|

시장보고서

상품코드

2064397

북미의 셰일가스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)North America Shale Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

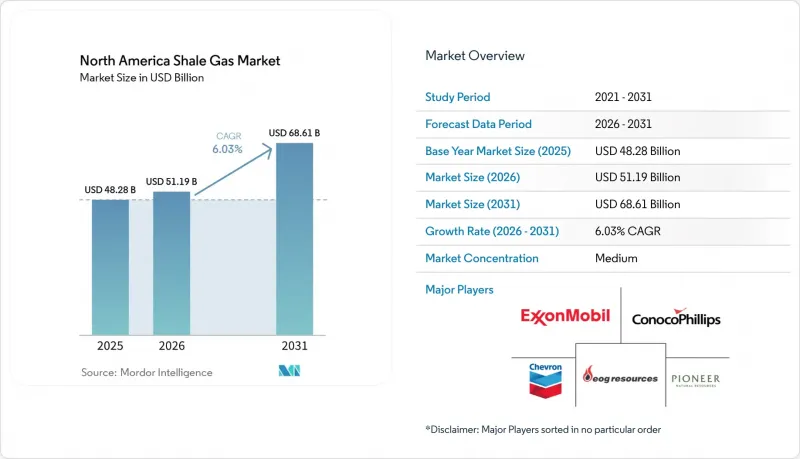

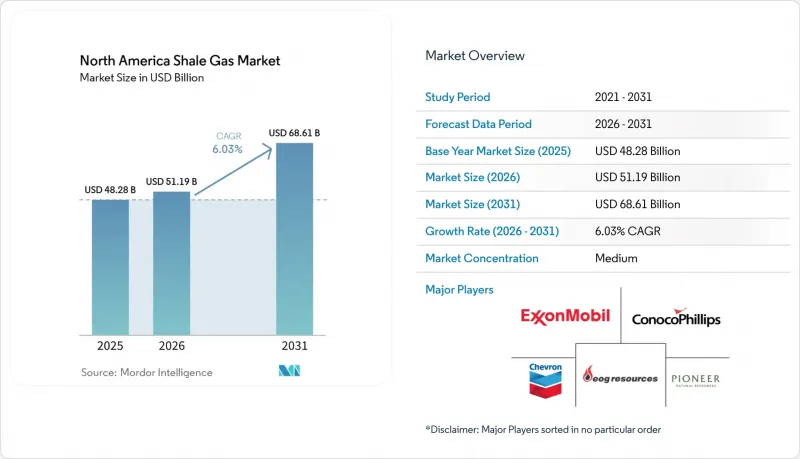

Mordor Intelligence에 의하면, 북미 셰일가스 시장 규모는 2025년 482억 8,000만 달러에서 2026년에는 511억 9,000만 달러로 확대되어 2031년까지 686억 1,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 6.03%로 성장할 전망입니다.

본 보고서는 탄화수소의 유형(셰일가스, 셰일오일), 채굴 기술(수평 시추만, 수압 파쇄만, 수평 시추와 수압 파쇄의 병용 등), 용도(발전, 산업·석유화학 원료, 주거·상업용 난방, 운송), 지역(미국, 캐나다, 멕시코)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미 셰일가스 시장 동향과 인사이트

수평 시추 및 수압 파쇄 기술의 보급

퍼미안 분지 및 마르셀러스층의 수평 시추공 길이는 현재 일반적으로 10,000피트를 초과하며, 시추공당 파쇄 단계 수는 60-80개에 달할 전망입니다. 셰브론의 트리플 플랙 패드 설계 덕분에 2025년에는 3개의 유정이 동시에 완공되었으며, 유정당 비용은 600만 달러 미만으로 떨어졌습니다. 할리버튼의 폐쇄 루프식 압력 제어 파쇄 기술은 프로판트 배치 효율을 최대 20% 향상시키고, 파쇄 반감기를 연장합니다. 전기 구동 차량을 도입함으로써 시추 현장에서 디젤 연료가 더 이상 필요하지 않게 되었으며, 마르셀러스층에서 진행된 시범 사업에서는 프랙처링에 따른 배출량을 60% 감축했습니다. 이러한 발전으로 인해 기술적으로 회수 가능한 자원량이 증가함에 따라, 북미 시장의 셰일가스 생산은 6%의 성장 궤도를 유지할 것이며, 사업자들은 기존 유정을 재자극하여 추가적인 회수가 가능해질 것입니다.

연방 및 주 차원의 유리한 세제 혜택

USC 45I는 한계 유정의 생산량에 대해 석유 환산 배럴당 3달러를 지급함으로써, 미국 내 약 30만 개의 저생산 유정에 혜택을 주고 있습니다. USC 45K 비전통적 연료 세액 공제는 석유 환산 배럴당 6.40달러를 지급하여 애팔래치아 지역의 데본기 셰일층 재개발을 지원하고 있습니다. 펜실베이니아주의 임팩트 수수료는 2024년에 지방 자치 단체에 2억 6,200만 달러를 환원함으로써, 시추 활동 지속에 대한 지역 사회의 지지를 이끌어 냈습니다. 텍사스주의 고비용 가스 면제 조치는 심부 수평 유정에 대한 자원세를 면제하고, 생산 개시 후 첫 10년 동안 실효 세율을 7.5%에서 거의 0%로 인하합니다. 이러한 우대 조치는 단기 주기의 시추를 가속화하고, 독립 기업들을 단기적인 가격 변동으로부터 보호하며, 북미 시장에서의 셰일가스 생산 확대를 뒷받침하고 있습니다.

변동하는 천연가스 가격이 투자 결정에 영향을 미침

헨리 허브 선물 가격은 2024년 2월 1MMBtu당 1.57달러에서 2025년 1월 겨울 폭풍 ‘파른’이 닥쳤을 때 6.80달러까지 등락하며, 333%에 달하는 큰 변동폭으로 인해 자본 예산 수립에 대한 신뢰를 떨어뜨렸습니다. 2027년부터 2028년까지의 선물 곡선은 평균 3.20달러 수준을 기록하고 있으며, 헤인즈빌 지역에서 현금 흐름을 흑자로 전환하기 위해 필요한 3달러의 기준치를 간신히 상회하는 수준에 머물러 있습니다. 서부 텍사스 지역의 파이프라인 혼잡이 심화되는 가운데, 와하 허브의 할인 폭은 헨리 허브 대비 2달러까지 확대되었습니다. TTF 및 JKM과의 상관관계로 인해 북미 생산자들은 지정학적 충격에 노출되어 있으며, 이로 인해 2026년 가스 시추 예산의 15-20%가 연기되는 사태가 발생하고 있습니다. 따라서 가격 변동성은 북미 시장의 셰일가스 생산 예상 성장률을 1퍼센트포인트 이상 끌어내리는 요인이 되고 있습니다.

부문별 분석

2025년 기준으로, 셰일가스는 북미 시장 규모에서 셰일가스 생산량의 77.5%를 차지했으나, 셰일오일은 연평균 성장률(CAGR) 6.6%를 기록하며 더 빠르게 성장했습니다. 퍼미안 분지에서는 원유 생산량이 하루 660만 배럴, 가스 생산량이 하루 22.2억 입방피트에 달했으며, 이를 통해 사업자는 원유 사업을 통해 가스 사업의 손실을 보전할 수 있게 되었습니다.

델라웨어 서브분지와 같이 액상 탄화수소가 풍부한 광구에서는 가스 대 원유 비율이 배럴당 약 3,500입방피트에 달하며, 헨리 허브 가격이 MMBtu당 3달러 미만으로 유지되는 경우에도 현금 흐름을 뒷받침하고 있습니다. 그 결과, 대형 독립 기업들은 드라이 가스가 많은 애팔래치아 지역에서 원유 중심의 분지로 시추 장비를 계속 재배치하고 있으며, 이러한 동향은 성장의 중심을 셰일 오일로 전환시키고 있음과 동시에, 이에 수반되는 생산량을 바탕으로 북미 셰일가스 생산 시장의 회복력을 유지하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the north america shale gas market size is expected to increase from USD 48.28 billion in 2025 to USD 51.19 billion in 2026 and reach USD 68.61 billion by 2031, growing at a CAGR of 6.03% over 2026-2031.

This report is Segmented by Hydrocarbon Type (Shale Gas, Shale Oil), Extraction Technology (Horizontal Drilling Only, Hydraulic Fracturing Only, Combined Horizontal and More), Application (Power Generation, Industrial and Petrochemical Feedstock, Residential and Commercial Heating, Transportation), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Shale Gas Market Trends and Insights

Proliferation of Horizontal Drilling & Hydraulic Fracturing

Lateral lengths in the Permian and Marcellus now commonly exceed 10,000 feet, while stage counts reach 60-80 per well. Chevron's triple-frac pad design completed three wells simultaneously in 2025 and cut per-well costs below USD 6 million. Halliburton's closed-loop pressure-managed fracturing lifts proppant placement efficiency by up to 20% and prolongs fracture half-life. Electric fleets eliminate diesel at the wellsite and have lowered fracturing emissions by 60% in Marcellus field pilots. These advances enlarge technically recoverable resources, keep the shale gas production in North America market on its 6% growth track, and allow operators to re-stimulate legacy wells for incremental recovery.

Favorable Federal and State-Level Tax Incentives

USC 45I grants USD 3 per barrel-of-oil-equivalent for marginal-well output, benefiting roughly 300,000 stripper wells across the United States . The USC 45K nonconventional fuels credit pays USD 6.40 per barrel-equivalent and supports Devonian shale redevelopment in Appalachia. Pennsylvania's Impact Fee returned USD 262 million to local governments in 2024 and nurtured community backing for continued drilling. Texas' high-cost gas exemption removes severance taxes for deep horizontal wells, shrinking the effective levy from 7.5% to near zero during the first decade of production. These incentives accelerate short-cycle drilling and insulate independents from near-term price swings, supporting expansion of the shale gas production in North America market.

Volatile Natural Gas Prices Impacting Investment Decisions

Henry Hub futures ranged from USD 1.57 per MMBtu in February 2024 to USD 6.80 during Winter Storm Fern in January 2025, a 333% swing that undercut capital budgeting confidence. Forward curves for 2027-2028 average near USD 3.20, barely above the USD 3.00 threshold needed for positive cash flow in the Haynesville. Waha hub discounts widened to USD 2.00 below Henry Hub as pipeline congestion intensified in West Texas. Correlation with TTF and JKM exposes North American producers to geopolitical shocks, prompting a 15-20% deferral of 2026 gas-directed drilling budgets. Price volatility therefore subtracts over one percentage point from forecast growth in the shale gas production in North America market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Domestic Demand for Low-Cost Petrochemical Feedstock

- Increasing LNG Bunkering Demand from Great Lakes Fleet (Post IMO 2030)

- Stringent Methane Emission Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Shale gas held 77.5% share of the shale gas production in North America market size in 2025, yet shale oil grew faster at a 6.6% CAGR. Permian output delivered 6.6 million bpd of crude with a 22.2 Bcf/d gas stream, enabling operators to cross-subsidize gas economics.

Liquids-heavy acreage such as the Delaware sub-basin posts gas-to-oil ratios near 3,500 cf/bbl, supporting cash flows even when Henry Hub prices linger below USD 3 per MMBtu. Consequently, large independents continue reallocating rigs from dry-gas Appalachia to oil-weighted basins, a trend that tilts growth toward shale oil yet leaves the shale gas production in North America market resilient on the back of associated volumes.

List of Companies Covered in this Report:

- Exxon Mobil Corporation

- Chevron Corporation

- ConocoPhillips

- EOG Resources Inc.

- Pioneer Natural Resources Co.

- BP plc

- Royal Dutch Shell plc

- TotalEnergies SE

- Occidental Petroleum Corporation

- Murphy Oil Corporation

- Equinor ASA

- Repsol SA

- Chesapeake Energy Corporation

- Range Resources Corporation

- Devon Energy Corporation

- Coterra Energy Inc.

- EQT Corporation

- Ovintiv Inc.

- Southwestern Energy Company

- Antero Resources Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of horizontal drilling & hydraulic fracturing

- 4.2.2 Favorable federal and state-level tax incentives

- 4.2.3 Growing domestic demand for low-cost petrochemical feedstock

- 4.2.4 Increasing LNG bunkering demand from Great Lakes shipping fleet (post IMO 2030)

- 4.2.5 AI-driven predictive maintenance reducing non-productive time

- 4.3 Market Restraints

- 4.3.1 Volatile natural gas prices impacting investment decisions

- 4.3.2 Stringent methane emission regulations

- 4.3.3 Municipal ground-water conservation opposition

- 4.3.4 Limited availability of specialized proppants

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Hydrocarbon Type

- 5.1.1 Shale Gas

- 5.1.2 Shale Oil

- 5.2 By Extraction Technology

- 5.2.1 Horizontal Drilling Only

- 5.2.2 Hydraulic Fracturing Only

- 5.2.3 Combined Horizontal and Hydraulic Fracturing

- 5.3 By Application

- 5.3.1 Power Generation

- 5.3.2 Industrial and Petrochemical Feedstock

- 5.3.3 Residential and Commercial Heating

- 5.3.4 Transportation (LNG and CNG)

- 5.4 By Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Exxon Mobil Corporation

- 6.4.2 Chevron Corporation

- 6.4.3 ConocoPhillips

- 6.4.4 EOG Resources Inc.

- 6.4.5 Pioneer Natural Resources Co.

- 6.4.6 BP plc

- 6.4.7 Royal Dutch Shell plc

- 6.4.8 TotalEnergies SE

- 6.4.9 Occidental Petroleum Corporation

- 6.4.10 Murphy Oil Corporation

- 6.4.11 Equinor ASA

- 6.4.12 Repsol SA

- 6.4.13 Chesapeake Energy Corporation

- 6.4.14 Range Resources Corporation

- 6.4.15 Devon Energy Corporation

- 6.4.16 Coterra Energy Inc.

- 6.4.17 EQT Corporation

- 6.4.18 Ovintiv Inc.

- 6.4.19 Southwestern Energy Company

- 6.4.20 Antero Resources Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment