 누릴 수 있는 입장에 있습니다.

중국의 저비용 생산 능력에 따른 가격 하락

중국의 칩 제조업체와 패키징 업체들은 생산 능력을 확대하고 있으며, 그 속도는 국내 수요 증가율을 웃돌고 있습니다. 이러한 불균형으로 인해 공급 과잉이 지속되면서 중출력 제품의 평균 판매 가격(ASP)을 끌어내리고 있습니다. 주류 칩 온 보드(COB)의 가격이 대폭 하락함에 따라, 대만과 동남아시아의 일부 수익성이 낮은 제조업체들은 생산 라인을 폐쇄하거나 틈새 시장으로 전환할 수밖에 없는 상황에 처해 있습니다. 중국 상장 LED 기업들의 평균 매출총이익률이 하락함에 따라, 이에 대응해 첫 번째 단계로 공동 가격 인상 공지가 발표되었습니다. 가치 회복을 위한 노력이 진행되고 있지만, 중동 및 아프리카의 범용 조명 기구 시장은 여전히 가격에 민감한 상황입니다. 그 결과, 많은 해외 브랜드들이 차별화가 더욱 두드러지는 프리미엄 하위 부문으로 밀려나는 상황이 되고 있습니다.

부문별 분석

50W를 초과하는 고출력 모듈은 2026-2031년 연평균 성장률(CAGR) 17.73%로 확대될 전망이며, 이는 COB LED 모듈 시장 전체의 성장률을 상회할 것으로 보입니다. 5,000 lm 이상을 제공하는 단일 광원 패키지는 경기장 투광등, 산업용 하이베이 조명, 실외 구역 조명에서 광학 시스템과 배선을 간소화합니다. Bridgelux의 2세대 F90 제품군은 이러한 추세를 상징하며, 40W 이미터에서 8,000 lm을 공급하는 동시에 60°C의 온도 변동 범위 내에서 Δu'v' 색차 변동을 0.004 미만으로 억제하고 있습니다. 한편, 중출력 제품의 COB LED 모듈 시장은 여전히 규모가 크며, 2025년에는 상업용 다운라이트 및 건축용 액센트 조명 분야에서 시장의 41.47%를 차지할 것으로 전망됩니다. 10W 미만의 저출력 모듈은 디스플레이 백라이트, 코브 조명, 장식용 스트립 등에 주로 사용되고 있지만, 더 얇은 폼팩터로 동등한 광속을 구현하는 칩 스케일 패키지(CSP)의 경쟁이 거세지고 있습니다.

이 출력축을 따라 구매 결정은 갈라집니다. 고출력 발광체를 구매하는 사람들은 수명과 열적 여유를 중시하며, 조기 광속 저하를 방지하기 위해 고가의 세라믹 기판이나 구리 코인을 기꺼이 받아들입니다. 전력 회사와 경기장 소유주들은 50,000시간의 가동 주기 동안 조명 기구 수를 줄이고 유지보수를 최소화함으로써 높은 도입 비용이 정당화된다고 보고 있습니다. 한편, 중출력 층에서는 루멘당 비용 측면에서 경쟁이 치열하게 벌어지고 있으며, 중국 공급업체들이 세계 브랜드보다 10-25% 저렴한 가격을 책정하고 있습니다. 이곳에서는 유럽, 미국 및 일본의 기존 제조업체들이 색 좌표를 안정화하고, 특히 CRI 90의 호스피탈리티 공간에서 DLC 프리미엄 리베이트 대상이 되는 우수한 형광체 블렌드를 제공함으로써 시장 점유율을 지키고 있습니다.

지역별 분석

아시아태평양은 2025년에 전 세계 매출의 66.73%를 차지한 것으로 평가되었으며, 2031년까지 COB LED 모듈 시장의 중심지로 자리매김할 것으로 보이며, 연평균 성장률(CAGR)은 17.95%를 나타낼 것으로 전망됩니다. 중국은 광둥성과 장쑤성에 위치한 엔드투엔드 LED 클러스터에 더해, 칩 파브 및 패키징 라인에 대한 설비 투자 비용을 보전해 주는 정부의 인센티브 덕분에 시장을 독점하고 있습니다. TV, 노트북, 모니터에 Mini-LED 백라이트가 채택되면서 국내 수요가 견조한 흐름을 유지하고 있는 반면, 적극적인 수출이 동남아시아 전역의 범용 제품 공급을 뒷받침하고 있습니다. 일본과 한국은 자동차, 디스플레이, 의료기기 분야에서 규모는 작지만 수익성이 높은 틈새 시장을 공략하고 있으며, 세라믹, AlGaN 에피택시, 엄격한 신뢰성 시험을 활용하여 프리미엄 가격을 확보하고 있습니다.

2025년에는 북미와 유럽을 합친 시장이 매출의 약 4분의 1을 차지했습니다. 전력 회사의 리베이트, DLC 프리미엄 티어, EU의 에코디자인 규정에 힘입은 개조 프로그램 덕분에, 형광등 트로퍼나 HID 투광등에서 150 lm/W 이상이며 CRI 90을 충족하는 COB 조명 기구로의 교체가 가속화되고 있습니다. 2026년 FIFA 월드컵 및 2028년 로스앤젤레스 올림픽과 관련된 경기장 개보수 공사는 깜빡임 없는 8K 방송 수준을 구현할 수 있는 고출력 모듈이 필요한 주목할 만한 프로젝트를 탄생시키고 있습니다. 유럽의 순환형 경제 정책에서는 디지털 제품 패스포트를 갖추고, 소켓 연결이 가능하며 수리가 가능한 COB 모듈이 선호되며, Zhaga Book 12를 준수하는 기계적 실적를 갖춘 공급업체가 우대받습니다.

남미, 중동 및 아프리카는 COB LED 모듈 시장으로서는 규모는 작지만 성장세를 보이고 있는 시장입니다. 브라질과 멕시코에서는 식품 가공 시설과 물류 단지에 산업용 LED 하이베이 조명이 도입되고 있습니다. 한편, 걸프협력회의(GCC) 회원국들은 모래와 염분이 포함된 안개에도 견딜 수 있는 IP69K 규격의 COB 투광등이 필요한 스마트 시티 회랑에 대한 투자를 추진하고 있습니다. 아프리카에서는 배터리 수명을 연장하기 위해 저전력 COB 엔진을 탑재한 Off-grid형 태양광 랜턴이 초기 단계임에도 불구하고 호응을 얻고 있지만, 가격에 대한 민감성 때문에 상위 모델의 보급은 제한적입니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the cOB lED module market size is projected to be USD 1.62 billion in 2025, USD 1.85 billion in 2026, and reach USD 4.02 billion by 2031, growing at a CAGR of 16.79% from 2026 to 2031.

This report is Segmented by Power Range (Low Power COB Modules, Mid Power COB Modules, and More), Application (General Lighting, Automotive Lighting, Industrial Lighting, Architectural and Outdoor Lighting, and More), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global COB LED Module Market Trends and Insights

Stringent Energy-Efficiency Regulations Worldwide

Regulatory tightening in the EU under Ecodesign Regulation 2019/2020 and parallel rules in the United States pushes suppliers to raise module efficacy, extend lumen maintenance, and curb flicker. COB products classified as light sources must secure EPREL registration before entering European channels, a requirement that adds compliance costs but also limits the entry of smaller, unaccredited fabricators. From December 2026, the Ecodesign for Sustainable Products Regulation adds circularity mandates that reward socketable, serviceable designs aligned with Zhaga Book 12 holders. The burden of third-party testing, IEC 62031 conformity, and photobiological safety accelerates consolidation among manufacturers with accredited labs capable of issuing declarations of conformity.

Rapid Decline in USD/Lumen for Mid-Power Modules

Between 2022 and 2025, prices for mid-power COB LED modules dropped significantly. This price drop was largely driven by Chinese suppliers, who capitalized on their domestic MOCVD capacity. However, this deflationary trend led to a significant halving of packaging houses' gross margins. By early 2026, in response to surging precious-metal prices, over 50 companies spanning the value chain implemented price increases to recoup lost margins. This price rebound has shifted the competitive landscape, moving the focus from mere pricing to differentiation. Key differentiators now include color stability, high-CRI phosphors, and integrated driver-on-board features, all of which justify elevated average selling prices. Suppliers from the West and Japan, armed with proprietary phosphor mixes, stand to gain the most from this evolving landscape, as their offerings emphasize value beyond just raw lumens.

Price Erosion from Chinese Low-Cost Capacity

Chinese chipmakers and packagers are ramping up capacity, outpacing domestic demand growth. This imbalance has led to a consistent supply surplus, pushing mid-power average selling prices (ASPs) downward. Mainstream Chip-on-Board (COB) prices declined significantly, prompting some marginal producers in Taiwan and Southeast Asia to either shut down production lines or pivot to niche applications. The average gross margin for publicly listed Chinese LED companies dipped, prompting the first wave of coordinated price increase notifications. While efforts to restore value are underway, the market for commodity luminaires in the Middle East and Africa remains price-sensitive. As a result, many foreign brands find themselves relegated to premium sub-segments, where differentiation is more pronounced.

Other drivers and restraints analyzed in the detailed report include:

- OEM Shift Toward Integrated Headlamp Architectures in EVs

- Mass Adoption of Smart, Connected Lighting Ecosystems

- High Thermal-Management Cost for Less Than 50 W Modules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-power modules above 50 W are on track to expand at 17.73% CAGR during 2026-2031, outstripping the broader COB LED module market. Single-source packages delivering more than 5,000 lm streamline optics and wiring in stadium floodlights, industrial high bays, and outdoor area fixtures. Bridgelux's Generation 2 F90 family illustrates the trend, offering 8,000 lm from a 40 W emitter while preserving Δu'v' color shift below 0.004 across a 60 °C temperature swing. Meanwhile, the COB LED module market for mid-power products remains large, accounting for 41.47% of the market in 2025 across commercial downlights and architectural accents. Low-power modules under 10 W cluster into display backlighting, cove lighting, and decorative strips, but face rising pressure from chip-scale packages that achieve equivalent flux in slimmer footprints.

The purchasing calculus diverges along this power axis. Buyers of high-power emitters prize lifetime and thermal headroom, tolerating premium ceramic substrates and copper coins to avoid premature lumen depreciation. Utilities and stadium owners view the higher acquisition cost as justified by reduced fixture counts and minimal maintenance over 50,000 h duty cycles. Conversely, the mid-power tier competes on dollars per lumen, with Chinese suppliers undercutting global brands by 10-25%. Here, Western and Japanese incumbents defend territory by offering better phosphor blends that lock in color point and qualify for DLC Premium rebates, especially in CRI 90 hospitality spaces.

Geography Analysis

Asia-Pacific accounted for 66.73% of global revenue in 2025 and will remain the epicenter of the COB LED module market through 2031, with a forecast 17.95% CAGR. China dominates with end-to-end LED clusters in Guangdong and Jiangsu, plus state incentives that defray capex for chip fabs and packaging lines. Mini-LED backlight adoption in televisions, notebooks, and monitors keeps domestic demand robust, while export aggressiveness fuels commodity supply across Southeast Asia. Japan and South Korea pursue smaller but lucrative niches in automotive, display, and medical equipment, leveraging ceramics, AlGaN epitaxy, and rigorous reliability tests to fetch premiums.

North America and Europe together accounted for roughly one-quarter of revenue in 2025. Retrofit programs driven by utility rebates, DLC Premium tiers, and EU Ecodesign rules accelerate replacement of fluorescent troffers and HID floodlights with COB fixtures exceeding 150 lm/W and CRI 90. Stadium renovations connected to the 2026 FIFA World Cup and the 2028 Los Angeles Olympics create headline projects that call for high-power modules capable of delivering flicker-free 8K broadcast levels. Circular-economy policies in Europe prefer socketable, repairable COB modules with digital product passports, rewarding suppliers that align mechanical footprints with Zhaga Book 12.

South America, the Middle East, and Africa are smaller but growing markets for COB LED modules. Brazil and Mexico deploy industrial LED high bays in food processing and logistics parks, while the Gulf Cooperation Council members invest in smart-city corridors that demand IP69K-rated COB floodlights to withstand sand and saline fog. Africa shows early traction for off-grid solar lanterns that integrate low-power COB engines for extended battery life, though price sensitivity limits the adoption of higher-tier products.

- ams OSRAM AG

- Samsung Electronics Co., Ltd.

- Nichia Corporation

- Lumileds Holding B.V.

- Seoul Semiconductor Co., Ltd.

- Citizen Electronics Co., Ltd.

- Bridgelux, Inc.

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Epistar Corporation

- Lextar Electronics Corp.

- Toyoda Gosei Co., Ltd.

- Luminus Devices, Inc.

- ProPhotonix Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Energy-Efficiency Regulations Worldwide

- 4.2.2 Rapid Decline in USD/Lumen for Mid-Power Modules

- 4.2.3 Mass Adoption of Smart, Connected Lighting Ecosystems

- 4.2.4 OEM Shift Toward Integrated Headlamp Architectures in EVs

- 4.2.5 Mini-LED Backlighting Boom in Premium Displays

- 4.2.6 Urban Stadium and Arena Renovations Demanding High-Power COB

- 4.3 Market Restraints

- 4.3.1 Price Erosion from Chinese Low-Cost Capacity

- 4.3.2 High Thermal-Management Cost for Less Than 50 W Modules

- 4.3.3 Competition from Chip-Scale and Flip-Chip Packages

- 4.3.4 Supply-Chain Volatility in Phosphor and Substrate Materials

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 Low Power COB Modules (Greater Than or Equal To 10 W)

- 5.1.2 Mid Power COB Modules (Less Than 10 W - Greater Than or Equal To 50 W)

- 5.1.3 High Power COB Modules (Less Than 50 W)

- 5.2 By Application

- 5.2.1 General Lighting

- 5.2.2 Automotive Lighting

- 5.2.3 Industrial Lighting

- 5.2.4 Architectural and Outdoor Lighting

- 5.2.5 Other Applications (Horticulture, UV, Specialty)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.5 South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ams OSRAM AG

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Nichia Corporation

- 6.4.4 Lumileds Holding B.V.

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 Citizen Electronics Co., Ltd.

- 6.4.7 Bridgelux, Inc.

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 LG Innotek Co., Ltd.

- 6.4.10 Epistar Corporation

- 6.4.11 Lextar Electronics Corp.

- 6.4.12 Toyoda Gosei Co., Ltd.

- 6.4.13 Luminus Devices, Inc.

- 6.4.14 ProPhotonix Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment