|

시장보고서

상품코드

2064412

남미의 석유 및 가스 드론 서비스 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)South America Oil And Gas Drone Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

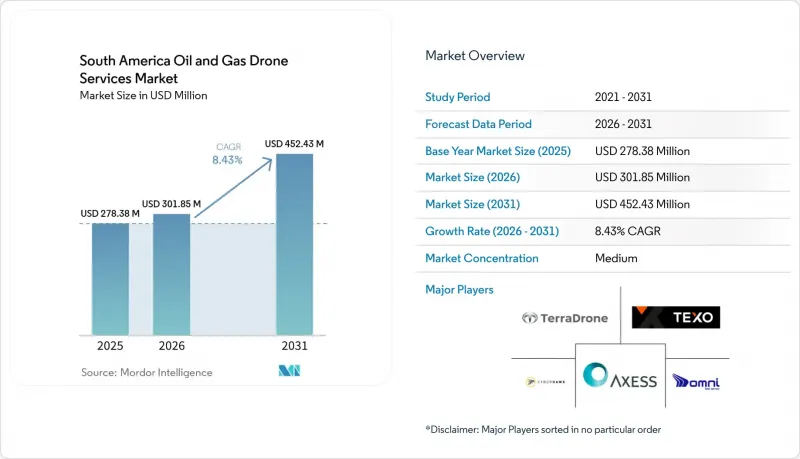

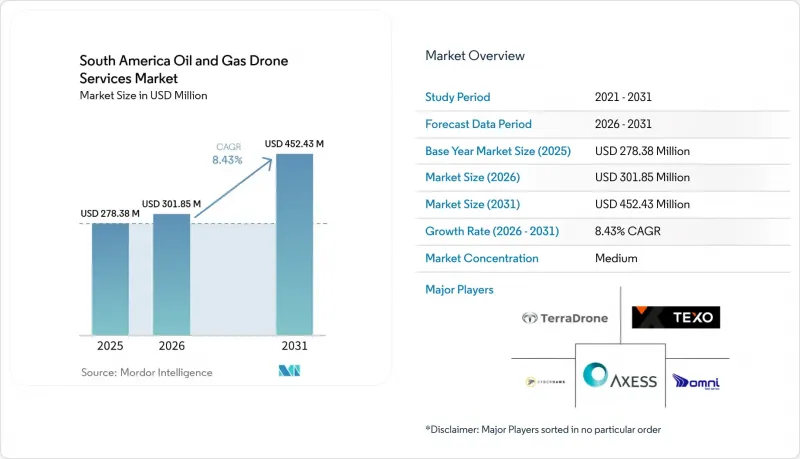

Mordor Intelligence에 의하면, 남미 석유 및 가스 드론 서비스 시장 규모는 2025년 2억 7,838만 달러, 2026년 3억 185만 달러에서 2031년까지 4억 5,243만 달러로 확대되어 2026년부터 2031년까지 CAGR 8.43%를 나타낼 것으로 예측됩니다.

본 보고서는 서비스 유형(점검·감시, 측량·매핑, 긴급 대응·환경 모니터링, 물류 지원), 용도(파이프라인 모니터링·건전성 평가 등), 드론 유형(멀티로터 등), 지역(브라질, 아르헨티나, 가이아나, 콜롬비아 및 기타 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

남미 석유 및 가스 드론 서비스 시장 동향 및 인사이트

비용과 안전성의 경제성이 종합적인 가치 제안을 재구축하고 있습니다.

남미의 석유 및 가스 분야 드론 서비스 시장에서는 사업자들이 드론을 활용한 점검을 밀폐된 공간 진입, 로프 액세스 및 기타 노동 집약적인 방식에 대한 대체 수단으로, 더 안전하고 재현성이 높은 선택지로 인식하고 있어 도입이 가속화되고 있습니다. 이러한 변화는 특히 브라질에서 두드러졌는데, Transpetro사는 드론을 활용한 밀폐 공간 조사로 전환한 후, 유조선 1척당 점검 주기당 최대 100만 레알(17만 1,000달러)의 비용 절감을 달성한 한편, 점검 기간은 1주일에서 3-4일로 단축되었습니다. 점검이 일상적인 운영 예산에 포함되면 조달이 안정되고 계약 갱신의 정당화도 용이해지므로, 이러한 상업적 효과는 중요합니다. 남미의 석유 및 가스 드론 서비스 시장은 공식적인 조사 환경에서 드론이 생성한 검사 데이터에 대한 신뢰도가 높아지고 있는 점에 힘입고 있습니다. 이로 인해, 이전에는 드론 활용을 핵심 프로세스가 아닌 시험적인 활동으로 간주했던 사업자들의 저항이 완화되고 있습니다. 현장 피폭 위험 감소, 가동 중단 시간 단축, 그리고 명확한 문서화라는 이러한 요소들이 결합되어 드론 서비스가 장기 유지보수 프로그램에 포함되고 있습니다.

파이프라인 및 핵심 자산의 건전성 요건이 장기 계약을 주도

남미의 석유 및 가스 드론 서비스 시장은 정기적인 육안 및 열화상 검사가 필요한 이 지역의 방대한 파이프라인, 터미널, 저장 시스템 및 해양 수송 자산 네트워크 덕분에 계속해서 혜택을 보고 있습니다. 자산의 고장은 이제 단순한 수리를 훨씬 뛰어넘는 운영상, 재무상, 그리고 평판상의 영향을 수반하기 때문에 사업자들은 문서화된 점검 이력을 더욱 중요하게 여기고 있습니다. 이는 기상 조건, 지형, 접근 제한으로 인해 수작업 검사가 느리고 일관성이 떨어지는 외딴 지역에서 특히 중요합니다. 이러한 상황에서 드론 서비스는 일회성 현장 작업이 아닌, 완전성 관리 프로그램의 일부로 자리 잡고 있으며, 이로 인해 계약 기간이 장기화되고 반복 업무가 더욱 빈번해지고 있습니다. 따라서 남미의 석유 및 가스 분야 드론 서비스 시장은 자산 점검 수요뿐만 아니라, 분산된 인프라 전반에 걸쳐 감사 가능한 점검 기록을 유지해야 할 필요성에서도 혜택을 보고 있습니다.

단편화된 BVLOS(시야 외 비행) 체계와 항공 승인 절차의 부담

남미의 석유 및 가스 분야 드론 서비스 시장은 사업자들이 국경을 넘어 각국의 개별 드론 허가 제도에 대응해야 하기 때문에 여전히 대규모 확장에 있어 큰 과제에 직면해 있습니다. 브라질의 ANAC는 2025년 6월에 ‘공개 협의 제09호’를 시작하여 RBAC 100을 제안했습니다. 이는 규제를 ‘개방’, ‘특정’, ‘인증’ 범주로 구성된 위험 기반 시스템으로 전환하는 것이며, SORA 등의 위험 평가 기법과 연계된 ‘특정’ 범주의 운영 체계를 도입하는 것입니다. 아르헨티나도 결의안 제550/2025호를 발표하고, RAAC 100, 101 및 102로의 전환을 추진하며, 기존의 등급별 시스템을 ICAO 및 라틴아메리카 규정에 부합하는 ‘오픈’, ‘특정’, ‘인증’ 범주로 대체했습니다. 이러한 진전에도 불구하고, ‘특정’ 범주에 속하는 BVLOS 임무에는 여전히 운항 승인 및 위험 완화 조치가 필요하며, 이로 인해 리드타임이 길어지고 국경을 넘는 통로에서의 작업에 드는 비용이 증가하고 있습니다. 따라서 남미의 석유 및 가스 분야 드론 서비스 시장에서는 현지 법인을 보유하고, 현지 규정 준수 대응 경험이 있으며, 국가별 승인 지연을 감당할 수 있는 능력을 갖춘 기업이 유리한 입장에 서게 됩니다.

부문별 분석

2025년, 검사 및 감시 부문은 41.8%의 점유율을 유지하며 남미 석유 및 가스 드론 서비스 시장에서 가장 큰 서비스 유형으로서의 입지를 지켰습니다. 이 부문이 주도적인 위치를 차지하고 있는 이유는 파이프라인, 탱크, 플레어 스택, 해양 구조물 및 기타 안전성이 중요한 자산에 대한 빈번한 점검이라는 해당 지역의 가장 시급한 요구를 충족시키고 있기 때문입니다. 이 분야의 입지는 브라질에서 가장 확고하며, 브라질에서는 해양 유지보수 프로그램이나 유조선 검사에서 드론을 활용한 육안 점검 및 밀폐 공간 진입이 이미 일상적으로 활용되고 있습니다. 또한, 드론을 활용한 초음파 두께 측정 워크플로가 공식적으로 채택된 점도 이 서비스 라인을 강화하고 있습니다. 이를 통해 드론에 의한 결과물이 공인된 검사 및 측량 환경에서 더욱 실용적으로 활용될 수 있기 때문입니다.

측량 및 매핑 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 9.8%로 확대될 것으로 예상되며, 남미의 석유 및 가스 드론 서비스 업계에서 가장 빠르게 성장하는 서비스 부문이 될 것입니다. 이러한 성장은 신흥 및 확장 중인 석유 및 가스 프로젝트 전반에 걸친 신규 노선 조사, 건설 전 계획, 부지 측량 및 디지털 트윈 개발을 통해 뒷받침되고 있습니다. 또한, ‘긴급 대응 및 환경 모니터링’ 역시 배기가스 규제나 누출 추적 가능성이 때때로 실시되는 현장 훈련이 아닌, 보다 일반적인 계약상 요건이 됨에 따라 그 중요성이 커지고 있습니다. 남미의 석유 및 가스 드론 서비스 업계에서 ‘물류 지원’은 여전히 가장 작은 부문에 그치고 있습니다. 이는 적재량 제한 및 운항 승인이 규제된 공역이나 복잡한 공역에서의 일상적인 화물 수송 임무를 여전히 제약하고 있기 때문입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the south america oil and gas drone services market size is projected to expand from USD 278.38 million in 2025 and USD 301.85 million in 2026 to USD 452.43 million by 2031, registering a CAGR of 8.43% between 2026 to 2031.

This report is Segmented by Service Type (Inspection & Monitoring, Surveying & Mapping, Emergency Response & Environmental Monitoring, and Logistics Support), Application (Pipeline Monitoring & Integrity, and More), Drone Type (Multi-Rotor, and More), and Geography (Brazil, Argentina, Guyana, Colombia, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

South America Oil And Gas Drone Services Market Trends and Insights

Cost and Safety Economics Are Reframing the Total Value Proposition

The South America oil and gas drone services market is seeing stronger adoption because operators are treating drone inspection as a safer and more repeatable alternative to confined-space entry, rope access, and other labor-heavy methods. This shift is especially visible in Brazil, where Transpetro reported savings of up to BRL 1 million, or USD 171,000, per tanker inspection cycle after moving to drone-based confined-space surveys, while inspection time fell from 1 week to 3 to 4 days. The commercial effect is important because once inspection moves into routine operating budgets, procurement becomes steadier and contract renewals become easier to justify. The South America oil and gas drone services market is also supported by growing comfort with drone-generated inspection data in formal survey environments, which reduces resistance from operators that previously viewed drone use as a pilot activity rather than a core process . This combination of lower field exposure, shorter downtime, and clearer documentation is helping drone services move into long-cycle maintenance programs.

Pipeline and Critical Asset Integrity Requirements Drive Long-Cycle Contracts

The South America oil and gas drone services market continues to gain from the region's large network of pipelines, terminals, storage systems, and offshore transfer assets that need regular visual and thermal review. Operators are placing more value on documented inspection history because asset failures now carry operational, financial, and reputational consequences well beyond the repair itself. That is especially relevant in remote corridors, where weather, terrain, and access limits make manual inspection slower and less consistent. In this setting, drone services are becoming part of integrity management programs rather than one-off field jobs, which supports longer contract duration and more frequent repeat work. The South America oil and gas drone services market therefore benefits not only from the need to inspect assets, but also from the need to preserve an auditable inspection trail across distributed infrastructure.

Fragmented BVLOS Frameworks and Aviation Approval Overhead

The South America oil and gas drone services market still faces a major scaling challenge because operators must navigate separate drone approval systems across national borders. Brazil's ANAC opened Public Consultation No. 09 in June 2025 and proposed RBAC 100, which shifts regulation toward a risk-based system with Open, Specific, and Certified categories and introduces a Specific Category operating framework tied to risk assessment methods such as SORA . Argentina also issued Resolution 550/2025 and moved to RAAC 100, 101, and 102, replacing its older class-based system with Open, Specific, and Certified categories aligned with ICAO and Latin American Aeronautical Regulations. Even with that progress, BVLOS missions in the Specific Category still require operational approvals and supporting risk mitigation, which adds lead time and raises deployment cost for cross-border corridor work. The South America oil and gas drone services market therefore favors firms with local entities, local compliance experience, and the ability to absorb country-specific approval delays.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Multi-Sensor Payloads Extend Inspection Scope Per Flight

- Offshore Brazil and Guyana Development Expanding Remote Inspection Demand

- Environmental and Infrastructure Limitations at the Operating Edge

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Inspection and Monitoring retained a 41.8% share in 2025, which kept it as the largest service type in the South America oil and gas drone services market. The segment leads because it addresses the region's most immediate need, which is frequent review of pipelines, tanks, flare stacks, offshore structures, and other integrity-sensitive assets. Its position is strongest in Brazil, where offshore maintenance programs and tanker inspections already support routine use of drone-based visual review and confined-space access. Formal acceptance of drone-based ultrasonic thickness workflows also strengthens this service line because it makes drone output more usable in recognized inspection and survey settings.

Surveying and Mapping is projected to expand at a 9.8% CAGR from 2026 to 2031, making it the fastest-growing service type in the South America oil and gas drone services industry. Growth is being supported by new route studies, pre-construction planning, right-of-way mapping, and digital twin development across emerging and expanding oil and gas projects. Emergency Response and Environmental Monitoring is also rising as emissions control and leak traceability become more regular contractual needs rather than occasional field exercises. In the South America oil and gas drone services industry, Logistics Support remains the smallest segment because payload limits and operating approvals still restrict routine cargo missions in controlled or complex airspace.

List of Companies Covered in this Report:

- Cyberhawk Innovations Limited

- Terra Drone Corporation

- OMNI Taxi Aereo

- TEXO DSI

- Axess GLASS Inc.

- SkyX Systems Corp.

- DATUM Ingenieria SAS

- DR1 Technology Solutions

- Aurora Data

- Uali

- Terra Vision

- Fugro

- Saipem

- Percepto

- Flyability

- Voliro

- Intertek

- GuyDrones

- DronesSkycam

- Aerodyne Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Market Definition

- 1.3 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Recent Trends and Developments

- 4.3 Market Drivers

- 4.3.1 Cost and safety gains versus scaffolding, rope access, and helicopters

- 4.3.2 Rising pipeline and critical asset integrity requirements

- 4.3.3 AI-enabled thermal, LiDAR, OGI, and digital twin inspection workflows

- 4.3.4 Offshore Brazil and Guyana development expanding remote inspection demand

- 4.3.5 Vaca Muerta methane-monitoring demand

- 4.3.6 Remote pipeline-right-of-way surveillance in hard-to-access corridors

- 4.4 Market Restraints

- 4.4.1 Fragmented aviation approvals and BVLOS constraints

- 4.4.2 Weather, salt spray, wind, and GPS-denied operating conditions

- 4.4.3 Sparse digital maintenance backbones at regional operators

- 4.4.4 Critical-infrastructure data sovereignty and security sensitivity

- 4.5 Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Inspection & Monitoring

- 5.1.2 Surveying & Mapping

- 5.1.3 Emergency Response & Environmental Monitoring

- 5.1.4 Logistics Support

- 5.2 By Application

- 5.2.1 Pipeline Monitoring & Integrity

- 5.2.2 Offshore Platforms & FPSOs

- 5.2.3 Refineries & Petrochemical Facilities

- 5.2.4 Exploration, Construction & ROW Survey

- 5.2.5 Emissions, Spill & ESG Monitoring

- 5.3 By Drone Type

- 5.3.1 Multi-rotor Drones

- 5.3.2 Fixed-wing Drones

- 5.3.3 Hybrid VTOL Drones

- 5.3.4 Confined-space / Indoor Drones

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Guyana

- 5.4.4 Colombia

- 5.4.5 Ecuador

- 5.4.6 Peru

- 5.4.7 Chile

- 5.4.8 Venezuela

- 5.4.9 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Cyberhawk Innovations Limited

- 6.4.2 Terra Drone Corporation

- 6.4.3 OMNI Taxi Aereo

- 6.4.4 TEXO DSI

- 6.4.5 Axess GLASS Inc.

- 6.4.6 SkyX Systems Corp.

- 6.4.7 DATUM Ingenieria SAS

- 6.4.8 DR1 Technology Solutions

- 6.4.9 Aurora Data

- 6.4.10 Uali

- 6.4.11 Terra Vision

- 6.4.12 Fugro

- 6.4.13 Saipem

- 6.4.14 Percepto

- 6.4.15 Flyability

- 6.4.16 Voliro

- 6.4.17 Intertek

- 6.4.18 GuyDrones

- 6.4.19 DronesSkycam

- 6.4.20 Aerodyne Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment