|

시장보고서

상품코드

2064354

진통제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Analgesics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

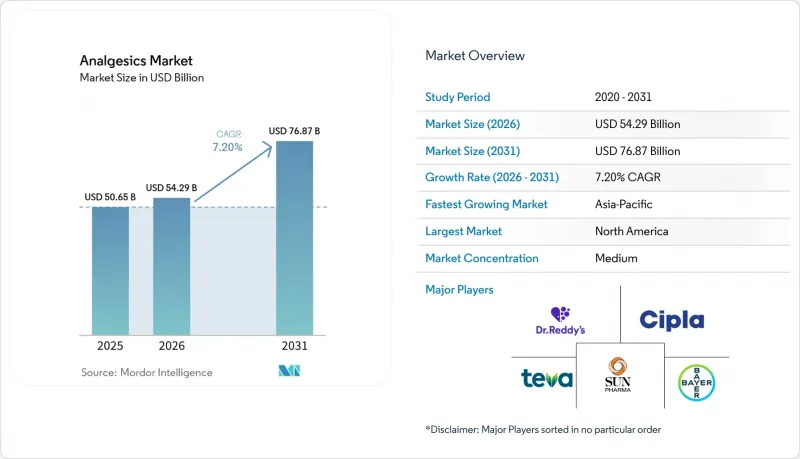

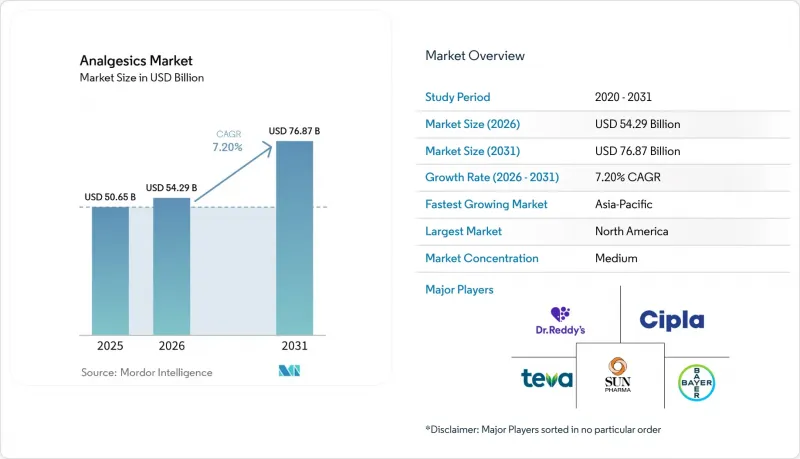

Mordor Intelligence에 의하면, 진통제 시장 규모는 2025년에 506억 5,000만 달러로 평가되었고 2026년 542억 9,000만 달러에서 2031년까지 768억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 7.20%를 나타낼 전망입니다.

본 보고서는 유형(처방약, 일반의약품), 약물 분류별(오피오이드, NSAIDs, 아세트아미노펜, 복합제, 국소/외용 진통제), 투여 경로(경구, 비경구, 외용, 경피, 직장), 통증 유형(근골격계, 외과적, 암, 신경병성, 편두통, 치과, 산과, 소아), 유통 채널(병원, 소매, 온라인 약국) 및 지역별로 분류되어 있습니다. 금액(달러).

세계 진통제 시장 동향 및 인사이트

증가하는 만성 통증과 근골격계의 부담

단일 질환이라기보다는 여러 요인의 영향을 받는 만성 통증은 진통제 시장의 주요 성장 동력입니다. 고령화, 비만, 장시간 앉아 있는 생활 습관, 그리고 중증 질환의 생존 기간 연장으로 인해 재발하는 통증에 대해 지속적인 치료가 필요한 환자 수가 증가하고 있습니다. 2025년 연구에 따르면, 2050년까지 55세 이상 성인의 퇴행성 관절염 환자 수가 증가할 것으로 예측되며, 이로 인해 근골격계 통증 치료에 대한 지속적인 수요가 부각되고 있습니다. 높은 BMI는 퇴행성 관절염과 관련된 기능 장애에 크게 기여하고 있으며, 고령화와 대사 위험 요인을 통해 환자층을 확대시키고 있습니다. 이러한 추세는 병원, 전문 클리닉, 소매점에서 수요를 뒷받침하는 한편, 장기적인 통증 관리를 위한 병용 전략과 특정 대상에 초점을 맞춘 제품의 매력도 높이고 있습니다.

고령화에 따른 퇴행성 관절염 및 신경성 통증 치료 수요 증가

진통제 시장은 북미, 유럽, 일본, 한국, 아시아의 도시 지역 등 고령화와 대사성 질환이 동시에 나타나는 지역에서 수요가 높은 것으로 나타납니다. 관절통과 신경통 모두에서 치료 대상이 되는 환자층이 확대되고 있습니다. 더 긴 치료 기간과 신중한 관리가 필요한 신경병성 통증은 2031년까지 가장 빠르게 성장할 통증 범주가 될 것으로 예측됩니다. 퇴행성 관절염은 여전히 광범위한 환자층을 유지하고 있으며, 근골격계 통증이 시장 수요의 핵심으로 자리 잡고 있습니다. 이러한 퇴행성 질환과 신경병성 질환으로 인한 이중적인 수요로 인해, 공급업체들은 기존의 오피오이드나 기본적인 경구용 진통제를 넘어선 제품 포트폴리오 다각화를 추진하고 있습니다.

오피오이드 남용 방지 대책 및 처방 규제 강화

오피오이드 규제는 진통제 시장의 일부를 계속해서 제한하는 한편, 대체 약물에 대한 기회를 창출하고 있습니다. 미국 마약단속국(DEA)은 2026년 옥시코돈 생산 할당량을 6% 이상 감축했으며, 주요 오피오이드의 할당량 감축은 10년 연속으로 이어졌습니다. 이러한 공급 환경의 긴축으로 인해, 병원에서 사용되는 중요한 진통제를 비롯한 일부 스케줄 II 의약품공급 부족에 대처하는 것이 과제가 되고 있습니다. 규제 당국의 감시도 처방 의사의 행동에 영향을 미치고 있어, 일상 진료에서 오피오이드의 장기 사용은 예전만큼 지속 가능하지 않게 되었습니다. 그 결과, 시장은 오피오이드의 기반 일부를 유지하면서도, 더 안전하고 표적화된 대안으로 성장의 초점을 옮겨가고 있습니다.

부문별 분석

2025년, 처방 진통제는 시장 매출의 67.29%를 차지하며 진통제 시장에서 주도적인 위치를 유지했습니다. 이러한 우위는 암성 통증, 수술 후 통증, 신경병성 통증 및 중증 근골격계 질환에 대한 병원 기반 치료에 대한 의존도를 반영하고 있습니다. 의사의 관리, 투여량 조절, 그리고 자가 관리 채널을 통해 구할 수 없는 전문 의약품에 대한 접근이 필요하기 때문에 처방약의 사용은 여전히 필수적입니다. 2025년 NOPAIN법의 시행으로 비오피오이드 치료에 대한 보험 급여가 더욱 확대되었고, 오피오이드 사용량이 감소했음에도 불구하고 처방전을 통한 치료 경로의 중요성은 여전히 보장되었습니다. 일반의약품(OTC) 진통제는 임상 수요의 변화보다는 판매 채널의 확대와 브랜드 확장에 힘입어, 2026년부터 2031년까지 연평균 성장률(CAGR) 8.20%를 기록하며 성장할 것으로 전망됩니다.

2025년 기준으로, 오피오이드는 약물 분류별 부문의 54.34%를 차지하며, 정책적 압력에도 불구하고 주도적인 위치를 유지했습니다. 이 사용 현황은 만성 통증, 완화 치료, 수술 후 관리, 그리고 대체 수단이 부족한 중증 통증 발작 상황에서 전통적으로 사용되어 온 양상을 반영하고 있습니다. 접근성이 제한된 지역에서는 오피오이드가 충족되지 않은 완화 치료 수요를 해결하기 위해 여전히 필수적입니다. 오피오이드 소비에 있어 전 세계적으로 나타나는 불균형은 시장 전반에 걸쳐 오피오이드 대체를 균등하게 추진하는 데 따르는 과제를 여실히 드러내고 있습니다.

NSAIDs는 2031년까지 연평균 성장률(CAGR) 9.10%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 의약품 군이 될 것입니다. 이러한 성장은 오피오이드 사용을 억제하는 치료법으로의 도입과 근골격계, 염증성 및 시술 후 통증 관리 분야에서 폭넓게 적용됨에 따라 주도되고 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 41.67%를 차지하며 진통제 시장에서 가장 큰 기여를 하는 지역으로서의 위상을 유지했습니다. 이 지역은 높은 의약품 지출, 강력한 브랜드의 입지, 그리고 대규모 만성 통증 환자층이라는 이점을 누리고 있습니다. ‘NOPAIN법’이나 오피오이드 공급 규제 강화와 같은 정책 변화가 시장을 계속해서 형성하고 있으며, 치료 접근법이 진화하는 가운데 북미가 가치 창출에서 중심적인 역할을 계속할 것으로 확실시되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 10.15%를 나타낼 것으로 예측되며, 진통제 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 이 지역의 성장은 만성 질환 부담 증가, 도시 지역의 의료 인프라 확충, 그리고 일반의약품(OTC) 및 처방전이 필요한 진통 요법에 대한 접근성 개선에 힘입어 이루어지고 있습니다. 2025년 Haleon이 중국의 OTC 합작 사업에서 잔여 지분 12%를 인수한 것은 이 중요한 성장 분야에서 지역 내 사업 확장과 시장 지배력 확보에 대한 전략적 초점을 여실히 보여주고 있습니다.

유럽은 확립된 의료 제도와 처방약 및 일반의약품 진통제에 대한 균형 잡힌 수요에 힘입어, 성숙 단계에 접어들었음에도 여전히 활기찬 시장을 유지하고 있습니다. 고령화, 만성 통증 유병률, 그리고 보험 급여 제도가 수요를 뒷받침하고 있으며, 규제 변경이 시장에 활력을 불어넣고 있습니다. 중동 및 아프리카는 규모는 작지만, 도시화와 제도 정비를 통해 완만한 성장 가능성을 보이고 있습니다. 남미 역시 고령화와 소매 약국 네트워크의 확장에 힘입어 꾸준한 수요를 보이고 있습니다. 이러한 지역들이 하나로 뭉쳐 진통제 시장의 성장을 주요 수익원 이외의 분야로도 다각화하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the analgesics market size was valued at USD 50.65 billion in 2025 and is estimated to grow from USD 54.29 billion in 2026 to reach USD 76.87 billion by 2031, at a CAGR of 7.20% during the forecast period (2026-2031).

This report is Segmented by Type (Prescription, OTC), Drug Class (Opioids, Nsaids, Acetaminophen, Combination, Local/Topical Analgesics), Route of Administration (Oral, Parenteral, Topical, Transdermal, Rectal), Pain Type (Musculoskeletal, Surgical, Cancer, Neuropathic, Migraine, Dental, Obstetric, Pediatric), Distribution Channel (Hospital, Retail, Online Pharmacies), and Geography. Value (USD).

Global Analgesics Market Trends and Insights

Rising Chronic Pain And Musculoskeletal Burden

Chronic pain, influenced by multiple factors rather than a single disease, is a key driver of the analgesics market. Aging, obesity, sedentary lifestyles, and longer survival after major illnesses are increasing the number of patients requiring ongoing treatment for recurring pain. A 2025 study projected a rise in osteoarthritis cases among adults aged 55 and older through 2050, highlighting sustained demand for musculoskeletal pain therapies. High BMI contributes significantly to osteoarthritis-related disabilities, expanding the patient pool through aging and metabolic risks. This trend supports demand across hospitals, specialty clinics, and retail settings, while boosting the appeal of combination strategies and targeted products for long-term pain management.

Aging-Linked Osteoarthritis And Neuropathic Pain Demand Increase

The analgesics market is experiencing strong demand in regions where aging and metabolic diseases overlap, such as North America, Europe, Japan, South Korea, and urban Asia. The treated population is expanding for both joint and nerve pain. Neuropathic pain, requiring longer treatment and careful adjustments, is projected to be the fastest-growing pain category through 2031. Osteoarthritis continues to maintain a broad patient base, keeping musculoskeletal pain central to market demand. This dual demand from degenerative and neuropathic conditions is driving suppliers to diversify portfolios beyond traditional opioids and basic oral analgesics.

Opioid Misuse Controls And Tighter Prescribing Frameworks

Opioid controls continue to restrict a segment of the analgesics market while creating opportunities for alternatives. The DEA has reduced oxycodone production quotas by over 6% for 2026, marking the tenth consecutive year of quota reductions for key opioids. This tighter supply environment has led to challenges in managing shortages for several Schedule II medicines, including critical hospital pain therapies. Regulatory oversight is also influencing prescriber behavior, making long-term opioid use less sustainable in routine practice. As a result, the market retains a portion of its opioid base but is shifting growth toward safer and more targeted options.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Non-Opioid And Multimodal Pain Care Protocols

- Online Pharmacy Expansion for OTC Analgesic Access

- NSAID And Acetaminophen Safety Liabilities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, prescription analgesics accounted for 67.29% of market revenue, maintaining their leadership in the analgesics market. This dominance reflects the reliance on hospital-based treatments for cancer pain, post-surgical pain, neuropathic pain, and severe musculoskeletal conditions. Prescription use remains essential due to physician oversight, dosage adjustments, and access to specialized products unavailable in self-care channels. The NOPAIN Act's implementation in 2025 further supported reimbursement for non-opioid treatments, ensuring the relevance of prescription pathways despite reduced opioid volumes. OTC analgesics are projected to grow at a CAGR of 8.20% from 2026 to 2031, driven by channel expansion and brand extensions rather than shifts in clinical demand.

Opioids held 54.34% of the drug class segment in 2025, maintaining their leading position despite policy pressures. Their share reflects legacy use in chronic pain, palliative care, post-operative settings, and severe pain episodes where alternatives are insufficient. In regions with limited access, opioids remain critical for addressing unmet palliative care needs. The global imbalance in opioid consumption highlights the challenges of transitioning away from opioids uniformly across markets.

NSAIDs are forecast to grow at a CAGR of 9.10% through 2031, making them the fastest-growing drug class. This growth is driven by their adoption in opioid-sparing regimens and their broad application in musculoskeletal, inflammatory, and post-procedural pain management.

Geography Analysis

In 2025, North America accounted for 41.67% of global revenue, maintaining its position as the largest contributor to the analgesics market. The region benefits from high pharmaceutical spending, strong brand presence, and a significant chronic pain patient base. Policy changes, such as the NOPAIN Act and stricter opioid supply controls, continue to shape the market, ensuring North America's central role in value creation as treatment approaches evolve.

Asia-Pacific is projected to grow at a CAGR of 10.15% through 2031, making it the fastest-growing region in the analgesics market. The region's growth is driven by an increasing chronic disease burden, expanding urban healthcare infrastructure, and improved access to OTC and prescription pain therapies. Haleon's acquisition of the remaining 12% equity in its China OTC joint venture in 2025 highlights the strategic focus on regional execution and market control in this key growth area.

Europe remains a mature yet active market, supported by established healthcare systems and balanced demand for prescription and OTC analgesics. Aging populations, chronic pain prevalence, and reimbursement structures sustain demand, while regulatory changes add dynamism. The Middle East and Africa, though smaller, show potential for gradual growth due to urbanization and capacity building. South America also demonstrates steady demand, driven by aging demographics and the reach of retail pharmacy networks. Together, these regions diversify the analgesics market's growth beyond its primary revenue contributors.

- Amneal Pharmaceuticals

- Apotex

- Assertio Holdings, Inc.

- Aurobindo Pharma

- Bayer

- Cipla

- Dr. Reddy's Laboratories

- Fresenius

- Grunenthal GmbH

- Haleon plc

- Hikma Pharmaceuticals

- Kenvue Inc.

- Lupin

- Opella

- Perrigo Company

- Purdue Pharma

- Reckitt Benckiser Group

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Chronic Pain and Musculoskeletal Burden

- 4.2.2 Aging-Linked Osteoarthritis and Neuropathic Pain Demand

- 4.2.3 Shift Toward Non-Opioid and Multimodal Pain Care

- 4.2.4 Online Pharmacy Expansion for OTC Access

- 4.2.5 IV Opioid-Sparing Multimodal Post-Operative Protocols

- 4.2.6 Closing Opioid-Access Gaps in LMIC Palliative Care

- 4.3 Market Restraints

- 4.3.1 Opioid Misuse Controls and Tighter Prescribing Rules

- 4.3.2 NSAID and Acetaminophen Safety Liabilities

- 4.3.3 API Concentration and Asia Supply Dependency

- 4.3.4 Regulatory Friction in Bioequivalence and Shortage Management

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Prescription

- 5.1.2 Over-the-Counter

- 5.2 By Drug Class

- 5.2.1 Opioids

- 5.2.2 NSAIDs

- 5.2.3 Acetaminophen

- 5.2.4 Combination Analgesics

- 5.2.5 Local Anesthetics and Topical Analgesics

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Parenteral

- 5.3.3 Topical

- 5.3.4 Transdermal

- 5.3.5 Rectal

- 5.4 By Pain Type

- 5.4.1 Musculoskeletal Pain

- 5.4.2 Surgical and Trauma Pain

- 5.4.3 Cancer Pain

- 5.4.4 Neuropathic Pain

- 5.4.5 Migraine and Headache

- 5.4.6 Dental and Orofacial Pain

- 5.4.7 Obstetric and Gynecologic Pain

- 5.4.8 Pediatric Pain

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail Pharmacies and Drug Stores

- 5.5.3 Online Pharmacies

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Amneal Pharmaceuticals, Inc.

- 6.3.2 Apotex Inc.

- 6.3.3 Assertio Holdings, Inc.

- 6.3.4 Aurobindo Pharma Limited

- 6.3.5 Bayer AG

- 6.3.6 Cipla Limited

- 6.3.7 Dr. Reddy's Laboratories Ltd.

- 6.3.8 Fresenius Kabi AG

- 6.3.9 Grunenthal GmbH

- 6.3.10 Haleon plc

- 6.3.11 Hikma Pharmaceuticals PLC

- 6.3.12 Kenvue Inc.

- 6.3.13 Lupin Limited

- 6.3.14 Opella

- 6.3.15 Perrigo Company plc

- 6.3.16 Purdue Pharma L.P.

- 6.3.17 Reckitt Benckiser Group plc

- 6.3.18 Sun Pharmaceutical Industries Ltd.

- 6.3.19 Teva Pharmaceutical Industries Ltd.

- 6.3.20 Viatris Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space and Unmet-need Assessment