|

시장보고서

상품코드

2064427

불멸화 세포주 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Immortalized Cell Line - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

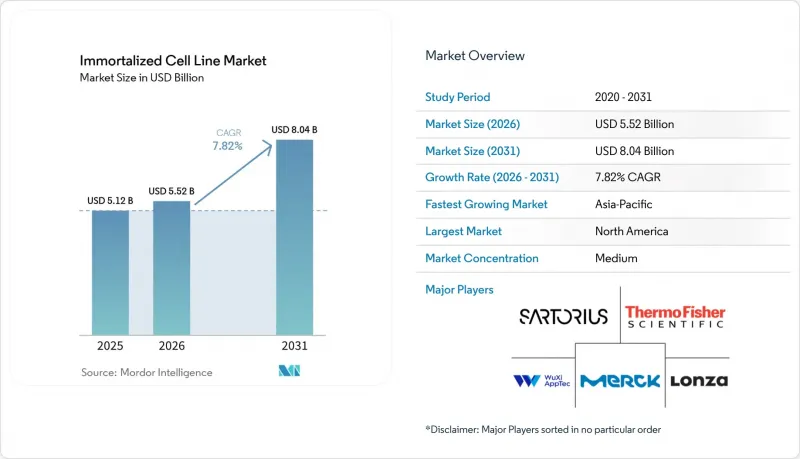

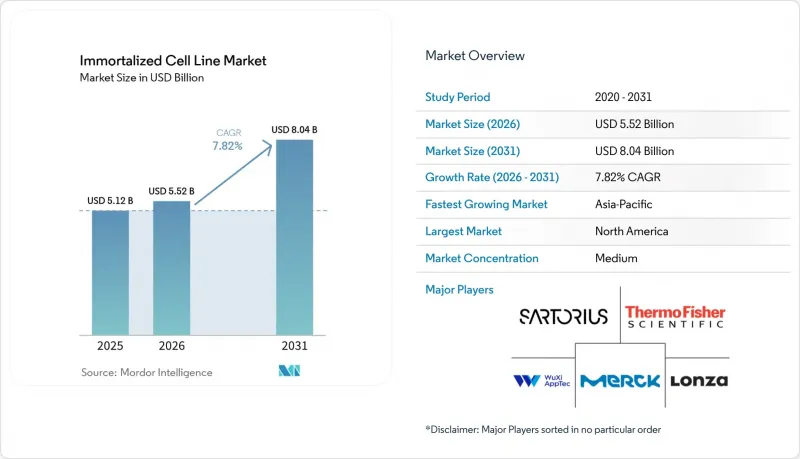

Mordor Intelligence에 의하면, 불멸화 세포주 시장 규모는 2025년 51억 2,000만 달러로 평가되었습니다. 2026년 55억 2,000만 달러에서 2031년까지 80억 4,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 7.82%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형(인간, 동물), 불멸화 기법(바이러스 매개, HTERT 매개 등), 용도(신약 개발, 독성 시험 등), 최종 사용자(제약·바이오기술 기업, 학술·연구 기관 등) 및 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 불멸화 세포주 시장 동향 및 인사이트

바이오의약품 및 바이러스 벡터 파이프라인 확대

불멸화 세포주 시장은 바이오의약품 및 유전자 치료제 생산 프로그램 전반에 걸쳐 GMP 인증을 받은 기질을 연속 배양해야 할 필요성이 높아짐에 따라 그 혜택을 누리고 있습니다. 포유류 연속 배양 세포주, 특히 CHO 및 HEK293 유래 세포주는 승인된 재조합 단백질 생산에서 여전히 핵심적인 역할을 하고 있으며, 한편 HEK293 유래 시스템은 AAV 및 렌티바이러스 벡터 제조에도 필수적입니다. 론자가 2026년 5월에 출시한 ‘Xcite AAV’ 안정 생산 세포주 플랫폼은 일시적 형질전환에 비해 AAV 역가가 10배에서 15배로 증가하며, 제조 원가를 80% 이상 절감할 수 있음을 보여주었습니다. 이는 안정적인 생산 형식이 얼마나 빠르게 상업적 활용으로 전환되고 있는지를 보여줍니다. 고용량 신경망 프로그램의 경우, 일시적인 시스템 부하가 실용적인 비용 한계를 초과하는 경우가 많기 때문에 이 성능은 중요합니다. 안정 세포주를 이용한 AAV 생산의 실용성이 높아짐에 따라, 불멸화 세포주 시장에서는 인증 생산 세포주, 세포 뱅크 및 분석 지원에 대한 수요가 더욱 증가하고 있습니다. 이러한 변화는 업스트림 공정의 세포주 설계와 다운스트림 공정의 제조 문서화를 단일 플랫폼에서 연계할 수 있는 공급업체에게도 유리하게 작용합니다.

신약 개발 및 독성 스크리닝의 활성화

불멸화 세포주 시장은 고처리량 스크리닝 분야에서 지속적인 지지를 받고 있으며, 이 분야에서 연속 배양 세포주는 재현성 있는 분석 성능의 표준 기반으로서 자리 잡고 있습니다. 3D 스페로이드, 오가노이드 공동 배양, 그리고 오가노이드-온-칩 시스템과 같은 보다 복잡한 분석 방식은 여전히, 더 긴 실험 기간 동안 안정적인 거동을 유지할 수 있는 세포주에 의존하고 있습니다. 머크 KGaA가 2025년 10월 프로메가와 체결한 제휴(이 회사가 이전에 HUB Organoids를 인수한 데 따른 것)는 공급업체가 불멸화 세포주를 대체하는 것이 아니라, 보다 정교한 스크리닝 환경 내에 통합되는 분석 시스템에 투자하고 있음을 보여줍니다. 또한, 2026년 4월 FDA가 발표한 인간 유전자 치료 제품에 대한 유전체 편집 안전성 평가 지침 초안에 따라, 개발 프로그램 전반에 걸쳐 검증된 세포 기반 효능 및 기능 분석의 필요성이 높아지고 있습니다. 이 요건으로 인해 프로그램별로 필요한 인증된 인간 세포 모델의 수가 증가합니다. 따라서 불멸화 세포주 시장은 연구량 증가뿐만 아니라, 현대 의약품 개발 과정에 반영된 더욱 엄격한 검증 요건으로부터도 혜택을 받게 될 것입니다.

높은 개발·검증·품질 관리 비용

불멸화 세포주 시장은 여전히 연구 용도에서 GMP 인증 생산 용도로 세포주를 전환할 때 발생하는 비용이라는 명확한 제약에 직면해 있습니다. 이 과정에는 STR 프로파일링, 마이코플라스마 검사, 외래 병원체 선별 검사, 바이러스 안전성 평가, 핵형 분석 및 안정성 평가가 필요하며, 이는 각 프로그램의 일정과 예산 모두에 부담을 주고 있습니다. 마스터 세포 은행에서 제조 종료 시점의 세포 윈도우에 이르기까지의 유전적 안정성을 입증해야 할 필요성은 여러 초기 단계 자산을 보유한 개발 기업에게 추가적인 부담이 됩니다. 소규모 바이오테크 기업들은 완전한 특성 평가를 미루거나, 이미 검증된 모주를 보유하고 있는 CDMO에 의존함으로써 이러한 과제를 해결하는 경우가 많습니다. 이러한 의존 관계는 가격 결정권을 통합형 서비스 제공업체로 넘겨주게 되어, 세포주 개발의 전 과정을 자체적으로 관리하고자 하는 기업의 유연성을 저해합니다. 또한, 불멸화 세포주 시장에 새로 진입한 기업들이 사업을 확장할 수 있는 속도도 제한하게 될 것입니다.

부문별 분석

2025년 기준으로, 인간 세포주는 매출의 55.3%를 차지하며 불멸화 세포주 시장에서 가장 큰 제품 카테고리가 되었습니다. 해당 부문은 2031년까지 연평균 성장률(CAGR) 8.4%로 확대될 것으로 예상되며, 이는 그 성장이 동물 유래 균주에서 비롯된 단기적인 구성 변화가 아니라 구조적인 수요에 의해 주도되고 있음을 의미합니다. 인간 세포주가 여전히 중심적인 위치를 차지하고 있는 이유는 인간의 질병 생물학을 보다 직접적으로 모델링하고, 인간과 관련된 항체 연구를 지원하며, 유전자 치료 프로그램에서 바이러스 벡터의 기질로 기능하기 때문입니다. HEK293, HeLa, Jurkat 등 각 세포주는 종양학, 독성학 및 벡터 생산 워크플로우에서 여전히 널리 사용되고 있습니다. 이러한 폭넓은 용도로 인해, 인간 세포주 부문은 불멸화 세포주 업계 전체에서 조달 결정의 핵심으로 자리매김하고 있습니다.

이 부문에서는 배치 간 일관성을 높이고, 보다 용도 특화된 이용 사례에 대응할 수 있기 때문에 유전자 변형 파생 균주의 상업적 비중이 높아지고 있습니다. 『Stem Cell Research &Therapy』 저널의 2025년 연구에 따르면, hTERT 불멸화 MSC 주에서 얻어지는 세포외 소포프로파일이 배치 간에 일관된 것으로 보고되었으며, 이는 치료용 EV 플랫폼에서 해당 소포를 사용하는 것을 뒷받침하는 결과입니다. 동물 세포주는 여전히 필수적인 역할을 담당하고 있으며, 특히 재조합 단백질 생산에 사용되는 CHO 세포주와, 기존 백신 및 연구 워크플로우에 사용되는 Vero 세포주 및 BHK-21 세포주가 대표적입니다. 동시에, 배양육 및 수의학 분야에서의 소, 말, 기타 종 특이적 세포주의 보급으로 인해 불멸화 세포주 시장의 잠재적 수요층이 확대되고 있습니다. 동물 유래 세포주에 대한 규제 시험 요건 역시, 이미 확립된 생물안전 및 특성 평가 실험실을 운영하고 있는 공급업체에게 유리하게 작용하고 있습니다.

2025년에는 바이러스 매개 불멸화가 매출의 40.2%를 차지하며, 불멸화 세포주 시장에서 가장 큰 방법 부문으로서의 위상을 유지했습니다. 이러한 대규모 도입 실적은 고증식성 연구용 세포주를 생성하기 위해 수십 년에 걸쳐 SV40, HPV E6/E7 및 아데노바이러스 도구를 사용해 온 사실을 반영하고 있습니다. 또한, Vero나 MDCK와 같은 백신 생산용 배지는 여전히 오랜 기간에 걸쳐 확립된 공정에 의존하고 있기 때문에 이 방법에는 안정적인 수요의 하한선이 존재합니다. 그럼에도 불구하고, hTERT를 통한 불멸화는 2031년까지 연평균 성장률(CAGR) 8.5%를 나타낼 것으로 예측되며, 가장 빠르게 성장하는 기술 부문이 될 전망입니다. 이러한 급속한 성장은 hTERT가 바이러스성 발암 단백질에 수반되는 p53 및 pRB 경로의 파괴를 유발하지 않으면서 복제 수명을 연장하기 때문에 안전성 프로파일이 더 우수함을 반영합니다.

2025년에 발표된 NIST의 연구는 정밀한 hTERT 녹인(knock-in)을 통해 안정적인 핵형과 면역학적 특징을 유지한 불멸화된 인간 1차 CD8+ T세포를 생성할 수 있음을 보여줌으로써 이러한 경향을 뒷받침했습니다. 하이브리도마 융합법은 재조합 플랫폼 시장 점유율이 지속적으로 확대되고 있음에도 불구하고, 기존의 단일클론 항체 워크플로우 및 다클론 항체 생산 분야에서 여전히 중요한 위치를 차지하고 있습니다. 자연 발생 및 화학적 지속화 방법은 여전히 틈새 시장 수준에 머물러 있지만, 일부 관할 구역에서 ‘비유전자변형(non-GMO)’이라는 지위가 규제상 중요한 의미를 띠고 있는 식품 생명공학 분야에서는 주목을 받고 있습니다. 영속화 세포주 업계의 구매자들에게 있어, 현재 방법 선택은 역사적인 견고성, 안전성 프로파일, 그리고 후속 규제 부담 간의 상충 관계를 더욱 명확하게 반영하는 방향으로 변화하고 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 38.2%를 차지하며 불멸화 세포주 시장 규모에서 가장 큰 점유율을 기록했습니다. 이 지역이 이러한 우위를 유지하고 있는 것은 활발한 바이오의약품 연구개발 활동은 물론, GMP 등급의 세포 은행 시설로 구성된 성숙한 네트워크, 그리고 세포 기질의 상세한 특성 평가를 요구하는 규제 체계가 결합되어 있기 때문입니다. 2026년 4월 FDA가 발표한 유전자 편집 안전성 평가에 관한 지침안은 개발 단계에서 인증 및 특성 평가가 완료된 세포 기반 분석법을 더욱 중시하고 있어, 이러한 수요를 더욱 촉진하고 있습니다. 또한, 2026년 5월 GI 파트너스가 찰스 리버가 매각한 CDMO 및 세포 솔루션 사업을 통합하여 로즈 바이오솔루션즈를 설립한 사실도 북미의 세포 솔루션 인프라에 대한 자본 유입이 계속되고 있음을 보여줍니다. 남미는 여전히 규모가 훨씬 작으며, 이 지역에서의 활동은 주로 브라질의 바이오시밀러 개발에 대한 의지나 아르헨티나의 CRO 거점 확대와 관련이 있지만, GMP 등급의 은행 인프라가 제한적이기 때문에 수요의 대부분은 연구용 등급의 이용에 그치고 있습니다.

유럽은 성숙한 제약·바이오기술 기반과 일관된 규제 체계를 갖추고 있어, 불멸화 세포주 시장에 안정적인 수요를 제공합니다. 셀비에(Servier)사는 2024년 11월, 8,600만 유로를 투자해 프랑스에 바이오 생산 시설 ‘Bio-S’를 개설하고, 포유류 연속 배양 세포주를 활용한 임상용 바이오의약품 생산을 지원했습니다. 또한, 이 지역에서는 첨단 의료 제품에 관한 GMP 지침 개정안에 따라 공정 관련 요구 사항이 더욱 엄격해질 전망이며, 이에 따라 불멸화 세포주를 사용하는 제조업체에 대한 규정 준수 기준이 강화될 것입니다. 중동 및 아프리카는 아직 초기 단계에 있지만, GCC 국가들의 의료 서비스 현대화와 WuXi Biologics가 카타르 자유무역지역청과 체결한 2025년 양해각서는 이 지역에서 제조 분야에 대한 관심이 조기에 높아지고 있음을 보여줍니다.

아시아태평양은 불멸화 세포주 시장에서 가장 빠르게 성장하고 있는 지역 블록으로, 2031년까지 연평균 성장률(CAGR) 8.9%로 확대될 것으로 전망됩니다. 중국은 그 성장 스토리의 가장 큰 원동력이며, 공공 R&D 지출, 리포지토리 구축, CDMO 확대가 모두 동시에 진행되고 있기 때문입니다. 국립줄기세포자원센터는 2025년을 목표로 불멸화된 인간 세포주의 공유 저장소를 적극적으로 구축하고 있으며, 이는 학술적 활용과 장기적인 생태계 심화 모두를 뒷받침하고 있습니다. 또한, WuXi Biologics는 2025년에 전년 대비 16.7%의 매출 성장을 기록했으며, 사상 최대인 209건의 신규 통합 프로젝트를 추가했습니다. 이는 해당 지역의 제조업 성장세를 보여줍니다. PackGene Biotech가 2025년 10월에 독자적인 HEK293 세포 뱅크 2건에 대해 FDA에 의약품 마스터 파일(DMF)을 신청한 점도 중요합니다. 이는 중국의 세포주 자산을 미국의 유전자 치료 규제 절차에 따라 직접적으로 규정하기 때문입니다. 인도에서도 업스트림 생산 인프라는 여전히 발전 초기 단계에 있지만, 생명공학 활동의 확대와 아웃소싱 수요 증가를 통해 불멸화 세포주 시장에 대한 하류 수요가 점차 형성되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the immortalized cell line market size is projected to expand from USD 5.12 billion in 2025 and USD 5.52 billion in 2026 to USD 8.04 billion by 2031, registering a CAGR of 7.82% between 2026 to 2031.

This report is Segmented by Product Type (Human, Animal), Immortalization Method (Viral-Mediated, HTERT-Mediated, and More), Application (Drug Discovery and Development, Toxicity Testing, and More), End User (Pharma/Biotech Companies, Academic/Research Institutes, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Immortalized Cell Line Market Trends and Insights

Biologics and Viral Vector Pipeline Expansion

The immortalized cell line market is benefiting from the widening need for continuously passaging GMP-qualified substrates across biologics and gene therapy production programs. Mammalian continuous cell lines, especially CHO and HEK293 derivatives, remain central to approved recombinant protein production, while HEK293-derived systems are also critical for AAV and lentiviral vector manufacturing. Lonza's May 2026 launch of the Xcite AAV stable producer cell line platform showed a 10-fold to 15-fold increase in AAV titer versus transient transfection and pointed to a cost-of-goods reduction of 80% or more, which shows how quickly stable producer formats are moving into commercial use. That performance matters because high-dose neurological programs have often pushed transient systems beyond workable cost limits. As stable-cell-line AAV production becomes more practical, the immortalized cell line market is seeing stronger demand for qualified producer lines, cell banking, and analytical support. This shift also favors suppliers that can connect upstream cell line design with downstream manufacturing documentation in one platform.

Drug Discovery and Toxicity-Screening Intensity

The immortalized cell line market continues to draw support from high-throughput screening, where continuous lines remain the standard base for repeatable assay performance. More complex assay formats such as 3D spheroids, organoid co-cultures, and organ-on-a-chip systems still depend on cell lines that can hold stable behavior over longer experimental windows. Merck KGaA's October 2025 partnership with Promega, built on the company's earlier acquisition of HUB Organoids, shows that suppliers are investing in assay systems that place immortalized lines inside more advanced screening environments rather than replacing them. The FDA's April 2026 draft guidance on safety assessment for genome editing in human gene therapy products also increases the need for validated cell-based potency and functional assays across development programs. That requirement expands the number of authenticated human cell models needed per program. The immortalized cell line market therefore gains not only from higher research volume, but also from stricter validation expectations built into modern drug development pathways.

High Development, Validation, and QC Costs

The immortalized cell line market still faces a clear restraint in the cost of moving a line from research use into GMP-qualified production use. That process requires STR profiling, mycoplasma testing, adventitious agent screening, viral safety evaluation, karyotyping, and stability assessment, which extends both timelines and budgets for each program. The need to show genetic stability from the master cell bank through the end-of-production cell window raises the burden further for developers with several early-stage assets. Smaller biotechs often respond by delaying full characterization or by relying on CDMOs that already hold validated parental lines. That dependence shifts pricing power toward integrated service providers and reduces flexibility for firms that want to own their full cell line development path. It also limits the pace at which new entrants can scale in the immortalized cell line market.

Other drivers and restraints analyzed in the detailed report include:

- CRISPR-Engineered Disease Models

- Authentication and Traceability Mandates

- Biosafety and Donor-Traceability Scrutiny

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Human cell lines held 55.3% of revenue in 2025, and that made them the largest product category in the immortalized cell line market. The same segment is also projected to expand at an 8.4% CAGR through 2031, which means its growth is being driven by structural demand rather than by a short-term mix shift from animal lines. Human lines stay central because they model human disease biology more directly, support human-relevant antibody work, and serve as viral vector substrates in gene therapy programs. HEK293, HeLa, and Jurkat lines remain widely used across oncology, toxicology, and vector production workflows. This breadth keeps the human line segment at the center of procurement decisions across the immortalized cell line industry.

Engineered derivatives are gaining more commercial weight within this segment because they support tighter batch consistency and more application-specific use cases. A 2025 study in Stem Cell Research & Therapy reported consistent batch-to-batch extracellular vesicle profiles from hTERT-immortalized MSC lines, which supports their use in therapeutic EV platforms. Animal cell lines still retain an essential role, especially CHO for recombinant protein production and Vero or BHK-21 for established vaccine and research workflows. At the same time, the spread of bovine, equine, and other species-specific lines into cultivated meat and veterinary applications is expanding the reachable demand pool for the immortalized cell line market. Regulatory testing demands for animal-derived lines also favor suppliers that already operate established biosafety and characterization laboratories.

Viral-mediated immortalization accounted for 40.2% of revenue in 2025, which kept it as the largest method segment in the immortalized cell line market. Its large installed base reflects decades of use with SV40, HPV E6/E7, and adenoviral tools for generating highly proliferative research lines. The method also holds a stable demand floor because vaccine production substrates such as Vero and MDCK remain tied to long-established processes. Even so, hTERT-mediated immortalization is projected to grow at an 8.5% CAGR through 2031, making it the fastest-growing method segment. That faster growth reflects a stronger safety profile because hTERT extends replicative lifespan without the same disruption of p53 or pRB pathways associated with viral oncoproteins.

The NIST study published in 2025 strengthened this direction by showing that precision hTERT knock-in can produce immortalized primary human CD8+ T cells with stable karyotype and preserved immunologic features. Hybridoma fusion remains relevant in legacy monoclonal antibody workflows and in polyclonal antibody generation, even though recombinant platforms continue to take share. Spontaneous and chemical immortalization methods stay niche, but they are drawing attention in food biotechnology where non-GMO positioning carries regulatory weight in some jurisdictions. For buyers across the immortalized cell line industry, the choice of method now reflects a clearer tradeoff between historical robustness, safety profile, and downstream regulatory burden.

Geography Analysis

North America accounted for 38.2% of global revenue in 2025, which gave the region the largest share of the immortalized cell line market size. The region holds this lead because it combines dense biopharmaceutical R&D activity with a mature network of GMP-grade cell banking facilities and a regulatory system that expects detailed cell substrate characterization. The FDA's April 2026 draft guidance on genome editing safety assessment adds to that demand because it places greater weight on authenticated and characterized cell-based assays during development. GI Partners' formation of Rose BioSolutions in May 2026 from Charles River's divested CDMO and Cell Solutions businesses also showed that capital continues to flow into North American cell solutions infrastructure. South America remains much smaller, and activity there is tied mainly to Brazil's biosimilar ambitions and Argentina's growing CRO base, while limited GMP-grade banking infrastructure keeps most demand closer to research-grade use.

Europe provides steady demand for the immortalized cell line market because it has a mature pharmaceutical and biotechnology base and a consistent regulatory framework. Servier inaugurated its Bio-S bioproduction unit in France in November 2024 with an investment of EUR 86 million, which supported clinical biologics production using mammalian continuous cell lines. The region is also facing tighter process expectations through proposed revisions to GMP guidance for advanced therapy medicinal products, which would raise compliance standards for manufacturers using immortalized substrates. The Middle East and Africa is still at an early stage, but healthcare modernization in the GCC and WuXi Biologics' 2025 memorandum with Qatar Free Zones Authority indicate an early buildout of regional manufacturing interest.

Asia-Pacific is the fastest-growing regional block in the immortalized cell line market and is projected to expand at an 8.9% CAGR through 2031. China is the largest force inside that growth story because public R&D spending, repository building, and CDMO expansion are all moving at the same time. The National Stem Cell Resource Center was actively building shared repositories of immortalized human cell lines in 2025, which supports both academic use and long-term ecosystem depth. WuXi Biologics also reported 16.7% year-on-year revenue growth in 2025 and added a record 209 new integrated projects, which shows the scale of manufacturing momentum in the region. PackGene Biotech's October 2025 filing of FDA Drug Master Files for 2 proprietary HEK293 cell banks is also important because it places Chinese cell line assets more directly within the U.S. gene therapy regulatory path. India is also building downstream demand for the immortalized cell line market through growth in biotech activity and outsourcing demand, even though upstream production infrastructure remains earlier in its development curve.

- ATCC

- AcceGen

- Applied Biological Materials Inc.

- Cell Biolabs

- Charles River

- Coriell Institute for Medical Research

- Creative Bioarray

- Creative Biolabs

- Innoprot

- InSCREENeX GmbH

- KBI Biopharma (Selexis)

- Leibniz Institute DSMZ

- Lonza Group

- Merck

- PromoCell

- Sartorius

- Stem Cell Technologies

- Thermo Fisher Scientific

- WuXi App Tec

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Biologics and Viral Vector Pipeline Expansion

- 4.2.2 Drug Discovery and Toxicity-Screening Intensity

- 4.2.3 CRISPR-Engineered Disease Models

- 4.2.4 Authentication and Traceability Mandates

- 4.2.5 Cultivated Meat and Non-Therapeutic Cell Demand

- 4.3 Market Restraints

- 4.3.1 High Development, Validation, and QC Costs

- 4.3.2 Biosafety and Donor-Traceability Scrutiny

- 4.3.3 Misidentification, Contamination, and Genetic Drift

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of new entrants

- 4.7.2 Bargaining power of suppliers

- 4.7.3 Bargaining power of buyers

- 4.7.4 Threat of substitutes

- 4.7.5 Competitive rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Human Cell Lines

- 5.1.2 Animal Cell Lines

- 5.2 By Immortalization Method

- 5.2.1 Viral-mediated Immortalization

- 5.2.2 hTERT-mediated Immortalization

- 5.2.3 Hybridoma Fusion

- 5.2.4 Spontaneous and Chemical Immortalization

- 5.3 By Application

- 5.3.1 Drug Discovery and Development

- 5.3.2 Toxicity Testing

- 5.3.3 Cancer Research

- 5.3.4 Biologics Manufacturing

- 5.3.5 Vaccine Development

- 5.3.6 Gene and Cell Therapy Research

- 5.4 By End User

- 5.4.1 Pharmaceutical and Biotechnology Companies

- 5.4.2 Academic and Research Institutes

- 5.4.3 CROs and CDMOs

- 5.4.4 Diagnostic Laboratories

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 ATCC

- 6.3.2 AcceGen

- 6.3.3 Applied Biological Materials Inc.

- 6.3.4 Cell Biolabs, Inc.

- 6.3.5 Charles River Laboratories

- 6.3.6 Coriell Institute for Medical Research

- 6.3.7 Creative Bioarray

- 6.3.8 Creative Biolabs

- 6.3.9 Innoprot

- 6.3.10 InSCREENeX GmbH

- 6.3.11 KBI Biopharma (Selexis)

- 6.3.12 Leibniz Institute DSMZ

- 6.3.13 Lonza Group

- 6.3.14 Merck KGaA

- 6.3.15 PromoCell GmbH

- 6.3.16 Sartorius AG

- 6.3.17 STEMCELL Technologies

- 6.3.18 Thermo Fisher Scientific

- 6.3.19 WuXi AppTec

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment