|

시장보고서

상품코드

2064360

의약품 관리용 AI 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)AI In Medication Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

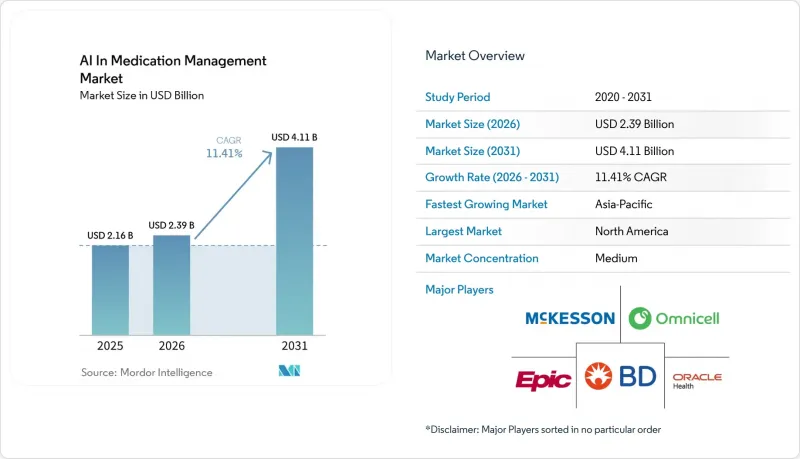

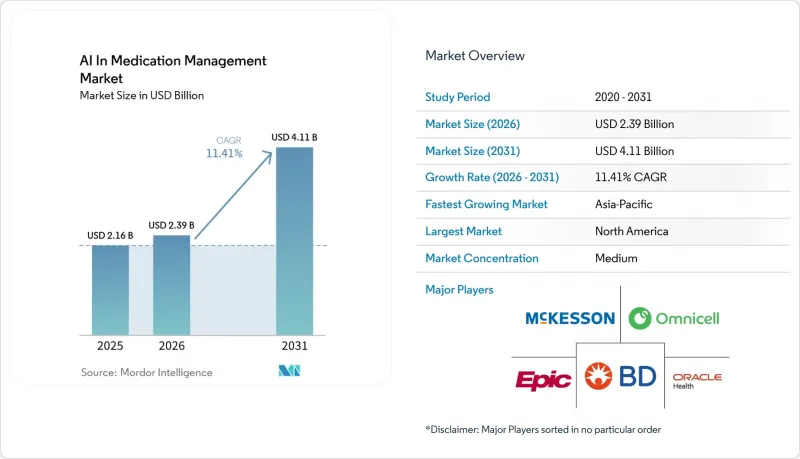

Mordor Intelligence에 의하면, 의약품 관리용 AI(인공지능) 시장 규모는 2025년 21억 6,000만 달러로 평가되었고, 2026년에는 23억 9,000만 달러로 추정되고, 2026-2031년 CAGR 11.41%로 성장을 지속할 전망이며, 2031년까지 41억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소별(소프트웨어, 서비스, 하드웨어), 배포 방식별(클라우드 기반 등), 기술별(머신러닝 및 예측 모델 등), 용도별(의사 결정 지원, 복약 순응도 등), 최종 사용자별(병원, 약국 등), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 의약품 관리용 AI 시장 동향 및 고찰

증가하는 투약 오류 및 약물 유해 사건(ADE)의 부담

의약품 관리용 AI 시장은 투약 오류나 유해 사건으로 인한 높은 임상 및 경제적 부담을 배경으로 계속해서 지지를 얻고 있습니다. 『Frontiers in Pharmacology』지 2025년 11월호에 실린 평가에 따르면, 미국의 입원 환자에서 연간 180만 건의 이상반응이 발생하고 있으며, 이와 관련된 사망자 수는 9,000명, 관련 비용은 400억 달러 이상에 달하는 것으로 보고되었습니다. 『BMC Medical Informatics and Decision Making』 저널의 또 다른 조사에 따르면, 의도차 않은 약물 부작용은 미국에서 매년 3,600만 명 이상의 입원 환자에게 영향을 미치고 있으며, 연간 치료비는 15억 달러를 초과합니다. 처방 약물의 양이 증가하고 의료진이 더 많은 경보에 대응해야 하는 상황에서 수동 확인의 신뢰성이 떨어지기 때문에 이러한 부담으로 인해 의료진은 처방전을 검토하고 위험 신호를 지속적으로 모니터링할 수 있는 AI 시스템으로 눈을 돌리고 있습니다. 『Digital Health』지의 2025년 체계적 문헌고찰에 따르면, AI가 생성한 경고의 85%는 임상적으로 타당했으며, 43%는 처방 내용의 수정으로 이어졌습니다. 이는 병원이 AI 기반 심사 체계를 끊임없는 의약품 안전 사고에 대한 실질적인 대응책으로 간주하는 이유를 설명하는 한 가지 요인이 되고 있습니다.

다제 병용 및 복잡한 투약 요법의 복잡성

의약품 관리용 AI 시장은 고령자나 여러 가지 만성 질환을 앓고 있는 환자들이 사용하는 치료 계획이 복잡해짐에 따라 더욱 성장하고 있습니다. 『헬스케어』지의 2024년 리뷰에 따르면, 외래 환자의 다제 병용률은 30.2%, 입원 환자의 경우 61.7%에 달하며, 이는 복잡한 약물 사용이 의료 서비스에 얼마나 널리 퍼져 있는지를 보여주고 있습니다. 같은 연구 결과에 따르면, 약물이 하나 추가될 때마다 이상반응의 위험이 12%에서 18%까지 증가하는 것으로 나타났으며, 이에 따라 상호작용의 위험을 파악하고 약물 감량 대상 약물을 특정할 수 있는 AI 도구의 가치가 높아지고 있습니다. 2025년에 발표된 ABiMed의 연구에 따르면, 응급실 내원 건수의 감소로 인해 환자 1인당 연간 273유로(298달러)의 비용 절감이 예상되며, 이에 따라 약물 검토는 임상적 필요성에서 측정 가능한 효율화 수단으로 변화하고 있습니다. 2025년 『Cureus』지에 발표된 스코핑 리뷰에 따르면, AI 도구가 50세 이상 성인을 대상으로 잠재적으로 부적절한 약물이나 반복적으로 나타나는 다중 질환 동반 패턴을 감지하는 데 효과적인 것으로 밝혀졌습니다. 이는 이러한 환자층이 확대됨에 따라 플랫폼에 대한 수요가 꾸준히 증가할 것임을 뒷받침합니다.

데이터 개인정보 보호와 AI 검증의 부담

의약품 관리용 AI 시장은 데이터 개인정보 보호 규정, 내부 거버넌스 심사 및 모델 검증 요건으로 인해 여전히 큰 도입 장벽에 직면해 있습니다. 2025년 12월까지 FDA가 1,451건 이상의 AI 탑재 의료기기를 승인한 것으로 평가되었으며(2025년 한 해에만 295건의 신규 승인을 포함), 규제 당국의 기대치가 높아지는 한편, ‘사전 변경 관리 계획(Predetermined Change Control Plan)’의 틀에 따라 제조업체는 향후 알고리즘 변경 사항을 사전에 정의하고, 도입 후 모델 드리프트를 모니터링해야 합니다. 『JMIR AI』에 게재된 941명의 대학병원 의사를 대상으로 한 전국 조사에 따르면, 62%가 대표성이 부족한 훈련 데이터로 인한 편향을 주요 우려 사항으로 꼽았으며, 78.9%가 AI 시스템으로 인한 임상 오류를 우려하고 있는 것으로 나타났습니다. 2026년 1월 FDA가 발표한 특정 투명성이 높은 임상 의사결정 지원 도구에 관한 지침에 따라 일부 범주에서는 부담이 완화되었으나, 의료 시스템에서는 환자의 위험이 높은 처방전이나 의약품 안전성 모니터링의 이용 사례에 대해서는 여전히 보다 엄격한 내부 심사 절차가 유지되고 있습니다. 이는 의약품 관리용 AI 시장이 규제가 완화된 환경이 아닌, 보다 엄격한 규정 준수 체제 하에서 확대되고 있음을 의미합니다.

부문별 분석

2025년 기준으로 소프트웨어는 의약품 관리용 AI 시장 규모의 47.32%를 차지했으며, 해당 시장에서 가장 큰 비중을 차지하는 요소가 되었습니다. 이 지위는 SaaS 기반의 임상 의사결정 지원, 복약 순응도 지원 및 의약품 안전성 모니터링 도구의 지속적인 수익 구조를 반영한 것으로, 이러한 도구들은 하드웨어 교체 주기를 기다릴 필요 없이 지속적으로 업데이트할 수 있습니다. Epic이 의약품 워크플로우에 AI를 직접 통합하고 있다는 점은 이러한 추세를 뒷받침합니다. 이 회사의 고객 중 85% 이상이 적어도 하나의 AI 도구를 이용하고 있으며, Summit Health는 Epic의 Penny AI 에이전트를 통해 사전 승인 신청 시간을 42% 단축했기 때문입니다. 의약품 관리용 AI 업계에서는 단독 기능의 폭넓음보다, 이러한 수준의 워크플로우에 통합되는 것이 더 중요하게 여겨지고 있습니다. 왜냐하면, 약제팀은 이미 사용 중인 시스템 내에서 클릭 횟수와 확인 시간을 줄일 수 있는 도구를 도입하고 있기 때문입니다.

서비스 시장은 2031년까지 연평균 성장률(CAGR) 11.73%로 확대될 것으로 예측되며, 이는 도입 지원이 ‘플러그 앤 플레이’라는 슬로건으로 대체되는 것이 아니라, 소프트웨어 판매와 병행하여 확대되고 있음을 보여줍니다. 의료 기관들은 검증, 통합 엔지니어링 및 직원 변경 관리를 점점 더 외부에 위탁하고 있습니다. 이는 도입에 대한 의욕에 비해, 사내의 임상 AI 관련 전문 지식이 여전히 부족하기 때문입니다. 하드웨어는 여전히 구조적으로 중요한 위치를 차지하고 있습니다. 왜냐하면 스마트 조제 기기, 연결형 복약 준수 센서, 로봇 시스템은 의약품 워크플로우를 실행 가능하고 측정 가능하게 만드는 물리적 제어 지점으로서의 역할을 계속하고 있기 때문입니다. 옴니셀(OmniCell)사의 ‘Titan XT’와 클라우드 연동형 ‘OmniSphere’ 아키텍처는 하드웨어의 가치가 단순히 캐비닛 교체 수요뿐만 아니라 데이터 생성 및 재고 관리의 지능화와 점점 더 밀접하게 연결되고 있음을 보여줍니다.

2025년에는 클라우드 기반 솔루션의 도입 비중이 64.73%를 차지했으며, 의약품 관리용 AI 시장에서 주도적인 위치를 확립했습니다. 이러한 경쟁력은 전사적인 가시성, 초기 투자 비용 절감, 그리고 병원, 약국, 유통 거점에 걸친 약제 업무의 일원화가 가능하다는 점에 기인합니다. BD사는 AWS에서 호스팅되고 있는 자사의 ‘Incada Connected Care Platform’이 이미 도입된 Pyxis 시스템에서 하루 평균 980만 건 이상의 약품 조제 거래를 처리하고 있다고 밝혔습니다. 이는 데이터 처리 능력이 현재 진료 현장에서의 실시간 AI 추론을 뒷받침하고 있음을 보여줍니다. 따라서, 의약품 관리용 AI 시장에서 클라우드의 규모는 단순한 호스팅 선호도의 문제가 아니라, 워크플로우 통합과 데이터 밀도 모두와 관련이 있습니다.

온프레미스 배포는 2031년까지 연평균 성장률(CAGR) 11.32%로 확대될 것으로 예상되며, 클라우드가 주도권을 쥐고 있는 상황에서도 가장 빠르게 성장하고 있는 형태입니다. 주권 문제에 민감한 관할 구역의 병원에서는 특히 암호화, 감사 가능성, 국가 안보 기준이 여전히 엄격한 경우, 고위험 임상 이용 사례에 대해 로컬 추론 및 로컬 데이터 처리를 선택하고 있습니다. 2025년 8월 징저우 중앙병원이 도입한 AI 디지털 약사 시스템은 10만 종 이상의 의약품을 포괄하며, 의료 등급의 암호화 데이터를 활용한 로컬 배포형 데이터베이스를 사용했습니다. 이는 아시아 일부 지역에서 온프레미스 수요가 증가하고 있는 이유를 보여줍니다. 따라서, 특히 클라우드 분석이 필요하지만 임상 데이터 세트 전체를 로컬 환경 밖으로 옮길 수 없는 시스템의 경우, 실용적인 중간 방안으로서 하이브리드 모델이 주목받고 있습니다.

지역별 분석

2025년, 북미는 의약품 관리용 AI 시장 점유율의 38.43%를 차지했으며, 여전히 최대 지역 기여자로서의 위상을 유지했습니다. 이 지역은 EHR(전자건강기록)의 높은 보급률, 성숙한 가치 기반의 보상 제도, 그리고 처방, 문서화, 조제, 전문 약국의 업무 흐름에 이미 AI를 통합한 의료 제공업체 기반이라는 이점을 누리고 있습니다. 2026년 1월 유타주가 도입한 주 정부 주도의 자동 처방전 갱신 프로그램은 190유형의 만성 질환 치료제 처방전 갱신에 AI가 합법적으로 관여할 수 있도록 허용하며, 갱신의 적시성, 환자의 안전성, 복약 순응도 성과 및 비용 효율성을 추적할 수 있다는 점에서 특히 중요합니다. Oracle의 ‘Clinical AI Agent’ 확대와 맥케슨, BD, 옴니셀 등 기업들의 대규모 조제 및 유통 자동화는 북미가 시범 운영 단계에서 업무에 통합된 인프라로 전환되고 있음을 보여줍니다. 이 지역은 여전히 경보 피로, 편향에 대한 우려, 거버넌스상의 마찰과 같은 과제에 직면해 있지만, 의약품 관리용 AI 시장의 확대에 있어 가장 활발한 상업 환경을 유지하고 있습니다.

유럽은 병원의 디지털화 프로그램과 보다 안전한 의약품 데이터 활용을 위한 규제 추진에 힘입어, 의약품 관리용 AI 시장에서 2위 지역 시장을 차지하고 있습니다. 독일의 ‘Krankenhauszukunftsgesetz(병원 미래법)’은 병원의 디지털화에 43억 유로(47억 달러)를 배정함으로써, 병원 시스템 전반에 걸친 의약품 업무 흐름의 현대화를 위한 명확한 수요 기반을 마련했습니다. BD가 2026년 3월 Sinteco와 제휴를 맺음에 따라, 유럽의 병원을 대상으로 한 첨단 단일 투여용 로봇 기술과 의약품 추적 관리 기능이 추가되었습니다. 이는 자동화 하드웨어와 의약품 데이터의 가시성 간의 연계를 위한 지속적인 투자를 반영한 것입니다. 이 지역의 규제 구조는 규정 준수 비용을 증가시키고 있지만, 한편으로는 검증, 추적성 및 워크플로우의 안전성을 대규모로 문서화할 수 있는 공급업체에게 유리한 조건을 제공합니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 13.09%를 기록하며 성장할 것으로 예상되며, 의약품 관리용 AI 시장에서 가장 빠르게 성장하는 지역 부문이 될 전망입니다. 일본의 약국 디지털화 프로그램은 견고한 운영 기반을 구축했으며, 2025년 5월까지 니혼초세이는 총 763개 약국에 AI를 활용한 복약 이력 작성 서비스를 도입했습니다. 이로 인해 매일 수작업으로 기록을 작성하는 데 소요되는 시간이 줄어들어, 약사는 환자와의 대화에 더 많은 시간을 할애할 수 있게 되었습니다. 중국에서도 임상 현장에서의 실용화가 진행되고 있으며, 산동성 제2인민병원에서는 2025년 시범 운영 기간 동안 투약 오류 방지율이 99.7%에 달했고, 환자 약물 모니터링 대상 비율이 70% 증가했다고 보고되었습니다. 한국과 인도에서는 약국에 AI를 도입할 수 있도록 지원하는 디지털 헬스 인프라가 확대되고 있습니다. 한편, 중동 및 아프리카 및 남미는 일부 국가에서 진행 중인 의료 서비스의 디지털화와 전문 약국에 대한 수요에 힘입어 여전히 초기 단계의 기회로 가득한 시장으로 남아 있습니다. 인프라 및 상호운용성의 제약으로 인해 최첨단 시스템을 제외한 분야에서의 단기적인 보급은 여전히 제한적이지만, 지역별 성장 동향을 고려할 때 아시아태평양은 의약품 관리용 AI 시장의 장기적인 성장 경로에서 계속해서 중심적인 위치를 차지하고 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the aI in medication management market size is expected to grow from USD 2.16 billion in 2025 to USD 2.39 billion in 2026 and is forecast to reach USD 4.11 billion by 2031 at 11.41% CAGR over 2026-2031.

This report is Segmented by Component (Software, Services, Hardware), Deployment Mode (Cloud-Based, and More), Technology (ML and Predictive Models, and More), Application (Decision Support, Adherence, and More), End User (Hospitals, Pharmacies, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global AI In Medication Management Market Trends and Insights

Rising Medication-Error and ADE Burden

The AI in medication management market continues to gain support from the high clinical and financial burden tied to medication errors and adverse drug events. A November 2025 evaluation in Frontiers in Pharmacology reported 1.8 million adverse drug events annually among hospitalized patients in the United States, with 9,000 associated deaths and more than USD 40 billion in related costs. Separate evidence in BMC Medical Informatics and Decision Making showed that unintended ADEs affected 5% of the more than 36 million hospitalized patients in the United States each year, while annual treatment costs exceeded USD 1.5 billion. This burden is pushing providers toward AI systems that can review prescriptions and monitor risk signals continuously, because manual review becomes less reliable as medication volumes rise and care teams face higher alert loads. A 2025 systematic review in Digital Health found that 85% of AI-generated alerts were clinically valid and 43% led to order revisions, which helps explain why hospitals are treating AI review layers as a practical response to persistent medication safety failures.

Polypharmacy and Complex-Regimen Complexity

The AI in medication management market is also being lifted by the growing complexity of regimens used by older adults and patients with multiple chronic conditions. A 2024 review in Healthcare reported polypharmacy prevalence at 30.2% among community-dwelling individuals and 61.7% among hospitalized patients, showing how widely complex medication use is now embedded in care deliver. The same body of evidence showed that each additional medication raised adverse-event risk by 12% to 18%, which increases the value of AI tools that can surface interaction risk and identify candidates for deprescribing. The ABiMed study published in 2025 estimated savings of EUR 273 (USD 298) per patient-year through reduced emergency department visits, which turns medication review from a clinical necessity into a measurable efficiency lever. A 2025 scoping review in Cureus found that AI tools were effective in detecting potentially inappropriate medications and recurring multimorbidity patterns in adults aged 50 and older, which supports steady platform demand as these patient cohorts expand.

Data Privacy and AI Validation Burden

The AI in medication management market still faces a meaningful adoption barrier from data privacy controls, internal governance reviews, and model validation requirements. Regulatory expectations moved higher as the FDA had authorized more than 1,451 AI-enabled medical devices by December 2025, including 295 new authorizations in 2025, while the Predetermined Change Control Plan framework required manufacturers to define future algorithm modifications in advance and monitor model drift after deployment. A national survey of 941 academic physicians published in JMIR AI found that 62% cited bias from unrepresentative training data as a core concern, and 78.9% worried about clinical errors attributable to AI systems. The FDA's January 2026 guidance for certain transparent clinical decision support tools lowered the burden for some categories, but health systems still maintain stricter internal review processes for prescribing and pharmacovigilance use cases where patient risk is higher. This means the AI in medication management market is expanding under tighter compliance discipline, not under a light-touch regulatory setting.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Cloud-Connected Medication Workflows

- Growth of AI-Enabled Medication Adherence Programs

- EHR and Pharmacy-System Interoperability Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 47.32% of the AI in medication management market size in 2025, which made it the largest component within the AI in medication management market. That position reflects the recurring revenue profile of SaaS-based clinical decision support, adherence, and pharmacovigilance tools, which can be updated continuously without waiting for hardware replacement cycles. Epic's direct embedding of AI within medication workflows supports this pattern, because more than 85% of its customer base used at least 1 AI tool and Summit Health reduced prior authorization submission time by 42% through Epic's Penny AI agent. In the AI in medication management industry, that level of workflow embedding matters more than standalone feature breadth, because medication teams are adopting tools that reduce clicks and review time inside systems they already use.

Services are projected to grow at 11.73% CAGR through 2031, which shows that deployment support is expanding alongside software sales instead of being displaced by plug-and-play claims. Health systems are increasingly outsourcing validation, integration engineering, and staff change management because internal clinical AI expertise remains scarce relative to implementation ambition. Hardware remains structurally important because smart dispensing devices, connected adherence sensors, and robotic systems are still the physical control points where medication workflows become executable and measurable. Omnicell's Titan XT and cloud-linked OmniSphere architecture show that hardware value is increasingly tied to data generation and inventory intelligence, not only to cabinet replacement demand.

Cloud-based deployment held 64.73% share in 2025, giving it the leading position in the AI in medication management market. This lead comes from enterprise-wide visibility, lower upfront capital needs, and the ability to centralize medication operations across hospitals, pharmacies, and distribution nodes. BD stated that its AWS-hosted Incada Connected Care Platform processes more than 9.8 million daily medication dispensing transactions from the installed Pyxis base, which shows the data throughput now supporting real-time AI inference at the point of care. Within the AI in medication management market, cloud scale is therefore tied to both workflow unification and data density rather than to hosting preference alone.

On-premises deployment is expected to expand at 11.32% CAGR through 2031, which makes it the fastest-growing mode despite cloud leadership. Hospitals in sovereignty-sensitive jurisdictions are choosing local inference and local data processing for high-risk clinical use cases, especially where encryption, auditability, and national security standards remain strict. Jingzhou Central Hospital's August 2025 AI digital pharmacist deployment used locally deployed databases covering more than 100,000 drug types with medical-grade encrypted data, which shows why on-premises demand is rising in parts of Asia. Hybrid models are therefore gaining ground as a practical middle path, especially where systems want cloud analytics but cannot move full clinical datasets outside local environments.

Geography Analysis

North America held 38.43% of the AI in medication management market share in 2025, which kept it as the largest regional contributor. The region benefits from high EHR penetration, mature value-based reimbursement, and a provider base that is already integrating AI into prescribing, documentation, dispensing, and specialty pharmacy workflows. Utah's January 2026 state-backed autonomous refill program is especially important because it allows AI to participate legally in prescription renewals for 190 chronic-condition medications and tracks refill timeliness, patient safety, adherence outcomes, and cost effects. Oracle's Clinical AI Agent expansion and large-scale distribution and dispensing automation by companies such as McKesson, BD, and Omnicell show that North America is moving from pilots toward embedded operational infrastructure. The region still faces alert fatigue, bias concerns, and governance friction, but it remains the most active commercial environment for scaling the AI in medication management market.

Europe is the second-largest regional market in the AI in medication management market, supported by hospital digitalization programs and a regulatory push toward safer medication data use. Germany's Krankenhauszukunftsgesetz allocated EUR 4.3 billion (USD 4.7 billion) to hospital digitalization, which created a clear demand base for medication workflow modernization across hospital systems. BD's March 2026 partnership with Sinteco added advanced unit-dose robotics and drug traceability capabilities for European hospitals, reflecting continued investment in the connection between automation hardware and medication data visibility. The region's regulatory structure is raising compliance costs, but it also favors vendors that can document validation, traceability, and workflow safety at scale.

Asia-Pacific is forecast to grow at 13.09% CAGR through 2031, making it the fastest-growing regional segment in the AI in medication management market. Japan's pharmacy digitalization programs have created a strong operating base, and by May 2025, Nihon Chouzai had deployed its AI medication history creation service across all 763 pharmacies, cutting daily manual documentation time and giving pharmacists more time for patient interaction. China is also showing measurable clinical use, with Shandong Provincial Second People's Hospital reporting a 99.7% medication error interception rate and a 70% increase in patient pharmaceutical monitoring coverage during 2025 trial operations. South Korea and India are expanding digital health infrastructure that can support pharmacy AI deployment, while Middle East and Africa and South America remain earlier-stage opportunity pools led by healthcare digitalization and specialty pharmacy demand in selected countries. Infrastructure and interoperability constraints still limit near-term penetration outside the most advanced systems, but the regional growth profile keeps Asia-Pacific central to the long-term expansion path of the AI in medication management market.

- AiCure

- Beckton Dickinson

- Epic Systems

- EveryDose

- InsightRX

- Latent Health

- Mckesson

- MDI Health

- MedAware

- Medisafe

- Merative

- Omnicell

- Oracle Health

- OrbitalRX

- PGxAI

- Plenful

- Praventa Health

- Synapse Medicine

- Truentity Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Medication-Error and ADE Burden

- 4.2.2 Polypharmacy and Complex-Regimen Complexity

- 4.2.3 Expansion of Cloud-Connected Medication Workflows

- 4.2.4 Growth of AI-Enabled Medication Adherence Programs

- 4.2.5 Drug-Shortage Orchestration and Substitution Intelligence

- 4.2.6 Value-Based Pharmacy Economics and Quality Incentives

- 4.3 Market Restraints

- 4.3.1 Data Privacy and AI Validation Burden

- 4.3.2 EHR and Pharmacy-System Interoperability Gaps

- 4.3.3 Alert Fatigue and Low Clinician Trust in AI Outputs

- 4.3.4 Liability and Auditability Constraints in High-Risk Workflows

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.3 Hardware

- 5.1.3.1 Smart Dispensing and Verification Devices

- 5.1.3.2 Connected Adherence Sensors and Devices

- 5.1.3.3 Robotic Dispensing and Packaging Systems

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 Hybrid

- 5.2.3 On-Premises

- 5.3 By Technology

- 5.3.1 Machine Learning and Predictive Models

- 5.3.2 Natural Language Processing

- 5.3.3 Computer Vision

- 5.3.4 Generative AI Assistants

- 5.3.5 Other Technologies (Graph and Rules-Augmented Reasoning, etc.)

- 5.4 By Application

- 5.4.1 Medication Decision Support and Interaction Checking

- 5.4.2 Medication Adherence and Engagement

- 5.4.3 Prescription and Order Verification

- 5.4.4 Medication Reconciliation

- 5.4.5 Inventory and Shortage Optimization

- 5.4.6 Precision Dosing and Therapy Optimization

- 5.4.7 ADE Surveillance and Pharmacovigilance

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Pharmacies

- 5.5.3 Payers and PBMs

- 5.5.4 Pharmaceutical and Life Sciences Companies

- 5.5.5 Home Care and Virtual Care Providers

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AiCure

- 6.3.2 Becton, Dickinson and Company

- 6.3.3 Epic Systems Corporation

- 6.3.4 EveryDose

- 6.3.5 InsightRX

- 6.3.6 Latent Health

- 6.3.7 McKesson Corporation

- 6.3.8 MDI Health

- 6.3.9 MedAware

- 6.3.10 Medisafe

- 6.3.11 Merative

- 6.3.12 Omnicell

- 6.3.13 Oracle Health

- 6.3.14 OrbitalRX

- 6.3.15 PGxAI

- 6.3.16 Plenful

- 6.3.17 Praventa Health

- 6.3.18 Synapse Medicine

- 6.3.19 Truentity Health

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment