|

시장보고서

상품코드

2064341

방사성 의약품 CDMO 및 CMO 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Radiopharmaceutical CDMO/CMO Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

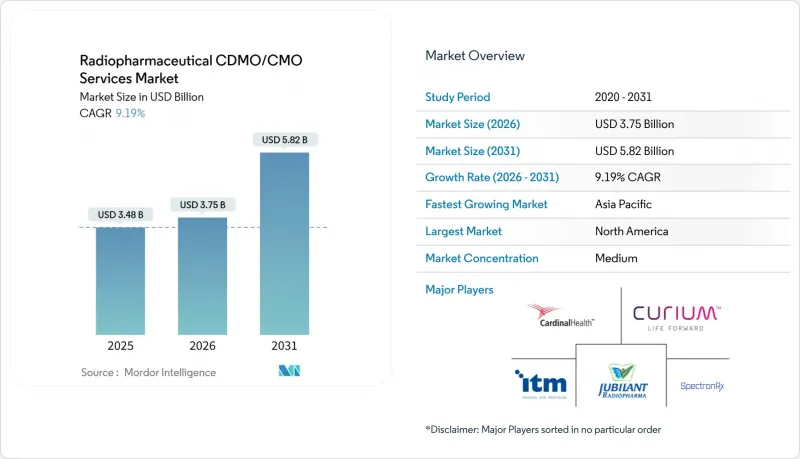

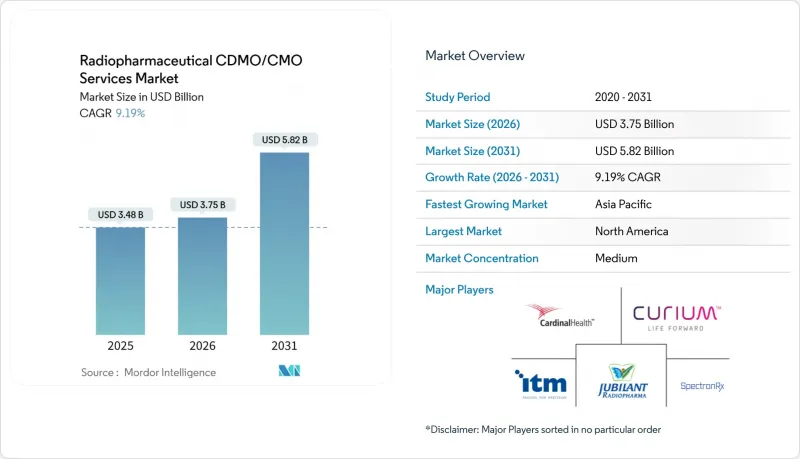

Mordor Intelligence에 의하면, 방사성 의약품 CDMO 및 CMO 서비스 시장 규모는 2025년 34억 8,000만 달러로 평가되었고, 2026년에는 37억 5,000만 달러로 추정되고, 2026-2031년 CAGR 9.19%로 성장을 지속할 전망이며, 2031년까지 58억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 서비스별(동위원소 생산 및 공급, 공정 개발 및 방사성 표지, 결합 등), 모달리티별(진단용, 치료용), 방사성 동위원소별(F-18, Ga-68, Tc-99m 등), 사업 규모별(전임상, 임상, 시판), 지역별(북미, 유럽, 아시아태평양, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 방사성 의약품 CDMO 및 CMO 서비스 시장 동향 및 인사이트

RLT의 승인 및 규모 확대가 외부 위탁에 따른 GMP 수요를 높이고 있습니다.

상업화 단계에 접어든 루테튬-177 치료의 경우, 배치 규모가 그램 단위에서 Kg 단위로 확대되면서 이중 인증을 받은 제조 시설의 GMP 슬롯 부족 문제를 초래하고 있습니다. Eckert &Ziegler사가 2025년 3월에 Actinium Pharmaceuticals사와 액티늄-225 공급 계약을 체결한 사례에서 볼 수 있듯이, 후원 기업들은 현재 2년 후까지 생산 능력을 확보하고 있습니다. 알파선 방출체의 격리를 위해서는 핫셀의 추가 건설이나 방사선 차폐층의 증설이 필요하기 때문에 공정 개발의 조기 아웃소싱이 촉진되고 있습니다. PET 영상용 추적자에서 치료용 페이로드로의 전환에 따라, CDMO는 규모 확대에 앞서 cGMP 기준에 따른 정제, 안정성 및 품질 관리(QC) 방법의 재검증을 수행해야 합니다. 방사화학 분야의 전문 인력이 부족한 점이 이러한 부족 현상을 더욱 악화시키고 있으며, 통합형 서비스의 프리미엄 가격 책정을 뒷받침하고 있습니다.

지역화(북미 주도, 아시아태평양 지역 확대)가 아웃소싱 촉진

북미는 잘 정립된 규제 체계와 인근에 위치한 동위원소 공급업체를 보유하고 있는 반면, 아시아태평양에서는 사이클로트론 건설이 진행되면서 동위원소 공급 비용이 낮아지고 있습니다. 2025년 4월 GE 헬스케어가 일본 메디피직스를 완전 자회사로 임베디드함에 따라, 일본은 13개 공장을 통해 광범위한 지역에 서비스를 제공할 수 있는 테라노스틱스 거점이 됩니다. 중국 내 F-18 및 Ga-68 생산은 수입 의존도를 낮추고, 비용 효율성을 중시하는 임상시험을 유치하고 있습니다. 인도와 호주는 제약 분야로의 사업 확장에 필요한 노하우와 ANSTO의 원자로에서 생산된 루테튬-177에 대한 접근성을 활용하여, 2차 거점으로서 두각을 나타내고 있습니다. 현지 공장은 반감기가 짧은 동위원소의 운송 시간을 단축하고, 붕괴로 인한 수율 저하를 완화합니다.

주요 동위원소(Lu-177, Ac-225, Ga-68)공급 부족 및 가격 변동

임상용 악티늄-225는 여전히 제한된 수의 토륨-229 발생기에 의존하고 있습니다. 액티늄 파마슈티컬스사는 자사의 사이클로트론 공법을 통해 순도 99.8%의 동위원소를 10-20배 더 저렴하게 공급할 수 있다고 주장하고 있지만, 상업적 규모의 생산 여부는 아직 미정입니다. 원자로 가동 중단으로 루테튬-177의 가격이 급등하는 한편, Ga-68 발생기공급 병목 현상이 PSMA PET 영상 검사를 제한하고 있습니다. 아시아태평양 지역(APAC)에서는 사이클로트론 설비의 밀도가 유럽 및 미국의 수준에 미치지 못하기 때문에 공급 부족이 더욱 심각합니다. 각 CDMO 업체들은 공급량을 확보하기 위해 다년 계약을 체결하고 있지만, 이로 인해 임시 연구에 대한 유연성이 저하되고 있습니다.

부문별 분석

프로세스 개발 및 방사성 표지, 결합 서비스는 후원사가 화학적 위험 완화를 앞당겨 추진하고 있는 데 따라 2031년까지 연평균 성장률(CAGR) 10.40%로 확대될 전망입니다. ABX의 6가지 개발용 핫셀은 모든 동위원소에 대한 표지 및 정제를 완벽하게 수행하기 위해 필요한 첨단 기술을 상징합니다. 한편, GMP 의약품 원료의약품 및 제제의 제조는 2025년 매출의 47.24%를 차지했으며, 이는 성숙기에 접어든 진단약 생산과 루테튬-177의 상업적 생산을 반영한 것입니다. 카디널 헬스(Cardinal Health)와 같은 기업들이 일반 제품 판매에서 액티늄-225 관련 장기 파트너십으로 전환함에 따라, 동위원소 생산 분야의 방사성 의약품 CDMO 및 CMO 서비스 시장 규모는 지속적으로 확대되고 있습니다. 규제 대응 CMC 및 콜드체인 물류와 같은 기타 번들 서비스는 여전히 틈새 시장이지만, 개발자들이 원스톱 솔루션을 요구함에 따라 그 가치가 높아지고 있습니다.

후원 기업들은 재검증이 필요 없이 전임상 단계와 GMP 화학 단계를 연결해 줄 수 있는 CDMO를 선호하고 있습니다. 퍼셉티브사는 전구체 합성, 분석법 및 문서화를 통합함으로써 80건 이상의 IND 신청 패키지 준비를 지원해 왔습니다. 대량 생산되는 F-18 FDG 배치의 이익률이 낮기 때문에 CDMO는 이러한 생산을 통해 현금 흐름을 확보하는 한편, 그 이익을 치료 인프라에 투자하고 있습니다. 개발 전문 지식이 없는 기업은 방사성 의약품 CDMO 및 CMO 서비스 시장에서 가격 주도형 범용 제품 공급업체로 전락할 위험이 있습니다.

진단용 의약품은 2025년 매출의 58.36%를 차지했으나, 치료용 파이프라인은 2031년까지 연평균 성장률(CAGR) 9.76%로 확대되고 있습니다. 치료용 배치는 동위원소의 희소성과 엄격한 격리 요건으로 인해 프리미엄 가격에 판매될 수 있습니다. Eckert &Ziegler사와 Actinium Pharmaceuticals사 간의 계약은 알파선 방출체에 관한 중요한 임상시험을 뒷받침하는 것으로, CDMO가 동위원소에 대한 접근성을 차별화 수단으로 활용하고 있는 좋은 사례입니다. APAC 지역에서 사이클로트론 설비가 보급됨에 따라 진단용 F-18 FDG의 이익률이 압박을 받고 있으며, 유럽 및 미국 공급업체들의 가격 결정력이 약화되고 있습니다.

치료제는 개발 기간이 긴 데다, 승인만 되면 블록버스터급 수익을 기대할 수 있기 때문에 GE 헬스케어의 일본 메디피직스 완전 인수와 같은 고액 인수합병을 이끌어내고 있습니다. 진료 방식의 다양화가 지역별 전문화를 촉진하고 있습니다. 북미와 유럽은 알파선 및 베타선 치료제에 대한 전문 지식에 주력하는 한편, 아시아태평양(APAC)은 급증하는 PET 수요에 대응하기 위해 진단용 시설의 대량 생산 체제를 확대되고 있습니다.

지역별 분석

북미는 FDA 규제가 명확하고 NorthStar 및 Cardinal Health와 같은 동위원소 공급업체와 지리적으로 인접해 있다는 점 덕분에 2025년 매출의 47.35%를 차지했습니다. 아시아태평양의 방사성 의약품 CDMO 및 CMO 서비스 시장 규모는 급속히 확대되고 있으며, 중국의 사이클로트론 도입과 GE 헬스케어의 일본 메디피직스 인수 이후 일본의 테라노스틱스로의 전환을 배경으로, 2031년까지 연평균 성장률(CAGR) 9.60%로 성장하고 있습니다. 인도는 저비용 생산 체계와 영어로 진행되는 신청 절차를 강점으로 삼고 있지만, 동위원소에 대한 접근성은 여전히 걸림돌로 남아 있습니다. 호주는 ANSTO가 원자로를 기반으로 루테튬-177을 공급하는 혜택을 누리고 있으며, 예측 가능한 동위원소 공급이 필요한 동남아시아의 임상시험을 유치하고 있습니다.

벨기에의 SCK CEN으로 대표되는 유럽의 강력한 원자력 연구 기반은 2025년 1분기에 가동을 시작할 예정인 SpectronRx사의 악티늄-225 제조 플랜트 등을 통해 생산 능력 확대를 뒷받침하고 있습니다. EMA(유럽의약품청)의 규제 조화로 인해 EU 전역에서의 유통은 용이해졌지만, 고방사능 동위원소의 경우 운송 물류가 여전히 복잡합니다. 중동 및 아프리카 및 남미는 현재 규모가 작지만, GCC 국가들의 의료 투자와 브라질의 제약 부문이 수입 비용 절감을 위해 현지 PET 및 치료제 공급을 확대함에 따라 성장할 가능성이 있습니다.

따라서, 방사성 의약품 CDMO 및 CMO 서비스 시장은 허브 앤 스포크 모델로 운영되고 있습니다. 공정 개발은 북미와 유럽에 집중되어 있으며, GMP 제조는 운송 중의 분해 손실을 최소화할 수 있는 지역 거점으로 확대되고 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the radiopharmaceutical cDMO/CMO services market size is expected to grow from USD 3.48 billion in 2025 to USD 3.75 billion in 2026 and is forecast to reach USD 5.82 billion by 2031 at 9.19% CAGR over 2026-2031.

This report is Segmented by Service (Isotope Production & Supply, Process Development & Radiolabeling/Conjugation, and More), Modality (Diagnostic, Therapeutic), Radioisotope (F-18, Ga-68, Tc-99m, and More), Scale of Operation (Preclinical, Clinical, Commercial), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Radiopharmaceutical CDMO/CMO Services Market Trends and Insights

RLT Approvals and Scaling Raise Outsourced GMP Demand

Commercial-stage lutetium-177 therapies have moved batch volumes from grams to kilograms, tightening GMP slots at dual-licensed plants. Sponsors now reserve capacity two years ahead, as shown by Eckert & Ziegler's March 2025 deal with Actinium Pharmaceuticals for actinium-225 supply . Alpha-emitter containment adds extra hot-cell construction and radioprotection layers, driving earlier outsourcing of process development. The shift from PET imaging tracers to therapeutic payloads means CDMOs must re-validate purification, stability, and QC methods under cGMP before scale-up. Limited radiochemistry talent compounds the squeeze, reinforcing premium pricing for integrated offerings.

Regionalization (NA Leadership, APAC Build-Out) Increases Outsourcing

North America commands mature regulatory pathways and proximate isotope suppliers, yet the Asia-Pacific is building cyclotrons that lower delivered isotope cost. GE HealthCare's 100% acquisition of Nihon Medi-Physics in April 2025 turns Japan into a theranostics hub that can serve the wider region from 13 plants. China's domestic F-18 and Ga-68 output trims import reliance and attracts cost-sensitive clinical trials. India and Australia stand out as secondary nodes, leveraging pharmaceutical scale-up know-how and access to ANSTO's reactor-based lutetium-177. Local plants cut transport time for short-lived isotopes and reduce decay-driven yield losses.

Scarcity and Price Volatility of Key Isotopes (Lu-177, Ac-225, Ga-68)

Clinical-grade actinium-225 still depends on limited thorium-229 generators. Actinium Pharmaceuticals claims its cyclotron method will deliver 10-20 times cheaper isotope at 99.8% purity, yet commercial scale is pending. Reactor outages spike lutetium-177 prices, while Ga-68 generator bottlenecks restrict PSMA PET imaging. APAC shortages are sharper because cyclotron density trails Western levels. CDMOs respond with multi-year offtake contracts that secure volumes but hamper flexibility for ad-hoc studies.

Other drivers and restraints analyzed in the detailed report include:

- Lu-177 and Emerging Ac-225 Supply Investments Unlock New Programs

- Specialist CDMOs Expand Capacity and Sites

- Dual GMP and Nuclear Transport/Licensing Burden Slows Tech Transfer

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Process Development & Radiolabeling/Conjugation services are rising at a 10.40% CAGR to 2031 as sponsors front-load chemistry risk mitigation. ABX's six development hot cells highlight the depth of capability needed to perfect labeling and purification across isotopes . Meanwhile, GMP Drug Substance & Drug Product Manufacturing still captured 47.24% of 2025 revenue, reflecting mature diagnostic output and commercial lutetium-177 runs. The Radiopharmaceutical CDMO/CMO Services Market size for isotope production continues to expand as companies like Cardinal Health shift from commodity sales to long-term actinium-225 partnerships. Other bundled services, such as regulatory CMC and cold-chain logistics, remain niche but gain value as developers seek one-stop solutions.

Sponsors gravitate to CDMOs that can bridge preclinical and GMP chemistry without re-validation. Perceptive has supported more than 80 IND packages by integrating precursor synthesis, analytical methods, and documentation. High-volume F-18 FDG batches carry lower margins, so CDMOs use these runs to feed cash flow while investing profits in therapeutic infrastructure. Those without development expertise risk relegation to price-driven commodity roles within the Radiopharmaceutical CDMO/CMO Services Market.

Diagnostic agents retained 58.36% of 2025 revenue, yet therapeutic pipelines are advancing at a 9.76% CAGR to 2031. Therapeutic batches command premium pricing due to isotope scarcity and stringent containment. Eckert & Ziegler's deal with Actinium Pharmaceuticals underpins pivotal alpha-emitter trials, exemplifying how CDMOs leverage isotope access for differentiation. Diagnostic F-18 FDG margins compress as cyclotron capacity spreads across APAC, eroding Western suppliers' pricing power.

Therapeutics carry longer timelines but promise blockbuster revenue on approval, attracting big-ticket mergers like GE HealthCare's full purchase of Nihon Medi-Physics. Modality divergence is driving geographic specialization: North America and Europe focus on alpha- and beta-therapeutic expertise, while APAC scales high-volume diagnostic plants to serve burgeoning PET demand.

Geography Analysis

North America commanded 47.35% of 2025 revenue due to FDA clarity and proximity to isotope suppliers such as NorthStar and Cardinal Health. The Radiopharmaceutical CDMO/CMO Services Market size in Asia-Pacific is catching up, expanding at a 9.60% CAGR through 2031 on the back of China's cyclotron rollout and Japan's theranostics pivot after GE HealthCare's buyout of Nihon Medi-Physics. India leverages low-cost manufacturing and English-language filings, though isotope access remains a hurdle. Australia benefits from ANSTO's reactor-based lutetium-177 supply, drawing South-East Asian clinical trials that need predictable isotope deliveries.

Europe's strong nuclear research base, exemplified by SCK CEN in Belgium, supports capacity ramps such as SpectronRx's actinium-225 plant operationalized in Q1 2025 . EMA harmonization eases pan-EU distribution, yet transport logistics remain complex for high-specific-activity isotopes. Middle East & Africa and South America are small today but may grow as GCC healthcare investments and Brazil's pharma sector push for local PET and therapy supply to cut import costs.

The Radiopharmaceutical CDMO/CMO Services Market therefore operates on a hub-and-spoke model: process development concentrates in North America and Europe, while GMP manufacturing spreads to regional nodes that minimize decay loss during transport.

- ABX advanced biochemical compounds

- AtomVie Global Radiopharma

- Cardinal Health Nuclear & Precision Health Solutions

- Curium Pharma

- Cyclotek

- Eckert & Ziegler Radiopharma

- Evergreen Theragnostics

- Isotopia Molecular Imaging

- ITM Isotope Technologies Munich

- Jubilant Radiopharma

- Minerva Imaging

- Monrol

- Nihon Medi-Physics

- NorthStar Medical Radioisotopes

- Nucleus RadioPharma

- PharmaLogic

- Siemens Healthineers PETNET Solutions

- SOFIE

- SpectronRx

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 RLT Approvals and Scaling Raise Outsourced GMP Demand

- 4.2.2 Regionalization (NA Leadership, APAC Build-Out) Increases Outsourcing

- 4.2.3 Lu-177 And Emerging Ac-225 Supply Investments Unlock New Programs

- 4.2.4 Specialist CDMOS Expand Capacity and Sites

- 4.2.5 Decentralized Multi-Site Networks to Beat Half-Life Logistics

- 4.2.6 Alpha-Emitters CDMO Playbooks (Containment/Generator Partnerships)

- 4.3 Market Restraints

- 4.3.1 Scarcity And Price Volatility of Key Isotopes (Lu-177, Ac-225, Ga-68)

- 4.3.2 Dual GMP And Nuclear Transport/Licensing Burden Slows Tech Transfer

- 4.3.3 Talent Gaps in Radiochemistry, HP, And QA/QP

- 4.3.4 Radioactive Waste Handling and Site Licensing Bottlenecks

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service

- 5.1.1 Isotope Production & Supply

- 5.1.2 Process Development & Radiolabeling/Conjugation

- 5.1.3 GMP Drug Substance & Drug Product Manufacturing

- 5.1.4 Others

- 5.2 By Modality

- 5.2.1 Diagnostic

- 5.2.2 Therapeutic

- 5.3 By Radioisotope

- 5.3.1 F-18

- 5.3.2 Ga-68

- 5.3.3 Tc-99m

- 5.3.4 Zr-89

- 5.3.5 I-131

- 5.3.6 Lu-177

- 5.3.7 Others

- 5.4 By Scale of Operation

- 5.4.1 Preclinical

- 5.4.2 Clinica

- 5.4.3 Commercial

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 ABX advanced biochemical compounds

- 6.4.2 AtomVie Global Radiopharma

- 6.4.3 Cardinal Health Nuclear & Precision Health Solutions

- 6.4.4 Curium

- 6.4.5 Cyclotek

- 6.4.6 Eckert & Ziegler Radiopharma

- 6.4.7 Evergreen Theragnostics

- 6.4.8 Isotopia Molecular Imaging

- 6.4.9 ITM Isotope Technologies Munich

- 6.4.10 Jubilant Radiopharma

- 6.4.11 Minerva Imaging

- 6.4.12 Monrol

- 6.4.13 Nihon Medi-Physics

- 6.4.14 NorthStar Medical Radioisotopes

- 6.4.15 Nucleus RadioPharma

- 6.4.16 PharmaLogic

- 6.4.17 Siemens Healthineers PETNET Solutions

- 6.4.18 SOFIE

- 6.4.19 SpectronRx

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment