|

시장보고서

상품코드

2064352

시력 관리 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Vision Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

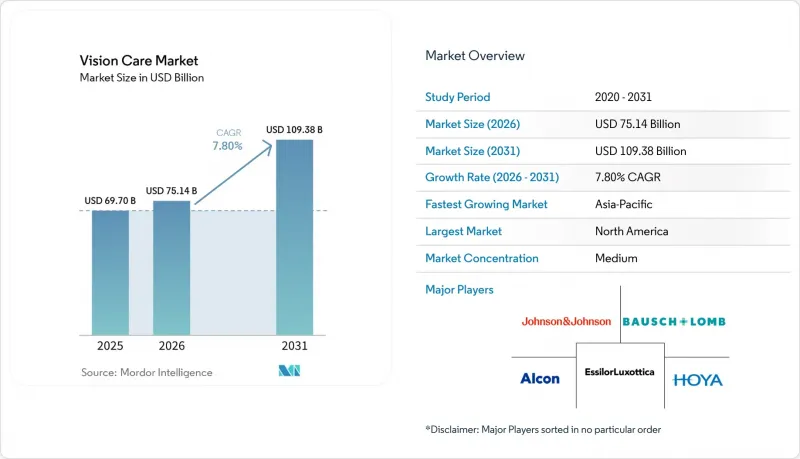

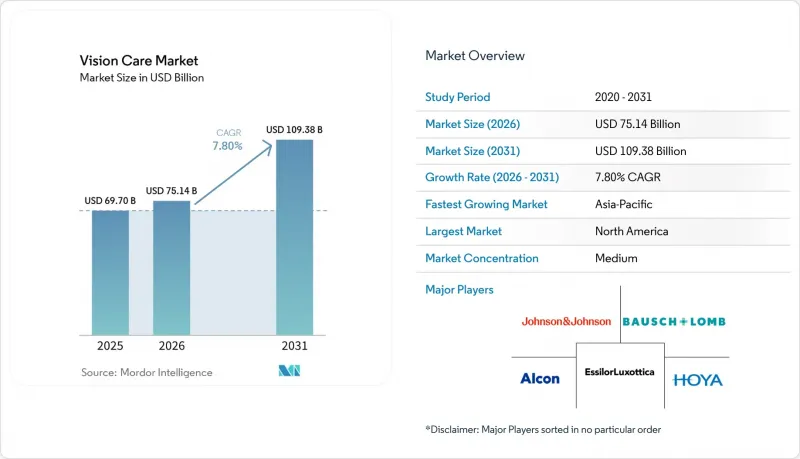

Mordor Intelligence에 의하면, 시력 관리 시장 규모는 2025년에 697억 달러로 평가되었고, 2026년 751억 4,000만 달러로 추정되고, 2031년까지 1,093억 8,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 7.80%를 나타낼 전망입니다.

본 보고서는 제품 유형별(안경 렌즈, 콘택트렌즈, 인공수정체, 눈 건강 제품, 시력 교정 기기), 용도별(교정, 치료, 예방, 미용), 연령대별(소아, 성인, 고령자), 유통 채널별(안경 소매점, 병원, 전자상거래, 약국), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

세계의 시력 관리 시장 동향 및 인사이트

굴절 이상과 근시로 인한 부담 증가

시력 관리 시장은 소아 및 청소년층의 굴절 이상, 특히 근시의 유병률 증가에 힘입어 성장하고 있습니다. 2025년 조사에 따르면, 이 연령대의 전 세계 근시 유병률은 2023년에 35.81%에 달했으며, 2050년까지 39.80%로 상승하여 약 7억 4,000만 명에게 영향을 미칠 것으로 예측됩니다. 이러한 추세에 따라 시장은 단초점 교정에서 근시 진행을 늦추도록 설계된 제품으로 전환되고 있으며, 이로 인해 환자 1인당 가치가 높아지고 있습니다. 2025년 FDA의 승인을 받은 ‘에시롤·스테레스트’는 미국에서 최초로 소아 근시 진행을 늦추는 안경용 렌즈로 자리매김하며, 목표 시장을 확대했습니다. 또한, 중국이 학교 내 근시 선별 검사에 주력하고 있는 점이, 특히 유병률이 이미 높은 동아시아 지역에서 수요를 지속적으로 견인하고 있습니다.

고령화에 따른 노안 및 백내장 관리에 대한 수요

고령화에 따라 노안 교정, 백내장 수술 및 수술 후 시력 개선에 대한 수요가 증가하고 있으며, 이는 시력 관리 시장의 성장에 기여하고 있습니다. 백내장은 여전히 전 세계 실명의 주요 원인이며, 연간 2,000만 건 이상의 수술이 이루어지고 있는데, 그중 유럽에서 430만 건, 미국에서 380만 건을 차지하고 있습니다. 시장에서는 안경에 대한 의존도를 낮추고, 보험 적용 제도 하에서도 본인 부담금을 발생시키는 프리미엄 인공수정체로의 전환이 나타나고 있습니다. 알콘이 2025년에 ‘클레온 파노프틱스 프로’를 출시한 것과, 보슈롬이 2025년 4분기에 프리미엄 인공수정체 매출이 20% 이상 증가했다고 보고한 사실은 고도의 시력 개선 효과에 대한 수요가 증가하고 있음을 여실히 보여주고 있습니다. 전 세계 실명 및 시각장애인은 2020년 3억 3,830만 명에서 2050년까지 5억 3,500만 명으로 증가할 것으로 예상되며, 고령화 추세가 앞으로도 시장 확대를 뒷받침할 것으로 보입니다.

프리미엄 제품의 가격 부담과 보험 환급 격차

많은 환자에게 있어 임상적 필요성이 고가의 교정 및 치료 서비스 비용을 훨씬 초과하고 있기 때문에 시력 관리 시장은 중대한 과제에 직면해 있습니다. 세계보건기구(WHO)의 ‘SPECS 2030’ 프레임워크는 2030년까지 굴절 이상 치료 서비스의 보험 적용 범위를 확대함으로써 이러한 격차를 해소하는 것을 목표로 하고 있습니다. 교정되지 않은 근시로 인한 연간 생산성 손실은 전 세계적으로 2,440억 달러로 추정되며, 저소득 지역에서는 여전히 기본적인 안경조차 구할 수 없는 사람들이 많습니다. 이러한 경제적 장벽은 근시 진행 억제 렌즈나 프리미엄 인공수정체와 같이 급성장 중인 제품 부문의 보급에 영향을 미치고 있습니다. 이러한 제품들은 대개 본인 부담에 의존하고 있기 때문입니다. 보험 적용 범위가 확대되거나 합리적인 가격의 대체품이 등장하지 않는다면, ‘합리적인 가격’이라는 과제가 성장 가능성이 높은 지역 시장 성장을 계속해서 제한할 것입니다.

부문별 분석

2025년 기준으로 안경 렌즈는 시력 관리 시장의 52.45%를 차지했으며, 처방전 보급률이 높고 모든 환자층에서 도입이 용이하다는 점 덕분에 주요 제품군으로서의 위상을 유지하고 있습니다. 이는 선진국과 개발도상국 모두에서 굴절 이상을 교정하는 데 있어 안경이 수행하는 기본적인 역할을 반영하고 있습니다. 판매량 증가세는 둔화되고 있지만, 프리미엄 디자인, 첨단 코팅, 근시 진행 억제 기능 등이 수익 성장을 이끌고 있습니다.

콘택트렌즈는 가장 빠르게 성장하는 부문으로, 2031년까지의 연평균 성장률(CAGR)은 8.20%로 전망됩니다. 이러한 성장은 프리미엄 1일용 렌즈, 착용감 개선, 그리고 근시 관리에서의 역할 확대에 힘입어 이루어지고 있으며, 프리미엄 안경과의 가격 차이는 점차 좁혀지고 있습니다. 인공수정체 역시 백내장 수술 증가와, 수술 후 시야 범위를 확대하는 삼초점 렌즈 및 확장 초점 심도(EDF) 디자인으로의 전환에 힘입어 주목을 받고 있습니다.

시력 교정용 시력 관리 시장은 2025년에 시장 점유율의 44.6%를 차지한 것으로 평가되었으며, 이는 안경 판매 및 정기적인 처방 갱신 분야에서 핵심 수익원으로서의 역할을 반영하고 있습니다. 시력 관리 분야의 환자 여정은 굴절 검사와 표준 교정에서 시작되므로, 이 부문의 중요성은 앞으로도 지속될 것입니다. 그러나 의료 서비스 제공업체들은 단일 교정용 제품의 판매에 그치지 않고, 정기적인 치료, 진단 및 사후 관리를 포함하도록 진료 범위를 확대되고 있습니다.

치료 및 질환 관리는 가장 빠르게 성장하고 있는 부문으로, 2031년까지의 연평균 성장률(CAGR)은 9.10%로 전망됩니다. 보슈롬의 안구건조증 관련 제품군의 2025년도 매출액은 11억 달러를 넘어섰으며, 그중 MIEBO가 3억 1,600만 달러를 차지해 치료 시장의 확대를 여실히 보여주고 있습니다. 자외선 노출, 안구건조증, 직장 내 눈의 피로에 대한 인식이 높아짐에 따라 예방 및 보호를 위한 시력 관리가 확대되고 있습니다. 한편, 미용 및 라이프스타일 관련 시력 관리는 여전히 소규모 틈새 시장으로, 질병 유병률보다는 패션 동향, 안전 기준 준수, 도시 지역의 소비 동향에 더 큰 영향을 받고 있습니다.

지역별 분석

2025년, 북미는 전 세계 시력 관리 시장의 44.67%를 차지했습니다. 이는 높은 1인당 지출, 광범위한 민간 보험 적용, 그리고 강력한 혁신 주기에 힘입은 결과입니다. 미국은 근시 환자 수가 많고 신제품이 빠르게 시장에 출시됨에 따라 지역 수요를 주도하고 있습니다. 2025년 9월 에시롤(Essilor)사의 ‘스텔레스트(Stellest)’가 FDA 승인을 받았고, 2026년 2월 EVO ICL 치료의 적용 연령이 확대됨에 따라 프리미엄 케어에 대한 접근성이 확대되었습니다. 캐나다와 멕시코도 시장에 깊이를 더하고 있지만, 가격 결정력의 주된 원동력은 여전히 미국입니다. 비용 인플레이션이 과제로 대두되고 있는 가운데, 알콘은 2026년 실적 전망에서 관세로 인한 순영향액을 1억 2,500만 달러에서 1억 7,500만 달러로 예측했습니다.

유럽은 고령화, 확립된 임상 네트워크, 그리고 프리미엄 수술용 제품의 꾸준한 보급에 힘입어 여전히 성숙한 시력 관리 시장입니다. 서유럽과 동유럽 간에 상환 정책이나 소비자 지출에 차이가 있기 때문에 지역에 따라 성장률이 다릅니다. 예를 들어, 독일 안경 시장에서는 소비자들의 지출이 신중해지면서 2026년 초 매출 증가율이 1%에서 2%에 그쳤습니다. 에시롤 룩스오티카의 옵테그라 인수는 해당 지역에서 안과 의료 서비스와 안경 판매의 통합이 진행되고 있음을 여실히 보여주고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 10.15%에 달할 것으로 예측되며, 시력 관리 시장에서 가장 빠른 성장세를 보일 것으로 전망됩니다. 이 지역은 수요 밀도가 높으며, 동아시아의 일부 지역에서는 체계적인 공공 검진 프로그램의 지원에 힘입어 학교를 졸업하는 학생들의 근시 유병률이 80%에서 90%에 달하고 있습니다. 동아시아에서는 유병률이 높고 고급 제품의 도입이 확대되고 있지만, 중국, 일본, 인도, 동남아시아에서는 접근성 격차가 존재하기 때문에 성장 여지가 있습니다. 남미, 중동 및 아프리카는 여전히 시장 규모가 작으며, 그 발전은 고급 제품의 보급이라기보다는 도시화나 접근성 개선에 좌우되는 경향이 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the vision care market size was valued at USD 69.70 billion in 2025 and is estimated to grow from USD 75.14 billion in 2026 to reach USD 109.38 billion by 2031, at a CAGR of 7.80% during the forecast period (2026-2031).

This report is Segmented by Product Type (Spectacle Lenses, Contact Lenses, Intraocular Lenses, Ocular Health Products, Vision Correction Devices), Application (Corrective, Therapeutic, Preventive, Cosmetic), Age Group (Pediatric, Adult, Geriatric), Distribution Channel (Optical Retail, Hospitals, E-Commerce, Pharmacies), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts in Value (USD).

Global Vision Care Market Trends and Insights

Rising Refractive Errors and Myopia Burden

The vision care market is experiencing growth due to the increasing prevalence of refractive errors, particularly myopia, among children and adolescents. A 2025 review highlighted that global myopia prevalence in this group reached 35.81% in 2023 and is projected to rise to 39.80% by 2050, affecting nearly 740 million individuals. This trend is driving the market beyond single-vision correction toward products designed to slow myopia progression, enhancing value per patient. The FDA's approval of Essilor Stellest in 2025, the first spectacle lens in the U.S. to slow pediatric myopia progression, has expanded the addressable market. Additionally, China's focus on school-level myopia screenings continues to drive demand, particularly in East Asia, where prevalence rates are already high.

Aging-Driven Demand for Presbyopia and Cataract Care

The aging population is fueling demand for presbyopia correction, cataract surgeries, and improved postoperative vision, contributing to the vision care market's growth. Cataracts remain the leading cause of global blindness, with over 20 million surgeries performed annually, including 4.3 million in Europe and 3.8 million in the U.S. The market is seeing a shift toward premium intraocular lenses, which reduce spectacle dependence and generate out-of-pocket payments even in reimbursed systems. Alcon's launch of Clareon PanOptix Pro in 2025 and Bausch + Lomb's reported premium IOL growth of over 20% in Q4 2025 highlight the increasing preference for advanced visual outcomes. With global blindness and visual impairments projected to rise from 338.3 million in 2020 to 535 million by 2050, the aging trend will continue to support market expansion

Premium-Product Affordability and Reimbursement Gaps

The vision care market faces a significant challenge as clinical needs far exceed the affordability of premium corrective or therapeutic services for many patients. The World Health Organization's SPECS 2030 framework aims to address this gap by increasing coverage for refractive error services by 2030. Annual productivity losses from uncorrected myopia are estimated at USD 244 billion globally, with many in low-income regions still lacking basic eyeglasses. This economic barrier impacts the adoption of fast-growing product segments like myopia-control lenses and premium surgical implants, which often rely on out-of-pocket spending. Without expanded reimbursements or affordable alternatives, affordability will continue to limit growth in high-potential regions.

Other drivers and restraints analyzed in the detailed report include:

- Digital-Eye-Strain Demand for Premium Lenses and Coatings

- Omnichannel Optical Retail and E-Commerce Expansion

- Counterfeit Products and Online Compliance Friction

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Spectacle lenses accounted for 52.45% of the vision care market in 2025, maintaining their position as the leading product type due to their widespread prescription and ease of adoption across patient groups. This reflects the foundational role of spectacles in addressing refractive errors in both developed and developing regions. Premium designs, advanced coatings, and myopia-control features are driving revenue growth, even as unit sales grow at a slower pace.

Contact lenses are the fastest-growing segment, with an 8.20% CAGR projected through 2031. Growth is driven by premium daily disposables, improved comfort, and their increasing role in myopia management, narrowing the value gap with premium spectacles. Intraocular lenses are also gaining traction due to rising cataract surgeries and a shift toward trifocal and extended-depth-of-focus designs, enhancing postoperative visual range.

Corrective vision care held 44.6% of the market share in 2025, reflecting its role as the core revenue driver for optical dispensing and routine prescription updates. Most patient journeys in vision care begin with refraction and standard correction, ensuring the segment's continued relevance. However, providers are broadening the scope of visits to include recurring therapy, diagnostics, and follow-up care, moving beyond single corrective sales.

Therapeutic and disease management is the fastest-growing segment, with a 9.10% CAGR projected through 2031. Bausch + Lomb's dry eye portfolio exceeded USD 1.1 billion in FY2025 revenue, with MIEBO contributing USD 316 million, highlighting the growing therapeutic market. Preventive and protective vision care is expanding as awareness of UV exposure, dry eye, and workplace strain increases. Cosmetic and lifestyle vision care remains a smaller niche, influenced more by fashion trends, safety compliance, and urban spending than disease prevalence.

Geography Analysis

In 2025, North America accounted for 44.67% of the global vision care market, driven by high per-capita spending, extensive private coverage, and strong innovation cycles. The U.S. leads regional demand due to a significant myopic population and rapid commercialization of new products. The FDA's approval of Essilor Stellest in September 2025 and the expanded age criteria for EVO ICL treatments in February 2026 have broadened access to premium care. While Canada and Mexico add depth, the U.S. remains the primary driver of pricing power. Cost inflation poses a challenge, with Alcon projecting a net tariff impact of USD 125 million to USD 175 million in its 2026 guidance.

Europe remains a mature vision care market, supported by aging populations, established clinical networks, and steady adoption of premium surgical products. Growth varies across the region due to differences in reimbursement policies and consumer spending between Western and Eastern Europe. Germany's optical market, for example, reported only 1% to 2% revenue growth in early 2026, constrained by cautious consumer spending. EssilorLuxottica's acquisition of Optegra highlights the growing integration of ophthalmology services with optical dispensing in the region.

Asia-Pacific is projected to achieve the fastest growth in the vision care market, with a 10.15% CAGR through 2031. The region benefits from high demand density, with myopia prevalence reaching 80% to 90% among school-leavers in parts of East Asia, supported by systematic public screening programs. East Asia leans toward high prevalence and premium product adoption, while China, Japan, India, and Southeast Asia offer growth potential due to uneven access. South America and the Middle East and Africa remain smaller contributors, with progress tied to urbanization and improved access rather than premium product penetration.

- Alcon

- Bausch + Lomb Corporation

- CooperVision Inc.

- EssilorLuxottica

- Fielmann Group

- HOYA

- JINS

- Johnson & Johnson

- Menicon

- Nidek

- Rayner

- Rodenstock

- Safilo Group S.p.A.

- SEED Co. Ltd.

- Shamir Optical Industry

- STAAR Surgical

- Topcon

- Visioneering Technologies

- Warby Parker

- ZEISS Vision Care / Carl Zeiss Meditec

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Refractive Errors and Myopia Burden

- 4.2.2 Aging-Driven Demand for Presbyopia and Cataract Care

- 4.2.3 Digital-Eye-Strain Demand for Premium Lenses and Coatings

- 4.2.4 Omnichannel Optical Retail and E-Commerce Expansion

- 4.2.5 FDA-Authorized Pediatric Myopia-Control Spectacles

- 4.2.6 Approved Low-Dose Atropine Broadens Pediatric Myopia Care

- 4.3 Market Restraints

- 4.3.1 Premium-Product Affordability and Reimbursement Gaps

- 4.3.2 Counterfeit Products and Online Compliance Friction

- 4.3.3 Tariff-Driven Cost Inflation in Optical Inputs

- 4.3.4 Quality-System Recalls and Single-Source Component Risk

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Spectacle Lenses

- 5.1.2 Contact Lenses

- 5.1.3 Intraocular Lenses

- 5.1.4 Ocular Health Products

- 5.1.5 Vision Correction Systems and Devices

- 5.2 By Application

- 5.2.1 Corrective Vision Care

- 5.2.2 Therapeutic and Disease Management

- 5.2.3 Preventive and Protective Vision Care

- 5.2.4 Cosmetic and Lifestyle Vision Care

- 5.3 By Age Group

- 5.3.1 Pediatric

- 5.3.2 Adult

- 5.3.3 Geriatric

- 5.4 By Distribution Channel

- 5.4.1 Optical Retail Stores and Chains

- 5.4.2 Hospitals and Ophthalmology Clinics

- 5.4.3 E-Commerce Platforms

- 5.4.4 Pharmacies and Drugstores

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Alcon Inc.

- 6.3.2 Bausch + Lomb Corporation

- 6.3.3 CooperVision Inc.

- 6.3.4 EssilorLuxottica

- 6.3.5 Fielmann Group

- 6.3.6 HOYA Corporation

- 6.3.7 JINS

- 6.3.8 Johnson & Johnson Vision

- 6.3.9 Menicon Co., Ltd.

- 6.3.10 Nidek Co., Ltd.

- 6.3.11 Rayner

- 6.3.12 Rodenstock GmbH

- 6.3.13 Safilo Group S.p.A.

- 6.3.14 SEED Co. Ltd.

- 6.3.15 Shamir Optical Industry

- 6.3.16 STAAR Surgical

- 6.3.17 Topcon Corporation

- 6.3.18 Visioneering Technologies

- 6.3.19 Warby Parker

- 6.3.20 ZEISS Vision Care / Carl Zeiss Meditec

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment