|

시장보고서

상품코드

2064425

가상 병동 관리 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Virtual Ward Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

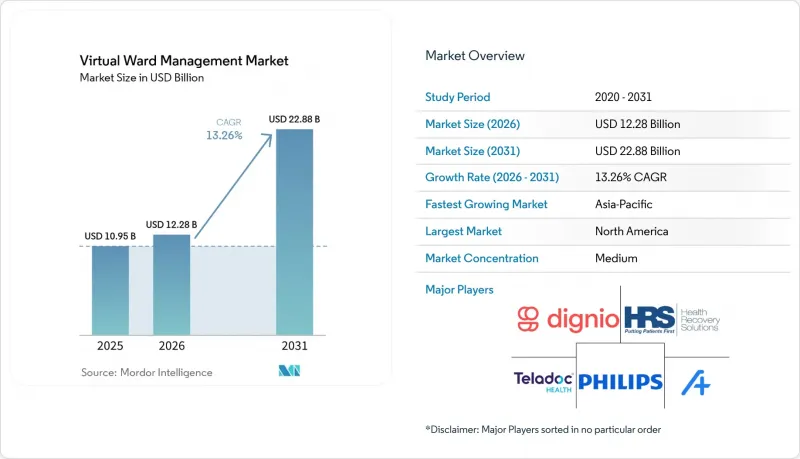

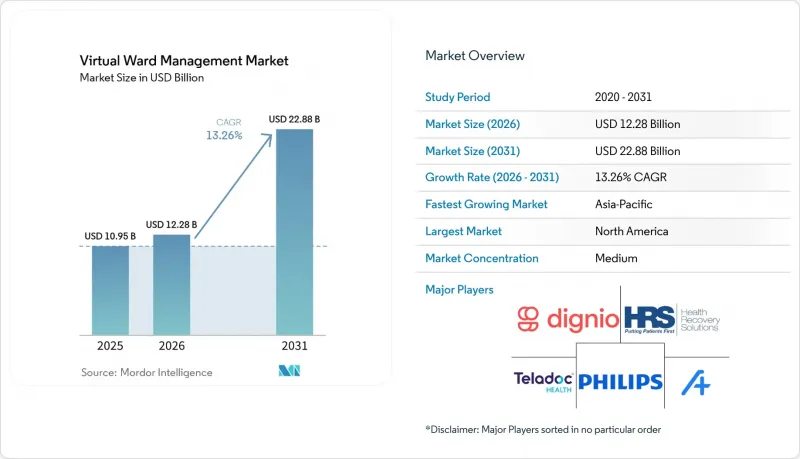

Mordor Intelligence에 의하면, 가상 병동 관리 시장 규모는 2025년 109억 5,000만 달러로 평가되었습니다. 2026년 122억 8,000만 달러에서 2031년까지 228억 8,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 13.26%를 나타낼 것으로 예측됩니다.

본 보고서는 구성 요소(플랫폼 및 소프트웨어, 서비스, 기기 및 주변기기), 기술(RPM, 원격의료, AI 및 분석, 상호운용성), 응용 분야(만성 질환, 급성기 후 관리, 급성기 예방, 노쇠, 외과, 종양학), 최종 사용자(병원 및 의료 시스템, 기타), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

세계의 가상 병동 관리 시장 동향 및 인사이트

병원의 수용 능력과 인력 부족으로 인한 압박

병상 부족과 간호 인력 부족으로 인해, 가상 병동 관리 시장은 단순한 선택적 혁신 모델에서 조달상의 우선 과제로 전환되고 있습니다. 2024년에 시작된 옥스너 헬스(Ochsner Health)의 재택 급성기 치료 프로그램은 입원 및 경과 관찰을 가상 진료와 대면 치료 유닛을 통한 재택 치료로 전환함으로써, 1년도 채 되지 않아 1,000병상일 이상을 절감했습니다. NHS 그레이터 맨체스터의 ‘Hospital&Home’ 프로그램은 883병상 규모에 달하며, 320만 명의 인구를 대상으로 하고 있습니다. 2025년 첫 8개월 동안 1만 9,000명 이상의 환자를 돌보았으며, 평균 입원 일수는 7.5일이었습니다. 또한, NHS 잉글랜드에서는 2024년에 매달 약 115만 병상일의 퇴원 지연이 발생했습니다. 이는 사회복지 서비스나 재택 지원이 충분히 신속하게 마련되지 않아, 임상적으로는 퇴원이 가능한 환자가 병원에 계속 머물러야 했던 것이 원인입니다. 이러한 상황에서 가상 병동 관리 시장이 확대되고 있습니다. 왜냐하면 물리적 병상 확충에는 보통 수년 단위의 자본 사이클이 필요한 반면, 가상 수용 능력은 몇 달 만에 추가할 수 있기 때문입니다.

고령화와 다중 질환 동반으로 인한 부담

가상 병동 관리 시장은 단기적인 일회성 회복 단계가 아니라, 여러 질환을 앓고 있는 고령 환자를 중심으로 구축되는 경향이 강해지고 있습니다. 『Frontiers in Public Health』 저널의 2025년 연구에 따르면, 2023년 말 기준 중국 인구 중 60세 이상 인구는 2억 9,700만 명에 달하고, 전체 인구의 21.1%를 차지했으며, 2050년까지 5억 명에 이를 것으로 예측됩니다. 이 연구에 따르면, 만성 질환 환자 및 장애인을 대상으로 한 지역 재택치료 서비스에 대한 수요가 현저히 높은 것으로 나타났으며, 회귀 계수는 각각 0.3과 0.5였습니다. 이는 지속적인 재택 모니터링 및 케어 코디네이션에 대한 수요가 안정적임을 시사합니다. 싱가포르에서 2026년 5월 『JMIR Formative Research』지에 게재된 후향적 연구에 따르면, 국립대학의료시스템(NUHS) 가상 진료 센터가 처리한 4,857건의 전화 상담을 분석한 결과, 상담자의 평균 연령은 70.5세였으며, 의료 관련 문의의 63.7%가 대면 진료로 전환되지 않고 해결된 것으로 밝혀졌습니다. 이러한 경향은 가상 병동 관리 시장에서 허약한 환자에 대한 지원, 만성 질환 관리 안내, 그리고 빈번한 관찰이 필요하지만 지속적인 입원 치료가 필요하지 않은 환자의 재택 관리로 더 광범위한 전환이 진행되고 있음을 뒷받침합니다.

주요 시장 이외의 지역에서 상환 제도의 불일치

미국, 영국 및 일부 유럽 시장을 제외한 지역에서는 가상 병동 관리 시장이 여전히 불균일한 보험 급여 체계에 직면해 있습니다. 일본 후생노동성의 2024년도 원격의료 조사 보고서에 따르면, 의사 간(D-to-D) 원격 병리 진단을 제공하는 기관의 84%가 운영비에 대한 정부 보조금을 받지 못하고 있었으며, 대부분의 계약에서 보수 분담 조건이 명시되어 있지 않았습니다. 프랑스에서는 2023년, 만성 질환에 대한 원격 모니터링에 대한 보험 급여가 일반법에 포함되었으나, 급성기 단계의 가상 진료 경로에 대해서는 여전히 공식적인 급여 범위가 좁아, 주요 대도시권 이외 지역에서의 확대가 지연되고 있습니다. 한국에서는 의료진의 파업을 거친 끝에, 2024년 2월에 드디어 원격의료가 법적으로 전면 허용되었습니다. 이는 해당국의 규제 완화가 치밀하게 계획된 지불 체계에 기반하여 구축된 것이 아니라, 사후 대응적인 성격이었습니다는 점을 보여줍니다. 그 결과, 가상 병동 관리 시장공급업체들은 국가별로 비용이 많이 드는 확장 모델을 채택할 수밖에 없게 되었으며, 이로 인해 재택 간호가 본래 가져야 할 규모의 경제성이 훼손되고 있습니다.

부문별 분석

2025년 기준으로 플랫폼 및 소프트웨어는 가상 병동 관리 시장 규모의 52.32%를 차지하며, 가장 큰 구성 요소 카테고리가 되었습니다. 가상 병동 관리 업계에서는 독립형 기기군보다 기존 전자의무기록 환경에 쉽게 통합할 수 있기 때문에 의료 서비스 제공업체들은 소프트웨어 중심의 도입을 선호하고 있습니다. 임상 지휘 센터 도구, 치료 조정 대시보드 및 가상 병동 용도는 환자 식별, 상황 격상 및 기록 방식을 결정하는 데 있어 현재 조달 과정에서 핵심적인 역할을 하고 있습니다. 워크플로우의 단편화는 임상 효율을 저하시키기 때문에 공급업체 선정은 병원의 EPR 시스템, 특히 Epic이나 Cerner 환경과의 상호 운용성과 밀접한 관련이 있습니다. 급성기 모니터링에는 여전히 기기나 주변 장비가 필요하지만, 과거에는 전용 의료용 센서에 의존하던 이용 사례가 검증된 일반용 웨어러블 기기로 대체되기 시작하면서, 이러한 기기나 주변 장비에 대한 부담은 커지고 있습니다.

이 서비스는 가상 병동 관리 시장에서 가장 빠르게 성장하고 있는 분야로, 2026년부터 2031년까지 연평균 성장률(CAGR) 14.27%를 나타낼 것으로 전망됩니다. 이러한 추세는 구조적인 아웃소싱 추세를 반영하고 있습니다. 많은 의료 시스템은 기술에 대한 투자는 가능할지라도, 24시간 365일 가동되는 가상 지휘 센터를 독자적으로 운영하기 위한 충분한 인력을 확보하지 못하고 있기 때문입니다. Health Recovery Solutions는 2026년 3월, Rimidi를 인수함으로써 이러한 번들형 접근 방식을 확대했습니다. 이를 통해 심혈관 대사성 만성 질환 관리 기능이 추가되어, Dexcom, FreeStyle Libre, Eversense의 CGM 데이터를 EHR 워크플로우에 직접 통합할 수 있게 되었습니다. 또한, 2026년 3월 Current Health가 Cardinal Health의 Velocare 솔루션과 체결한 물류 제휴는 기기 배송, 설치, 회수 및 공급 관리가 가상 병동 관리 시장에서 독립적이면서도 필수적인 서비스 계층으로 자리 잡고 있음을 여실히 보여주었습니다. 따라서 구성 요소의 조합은 일회성 기술 구매 결정에서 모니터링, 워크플로우 관리, 재택 물류까지를 단일 운영 패키지로 통합한 지속적인 서비스 관계로 점차 전환되고 있습니다.

2025년 기준으로 원격의료 및 가상 상담은 기술 부문의 35.73%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 13.76%로 확대될 것으로 전망됩니다. 이는 최대 부문와 성장률이 가장 높은 부문이 동일한 유일한 세분화 유형으로, 가상 병동 관리 시장에서 원격의료가 성장 정체를 겪지 않고 여전히 확대를 이어가고 있음을 보여줍니다. 이 부문은 의료 종사자들이 익숙한 환경과 보상 범위 확대라는 두 가지 이점을 모두 누리고 있습니다. 따라서 새로운 기기 범주를 중심으로 진료 모델을 재설계하는 것보다, 급성기 및 급성기 이후의 진료 경로에 원격 진료를 통합하는 것이 더 쉬워졌습니다. Teladoc Health는 2026년 1월, Prism 플랫폼을 통해 강화된 ‘24/7 Care’ 서비스를 시작했습니다. 이 회사에 따르면, 이 서비스는 의료 종사자들 간의 실시간 전문의 상담을 지원하며, 통합 케어 플랫폼 전반에서 회원들의 우려 사항 중 95% 이상을 단 한 번의 상담으로 해결하고 있다고 합니다. 이는 가상 병동 관리 시장에 있어 중요한 의미를 지닙니다. 왜냐하면 급성기 가상 진료 경로는 단순한 수동적인 데이터 전송뿐만 아니라, 임상적 판단에 대한 신속한 접근에 의존하고 있기 때문입니다.

원격 환자 모니터링과 AI 분석은 현재 가상 병동 관리 업계에서 차별화가 가장 빠르게 진행되고 있는 기술 분야입니다. 예측적 상태 악화 경보, 자동 기록, 위험도 계층화 도구는 에스컬레이션 지연과 임상 기록 부담을 줄일 수 있기 때문에 시범 운영 단계에서 일상적인 도입 단계로 점차 전환되고 있습니다. Huma는 2025년, Aluna를 인수함으로써 이러한 방향성을 확대했습니다. 이를 통해 미국 내 150개 이상의 의료 시스템과 50만 명의 계약 환자를 대상으로 하는 천식 및 COPD 관리를 위한 FDA 승인 호흡 모니터링 도구가 추가되었습니다. 상호 운용성은 여전히 가장 뚜렷한 미해결 과제입니다. 왜냐하면 대부분의 가상 병동 도입 사례에서 여전히 여러 기기나 플랫폼에서 데이터를 수집하고 있으며, 모니터링 도구와 병원 기록 간의 연결성이 낮아 도입 비용을 증가시키고, 임상 현장에서의 도입을 지연시키고 있기 때문입니다.

지역별 분석

2025년, 북미는 가상 병동 관리 시장 규모의 39.64%를 차지하며 여전히 최대 지역 부문을 유지했습니다. 이 지역은 CMS(미국 의료보험 및 의료서비스 센터)의 ‘급성기 병원 재택 치료(Acute Hospital Care at Home)’ 면제 조치가 2030년까지 연장됨에 따라, 공공 지급 지원 기간이 가장 오래 지속된다는 혜택을 누리고 있습니다. 미국 의사협회(AMA)의 보고서에 따르면, 현재 37개 주의 139개 의료 시스템에서 366개의 승인된 ‘병원 재택 간호’ 프로그램이 운영되고 있으며, 이는 시장이 제한적인 시범 사업 단계를 넘어섰음을 보여줍니다. 클리블랜드 클리닉, 탬파 종합병원, 펜 메디신 등 주요 의료 기관들의 도입 속도는 일회성 혁신 자금이 아닌, 지속적인 상환 체제에 기반해 구축된 운영 규모를 반영하고 있습니다. 캐나다에서는 각 주 차원의 지원이 활발히 이루어지고 있는 반면, 멕시코는 도입 초기 단계에 머물러 있어 시스템 전반으로의 확대는 제한적입니다.

유럽은 영국, 독일, 프랑스가 주도하는 가상 병동 관리 시장에서 여전히 2위의 규모를 자랑하고 있습니다. 독일의 ‘Virtual Hospital NRW’는 2025년 1월부터 전국에서 이용되었으며, 독일의 광범위한 병원 개혁 프레임워크에서 원격의료 네트워크 구조가 적격 인프라로 인정받고 있기 때문에 사업자들은 투자를 위한 직접적인 정책 경로를 확보하게 되었습니다. 영국은 공식적인 가상 병동 수용 능력 목표를 통해 서비스 규모 확대를 지속적으로 추진하고 있으며, 2026년 말까지 2,000병상을 확보하겠다는 스코틀랜드의 2025년 7월 자금 조달 방안은 이러한 국가적 의지를 더욱 공고히 했습니다. 프랑스는 병원 투자 계획이나 RESAH가 주관하는 ‘혁신적인 디지털 솔루션’ 시장을 대상으로 한 Rofim사의 원격의료 플랫폼 선정과 같은 공공 조달 채널을 통해 조달 경로를 확대되고 있습니다.

아시아태평양은 2026년부터 2031년까지 연평균 성장률(CAGR) 15.92%를 나타낼 것으로 예측되며, 가상 병동 관리 시장에서 가장 두드러진 성장을 보일 지역 부문이 될 전망입니다. 이 지역이 확대되고 있는 이유는 고령화, 도시 지역 병원의 과밀화, 디지털 인프라의 개선으로 인해 정부와 의료 제공업체들이 입원 치료 대신 재택 간호라는 대안을 마련해야 하는 압박을 받고 있기 때문입니다. 중국 광둥성 제2성립종합병원은 IoT, AI, 클라우드 컴퓨팅 및 임상 등급 웨어러블 기기를 결합하여, 가정 환경에서도 입원 환자에 대한 모니터링과 동등한 기능을 구현하고 병원 기록으로 데이터를 안전하게 전송하는 ‘5G 스마트 홈 병동’ 모델에 대해 설명했습니다. 한국에서도 원격 모니터링을 재택 입원 모델로 확대하고 있으며, 2026년 4월에는 지역 밀착형 서비스 제공을 목적으로 Sciths와 연세송클리닉이 시범 파트너십을 체결했습니다. 중동 및 아프리카 및 남미는 여전히 초기 단계 시장이지만, GCC 국가들의 정부 주도의 디지털 헬스 인프라와 브라질의 장기적인 공공 조달 기회 덕분에 향후 사업 확장에 있어 중요한 시장으로 남아 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the virtual ward management market size is projected to expand from USD 10.95 billion in 2025 and USD 12.28 billion in 2026 to USD 22.88 billion by 2031, registering a CAGR of 13.26% between 2026 to 2031.

This report is Segmented by Component (Platforms and Software, Services, Devices and Peripherals), Technology (RPM, Telehealth, AI and Analytics, Interoperability), Application (Chronic Disease, Post-Acute, Acute Avoidance, Frailty, Surgical, Oncology), End User (Hospitals and Health Systems, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts are in Value (USD).

Global Virtual Ward Management Market Trends and Insights

Hospital Capacity and Staffing Pressure

Hospital bed shortages and nursing gaps are moving the virtual ward management market from an optional innovation model into a procurement priority. Ochsner Health's acute care at home program, launched in 2024, saved more than 1,000 bed-days in less than 1 year by diverting admissions and observation stays into home-based care supported by a virtual physician and an in-person care unit. NHS Greater Manchester's Hospital@Home program reached 883 beds and served a population of 3.2 million, and it cared for more than 19,000 patients in the first 8 months of 2025 with an average episode length of 7.5 days. NHS England also faced an estimated 1.15 million delayed-discharge bed-days per month in 2024, which kept clinically ready patients in hospital because social care and home support were not in place fast enough. In that setting, the virtual ward management market gains ground because virtual capacity can be added in months, while physical bed expansion usually takes a multi-year capital cycle.

Aging and Multimorbidity Burden

The virtual ward management market is increasingly built around older patients with overlapping conditions rather than around short, one-time recovery episodes. A 2025 study in Frontiers in Public Health reported that China's population aged 60 and above reached 297 million, or 21.1% of the total, by the end of 2023, and it is projected to reach 500 million by 2050. The same study found significantly higher demand for community home medical services among chronically ill individuals and disabled individuals, with regression coefficients of 0.3 and 0.5, respectively, which points to steady demand for continuous home monitoring and care coordination. In Singapore, a retrospective study published in JMIR Formative Research in May 2026 reviewed 4,857 calls handled by the National University Health System Virtual Care Centre and found a mean caller age of 70.5 years, while 63.7% of medical queries were resolved without physical escalation. This pattern supports a broader shift in the virtual ward management market toward frailty support, chronic care navigation, and home-based management of patients who need frequent observation but not continuous inpatient intervention.

Reimbursement Inconsistency Outside Lead Markets

Outside the United States, the United Kingdom, and a limited group of European markets, the virtual ward management market still faces uneven reimbursement pathways. Japan's FY2024 telemedicine research report from the Ministry of Health, Labour and Welfare found that 84% of institutions offering D-to-D remote pathology diagnosis received no government subsidy for operating costs, and remuneration-sharing terms were undefined in most contracts. France placed telesurveillance reimbursement into common law for chronic conditions in 2023, but acute virtual care pathways still have narrower formal payment coverage, which slows scale outside the main urban corridors. South Korea only moved to full legal telemedicine permission in February 2024 after a healthcare labor disruption, which shows that regulatory opening there has been reactive rather than built around a fully planned payment architecture. This leaves vendors in the virtual ward management market with a costly country-by-country expansion model that weakens the scale efficiency that home-based care should otherwise offer.

Other drivers and restraints analyzed in the detailed report include:

- Reimbursement Normalization for Hospital-At-Home

- Cybersecurity and Clinical Governance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platforms and software represented 52.32% of the virtual ward management market size in 2025, which made this the largest component category. In the virtual ward management industry, providers are favoring software-led deployments because these systems fit more easily into existing electronic patient record environments than stand-alone device stacks. Clinical command center tools, care coordination dashboards, and virtual ward applications sit at the center of current procurement because they determine how patients are identified, escalated, and documented. Vendor selection is therefore tied closely to interoperability with hospital EPR systems, especially Epic and Cerner environments, because fragmented workflows reduce clinical efficiency. Devices and peripherals remain necessary for acute monitoring, but they are facing more pressure as validated consumer wearables begin to cover use cases that once depended on proprietary medical sensors.

Services are the fastest-growing component in the virtual ward management market, with a projected CAGR of 14.27% from 2026 to 2031. That pattern reflects a structural outsourcing trend because many health systems can fund technology but still do not have enough staff to run a 24/7 virtual command center on their own. Health Recovery Solutions expanded this bundled approach in March 2026 through its acquisition of Rimidi, which added cardiometabolic chronic care capabilities and direct integration of CGM data from Dexcom, FreeStyle Libre, and Eversense into EHR workflows. Current Health's March 2026 logistics partnership with Cardinal Health's Velocare solution also highlighted how device delivery, setup, retrieval, and supply management are becoming a separate but essential service layer in the virtual ward management market. The component mix is therefore shifting from one-time technology purchase decisions toward recurring service relationships that combine monitoring, workflow management, and home logistics into a single operational package.

Telehealth and virtual consultation held 35.73% of the technology segment in 2025 and is also projected to expand at a 13.76% CAGR through 2031. This is the only segmentation type in which the largest segment and the fastest-growing segment are the same, which shows that telehealth in the virtual ward management market is still scaling rather than flattening. The segment benefits from both clinician familiarity and broadening reimbursement, which makes it easier to insert remote consultation into acute and post-acute pathways than it is to redesign the care model around a new device category. Teladoc Health launched its enhanced 24/7 Care service in January 2026 through the Prism platform, and the company said the service supports real-time provider-to-provider specialist consultation and resolves more than 95% of member concerns in a single session across its integrated care base. That matters for the virtual ward management market because acute virtual pathways depend on fast access to clinical judgment, not just on passive data transmission.

Remote patient monitoring and AI analytics are the technology layers where differentiation is now moving fastest in the virtual ward management industry. Predictive deterioration alerts, automated documentation, and risk stratification tools are shifting from pilots into day-to-day deployment because they can reduce escalation delays and clinical documentation burden. Huma expanded this direction in 2025 through the acquisition of Aluna, which added FDA-cleared respiratory monitoring tools for asthma and COPD management across more than 150 US health systems and 500,000 contracted lives. Interoperability remains the clearest unmet need because most virtual ward deployments still pull data from multiple devices and platforms, and weak connector coverage between monitoring tools and hospital records raises deployment cost and slows clinical adoption.

Geography Analysis

North America accounted for 39.64% of the virtual ward management market size in 2025, which kept it as the largest regional segment. The region benefits from the longest runway of formal payment support because the CMS Acute Hospital Care at Home waiver now runs through 2030. The American Medical Association reported that 366 approved hospital-at-home programs are now spread across 139 health systems in 37 states, which shows that the market has moved beyond limited pilot concentration. The pace of deployment by major providers, including Cleveland Clinic, Tampa General Hospital, and Penn Medicine, reflects an operating scale that is being built on reimbursement continuity rather than on one-off innovation funding. Canada adds supportive provincial momentum, while Mexico remains at an earlier adoption stage with more limited systemwide rollout.

Europe remains the second-largest region in the virtual ward management market, led by the United Kingdom, Germany, and France. Germany's Virtual Hospital NRW became nationally available from January 2025, and its broader hospital transformation framework recognizes telemedical network structures as eligible infrastructure, which gives operators a direct policy route for investment. The United Kingdom continues to push service scale through formal virtual ward capacity targets, and Scotland's July 2025 funding package for 2,000 beds by end-2026 reinforced that national commitment. France is widening procurement pathways through its hospital investment plan and through public purchasing channels, such as the RESAH selection of Rofim's telemedicine platform for the Innovative Digital Solutions market.

Asia-Pacific is projected to grow at a 15.92% CAGR from 2026 to 2031, making it the fastest-growing regional segment in the virtual ward management market. The region is expanding because aging populations, urban hospital crowding, and improving digital infrastructure are pushing governments and providers to build home-based alternatives to inpatient care. China's Guangdong Second Provincial General Hospital described a 5G Smart Home Ward model that combines IoT, AI, cloud computing, and clinical-grade wearables into a home-based equivalent of inpatient monitoring with secure transmission into the hospital record. South Korea is also extending remote monitoring into home hospitalization models, including the April 2026 pilot partnership between Sciths and Yonsei Song Clinic for community-based service delivery. The Middle East and Africa and South America remain earlier-stage markets, but government-backed digital health infrastructure in GCC countries and longer-term public procurement opportunities in Brazil keep them relevant for later expansion.

- Agyle Health

- Biofourmis

- Current Health

- Dignio

- Doccla

- Generated Health

- Gro Health

- Health Call Solutions

- Health Recovery Solutions

- Huma

- Inbound Health

- Kensa Health

- Medoma

- Ortus-iHealth

- patientMpower

- Koninklijke Philips

- Provide Digital

- Sciensus

- Teladoc Health

- Veta Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hospital Capacity and Staffing Pressure

- 4.2.2 Aging and Multimorbidity Burden

- 4.2.3 Reimbursement Normalization for Hospital-At-Home

- 4.2.4 RPM And AI-Enabled Deterioration Detection

- 4.2.5 Occupancy And Admission-Avoidance KPI Pressure

- 4.2.6 Home Diagnostics and Logistics Orchestration Demand

- 4.3 Market Restraints

- 4.3.1 Reimbursement Inconsistency Outside Lead Markets

- 4.3.2 Cybersecurity and Clinical Governance Burden

- 4.3.3 Home Suitability and Caregiver Readiness Gaps

- 4.3.4 Device Logistics and EPR Interoperability Friction

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Component

- 5.1.1 Platforms and Software

- 5.1.2 Services

- 5.1.3 Devices and Peripherals

- 5.2 By Technology

- 5.2.1 Remote Patient Monitoring

- 5.2.2 Telehealth and Virtual Consultation

- 5.2.3 AI and Analytics

- 5.2.4 Interoperability and Workflow Orchestration

- 5.3 By Application

- 5.3.1 Chronic Disease Management

- 5.3.2 Post-Acute and Early Supported Discharge

- 5.3.3 Acute Admission Avoidance

- 5.3.4 Frailty and Elderly Care

- 5.3.5 Surgical Pathway Monitoring

- 5.3.6 Oncology and Specialty Pathways

- 5.4 By End User

- 5.4.1 Hospitals and Health Systems

- 5.4.2 Integrated Delivery Networks and Provider Groups

- 5.4.3 Community and Home Healthcare Providers

- 5.4.4 Payers and Government Programs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Agyle Health

- 6.3.2 Biofourmis

- 6.3.3 Current Health

- 6.3.4 Dignio

- 6.3.5 Doccla

- 6.3.6 Generated Health

- 6.3.7 Gro Health

- 6.3.8 Health Call Solutions

- 6.3.9 Health Recovery Solutions

- 6.3.10 Huma

- 6.3.11 Inbound Health

- 6.3.12 Kensa Health

- 6.3.13 Medoma

- 6.3.14 Ortus-iHealth

- 6.3.15 patientMpower

- 6.3.16 Philips

- 6.3.17 Provide Digital

- 6.3.18 Sciensus

- 6.3.19 Teladoc Health

- 6.3.20 Veta Health

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment