|

시장보고서

상품코드

2064414

남미의 풍력 터빈 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)South America Wind Turbine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

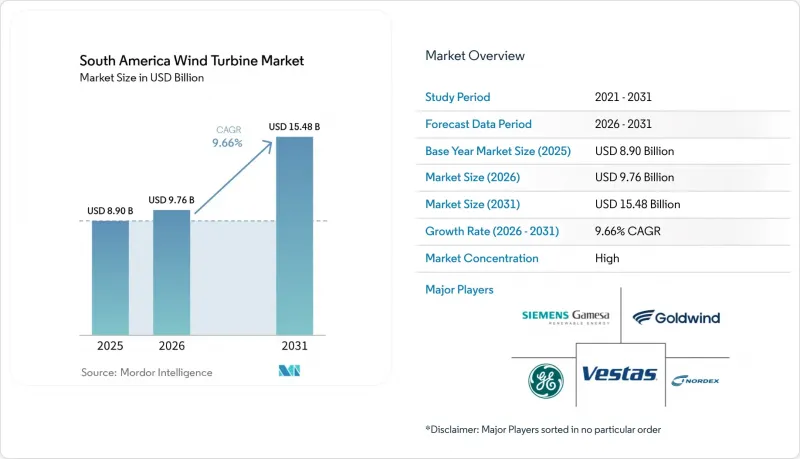

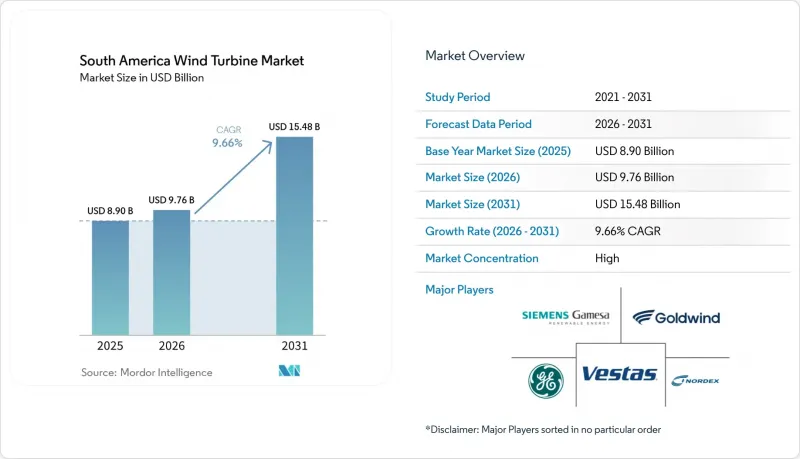

Mordor Intelligence에 의하면, 남미의 풍력 터빈 시장 규모는 2025년 89억 달러로 평가되었습니다. 2026년 97억 6,000만 달러에서 2031년까지 154억 8,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 9.66%를 나타낼 것으로 예측됩니다.

본 보고서는 설치 장소(육상, 해상), 정격 출력(소형, 중형, 대형, 초대형), 축 유형(수평축, 수직축), 구성 부품(로터 블레이드, 나셀·드라이브트레인, 발전기 등), 최종 용도(유틸리티 규모, 상업 및 산업용, 기타), 지역(브라질, 칠레, 아르헨티나, 콜롬비아, 기타 남미)에 따라 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

남미의 풍력 터빈 시장 동향 및 인사이트

LCOE의 하락으로 인해, 육상 풍력이 해당 지역에서 가장 저렴한 조절 가능한 전원이 되었습니다.

육상 발전 비용의 저렴함은 해당 지역의 신규 터빈 수요를 뒷받침하는 가장 확실한 요인 중 하나로 계속해서 자리 잡고 있습니다. 브라질의 육상 풍력 발전 LCOE는 2024년에 0.025달러/kWh까지 하락했으며, 브라질의 풍력 발전 설비군은 56%의 설비 가동률을 달성했습니다. 이는 전 세계 육상 평균을 크게 웃도는 수치입니다. 이러한 비용 우위는 자금 조달 비용이 높은 수준을 유지하거나 송전망 접근이 불확실해질 경우에도 개발 사업자가 프로젝트의 수익성을 유지할 수 있는 여지를 제공한다는 점에서 중요합니다. 또한, 이러한 비용 우위 덕분에 특히 브라질 북동부 및 기타 강풍이 부는 지역에서 육상 프로젝트들은 조달 라운드와 양자 계약에서 경쟁력을 발휘하고 있습니다. 남미의 풍력 터빈 시장의 경우, 이는 신규 설치에 대한 기본 시나리오가 정책 지원뿐만 아니라 여전히 육상 풍력의 경제성에 의해 결정된다는 것을 의미합니다.

재생에너지 PPA 및 입찰 프로젝트 파이프라인이, 정부의 전력 임베디드을 넘어선 계약의 확실성을 확대

신규 풍력 프로젝트 수요 기반은 주로 정부 주도의 경매에 의존하던 기존 모델보다 점차 확대되고 있습니다. 기업 구매자, 산업 사용자, 대규모 디지털 인프라 사업자들이 장기적인 재생에너지 조달에서 더 큰 역할을 수행하게 됨에 따라, 개발자들은 계약 수익을 창출할 수 있는 다양한 경로를 확보할 수 있게 되었습니다. 아마존은 2026년 말까지 칠레에 AWS 인프라 리전을 구축할 것이라고 발표했으며, 40억 달러 이상을 투자할 계획입니다. 해당 사이트에서는 재생에너지가 운영 모델의 일부를 차지하고 있습니다. 이는 프로젝트 개발에 있어 중요한 의미를 지닙니다. 왜냐하면, 구매자층이 두터워지면 정부가 조달 규모를 축소하더라도 풍력 발전 설비 확충을 뒷받침할 수 있기 때문입니다. 남미의 풍력 터빈 시장에서 이러한 변화는 계약의 다양성을 높여, 신용도가 높은 대규모 구매처의 요구에 맞추어 풍력 발전 사업 계획을 조정할 수 있는 개발업체에 유리하게 작용하고 있습니다.

송전망의 과부하가 브라질 북동부 풍력 발전 벨트 전역에 구조적인 수익 위험을 초래합니다.

브라질 북동부 지역의 송전망 과부하는 여전히 대규모 풍력 발전 프로젝트의 주요 운영상의 제약 요인으로 작용하고 있습니다. 풍력 및 태양광 발전소에서 출력 제한으로 인한 손실은 2025년에 220% 증가하여 3,290만 MWh에 달했습니다. 이는 이 문제가 지역적인 운영상의 과제에서 더 광범위한 투자상의 우려로 급속히 확대되었음을 보여줍니다. 손실된 메가와트시를 개별 프로젝트에 배분하지 않더라도, 시장에 미치는 영향은 분명합니다. 왜냐하면 금융 기관, OEM, 개발사들은 한때 가장 안전한 풍력 발전 회랑으로 여겨졌던 지역에서도 가동률 저하를 고려하지 않을 수 없게 되었기 때문입니다. 이것이 바로 남미의 풍력 터빈 시장이 여전히 성장하고 있는 점, 입지 조건의 질, 지역 수요와의 부합, 송전망 강화 속도에 대한 관심이 높아지고 있는 이유입니다.

부문별 분석

2025년, 육상 풍력 발전은 설치 기준의 90.6%를 차지했으며, 지역 전체의 터빈 수요에서 확고한 중심적 위치를 계속 차지하고 있습니다. 남미의 풍력 터빈 시장의 이 분야는 브라질, 아르헨티나, 칠레에 구축된 육상 개발 회랑의 혜택을 지속적으로 누리고 있습니다. 이 지역들은 풍력 자원이 풍부하며, 금융 기관이나 전력 회사에게 있어 공급 모델도 이미 익숙한 것입니다. 또한, 육상 프로젝트는 해상 프로젝트보다 기존의 제조 및 물류 네트워크에 더 적합하며, 공급 환경이 어려워졌을 때도 비용 경쟁력을 유지하는 데 도움이 됩니다. 이러한 장점은 현지 조달률, 자금 조달의 용이성, 운송 실행력이 터빈 기술과 거의 동등한 수준의 영향력을 프로젝트의 자금 조달 가능성에 미칠 수 있는 이 지역에서 특히 중요합니다.

해상 풍력 발전은 훨씬 소규모의 기반에서 시작되지만, 2031년까지 연평균 성장률(CAGR) 18.1%를 나타낼 것으로 예측되며, 남미의 풍력 터빈 시장에서 가장 빠르게 확대될 도입 부문이 될 것입니다. 이러한 성장 시나리오는 향후 플랫폼의 규모 확대, 브라질의 정책 체계 정비, 그리고 장래에 해상 발전 활용이 가능한 연안 산업 클러스터에 대한 관심 고조에 힘입어 뒷받침되고 있습니다. 그렇긴 하지만, 해상 풍력은 여전히 항만 정비, 공급망 확충, 프로젝트 실행 경험이 필요하기 때문에 예측 기간의 대부분 동안 육상 풍력보다 수익 규모는 작은 상태를 유지할 것으로 보입니다. 따라서 해상 풍력은 OEM, 개발사, 정부가 향후 제조 및 서비스 역량과 연안 인프라에 대해 생각하는 방식을 변화시키고 있기 때문에 단기적인 주요 영향은 양적인 것이 아니라 전략적인 것이 될 것입니다.

2025년에는 1-5MW급 대형 터빈이 시장의 45.7%를 차지했습니다. 이는 지난 10년 동안 건설된 지역 풍력 발전 프로젝트의 대부분이 이 등급에 속했다는 사실을 반영하고 있습니다. 이러한 설치 실적을 바탕으로, 해당 부문은 계속해서 중요한 위치를 차지하고 있습니다. 왜냐하면 이 출력 등급에 대해서는 설비에 대한 숙련도, 서비스 체계, 그리고 자금 조달에 대한 안정감이 이미 확립되어 있기 때문입니다. 실제로 이를 통해 개발업체들은 브라질 북동부, 파타고니아, 칠레의 풍력 회랑에서 새로운 조달 결정을 평가할 때 안정적인 기준점을 확보할 수 있습니다. 또한, 개발 업체들이 더 대형 기체를 모색하고 있음에도 불구하고, 대형 터빈급 기체가 여전히 단기 수주 활동의 대부분을 차지하고 있음을 의미합니다.

5MW 초과 부문은 발전소 1기당 발전량 증가, 프로젝트당 터빈 대수 감소, 대규모 그린필드 개발의 경제성 향상 등을 배경으로 연평균 성장률(CAGR) 13.8%라는 가장 높은 성장률을 나타낼 것으로 전망됩니다. 골드윈드사가 브라질에 설립한 첫 해외 공장에서 2024년에 5.3MW에서 7.5MW급 터빈 생산을 시작했습니다. 이는 해당 지역공급 상황이 더 높은 출력의 기종에 대응하기 시작하고 있음을 보여줍니다. 따라서 남미의 풍력 터빈 업계는 출력 범위의 다양화를 향해 나아가고 있지만, 개발업체들은 여전히 터빈의 규모와 물류, 설치 조건, 이용 가능한 송전망 용량 간의 균형을 고려해야 하기 때문에 이러한 전환은 점진적으로 이루어질 것으로 보입니다. 예측 기간 동안 초대형 부문 시장 점유율 확대는 주로, 높은 출력과 낮은 BOS(밸런스 오브 시스템) 비용이 대형 구성품으로 인한 시공의 복잡성을 상쇄할 수 있는 프로젝트에서 예상됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the south america wind turbine market size is projected to expand from USD 8.90 billion in 2025 and USD 9.76 billion in 2026 to USD 15.48 billion by 2031, registering a CAGR of 9.66% between 2026 to 2031.

This report is Segmented by Location of Deployment (Onshore, Offshore), Capacity Rating (Small, Medium, Large, Very Large), Axis Type (Horizontal, Vertical), Component (Rotor Blades, Nacelle & Drivetrain, Generator, and More), End-Use Application (Utility-Scale, Commercial & Industrial, and More), and Geography (Brazil, Chile, Argentina, Colombia, Rest of South America). Forecasts are in Value (USD).

South America Wind Turbine Market Trends and Insights

Declining LCOE Turns Onshore Wind Into the Region's Cheapest Dispatchable Resource

Lower onshore generation costs remain one of the clearest supports for new turbine demand in the region. Brazil's onshore wind LCOE fell to USD 0.025/kWh in 2024, and the country's wind fleet achieved capacity factors of 56%, which is well above the global onshore average . That cost position matters because it gives developers room to preserve project returns even when financing stays expensive or transmission access becomes less predictable. It also keeps onshore projects competitive in procurement rounds and bilateral contracts, especially in Brazil's Northeast and other high-wind corridors. For the South America wind turbine market, this means the base case for new installations is still being set by onshore economics rather than by policy support alone.

Renewable-PPA and Auction Pipeline Extends Contract Certainty Beyond Government Offtake

The demand base for new wind projects is becoming broader than the earlier model that depended mainly on government-led auctions. Corporate buyers, industrial users, and large digital infrastructure operators are taking a larger role in long-term renewable procurement, which gives developers more than one route to contract revenues. Amazon announced an investment of more than USD 4 billion to launch an AWS infrastructure region in Chile by the end of 2026, with renewable energy forming part of the operating model for that site. This matters for project development because a deeper buyer pool can support wind additions even when sovereign procurement slows. In the South America wind turbine market, that change is improving contract diversity and favoring developers that can match wind generation profiles with the needs of large, creditworthy offtakers.

Grid Congestion Creates Structural Revenue Risk Across NE Brazil's Wind Belt

Grid congestion in Northeast Brazil remains the main operating constraint for utility-scale wind projects. Curtailment losses for wind and solar plants rose 220% in 2025 and reached 32.9 million MWh, which shows how quickly the issue has moved from a local operating challenge to a broader investment concern. The market effect is clear even without assigning every lost megawatt-hour to a single project, because lenders, OEMs, and developers now have to account for weaker utilization in areas that were once seen as the safest wind corridors. This is why the South America wind turbine market is still growing, but with stronger attention on location quality, local demand pairing, and the pace of transmission reinforcement.

Other drivers and restraints analyzed in the detailed report include:

- Green-Hydrogen Export Hubs Co-locate Wind Infrastructure at Port-Adjacent Sites

- Data-Centre-Led Transmission Upgrades Generate Incremental Wind Demand

- Currency Volatility and High Capital Costs Act as a Structural Barrier to Foreign Investment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Onshore represented 90.6% of the installed base in 2025, which kept it firmly at the center of turbine demand across the region. This part of the South America wind turbine market continues to benefit from established land-based development corridors in Brazil, Argentina, and Chile, where wind resources are strong and the delivery model is already familiar to lenders and utilities. Onshore projects also fit existing manufacturing and logistics networks better than offshore projects do, which helps preserve cost competitiveness when supply conditions tighten. That advantage is especially important in a region where local content, financing access, and transport execution can still influence project bankability almost as much as turbine technology.

Offshore starts from a much smaller base, but it is projected to grow at an 18.1% CAGR through 2031, which makes it the fastest-moving deployment category in the South America wind turbine market. The growth case rests on future platform scaling, a formalizing policy framework in Brazil, and increasing interest in coastal industrial clusters that could use offshore power over time. Even so, offshore will remain a smaller revenue pool than onshore through most of the forecast period because it still needs port readiness, supply-chain depth, and project execution experience. The main near-term effect is therefore strategic rather than volumetric, since offshore is changing how OEMs, developers, and governments think about future manufacturing, service capabilities, and coastal infrastructure.

Large turbines in the 1-5 MW range accounted for 45.7% of the market in 2025, which reflects how most regional wind projects were built over the past decade. That installed base keeps the segment important because fleet familiarity, service capabilities, and financing comfort are already in place for this rating class. In practice, this gives developers a stable reference point when they evaluate new procurement decisions in Brazil's Northeast, Patagonia, and Chile's wind corridors. It also means the large-turbine class still anchors most near-term order activity even as developers look for larger machines.

The above 5 MW segment is projected to record the fastest growth at 13.8% CAGR, driven by a search for higher yield per unit, fewer turbines per project, and better economics in large greenfield developments. Goldwind's first overseas factory in Brazil began producing turbines in the 5.3 MW to 7.5 MW range in 2024, which showed that the regional supply picture is starting to adapt to higher-capacity machines. The South America wind turbine industry is therefore moving toward a wider mix of ratings, but the shift will be gradual because developers still have to balance turbine scale against logistics, site conditions, and available grid capacity. Over the forecast period, the very large category should gain share mainly in projects where stronger output and lower balance-of-system intensity can offset the execution complexity that comes with bigger components.

List of Companies Covered in this Report:

- Vestas Wind Systems A/S

- Siemens Gamesa Renewable Energy SA

- GE Vernova (GE Renewable Energy)

- Nordex SE

- Goldwind Science & Technology Co.

- Iberdrola SA

- Acciona Energia

- Enel Green Power Latin America

- ENGIE Brasil Energia

- Neoenergia (Iberdrola)

- Latin America Power (LAP)

- Colbun SA

- Omega Energia

- Voltalia SA

- Statkraft Latin America

- Mainstream Renewable Power

- Casa dos Ventos Energias Renovaveis

- Enercon GmbH

- Elecnor SA

- Grupo Envision

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining LCOE for On-shore Wind

- 4.2.2 Accelerating Renewable-PPA & Auction Pipeline

- 4.2.3 National Decarbonisation Targets (NDC-aligned)

- 4.2.4 Green-Hydrogen Export Hubs in Patagonia & NE Brazil

- 4.2.5 Data-centre-led Transmission Upgrades (Amazon, MSFT)

- 4.2.6 State-level Manufacturing Incentives in Ceara & Pernambuco

- 4.3 Market Restraints

- 4.3.1 Grid Congestion & Curtailment in NE Brazil

- 4.3.2 Turbine-component Port & Logistics Bottlenecks

- 4.3.3 Currency Volatility & High Financing Costs Across Emerging South American Economies

- 4.3.4 Limited Local Manufacturing Capacity for Large Turbine Components and Dependence on Imports

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Location of Deployment

- 5.1.1 Onshore

- 5.1.2 Offshore

- 5.1.2.1 Fixed-bottom

- 5.1.2.2 Floating

- 5.2 By Capacity Rating

- 5.2.1 Small (Below 100 kW)

- 5.2.2 Medium (100 kW to 1 MW)

- 5.2.3 Large (1 to 5 MW)

- 5.2.4 Very Large (Above 5 MW)

- 5.3 By Axis Type

- 5.3.1 Horizontal Axis

- 5.3.2 Vertical Axis

- 5.4 By Component

- 5.4.1 Rotor Blades

- 5.4.2 Nacelle and Drivetrain

- 5.4.3 Generator

- 5.4.4 Tower

- 5.4.5 Power-Electronics and Control

- 5.5 By End-Use Application

- 5.5.1 Utility-Scale

- 5.5.2 Commercial and Industrial

- 5.5.3 Residential and Micro-grid

- 5.6 By Geography

- 5.6.1 Brazil

- 5.6.2 Chile

- 5.6.3 Argentina

- 5.6.4 Colombia

- 5.6.5 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Vestas Wind Systems A/S

- 6.4.2 Siemens Gamesa Renewable Energy SA

- 6.4.3 GE Vernova (GE Renewable Energy)

- 6.4.4 Nordex SE

- 6.4.5 Goldwind Science & Technology Co.

- 6.4.6 Iberdrola SA

- 6.4.7 Acciona Energia

- 6.4.8 Enel Green Power Latin America

- 6.4.9 ENGIE Brasil Energia

- 6.4.10 Neoenergia (Iberdrola)

- 6.4.11 Latin America Power (LAP)

- 6.4.12 Colbun SA

- 6.4.13 Omega Energia

- 6.4.14 Voltalia SA

- 6.4.15 Statkraft Latin America

- 6.4.16 Mainstream Renewable Power

- 6.4.17 Casa dos Ventos Energias Renovaveis

- 6.4.18 Enercon GmbH

- 6.4.19 Elecnor SA

- 6.4.20 Grupo Envision

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment