|

시장보고서

상품코드

2064409

동아시아의 재생에너지 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)East Asia Renewable Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

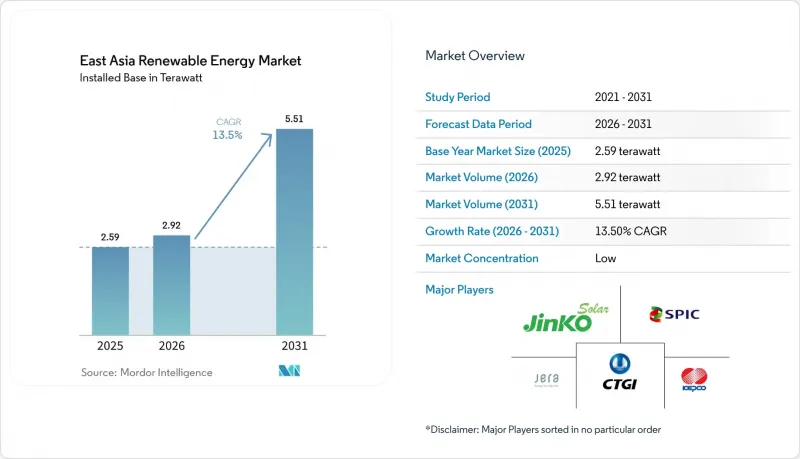

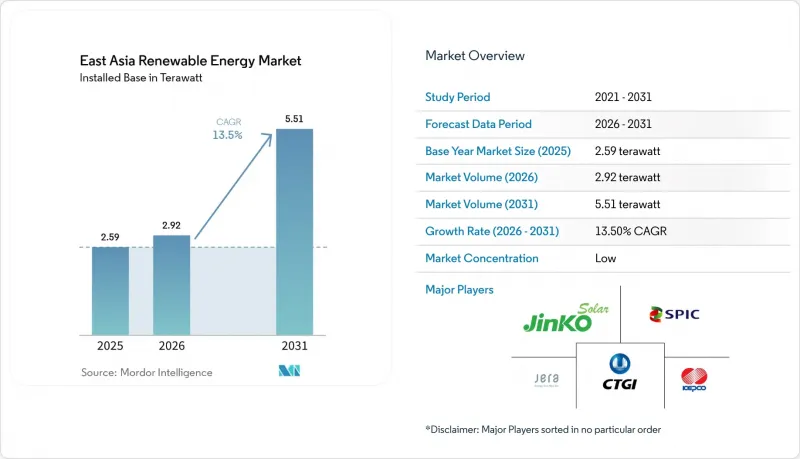

Mordor Intelligence에 의하면, 동아시아 재생에너지 시장 규모(설치 기반)는 2025년에 2.59 테라와트, 2026년에 2.92 테라와트가 되어, 2031년까지 5.51 테라와트에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 13.5%로 성장할 전망입니다.

본 보고서는 기술별(태양광, 풍력, 수력, 바이오에너지, 지열, 해양 에너지), 최종 사용자별(유틸리티, 상업 및 산업, 주택), 지역별(중국, 일본, 한국, 대만, 기타 동아시아)로 분류되어 있습니다. 시장 전망은 용량(TW) 단위로 표시되어 있습니다.

동아시아 재생에너지 시장 동향과 인사이트

정부의 탈탄소화 의무와 보조금 제도

현재 지역 정책 체계에는 경제 계획에 기가와트 규모의 목표가 포함되어 있습니다. 중국의 제15차 5개년 계획에서는 성(省)의 GDP 지표를 재생에너지 도입 실적과 연계하여, 발전 용량 증가에 대한 정치적 책임을 확보하고 있습니다. 2024년에 수립된 일본의 제7차 에너지 기본계획에서는 2040년 재생에너지 전력 목표를 50%로 상향 조정하고, 도매 가격에 따라 변동하는 고정가격임베디드제도(FIT)를 경매 방식으로 전환했습니다. 이를 통해 재정적 위험을 줄이면서 개발사의 현금 흐름을 보호하고 있습니다. 한국의 ‘RE3020’에 따르면, 2030년까지 공공기관이 전력의 35%를 재생에너지로 조달해야 할 의무가 있으며, 이에 따라 2025년에는 이미 18건의 대형 태양광 발전 입찰이 실시되었습니다. 대만은 2030년까지 280억 달러 규모의 해상 풍력 및 청정 수소 기금을 법제화했으며, 에너지국이 분기별로 이를 감독하고 있습니다. 이러한 프로그램들을 종합해 보면, 지역별 탄소 가격의 하한선은 톤당 45달러 수준이 될 것이며, 이로 인해 향후 10년이 끝나기 전에 배출 감축 조치가 취해지지 않은 석탄 발전은 경쟁력을 잃게 될 것입니다.

태양광 발전 및 풍력 발전의 LCOE의 급격한 하락

아시아태평양 지역의 태양광 및 풍력 발전의 균등화 발전 비용(LCOE)은 2024년에 16% 하락했습니다. 이는 폴리실리콘공급 과잉, N형 셀의 효율이 25%를 넘어섰으며, 양면 수광형 모듈의 채택률이 70%에 육박함에 따라 모듈 가격이 1와트당 0.09달러까지 하락했기 때문입니다. 2024년 중국 대형 태양광 발전의 평균 발전 비용은 1MWh당 27달러로, 천연가스보다 35% 저렴해졌습니다. 내몽골 자치구의 풍력 발전 입찰에서 로터 직경 180미터의 6.5MW급 터빈을 도입함에 따라 2025년 낙찰 가격은 1MWh당 31달러로 결정되었습니다. 해상 풍력은 여전히 비용이 높지만, 전라남도에서는 두산 에너빌리티(Doosan Enerbility)의 15MW급 나셀이 양산 규모에 도달함에 따라, 2028년까지 1MWh당 55달러를 목표로 하는 지역 밀착형 공급망이 구축되고 있습니다. 지속적인 비용 절감에 힘입어 동아시아 재생에너지 시장의 잠재 규모는 확대되고 있으며, 저녁 시간대 피크 수요 시기의 프리미엄을 확보하기 위한 하이브리드 에너지 저장 시스템의 도입이 촉진되고 있습니다.

송전망의 혼잡 및 출력 억제 위험

2025년에 180GW 규모의 태양광 발전 설비가 신설되었으나, 송전망 확장이 이를 따라가지 못해 2026년 1월부터 2월에 걸쳐 중국의 태양광 발전 출력 억제율은 9.2%에 달했습니다. 티베트에서는 400MW의 부하에 비해 3GW 용량의 송전선로 한 가닥밖에 이용할 수 없기 때문에 낮 시간대 태양광 발전량의 17%가 버려졌습니다. 국가전망은 2027년까지 5개의 새로운 초고압 회랑 건설에 6,500억 위안(인민폐)을 배정했으나, 일반적인 건설 기간은 최대 4년에 달할 전망입니다. 홋카이도에서는 HVDC 도입 후 출력 억제 현상이 감소하고 있으며, 대상 지역을 선별하여 송전망을 정비함으로써 병목 현상을 해소할 수 있음이 밝혀졌으나, 한국에서는 여전히 축전 설비가 설치되지 않은 경우 변동형 재생에너지의 비율을 25%로 제한하고 있습니다. 지속적인 송전망 과부하는 단기적인 신규 도입을 억제하여 동아시아 재생에너지 시장의 성장 여지를 좁히고 있습니다.

부문별 분석

2025년 기준으로 태양광 발전은 설치 용량의 53.1%를 차지했습니다. 지속적인 비용 절감, 사막의 메가 베이스, 그리고 지붕 설치 의무화로 인해 그 우위는 확고해졌지만, 폴리실리콘 감사로 인해 공급망은 양극화되고 있습니다. 2025년 해양 에너지의 기반은 300MW 미만으로 낮은 수준이지만 연평균 성장률(CAGR) 43.4%를 뒷받침하고 있으며, 한국의 시파 댐과 일본의 프로테우스 터빈이 상용화 준비를 마쳤음을 보여줍니다.

터빈의 대형화로 인해 풍력 발전의 기여도가 높아지고 있습니다. 16MW급 플랫폼은 현재 연간 80GWh를 발전하고 있으며, 2020년 발전량은 2배로 증가했습니다. 중국의 3.6GW급 펑닝(豊寧) 발전소와 같은 양수 발전은 변동하는 발전량을 안정화시키는 한편, 규슈 지역의 지열 발전 증설은 일본의 에너지 구성을 다각화하고 있습니다. 태양광 발전 비용이 와트당 0.10달러 아래로 떨어진 가운데, 집광형 태양열 발전과 바이오에너지는 여전히 틈새 시장에 머물러 있습니다. 해양 기술 시범 사업이 성공한다면, 동아시아 재생에너지 시장의 개척 영역은 기존의 자원 범위를 넘어 확대될 가능성이 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the east asia renewable energy market size in terms of installed base is projected to be 2.59 terawatt in 2025, 2.92 terawatt in 2026, and reach 5.51 terawatt by 2031, growing at a CAGR of 13.5% from 2026 to 2031.

This report is Segmented by Technology (Solar Energy, Wind Energy, Hydropower, Bioenergy, Geothermal, Ocean Energy), End-User (Utilities, Commercial and Industrial, Residential), and Geography (China, Japan, South Korea, Taiwan, Rest of East Asia). The Market Forecasts are Provided in Terms of Volume (TW).

East Asia Renewable Energy Market Trends and Insights

Government Decarbonization Mandates & Subsidy Mechanisms

Regional policy frameworks now embed gigawatt-scale targets in economic planning. China's 15th Five-Year Plan ties provincial GDP metrics to renewable roll-outs, ensuring political accountability for capacity gains. Japan's seventh Strategic Energy Plan finalized in 2024 raised the 2040 renewable electricity goal to 50% and switched to feed-in-premium auctions that flex with wholesale prices, reducing fiscal exposure while safeguarding developer cash flows. South Korea's RE3020 requires public institutions to source 35% of power from renewables by 2030, already catalyzing 18 utility-scale solar tenders in 2025. Taiwan legislated a USD 28 billion offshore wind and green hydrogen fund through 2030, monitored quarterly by the Bureau of Energy. Together these programs imply a regional carbon price floor near USD 45 per ton, rendering unabated coal uncompetitive before the decade's end.

Rapid LCOE Decline for Solar PV & Wind

Asia-Pacific solar and wind levelized costs fell 16% in 2024 as polysilicon oversupply, N-type cell efficiencies above 25%, and bifacial adoption near 70% drove module prices to USD 0.09 per watt. China's utility-scale PV averaged USD 27 per MWh in 2024, undercutting gas by 35%. Inner Mongolia wind auctions cleared at USD 31 per MWh in 2025 thanks to 6.5 MW turbines with 180-meter rotors. Offshore wind remains pricier, yet localized supply chains in Jeollanam-do aim for USD 55 per MWh by 2028 as Doosan Enerbility's 15 MW nacelles reach volume scale. Continuous cost compression widens the East Asia renewable energy market addressable base and encourages hybrid storage pairings that secure evening-peak premiums.

Grid Congestion & Curtailment Risk

Solar curtailment in China hit 9.2% during Jan-Feb 2026 as 180 GW of 2025 additions outpaced transmission growth. Tibet dumped 17% of midday solar because a lone 3 GW line serves a 400 MW load. State Grid has earmarked CNY 650 billion for five new ultra-high-voltage corridors through 2027, yet typical build times run up to four years. Hokkaido's curtailment drop post-HVDC shows targeted links can resolve bottlenecks, but Korea still caps variable renewable share at 25% without co-located storage. Persistent congestion restrains near-term additions and trims the East Asia renewable energy market growth runway.

Other drivers and restraints analyzed in the detailed report include:

- Corporate-PPA Boom from Data-Center & Heavy-Industry Buyers

- Cross-Border HVDC Super-Grid Build-Out

- Land-Use & Permitting Delays for Onshore Assets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solar Energy commanded 53.1% of installed capacity in 2025. Continuous cost declines, desert mega-bases, and rooftop mandates cement its primacy, though polysilicon audits bifurcate supply chains. Ocean Energy's low 2025 base under 300 MW underpins its 43.4% CAGR, with South Korea's Sihwa barrage and Japan's Proteus turbine signaling commercial readiness.

Turbine scaling lifts wind contributions; 16 MW platforms now generate 80 GWh annually, doubling 2020 units. Pumped-storage hydro like China's 3.6 GW Fengning plant stabilizes variable output, while geothermal additions in Kyushu diversify Japan's mix. Concentrating solar and bioenergy stay niche as PV costs plunge below USD 0.10 per watt. Ocean technology pilot success could expand the East Asia renewable energy market frontier beyond traditional resources.

List of Companies Covered in this Report:

- State Power Investment Corporation (SPIC)

- China Three Gorges Corp (CTG)

- JinkoSolar Holding Co Ltd

- LONGi Green Energy Technology Co Ltd

- Xinjiang Goldwind Science & Technology Co Ltd

- Trina Solar Ltd

- JA Solar Technology Co Ltd

- Siemens Gamesa Renewable Energy SA

- Vestas Wind Systems A/S

- Eurus Energy Holdings Corp

- Korea Electric Power Corp (KEPCO)

- JERA Co Inc

- Mitsubishi Corp (Renewables)

- Orsted A/S (Taiwan JV)

- CGN New Energy Holdings Co Ltd

- Shenergy Group Co Ltd

- Tokyo Electric Power Renewable Power Co

- Hanwha Q-Cells Co Ltd

- SK E&S Co Ltd

- Orsted Japan KK

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government decarbonisation mandates & subsidy mechanisms

- 4.2.2 Rapid LCOE decline for solar PV & wind

- 4.2.3 Corporate-PPA boom from data-centre & heavy-industry buyers

- 4.2.4 Cross-border HVDC "super-grid" build-out (CN-JP-KR)

- 4.2.5 Localised offshore-wind manufacturing clusters (Fujian, Jeollanam)

- 4.2.6 AI-driven generation forecasting raising grid-penetration ceilings

- 4.3 Market Restraints

- 4.3.1 Grid congestion & curtailment risk

- 4.3.2 Land-use & permitting delays for onshore assets

- 4.3.3 Polysilicon price-spikes from Xinjiang audit squeeze

- 4.3.4 Typhoon-zone insurance premia for offshore wind farms

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Solar Energy (PV and CSP)

- 5.1.2 Wind Energy (Onshore and Offshore)

- 5.1.3 Hydropower (Small, Large, PSH)

- 5.1.4 Bioenergy

- 5.1.5 Geothermal

- 5.1.6 Ocean Energy (Tidal and Wave)

- 5.2 By End-User

- 5.2.1 Utilities

- 5.2.2 Commercial and Industrial

- 5.2.3 Residential

- 5.3 By Geography

- 5.3.1 China

- 5.3.2 Japan

- 5.3.3 South Korea

- 5.3.4 Taiwan

- 5.3.5 Rest of East Asia (Mongolia, Hong Kong, Macau)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 State Power Investment Corporation (SPIC)

- 6.4.2 China Three Gorges Corp (CTG)

- 6.4.3 JinkoSolar Holding Co Ltd

- 6.4.4 LONGi Green Energy Technology Co Ltd

- 6.4.5 Xinjiang Goldwind Science & Technology Co Ltd

- 6.4.6 Trina Solar Ltd

- 6.4.7 JA Solar Technology Co Ltd

- 6.4.8 Siemens Gamesa Renewable Energy SA

- 6.4.9 Vestas Wind Systems A/S

- 6.4.10 Eurus Energy Holdings Corp

- 6.4.11 Korea Electric Power Corp (KEPCO)

- 6.4.12 JERA Co Inc

- 6.4.13 Mitsubishi Corp (Renewables)

- 6.4.14 Orsted A/S (Taiwan JV)

- 6.4.15 CGN New Energy Holdings Co Ltd

- 6.4.16 Shenergy Group Co Ltd

- 6.4.17 Tokyo Electric Power Renewable Power Co

- 6.4.18 Hanwha Q-Cells Co Ltd

- 6.4.19 SK E&S Co Ltd

- 6.4.20 Orsted Japan KK

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment