|

시장보고서

상품코드

2064355

모바일 헬스 앱 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)MHealth Apps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

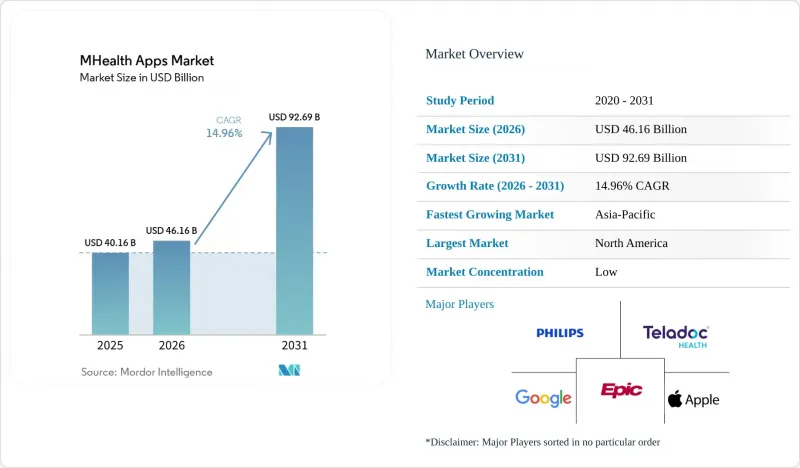

Mordor Intelligence에 의하면, 모바일 헬스 앱 시장 규모는 2025년 401억 6,000만 달러로 평가되었고, 2026년에는 461억 6,000만 달러로 추정되고, 2031년까지 926억 9,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 14.96%로 성장할 전망입니다.

본 보고서는 앱 유형별(질환 및 치료 관리, 웰니스 관리, 기타 앱), 플랫폼별(Android, iOS, 기타), 기능별(모니터링, 피트니스 솔루션, 진단, 치료, 케어 내비게이션), 최종 사용자별(환자 및 소비자, 의료 제공업체, 보험사 및 고용주, 생명과학), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

세계의 모바일 헬스 앱 시장 동향 및 인사이트

스마트폰 및 웨어러블 기기의 보급이 모바일 헬스 앱 시장의 잠재 고객 기반을 확대되고 있습니다.

2025년, 전 세계 웨어러블 기기 출하량은 6억 1,150만 대에 달했고, 전년 대비 9.1% 증가했으며, 이는 모바일 헬스 앱의 사용자 기반을 대폭 확대시켰습니다. 중국의 정책 지원과 다양한 가격대가, 특히 대규모 소비자 시장에서 커넥티드 기기의 주류화를 촉진했습니다. 2025년 9월 애플이 고혈압 알림 기능을 승인한 것은 규제 대상인 선별 검사 도구로서 소비자용 하드웨어가 수행하는 역할을 부각시켰습니다. 웨어러블 기기가 임상적으로 더 관련성이 높은 신호를 포착할 수 있게 됨에 따라, 앱 개발자들은 모니터링 및 코칭 제품을 강화하여 사용자의 입력 부담을 줄이는 동시에 참여도를 높이고 있습니다. 2026년까지 신규 웨어러블 기기의 40%가 AI 기능을 탑재할 것으로 예상되며, 이는 개인 맞춤화와 성능에 대한 기대를 높일 것으로 보입니다.

AI를 활용한 개인화를 통해, 고객 참여 모델은 ‘알림’에서 ‘예측적 케어’로 전환됩니다.

2025년에 수행된 66건의 연구를 검토한 결과, 머신러닝 알고리즘은 61%의 사례에서 개인 맞춤형 권장 사항을 제공하여 임상시험에서 약물 복용 순응도를 향상시킨 것으로 나타났습니다. 모바일 헬스 앱 시장은 단순한 알림 기반의 상호작용을 넘어, 측정 가능한 가치를 제공해야 한다는 요구를 받고 있습니다. 또한 AI는 트리아지 및 위험 우선순위 지정을 강화하고, 경보 피로를 줄임으로써 의료진의 업무 흐름도 개선하고 있습니다. Tempus AI는 2025년 1월에 ‘olivia’를 출시하여 1,000개 이상의 의료 시스템과 연동해 AI 기반 임상 요약문을 생성하고 있습니다. 이러한 협업형 치료로의 전환은 기록, 기기 데이터, 예측 분석을 통합함으로써, 개인 맞춤화를 단순한 알림 단계에서 한 걸음 더 나아가 선제적인 개입 및 워크플로우 최적화 단계로 발전시키고 있습니다.

데이터 개인정보 보호 및 사이버 보안에 대한 감시 강화가 ‘신뢰의 비용’을 끌어올리고 있습니다.

2025년에 실시된 272개의 안드로이드 모바일 헬스 앱에 대한 감사 결과, 보안 점수는 100점 만점에 평균 47점에 그쳤으며, 42.6%가 구식 SHA-1 암호화를 사용하고 있고, 42개의 앱이 암호화되지 않은 데이터를 전송하고 있는 것으로 밝혀졌습니다. 개인정보와 관련된 불만이나 기술적 문제는 55만 3,000건 이상의 사용자 리뷰와 관련이 있는 것으로 나타났으며, 신뢰성 문제가 사용자 이탈로 이어질 수 있다는 점이 부각되었습니다. 플랫폼이 더욱 복잡한 데이터를 수집함에 따라, 모바일 헬스 앱 시장에서는 암호화, 동의 관리, 공급업체 모니터링에 드는 비용이 증가하고 있습니다. 여러 지역으로의 사업 확장은 데이터 규제의 차이로 인해 규정 준수를 더욱 복잡하게 만들고, 운영 비용을 증가시키며, 시장의 확장성을 저해하고 있습니다.

부문별 분석

2025년, 모바일 헬스 앱 시장의 54.75%를 질환 및 치료 관리 앱이 차지했습니다. 이는 CGM(연속 혈당 모니터링)과 연계된 당뇨병 관리, 약물 복용 순응도, 원격 모니터링 도구와 같은 만성 질환 분야의 활용 사례에 힘입은 결과입니다. 임상적으로 검증된 제품들이 보험 환급 및 고용주의 복리후생과 같은 수익 채널을 주도하고 있으며, 시장이 확대됨에 따라 의료 중심 용도이 라이프스타일 앱을 앞지르고 있습니다.

웰니스 관리 앱 시장은 피트니스 추적, 영양 지원, 정신 건강, 수면 모니터링, 체중 관리에 힘입어 2026-2031년 연평균 성장률(CAGR) 16.70%를 기록하며 성장할 것으로 전망됩니다. 이 카테고리는 예방 단계의 초기 단계부터 사용자를 참여시킴으로써 시장 확대에 기여하고 있습니다. DexCom은 2025년에 동반자 앱 기능을 탑재한 G7 15 Day CGM 시스템을 출시하며, 임상 분야에서의 수익 창출과 예방 중심의 보급 사이에서 균형을 맞추었습니다.

2025년, 모바일 헬스 앱 시장 매출의 48.75%를 iOS가 차지했습니다. 이는 사용자 1인당 매출액의 높음, Apple Watch와의 연동, 그리고 북미와 서유럽에서의 확고한 입지에 힘입은 결과입니다. 이 플랫폼은 사용자가 원활한 생태계를 중시하는 프리미엄 만성 질환 관리 및 기업 주도형 프로그램 분야에서 뛰어난 성과를 보여줍니다.

안드로이드는 남아시아 및 동남아시아의 스마트폰 보급 확대에 힘입어, 2026-2031년 연평균 성장률(CAGR) 17.45%를 기록하며 성장할 것으로 전망됩니다. 저가형 단말기는 특히 확장 가능한 모바일 헬스케어 도구에 대한 수요가 증가하고 있는 지역에서 목표 시장을 확대하고 있으며, 안드로이드는 시장 규모 확대에 있어 매우 중요한 역할을 하고 있습니다.

지역별 분석

2025년, 북미는 모바일 헬스 앱 시장의 41.61%를 차지했으며, 최대 지역 기여자로서의 위상을 유지했습니다. 이 지역은 인터넷 접속의 보급, 만성 질환의 높은 유병률, 그리고 2025년 메디케어 의사 보수 일정에 기반한 디지털 치료를 지원하는 보상 구조의 혜택을 받고 있습니다. 미국에서는 2025년 1월 기준으로 민간 보험에 가입한 환자의 14.9%가 원격의료 비용을 청구했으며, 원격의료를 통한 진단 중 58.5%를 정신 질환이 차지하고 있습니다. 보험 가입자 밀도가 높고 전자의무기록(EHR) 도입이 활발히 진행되고 있는 점이, 환급 대상이 되는 통합형 용도 모델에 대한 해당 지역의 적합성을 한층 더 높이고 있습니다.

유럽은 자금력이 풍부한 사업자에게 유리한 엄격한 데이터 거버넌스와 의료기기 규제의 영향으로, 모바일 헬스 앱 시장에서 여전히 2위의 규모를 유지하고 있습니다. GDPR(EU 개인정보보호규정)이나 의료기기 규정(MDR)과 같은 체계는 규정 준수 기준을 높여, 소규모 공급업체에게는 장벽이 되고 있습니다. 영국의 NHS 앱이나 독일의 DiGA 프레임워크와 같은 공적 보험자의 지원책은 보험 급여와 규정 준수 요건을 조화시킴으로써 지속 가능한 성장을 뒷받침하고 있습니다.

아시아태평양은 2026-2031년 연평균 성장률(CAGR) 15.66%를 기록하며 성장할 것으로 예상되며, 모바일 헬스 앱 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 중국은 웨어러블 기기의 보급에 힘입어 해당 지역을 주도하고 있으며, 손목 착용형 기기 시장 규모는 2026년까지 7,958만 대에 달할 것으로 예측됩니다. 화웨이는 2025년에 2,550만 대의 스마트 워치를 출하하여 전년 대비 21.7% 증가했습니다. 인도는 디지털 헬스케어 정책과 저비용 구독 모델을 가능하게 하는 결제 인프라에 힘입어 가장 빠르게 성장하고 있는 국가 시장입니다. 중동 및 아프리카은 수익 규모는 작지만, GCC 국가들의 디지털 헬스케어 투자와 새로운 의료 제공 모델의 부상으로 성장 궤도에 올라섰습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

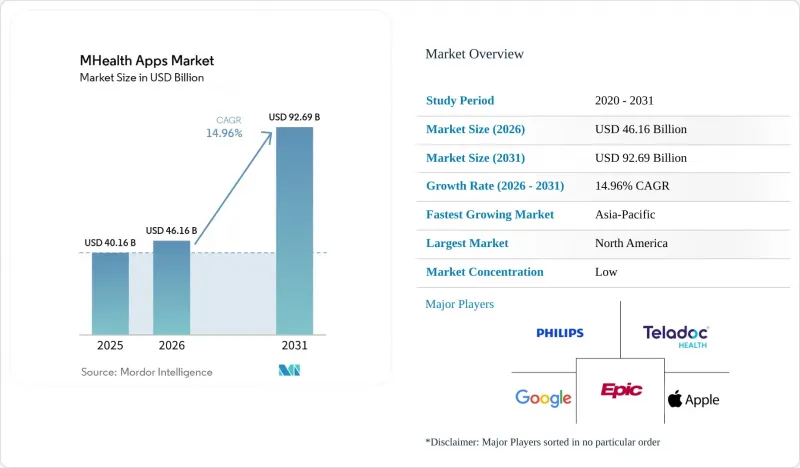

AJY 26.06.24According to Mordor Intelligence, the mHealth apps market size is expected to increase from USD 40.16 billion in 2025 to USD 46.16 billion in 2026 and reach USD 92.69 billion by 2031, growing at a CAGR of 14.96% over 2026-2031.

This report is Segmented by App Type (Disease & Treatment Management, Wellness Management, Other App Types), Platform (Android, IOS, Others), Functionality (Monitoring, Fitness Solutions, Diagnostics, Treatment, Care Navigation), End User (Patients & Consumers, Healthcare Providers, Payers & Employers, Life Sciences), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts in Value (USD).

Global MHealth Apps Market Trends and Insights

Smartphone and Wearable Penetration Extends the mHealth Apps Market's Addressable Base

In 2025, global wearable device shipments reached 611.5 million units, a 9.1% increase from the previous year, significantly expanding the user base for mHealth apps. Policy support and diverse price tiers in China drove connected devices into mainstream adoption, especially in high-volume consumer markets. Apple's approval for its Hypertension Notification Feature in September 2025 highlighted the role of consumer hardware as a regulated screening tool. With wearables capturing more clinically relevant signals, app developers are enhancing monitoring and coaching products, reducing user input effort and increasing engagement. By 2026, 40% of new wearables are expected to feature AI-enabled functions, driving personalization and performance expectations.

AI-Enabled Personalization Shifts the Engagement Model From Reminders to Anticipatory Care

A 2025 review of 66 studies showed machine learning algorithms delivered personalized recommendations in 61% of cases and improved medication adherence in trials. The mHealth apps market is under pressure to deliver measurable value beyond reminder-based interactions. AI is also improving provider workflows by enhancing triage and risk prioritization, reducing alert fatigue. Tempus AI launched 'olivia' in January 2025, integrating with over 1,000 health systems and generating AI-driven clinical summaries. This shift towards coordinated care combines records, device data, and predictive analytics, moving personalization from reminders to proactive interventions and workflow optimization.

Data Privacy and Cybersecurity Scrutiny Elevate the Cost of Trust

A 2025 audit of 272 Android mHealth apps revealed an average security score of 47 out of 100, with 42.6% using outdated SHA-1 encryption and 42 apps transmitting unencrypted data. Privacy complaints and technical issues were linked to over 553,000 user reviews, highlighting how trust issues can lead to user abandonment. The mHealth apps market faces rising costs for encryption, consent management, and vendor oversight as platforms collect more complex data. Expanding into multiple regions further complicates compliance due to varying data regulations, increasing operating costs and slowing market scalability.

Other drivers and restraints analyzed in the detailed report include:

- Reimbursable Digital Therapeutics Pathways Create a Structural Revenue Floor

- EHR-Embedded Digital Prescribing Workflows Convert App Downloads Into Care Pathways

- Low Long-Term Engagement Undermines Clinical Outcome Evidence and Commercial Viability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Disease and Treatment Management Apps accounted for 54.75% of the mHealth apps market, driven by chronic condition use cases like CGM-linked diabetes management, medication adherence, and remote monitoring tools. Clinically validated products dominate revenue channels such as reimbursement and employer benefits, keeping medically oriented applications ahead of lifestyle offerings as the market expands.

Wellness Management Apps are projected to grow at a 16.70% CAGR from 2026 to 2031, fueled by fitness tracking, nutrition support, mental wellness, sleep monitoring, and weight management. This category broadens the market by engaging users earlier in the prevention journey. DexCom launched its G7 15 Day CGM system in 2025 with companion app features, balancing clinical monetization with prevention-led adoption.

In 2025, iOS captured 48.75% of revenue in the mHealth apps market, driven by higher revenue per user, integration with Apple Watch, and strong positioning in North America and Western Europe. The platform excels in premium chronic care and employer-sponsored programs, where users value its seamless ecosystem.

Android is forecast to grow at a 17.45% CAGR from 2026 to 2031, supported by widespread smartphone adoption in South and Southeast Asia. Affordable devices expand the addressable market, particularly in regions with rising demand for scalable mobile health tools, making Android pivotal for market scale.

Geography Analysis

In 2025, North America accounted for 41.61% of the mHealth apps market, maintaining its position as the largest regional contributor. The region benefits from widespread internet access, a high prevalence of chronic diseases, and a reimbursement structure supporting digital therapeutics under the 2025 Medicare Physician Fee Schedule. In the United States, 14.9% of commercially insured patients had telehealth claims in January 2025, with mental health conditions comprising 58.5% of telehealth diagnostic encounters. High payer density and mature EHR adoption further enhance the region's suitability for reimbursable and integrated application models.

Europe remained the second-largest region in the mHealth apps market, driven by stringent data governance and device regulations that favor well-capitalized operators. Frameworks like GDPR and the Medical Device Regulation raise compliance standards, creating barriers for smaller vendors. Public payer pathways, such as the NHS App in the UK and Germany's DiGA framework, support sustainable growth by aligning reimbursement with compliance requirements.

Asia-Pacific is projected to grow at a 15.66% CAGR from 2026 to 2031, making it the fastest-growing region in the mHealth apps market. China leads the region, supported by strong adoption of wearable devices, with its wrist-worn device market expected to reach 79.58 million units by 2026. Huawei shipped 25.5 million smartwatches in 2025, reflecting a 21.7% year-over-year increase. India is the fastest-growing country market, driven by digital health policies and payment infrastructure enabling low-cost subscription models. The Middle East and Africa, though smaller in revenue, are on a growth trajectory due to digital health investments in GCC countries and emerging care delivery models.

- Abbott Laboratories

- Ada Health GmbH

- AirStrip Technologies, Inc.

- Apple

- Calm.com, Inc.

- Dexcom

- Doximity, Inc.

- Epic Systems

- Garmin

- Google LLC / Fitbit

- Headspace, Inc.

- Koninklijke Philips

- Medisafe, Inc.

- MyFitnessPal, Inc.

- Noom, Inc.

- Omada Health

- Samsung Group

- Teladoc Health

- Veradigm

- Withings S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Smartphone and Wearable Penetration

- 4.2.2 Rising Chronic Disease Self-Management Demand

- 4.2.3 Telehealth and Remote Monitoring Normalization

- 4.2.4 AI-Enabled Personalization and Analytics

- 4.2.5 Reimbursable Digital Therapeutics Pathways

- 4.2.6 EHR-Embedded Digital Prescribing Workflows

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cybersecurity Scrutiny

- 4.3.2 Low Long-Term Engagement and App Abandonment

- 4.3.3 Rising Clinical Evidence Burden for Samd and AI Claims

- 4.3.4 App-Store Data-Sharing Enforcement and Cross-Border Data Rules

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By App Type

- 5.1.1 Disease & Treatment Management Apps

- 5.1.1.1 Chronic Disease Management Apps

- 5.1.1.2 Medication Adherence Apps

- 5.1.1.3 Remote Monitoring Apps

- 5.1.1.4 Women's Health & Pregnancy Apps

- 5.1.1.5 Diagnostic & Symptom Checker Apps

- 5.1.2 Wellness Management Apps

- 5.1.2.1 Fitness & Exercise Tracking Apps

- 5.1.2.2 Nutrition & Diet Apps

- 5.1.2.3 Mental Wellness & Mindfulness Apps

- 5.1.2.4 Sleep Tracking Apps

- 5.1.2.5 Weight Management Apps

- 5.1.3 Other App Types

- 5.1.3.1 Personal Health Record Apps

- 5.1.3.2 Telehealth & Virtual Consultation Apps

- 5.1.3.3 Health Education & Awareness Apps

- 5.1.3.4 Professional Reference & Networking Apps

- 5.1.1 Disease & Treatment Management Apps

- 5.2 By Platform

- 5.2.1 Android

- 5.2.2 iOS

- 5.2.3 Other Platforms

- 5.3 By Functionality

- 5.3.1 Monitoring Services

- 5.3.2 Fitness Solutions

- 5.3.3 Diagnostic Services

- 5.3.4 Treatment Services

- 5.3.5 Care Navigation & Engagement

- 5.4 By End User

- 5.4.1 Patients & Consumers

- 5.4.2 Healthcare Providers

- 5.4.3 Payers & Employers

- 5.4.4 Life Sciences & Research Organizations

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Ada Health GmbH

- 6.3.3 AirStrip Technologies, Inc.

- 6.3.4 Apple Inc.

- 6.3.5 Calm.com, Inc.

- 6.3.6 DexCom, Inc.

- 6.3.7 Doximity, Inc.

- 6.3.8 Epic Systems Corporation

- 6.3.9 Garmin Ltd.

- 6.3.10 Google LLC / Fitbit

- 6.3.11 Headspace, Inc.

- 6.3.12 Koninklijke Philips N.V.

- 6.3.13 Medisafe, Inc.

- 6.3.14 MyFitnessPal, Inc.

- 6.3.15 Noom, Inc.

- 6.3.16 Omada Health, Inc.

- 6.3.17 Samsung Electronics Co., Ltd.

- 6.3.18 Teladoc Health, Inc.

- 6.3.19 Veradigm LLC

- 6.3.20 Withings S.A.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment