|

시장보고서

상품코드

2064437

무선 디스플레이 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Wireless Display - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

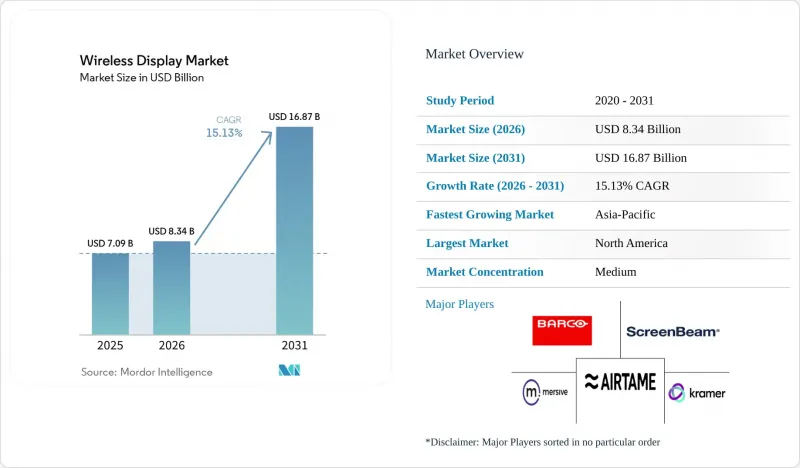

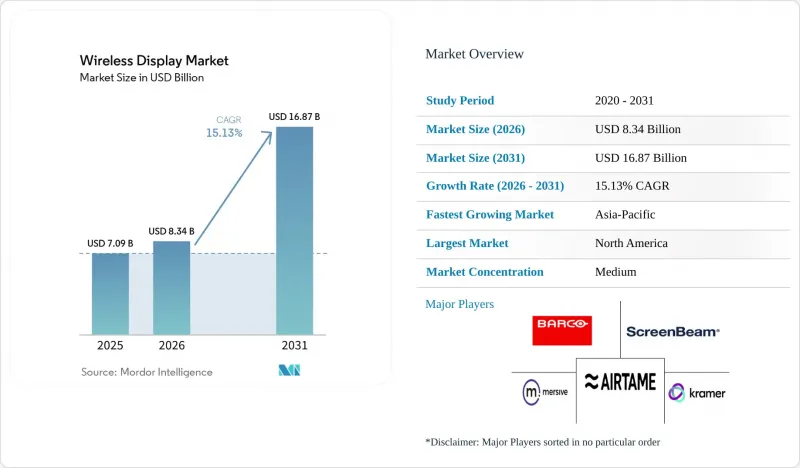

Mordor Intelligence에 의하면, 무선 디스플레이 시장 규모는 2025년에 70억 9,000만 달러로 평가되었고, 2026년 83억 4,000만 달러로 추정되고, 2031년까지 168억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 15.13%를 나타낼 전망입니다.

본 보고서는 제공 형태별(하드웨어, 소프트웨어 및 서비스), 기술 프로토콜별(AirPlay, Miracast, Google Cast, 무선 HDMI 및 무선 HD, 기타), 최종 사용자별(주거용, 상업시설), 용도별(소비자용 엔터테인먼트 및 스트리밍, 기업용 프레젠테이션 및 협업, 교육 및 훈련, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 무선 디스플레이 시장 동향 및 인사이트

하이브리드 근무와 BYOD 도입이 기업의 무선 인프라를 재구축하고 있습니다.

상시적인 하이브리드 근무 방식의 도입으로 인해 회의실에서는 고정된 컴퓨터가 아닌 다수의 개인용 기기를 지원해야 할 필요가 생기면서, 무선 디스플레이 시장은 기업의 업무 흐름에 더욱 깊이 스며들고 있습니다. 시스코가 2025년 11월 30개 시장을 대상으로 실시한 조사에 따르면, 무선 부문 리더의 55%가 무선 네트워크에 대한 의존도가 높아지고 있는 주된 원인으로 BYOD(개인 기기 사용)와 사용자의 이동성을 꼽았습니다. 이 조사에 따르면, 조사 전 5년 동안 80%의 조직이 무선 인프라에 대한 지출을 늘린 것으로 나타났으며, 이는 이러한 수요가 단기적인 회의실 업그레이드가 아닌 장기적인 네트워크 투자와 관련이 있음을 보여줍니다. 따라서 기업들은 다양한 기기가 혼재되어 심각한 호환성 문제를 야기하기 때문에 하나의 회의실에서 AirPlay, Miracast, Google Cast를 모두 지원하는 시스템에 대해 더 높은 단가를 기꺼이 지불하고 있습니다. 또한, 기기 관리, 분석, 구독 기반 지원이 기업의 표준 구매 항목으로 자리 잡아가고 있어, 이러한 변화로 인해 수익은 소프트웨어 및 서비스 쪽으로 이동하고 있습니다.

Wi-Fi 6E 및 인프라 업그레이드를 통한 지연 한계 해소

Wi-Fi 6E가 미국에서 1,200 MHz의 비면허 6GHz 대역에 대한 접속을 제공하며, 이후 주요 국가 및 지역에서 지원이 확대됨에 따라 무선 디스플레이 시장은 액세스 포인트의 교체 주기가 연장되는 혜택을 누리고 있습니다. 시스코는 2025년 하반기 자사의 관리 네트워크 전반에 걸쳐 Wi-Fi 6E 및 Wi-Fi 7 액세스 포인트 도입 건수가 전년 대비 23% 증가했다고 보고했으며, 이는 기업들의 전환이 이미 상당한 규모로 진행 중임을 보여줍니다. 또한, 2025년에는 관리 대상 네트워크 500만 개 전체에서 6GHz 클라이언트 활성화 건수가 전년 대비 60% 증가한 것으로 보고되었으며, 이는 고급 캐스트 이용 사례에 대한 엔드포인트의 준비 태세가 강화되고 있음을 보여줍니다. 기존 5GHz 방식 도입 시에는 밀집된 교실이나 사무실 환경에서 운영에 어려움을 겪는 경우가 많았으나, 6GHz의 대역폭 덕분에 여러 소스로부터의 고해상도 공유 환경이 개선됩니다. 3-4년 주기로 액세스 포인트를 교체하는 기업들은 2026-2029년에 걸쳐 진행될 이 네트워크 전환에 맞추어 무선 프레젠테이션 장비를 구매할 가능성이 높으며, 이는 예측 기간 동안의 단위 수요를 뒷받침할 것입니다.

프로토콜의 세분화가 기업의 조달 결정을 복잡하게 만듭니다.

AirPlay, Miracast, Google Cast 및 독자적인 프로토콜이 혼재된 기기 환경 전반에서 일관된 사용자 경험을 제공하지 못하기 때문에 무선 디스플레이 시장은 여전히 심각한 상호 운용성 문제에 직면해 있습니다. 구매자는 멀티 프로토콜을 지원하는 하드웨어에 고액을 지불하거나, 공용 공간에서 사용자에게 불편을 주는 호환성 문제를 감수하는 것 중 하나를 선택할 수밖에 없습니다. 규제가 엄격한 환경에서는 단순한 화면 공유와 마찬가지로 보안 설계가 중요시되게 되었기 때문에 이 문제는 더욱 심각해지고 있습니다. 2026년 3월 Cloud Security Alliance가 발표한 조사 보고서에 따르면, WPA2 및 WPA3 네트워크 모두에 영향을 미치는 Wi-Fi 클라이언트 분리 취약점이 확인되었습니다. 이는 IEEE 802.11 표준 자체에서 기인한 것으로, 공급업체가 패치를 적용하는 것만으로는 위험을 완전히 제거할 수 없음을 의미합니다. 프로토콜이 복잡해지고 보안 검토가 동시에 이루어지면 조달 승인 주기가 길어지며, 일부 조직에서는 보다 적절한 일관성이 확보될 때까지 업데이트 결정을 미루고 있습니다.

부문별 분석

2025년, 무선 디스플레이 시장 규모의 54.32%를 하드웨어가 차지했습니다. 이는 가정이나 상업시설에 널리 도입된 어댑터, 통합형 프레젠테이션 시스템, 임베디드 모듈과 같은 대규모 도입 기반에 힘입은 결과입니다. 이러한 우위는 무선 디스플레이 산업에서 지금까지의 투자가 물리적 회의실용 하드웨어나 디스플레이 단말기에 얼마나 집중되어 왔는지를 여전히 반영하고 있습니다. 많은 구매자들이 여러 사용자 간에 신뢰할 수 있는 캐스팅을 지원하기 위해 여전히 전용 수신기, 스마트 회의실 기기 또는 디스플레이 통합형 모듈을 필요로 하고 있기 때문에 이 부문은 계속해서 중요한 위치를 차지하고 있습니다. 동시에, 기업 구매자들이 단일 기능의 동글보다는 회의실 제어, 기기 연결, 클라우드 관리를 결합한 번들형 시스템을 선호하는 추세에 따라 하드웨어 수요의 구성도 변화하고 있습니다.

소프트웨어 및 서비스 부문은 2026-2031년 연평균 성장률(CAGR) 15.53%를 나타낼 것으로 예측되며, 무선 디스플레이 시장에서 가장 빠르게 성장하는 부문이 될 것입니다. 이러한 성장은 기업이 이용 정책 및 기기군의 성능을 관리하는 데 도움이 되는 구독형 화면 공유, 기기 관리, 분석 플랫폼과 밀접한 관련이 있습니다. Airtame는 2025년 12월, Wi-Fi 6E 칩셋을 탑재한 ‘Airtame 3’를 발표했습니다. 라이선싱 모델은 핵심 기능의 경우 대당 연간 120달러, 풀 하이브리드 회의 기능의 경우 대당 연간 300달러로 책정되어 있어, 제품 스택에 지속적인 수익이 반영되어 있음을 보여줍니다. 매니지드 서비스 분야에서도 확장 여지가 있습니다. 다중 벤더 환경 도입 및 제로 트러스트 통합을 담당하는 IT 팀은 펌웨어 관리, 보안 대책, 지속적인 운영 관리와 관련해 외부 지원을 선호할 가능성이 있기 때문입니다.

2025년 기준으로 AirPlay는 무선 디스플레이 시장에서 32.56%의 점유율을 차지했습니다. 이는 Apple 기기가 이미 iPhone, iPad, MacBook 사용자를 아우르는 성숙한 네이티브 생태계를 통해 화면 미러링을 구현하고 있기 때문입니다. 이러한 도입 기반을 바탕으로 AirPlay는 Apple 기기가 널리 보급된 가정 및 업무 환경 모두에서 우위를 점했습니다. 한편, Miracast는 기업, 교육 기관, 공공기관에서 Windows 기반 단말기들이 여전히 중요한 역할을 하고 있기 때문에 상용 환경에서 입지를 유지하고 있습니다. Wireless HDMI와 WirelessHD는 프로토콜의 폭넓은 유연성보다는 처리량을 중시하는 제한적인 요구 사항에 계속 대응하고 있는 반면, Intel WiDi는 구형 단말기의 사용이 줄어들면서 그 중요성을 점차 잃어가고 있습니다.

Google Cast는 2026년부터 2031년까지 연평균 성장률(CAGR) 16.33%를 나타낼 것으로 예측되며, 이에 따라 무선 디스플레이 시장에서 가장 빠르게 성장하는 프로토콜 그룹이 될 것입니다. 이러한 성장세는 안드로이드와 크롬 OS의 긴밀한 통합은 물론, 구글 인증 TV 및 회의실용 하드웨어에서의 활용 확대에 기인합니다. 이러한 상황으로 인해 구매자들은 회의실을 단일 디바이스 생태계에 얽매이지 않고, 단일 엔드포인트에서 여러 프로토콜을 지원하는 소프트웨어 정의형 수신기로 전환하고 있습니다. 이러한 방향성은 중요합니다. 이는 구매자들이 프로토콜 전용 회의실용 하드웨어보다는 폭넓은 호환성, 정책 제어, 그리고 더욱 간편한 도입을 점점 더 요구하고 있기 때문입니다.

지역별 분석

2025년, 북미는 무선 디스플레이 시장 점유율의 34.58%를 차지하며 최대 지역 시장이 되었습니다. 이 지역은 성숙한 기업의 무선 인프라, 교육 부문의 활발한 기기 교체 주기, 그리고 다수의 플랫폼 공급업체 및 솔루션 통합업체의 존재라는 이점을 누렸습니다. 상용 노트북에 USB-C가 보급됨에 따라, 2025년까지 케이블이 필요 없는 회의실 업무 흐름에 대한 실질적인 장벽이 해소되어, 무선 프레젠테이션을 대규모로 지원하는 것이 쉬워졌습니다. 교육 분야의 FERPA나 의료 분야의 HIPAA와 같은 규정 준수 규칙 역시, 기관의 구매 과정에서 정책 관리와 보안이 중요한 고려 사항이었기 때문에 소비자용 제품보다 엔터프라이즈급 시스템을 선호하는 요인이 되었습니다. Crestron은 2026년 1월, AI 지원형 회의실 구축을 위해 NPU가 통합된 Intel Core Ultra 프로세서를 탑재한 협업 하드웨어 코어 ‘Collab Compute’를 도입하며, 이러한 방향성을 한층 더 강화했습니다.

아시아태평양은 2026-2031년 연평균 성장률(CAGR) 16.04%를 기록하며 성장할 것으로 예상되며, 무선 디스플레이 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 수요는 중국과 인도에서의 스마트 교실 도입, 새로운 기업 캠퍼스 건설, 주요 아시아태평양 시장에서의 6GHz 대역 승인 절차가 빠르게 진행되고 있는 데 힘입어 뒷받침되고 있습니다. 이러한 지역적 경향은 북미와 달리, 새로운 교육 기관이나 공공 기관의 프로젝트에서는 기존의 유선 시스템을 대체하는 대신 무선 방식의 회의실 연결을 기본 표준으로 채택할 수 있기 때문입니다. 또한 한국, 일본, 호주 역시 Wi-Fi 6E로의 규제 측면에서의 광범위한 전환으로 인한 혜택을 누리고 있으며, 이를 통해 액세스 포인트 업그레이드와 무선 프레젠테이션 기기 구매를 연계하기가 쉬워졌습니다.

유럽은 성숙 단계에 접어들었음에도 지속적으로 혁신이 이루어지고 있는 무선 디스플레이 시장이며, 영국과 독일이 기업 수요의 주요 중심지입니다. EU 내 주파수 대역의 조화를 통해 Wi-Fi 6E 도입 시 북미와의 시차 차이가 줄어들었고, 차세대 캐스트 인프라 구축 환경이 개선되었습니다. 벨기에에 본사를 둔 Barco는 2024년에 9억 4,700만 유로(10억 2,465만 달러 상당)의 매출을 기록했으며, 2025년 6월에는 Microsoft의 Device Ecosystem Platform에서 ClickShare Hub를 출시함으로써 해당 지역에서의 입지를 공고히 했습니다. 중동 및 아프리카는 여전히 기여도가 가장 낮은 편이지만, 아랍에미리트와 사우디아라비아의 스마트 빌딩 프로그램의 혜택을 받고 있습니다. 한편, 남미 지역은 여전히 초기 단계에 있지만, 부동산 투자가 안정화되는 가운데 브라질과 아르헨티나가 상업적 도입을 주도하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the wireless display market size was valued at USD 7.09 billion in 2025 and estimated to grow from USD 8.34 billion in 2026 to reach USD 16.87 billion by 2031, at a CAGR of 15.13% during the forecast period (2026-2031).

This report is Segmented by Offering (Hardware, and Software and Services), Technology Protocol (AirPlay, Miracast, Google Cast, Wireless HDMI and Wireless HD, and More), End-User (Residential, and Commercial), Application (Consumer Entertainment and Streaming, Enterprise Presentation and Collaboration, Education and Training, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Wireless Display Market Trends and Insights

Hybrid Work and BYOD Adoption Reshaping Enterprise Wireless Infrastructure

Permanent hybrid work arrangements have pushed the wireless display market deeper into enterprise workflows, as meeting rooms now need to support many personal devices rather than a fixed room computer. Cisco reported that 55% of wireless leaders cited BYOD and user mobility as the main drivers of rising dependence on wireless networks in its November 2025 survey across 30 markets. The same study found that 80% of organizations increased wireless infrastructure spending over the five years before the survey, indicating that this demand is tied to long-term network investment rather than short-term room upgrades. Enterprises are therefore accepting higher unit costs for systems that can support AirPlay, Miracast, and Google Cast in a single room because mixed device fleets create a real compatibility problem. This change is also shifting revenue toward software and services because device management, analytics, and subscription support are becoming part of the standard enterprise purchase.

Wi-Fi 6E And Infrastructure Upgrades Removing The Latency Ceiling

The wireless display market is benefiting from a broader access point refresh cycle, as Wi-Fi 6E provides access to 1,200 MHz of unlicensed 6 GHz spectrum in the United States and has since gained support across several major countries and regions. Cisco recorded a 23% year-over-year increase in Wi-Fi 6E and Wi-Fi 7 access point deployments across its managed networks in the second half of 2025, indicating that enterprise migration is already underway at a meaningful scale. It also reported a 60% year-over-year increase in 6 GHz clients activated across 5 million managed networks in 2025, indicating stronger endpoint readiness for advanced casting use cases. Earlier 5 GHz deployments often struggled in dense classrooms and office environments, but 6 GHz capacity improves conditions for multi-source, high-resolution sharing. Enterprises that refresh access points on three-to-four-year cycles are likely to align wireless presentation purchases with this network transition between 2026 and 2029, which supports unit demand during the forecast window.

Protocol Fragmentation Complicating Enterprise Procurement Decisions

The wireless display market still faces a real interoperability problem because AirPlay, Miracast, Google Cast, and proprietary stacks do not deliver a consistent experience across mixed device fleets. Buyers can either pay a higher price for multi-protocol hardware or accept compatibility gaps that frustrate users in shared rooms. This issue becomes harder in regulated environments because security design now matters as much as simple screen sharing. A March 2026 research note from the Cloud Security Alliance identified vulnerabilities in Wi-Fi client isolation that affect both WPA2 and WPA3 networks and stem from the IEEE 802.11 standard itself, meaning vendor patching alone does not fully eliminate the risk. When protocol complexity and security reviews occur simultaneously, procurement approval cycles lengthen, and some organizations delay refresh decisions until better alignment emerges.

Other drivers and restraints analyzed in the detailed report include:

- Smart TV and Interactive Flat Panel Expansion Creating Embedded Display Demand

- Classroom and Meeting Room Digitalization Programs Sustaining Structural Demand

- Wired Connectivity Retaining a Performance Advantage in Bandwidth-Intensive Applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware retained 54.32% of the wireless display market size in 2025, supported by the large installed base of adapters, integrated presentation systems, and embedded modules across homes and commercial venues. That lead still reflects how much prior spending in the wireless display industry went into physical room hardware and display endpoints. The segment remains important because many buyers still need dedicated receivers, smart meeting room devices, or display-integrated modules to support reliable casting across multiple users. At the same time, the composition of hardware demand is changing as enterprise buyers prefer bundled systems that combine room control, device connectivity, and cloud administration instead of single-function dongles.

Software and services are projected to grow at a 15.53% CAGR from 2026 to 2031, making it the fastest-growing segment of the wireless display market. This growth is tied to subscription-based screen-sharing, device-management, and analytics platforms that help enterprises manage usage policies and fleet performance. Airtame introduced Airtame 3 in December 2025 with a Wi-Fi 6E chipset and a licensing model priced at USD 120 per device per year for core features and USD 300 per device per year for full hybrid conferencing, demonstrating how recurring revenue is built into the product stack. Managed services also have room to expand, as IT teams handling multi-vendor deployments and zero-trust integration may prefer external support for firmware management, security policy, and ongoing administration.

AirPlay held 32.56% share of the wireless display market in 2025 because Apple devices already route screen mirroring through a mature native ecosystem across iPhone, iPad, and MacBook users. That installed base gave AirPlay an advantage in both residential use and business settings where Apple endpoints are common. Miracast still keeps a place in commercial environments because Windows-based fleets remain important across enterprise, education, and public institutions. Wireless HDMI and WirelessHD continue to serve narrower needs where throughput matters more than broad protocol flexibility, while Intel WiDi keeps losing relevance as legacy endpoints cycle out of use.

Google Cast is forecast to grow at a 16.33% CAGR from 2026 to 2031, which makes it the fastest-growing protocol group in the wireless display market. Its momentum comes from deep integration across Android and Chrome OS, as well as wider availability on Google-certified TVs and meeting room hardware. These conditions are pushing buyers toward software-defined receivers that support multiple protocols from a single endpoint, rather than forcing a room to rely on a single device ecosystem. That direction matters because buyers increasingly want broad compatibility, policy control, and simpler deployment instead of protocol-specific room hardware.

Geography Analysis

North America held 34.58% of the wireless display market share in 2025, making it the largest regional market. The region benefited from mature enterprise wireless infrastructure, active device refresh cycles in education, and the presence of many platform vendors and solution integrators. USB-C adoption across commercial notebooks removed a practical barrier to cable-free room workflows by 2025, which made wireless presentation easier to support at scale. Compliance rules such as FERPA in education and HIPAA in healthcare also favored enterprise-grade systems over consumer-grade products, as policy control and security were key considerations in institutional buying. Crestron reinforced this direction in January 2026, when it introduced Collab Compute, a collaboration hardware core built on an Intel Core Ultra processor with an integrated NPU for AI-assisted meeting room deployments.

Asia-Pacific is projected to grow at a 16.04% CAGR from 2026 to 2031, making it the fastest-growing region in the wireless display market. Demand is being supported by smart classroom rollouts in China and India, new corporate campus construction, and the rapid pace of 6 GHz authorization across major APAC markets. This regional pattern differs from North America because greenfield education and institutional projects can adopt wireless room connectivity as the default standard instead of replacing legacy wired systems. South Korea, Japan, and Australia also benefit from the wider regulatory shift toward Wi-Fi 6E, which helps align access point upgrades with wireless presentation purchases.

Europe remains a mature yet continually refreshing wireless display market, with the United Kingdom and Germany as key centers of enterprise demand. The EU's spectrum harmonization reduced the timing gap with North America for Wi-Fi 6E deployment, which improved the conditions for next-generation casting infrastructure. Barco, headquartered in Belgium, reported EUR 947 million in sales in 2024, equivalent to USD 1,024.65 million, and strengthened its regional position in June 2025 with the launch of ClickShare Hub on Microsoft's Device Ecosystem Platform. The Middle East and Africa remain the smallest contributors but are benefiting from smart building programs in the UAE and Saudi Arabia, while South America is still at an early stage, with Brazil and Argentina leading commercial adoption as real estate investment stabilizes.

- Barco NV

- Airtame ApS

- ScreenBeam Inc.

- Mersive Technologies, Inc.

- Kramer Electronics Ltd.

- WolfVision GmbH

- Kindermann GmbH

- Crestron Electronics, Inc.

- RGB Systems, Inc. dba Extron Electronics

- TEKVOX, Inc.

- SMART Technologies ULC

- Promethean Limited

- Legamaster International B.V.

- Squirrels LLC

- Splashtop Inc.

- DisplayNote Technologies Limited

- Avocor Technologies

- Yealink Network Technology Co., Ltd.

- Vivitek Corporation

- Newline Interactive Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hybrid Work and BYOD Collaboration Normalization

- 4.2.2 Rising Installed Base of Smart TVs, Interactive Flat Panels, and Connected Projectors

- 4.2.3 Wi-Fi 6, Wi-Fi 6E, and 5G Upgrades Improving Low-Latency Casting

- 4.2.4 Classroom and Meeting Room Digitalization Programs

- 4.2.5 USB-C Laptop Transition Accelerating Demand for Cable-Free Room Workflows

- 4.2.6 Security-Certified Native Casting and Guest Network Segmentation Becoming Procurement Differentiators

- 4.3 Market Restraints

- 4.3.1 Protocol Fragmentation Across AirPlay, Miracast, Google Cast, and Proprietary Stacks

- 4.3.2 HDMI and USB-C Cable Reliability Still Outperform Wireless in High-Bandwidth Use Cases

- 4.3.3 Smart TV Native Casting Reducing Incremental Demand for Standalone Receivers in Consumer Settings

- 4.3.4 Enterprise RF Congestion and Zero-Trust Network Policies Extending Deployment Cycles

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.1.1 Wireless Display Adapters and Dongles

- 5.1.1.2 Integrated Wireless Presentation Systems

- 5.1.1.3 Embedded Wireless Display in Smart TVs and Interactive Flat Panels

- 5.1.2 Software and Services

- 5.1.2.1 Screen Mirroring and Casting Software

- 5.1.2.2 Device Management and Analytics Software

- 5.1.1 Hardware

- 5.2 By Technology Protocol

- 5.2.1 Professional and Managed Services

- 5.2.2 AirPlay

- 5.2.3 Miracast

- 5.2.4 Google Cast

- 5.2.5 Wireless HDMI and WirelessHD

- 5.2.6 Intel WiDi Legacy Installed Base

- 5.2.7 Other Technology Protocols

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.4 By Application

- 5.4.1 Consumer Entertainment and Streaming

- 5.4.2 Enterprise Presentation and Collaboration

- 5.4.3 Education and Training

- 5.4.4 Healthcare Visualization and Collaboration

- 5.4.5 Digital Signage and Public Information

- 5.4.6 Government and Defense

- 5.4.7 Industrial and Control Room Visualization

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Spain

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Barco NV

- 6.4.2 Airtame ApS

- 6.4.3 ScreenBeam Inc.

- 6.4.4 Mersive Technologies, Inc.

- 6.4.5 Kramer Electronics Ltd.

- 6.4.6 WolfVision GmbH

- 6.4.7 Kindermann GmbH

- 6.4.8 Crestron Electronics, Inc.

- 6.4.9 RGB Systems, Inc. dba Extron Electronics

- 6.4.10 TEKVOX, Inc.

- 6.4.11 SMART Technologies ULC

- 6.4.12 Promethean Limited

- 6.4.13 Legamaster International B.V.

- 6.4.14 Squirrels LLC

- 6.4.15 Splashtop Inc.

- 6.4.16 DisplayNote Technologies Limited

- 6.4.17 Avocor Technologies

- 6.4.18 Yealink Network Technology Co., Ltd.

- 6.4.19 Vivitek Corporation

- 6.4.20 Newline Interactive Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment