|

시장보고서

상품코드

2064345

LED 백라이트 모듈 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)LED Backlight Module - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

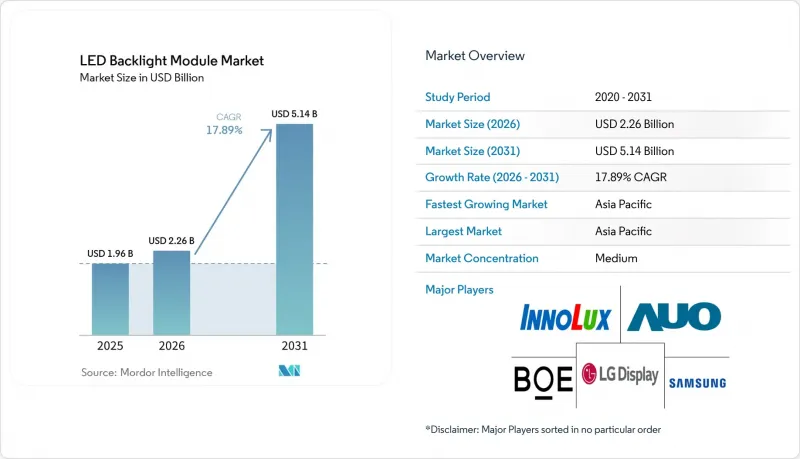

Mordor Intelligence에 의하면, LED 백라이트 모듈 시장 규모는 2025년 19억 6,000만 달러로 평가되었고, 2026년에는 22억 6,000만 달러로 추정되고, 2031년까지 51억 4,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 17.89%로 성장할 전망입니다.

본 보고서는 백라이트 기술별(엣지 라이트형 LED 모듈, 직하형 LED 모듈), 패널 크기별(소형 패널, 중형 패널 등), 용도별(TV용, 모니터 및 노트북용, 스마트폰 및 태블릿용, 자동차용 디스플레이 등), 지역별(북미, 유럽, 아시아태평양, 남미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 LED 백라이트 모듈 시장 동향 및 분석

프리미엄 TV 시장에서 Mini-LED 백라이트의 보급 확대

삼성의 Neo QLED 및 LG의 QNED 라인업에는 1,000개 이상의 디밍 존을 갖춘 미니 LED 모듈이 탑재되어 있어, 1,500니트를 넘는 최대 밝기와 100% DCI-P3 색역을 구현하고 있습니다. 북미에서는 65형 모델이 1,000달러 미만으로 판매되는 등 소매 가격이 하락세를 보이며, 초기 애호가층을 넘어 보급이 확대되고 있습니다. 각 Mini-LED 백라이트에는 5,000-2만 5,000개의 칩이 채택되어 있으며, 이는 구역별 펄스 폭 변조(PWM) 기능을 갖춘 첨단 드라이버 IC에 대한 수요를 이끌고 있습니다. 그 결과 발생하는 부품 비용 상승은 직접 라이트 방식공급업체들에게 수년에 걸쳐 수익에 긍정적인 영향을 미치며, LED 백라이트 모듈 시장에서 프리미엄 구성으로의 전환을 가속화하고 있습니다.

고휘도 자동차용 디스플레이 수요 증가

전기자동차의 조종석 재설계에 따라, 주간 시인성을 확보하기 위해 2,000-3,000니트의 백라이트가 필수적입니다. HARMAN의 ‘Ready Display’ 플랫폼은 이중화된 LED 스트링과 1,000개 이상의 조광 구역을 통합하여, ISO 15008의 가시성 요구 사항과 ISO 26262의 기능 안전 규정을 모두 충족합니다. 현재 자동차 티어 기업들은 이 기능에 대해 모듈 가격의 10-15%에 해당하는 프리미엄을 지불하고 있으며, 이로 인해 향후 수년에 걸친 설계 채택이 확정되면서 LED 백라이트 모듈 시장 전체의 평균 판매 가격이 상승하고 있습니다.

OLED 및 Micro-LED 디스플레이로 인한 경쟁 심화

800달러를 넘는 가격대의 플래그십 스마트폰이나 태블릿에서는 OLED 패널이 주류를 이루며, 기존의 백라이트를 대체하고 있습니다. Micro-LED 시범 프로젝트는 유기 물질의 열화를 동반하지 않으면서 OLED 수준의 명암비를 구현할 것으로 기대되며, 양산 시 수율이 안정화된다면 대형 화면용 양산화가 진행될 가능성이 있습니다. 이러한 자체 발광 기술들은 프리미엄 시장 점유율을 잠식하고 있으며, LED 백라이트 모듈 시장이 도달할 수 있는 상한선을 낮추고 있습니다.

부문별 분석

직접 라이트 방식의 Mini-LED 모듈은 TV 및 게이밍 모니터에서의 채택 확대에 힘입어 연평균 성장률(CAGR) 18.23%를 나타낼 것으로 전망됩니다. 엣지 라이트 방식의 LED 백라이트 모듈 시장은 다소 완만한 성장에 그칠 전망이지만, 가벼운 무게와 20달러 미만의 부품 원가 덕분에 노트북과 저가형 TV에 있어 여전히 필수적인 존재로 남을 것입니다. 각 제조업체들은 시장 점유율을 지키기 위해 듀얼 엣지 구성과 반사형 캐비티를 지속적으로 개선하고 있지만, 수천 개에 달하는 조광 구역이 제공하는 명암비의 우위 덕분에 Mini-LED가 장기적인 성장의 원동력이 될 것으로 전망됩니다.

생산 비용의 추이 또한 이러한 양극화를 뒷받침하고 있습니다. 드라이버 IC 가격 하락과 LED 비닝 수율 향상으로 인해, Mini-LED TV의 실제 판매 가격은 2022년 3,000달러에서 2025년에는 1,200달러 가까이까지 떨어질 전망입니다. 한편, 엣지 라이트 방식의 생산 라인은 가동률이 높고 설비 투자 부담도 적기 때문에 평균 판매 가격이 하락하더라도 제조업체는 이익을 확보할 수 있어 LED 백라이트 모듈 시장 전체적으로 균형 잡힌 성장이 기대됩니다.

지역별 분석

아시아태평양은 2025년에 매출의 67.82%를 차지한 것으로 평가되었으며, BOE, 티엔마(Tianma), TCL CSOT의 생산 확대와 더불어 중국, 베트남, 인도의 지원 정책에 힘입어 연평균 성장률(CAGR) 18.35%를 유지할 것으로 전망됩니다. 현지화 프로그램을 통해 국내에서 생산된 하위 조립품에 대한 수입 관세가 면제됨에 따라 입고 비용이 절감되고, 모듈 통합 라인에 대한 내부 투자가 촉진되고 있습니다. 광둥성과 장쑤성의 생산 거점에서는 현재 LED 에피택시, 형광체 합성, 양자점 필름 생산이 통합되어 지역 공급망이 강화되고 있습니다.

북미와 유럽에서는 자동차용 디스플레이 시장이 전반적으로 눈부신 성장을 기록하고 있습니다. 전력 소비 규제가 강화됨에 따라, 상업용 사이니지 및 호텔 및 레스토랑용 디스플레이 분야에서 고효율 백라이트로의 전환이 가속화되고 있습니다. 재팬 디스플레이가 미국에서 130억 달러 규모의 공장을 건설하는 등 제안된 리쇼어링(국내 복귀) 프로젝트는 LED 백라이트 모듈 시장의 성장세를 유지하는 동시에, 아시아태평양 이외의 지역으로공급원 다각화로 이어질 가능성이 있습니다.

남미, 중동 및 아프리카는 여전히 발전 단계에 있으며, 현지 통합업체들이 소매용 사이니지 및 가격에 민감한 TV용 모듈을 조립하고 있습니다. 이 지역들의 생산량은 아시아태평양의 우위를 위협하기에는 부족하지만, 관세 장벽과 지역별 현지 조달 규정에 따라 예측 기간 동안 현지 조립이 점차 확대될 가능성이 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

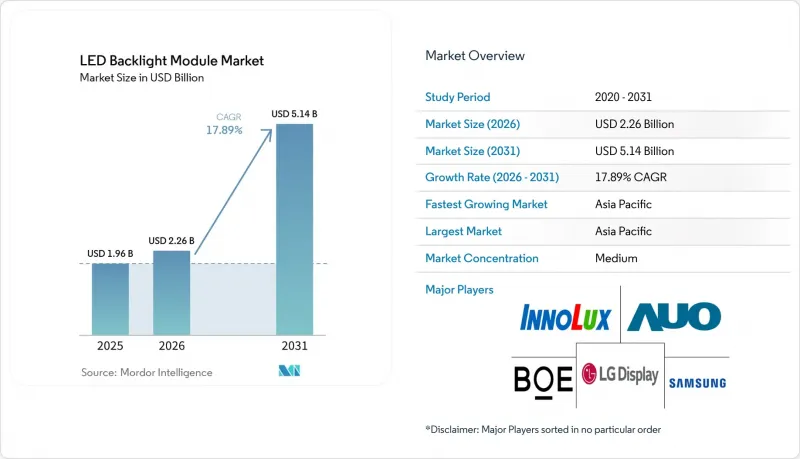

AJY 26.06.24According to Mordor Intelligence, the lED backlight module market size is expected to increase from USD 1.96 billion in 2025 to USD 2.26 billion in 2026 and reach USD 5.14 billion by 2031, growing at a CAGR of 17.89% over 2026-2031.

This report is Segmented by Backlighting Technology (Edge-Lit LED Modules and Direct-Lit LED Modules), Panel Size (Small-Size Panels, Medium-Size Panels, and More), Application (Television, Monitor/Laptop, Smartphone/Tablet, Automotive Display, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global LED Backlight Module Market Trends and Insights

Growing Penetration of Mini-LED Backlighting in Premium TVs

Samsung's Neo QLED and LG's QNED lineups now ship with 1,000-plus dimming-zone Mini-LED modules that deliver peak brightness beyond 1,500 nits and 100% DCI-P3 gamut. Retail price compression 65-inch sets selling below USD 1,000 in North America broadens adoption beyond early enthusiasts. Each Mini-LED backlight employs 5,000-25,000 chips, driving demand for advanced driver ICs with per-zone pulse-width modulation. The resulting bill-of-materials uplift underpins a multiyear revenue tailwind for direct-lit suppliers and accelerates the LED backlight module market's migration toward premium configurations.

Rising Demand for High-Brightness Automotive Displays

Electric-vehicle cockpit redesigns mandate 2,000-3,000 nit backlights for daytime readability. HARMAN's Ready Display platform integrates redundant LED strings and over 1,000 dimming zones to satisfy both ISO 15008 legibility and ISO 26262 functional-safety rules. Automotive tiers now pay 10-15% module premiums for this capability, locking in multiyear design wins and lifting average selling prices across the LED backlight module market.

Intensifying Competition from OLED and Micro-LED Displays

OLED panels dominate flagship smartphones and tablets priced above USD 800, displacing conventional backlights. Micro-LED pilots promise OLED-like contrast without organic degradation and could enter large-screen production once mass transfer yields stabilize. These self-emissive technologies siphon premium share, trimming the attainable ceiling for the LED backlight module market.

Other drivers and restraints analyzed in the detailed report include:

- Supply-Chain Localization Incentives in China and India

- Cost Advantages of Edge-Lit Architectures for Thin Notebooks

- IP Royalty Disputes Elevating BOM Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct-lit Mini-LED modules are projected to post an 18.23% CAGR, reflecting rising adoption in televisions and gaming monitors. The LED backlight module market for edge-lit designs will expand more slowly, yet its lightweight profile and sub-USD 20 bill of materials keep it vital for notebooks and budget TVs. Manufacturers continue to refine dual-edge configurations and reflective cavities to defend share, but the contrast advantage of thousands of dimming zones positions Mini-LED as the long-term growth engine.

Production cost curves reinforce this split. Falling driver-IC prices and improved LED binning yields reduced Mini-LED television street prices from USD 3,000 in 2022 to nearly USD 1,200 in 2025. Conversely, edge-lit lines enjoy higher utilization and low capital intensity, enabling manufacturers to profit even as average selling prices decline, ensuring balanced growth across the LED backlight module market.

Geography Analysis

Asia Pacific contributed 67.82% of revenue in 2025 and is projected to sustain an 18.35% CAGR, underpinned by BOE, Tianma, and TCL CSOT expansions, as well as supportive incentives in China, Vietnam, and India. Localization programs reduce landed costs by exempting domestic sub-assemblies from import duties, driving internal investment into module integration lines. Capacity corridors in Guangdong and Jiangsu now combine LED epitaxy, phosphor synthesis, and quantum-dot film production, fortifying the regional supply chain.

North America and Europe collectively register outsized growth in automotive displays. Stricter power-consumption limits accelerate the transition to high-efficiency backlights across commercial signage and hospitality displays. Proposed reshoring projects, such as Japan Display's USD 13 billion fab in the United States, could diversify supply away from the Asia Pacific while maintaining momentum for the LED backlight module market.

South America, the Middle East, and Africa remain nascent, with local integrators assembling modules for retail signage and price-sensitive televisions. Volumes in these regions are insufficient to challenge Asia Pacific dominance, yet tariff barriers and regional content rules could spur incremental localized assembly over the forecast horizon.

- Samsung Electronics Co., Ltd.

- LG Display Co., Ltd.

- BOE Technology Group Co., Ltd.

- AU Optronics Corp.

- Innolux Corporation

- Sharp Corporation

- Shenzhen Refond Optoelectronics Co., Ltd.

- Tianma Microelectronics Co., Ltd.

- Japan Display Inc.

- Rohinni LLC

- Radiant Opto-Electronics Corporation

- Lextar Electronics Corporation

- Winstar Display Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Penetration of Mini-LED Backlighting in Premium TVs

- 4.2.2 Rising Demand for High-Brightness Automotive Displays

- 4.2.3 Cost Advantages of Edge-Lit Architectures for Thin Notebooks

- 4.2.4 Supply-Chain Localisation Incentives in China and India

- 4.2.5 Energy-Efficiency Regulations Favouring LED Backlight Retrofits

- 4.2.6 Integration of Quantum-Dot Enhancement Films in LCD Panels

- 4.3 Market Restraints

- 4.3.1 Intensifying Competition from OLED and Micro-LED Displays

- 4.3.2 IP Royalty Disputes Elevating BOM Costs

- 4.3.3 Supply Volatility of High-Performance Phosphors

- 4.3.4 Environmental Scrutiny on Rare-Earth Extraction

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Backlighting Technology

- 5.1.1 Edge-lit LED Modules

- 5.1.2 Direct-lit LED Modules (Full Array / Mini-LED)

- 5.2 By Panel Size

- 5.2.1 Small-size Panels (Less Than or Equal To 10 inches)

- 5.2.2 Medium-size Panels (Less Than 10 to Greater Than or Equal to 32 inches)

- 5.2.3 Large-size Panels (Less Than 32 inches)

- 5.3 By Application

- 5.3.1 Television (TV) Backlight Modules

- 5.3.2 Monitor / Laptop Backlight Modules

- 5.3.3 Smartphone / Tablet Backlight Modules

- 5.3.4 Automotive Display Backlight Modules

- 5.3.5 Other Application - Display Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Samsung Electronics Co., Ltd.

- 6.4.2 LG Display Co., Ltd.

- 6.4.3 BOE Technology Group Co., Ltd.

- 6.4.4 AU Optronics Corp.

- 6.4.5 Innolux Corporation

- 6.4.6 Sharp Corporation

- 6.4.7 Shenzhen Refond Optoelectronics Co., Ltd.

- 6.4.8 Tianma Microelectronics Co., Ltd.

- 6.4.9 Japan Display Inc.

- 6.4.10 Rohinni LLC

- 6.4.11 Radiant Opto-Electronics Corporation

- 6.4.12 Lextar Electronics Corporation

- 6.4.13 Winstar Display Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment