|

시장보고서

상품코드

2064440

에어쿠션 포장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Air Cushion Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

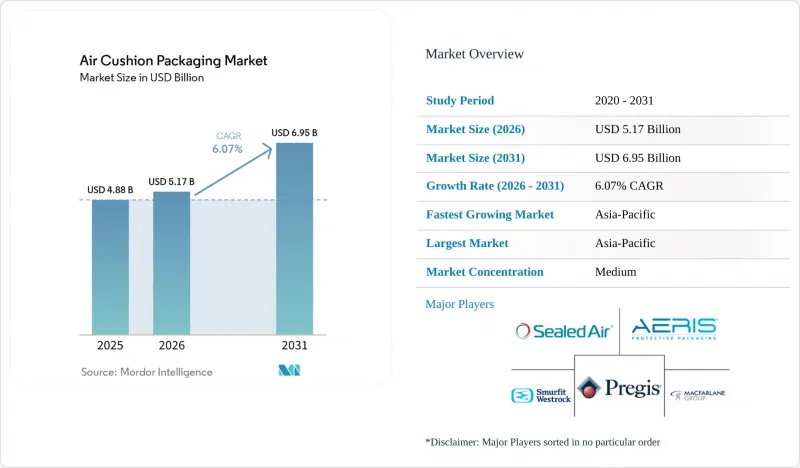

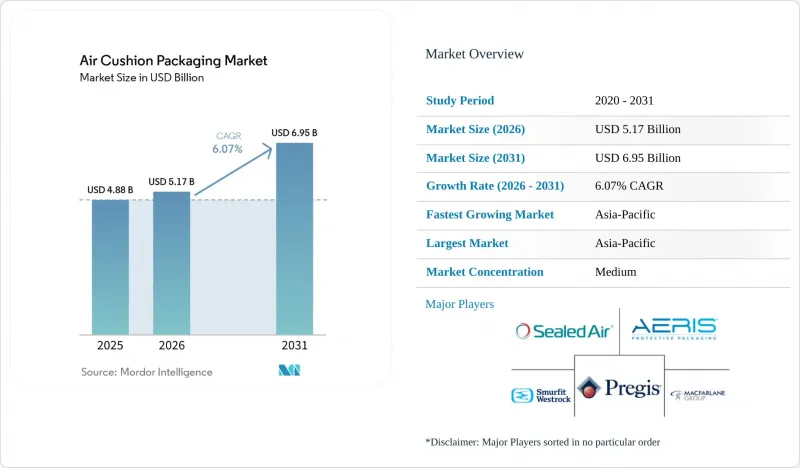

Mordor Intelligence에 의하면, 에어쿠션 포장 시장 규모는 2025년 48억 8,000만 달러로 평가되었습니다. 2026년에는 51억 7,000만 달러로 확대되어 2026-2031년 CAGR은 6.07%를 나타내, 2031년까지 69억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(에어 필로우, 버블 쿠션, 에어 튜브), 소재 유형(폴리에틸렌, 폴리프로필렌, 폴리에틸렌 테레프탈레이트 등), 최종 이용 산업(전자상거래, 가전, 식품 및 음료, 의약품 및 의료기기, 퍼스널케어 및 화장품, 자동차 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 에어쿠션 포장 시장 동향 및 인사이트

전자상거래 소포 증가와 파손 방지 수요

온라인 주문량 증가는 여전히 에어쿠션 포장 시장에 있어 가장 강력한 수요 기반이 되고 있습니다. 이는 출하량이 늘어날 때마다 운송 중 보호에 대한 새로운 요구가 발생하기 때문입니다. 주문 평균 금액이 줄어들고 출하되는 상품 수량이 감소함에 따라, 그 압박은 점점 더 커지고 있습니다. 왜냐하면, 상품이 헐겁게 채워진 골판지 상자는 상품이 꽉 채워진 여러 품목의 주문에 비해 내부에서 상품이 움직이거나 파손되기 쉽기 때문입니다. 따라서 제품 파손이 즉시 반품, 교환 비용 및 고객 서비스 비용으로 이어지는 카테고리에서는 에어쿠션 포장 시장의 중요성이 더욱 커지고 있습니다. 아마존이 과거에 플라스틱 에어필로우를 매우 대규모로 도입했던 사실은 이 회사가 다른 소재로의 전환을 추진하기 전까지 대량 처리 물류 센터에서 팽창식 충진재가 얼마나 핵심적인 역할을 했는지를 보여줍니다. 보호 포장의 비용은 여전히 역물류나 제품 손실 비용보다 훨씬 낮기 때문에 적은 양의 자재로 정밀한 완충 효과를 제공할 수 있는 공급업체에게는 여전히 큰 경제적 이점이 있다고 할 수 있습니다. 에어쿠션 포장 시장에서 이는 소포 수 증가 그 자체뿐만 아니라 대량 배송 네트워크에서 예방 가능한 손상을 방지하기 위한 비용과도 직결됩니다.

창고 자동화 및 온디맨드 확장 기술 도입

창고 자동화는 에어쿠션 포장 시장이 풀필먼트 센터 전체에서 어떻게 전개되는지를 변화시키고 있으며, 이는 단순히 자재 사용량에만 국한된 것이 아닙니다. 2025년 창고 자동화에 관한 조사에 따르면, 조사 대상 물류 업체의 37%가 핵심 업무 개선 방안으로 자동화 도입을 계획했으며, 이는 인라인 보호 포장 시스템에 대한 지속적인 관심을 뒷받침하고 있습니다. 실무상, 자동화 라인에서는 주문형 충진이 선호됩니다. 이는 보관 공간을 줄이고, 사용 전 공기 누출 위험을 낮추며, 골판지 상자 규격에 더욱 부합하는 생산이 가능하기 때문입니다. Storopack사는 2025년 9월, 공기나 종이 완충재를 공급하기 전에 공극 용적을 계산하는 AI 기반 비전 스캔 기능을 모듈에 추가했습니다. 이는 더 높은 정밀도와 폐기물 감축을 목표로 하는 에어쿠션 포장 시장의 방향성을 반영하고 있습니다. 또한, 에어쿠션 포장 시장은 기계 도입이 소모품의 지속적인 구매로 이어지기 쉽다는 점에서도 혜택을 보고 있습니다. 이로 인해 공급업체에 대한 충성도가 높아지고, 시스템 도입 후 다른 업체로 전환하는 데 드는 비용이 증가합니다. 풀필먼트 업체들이 포장 스테이션의 자동화를 추진함에 따라, 에어쿠션 포장 시장에서는 하드웨어의 신뢰성, 소프트웨어 제어, 필름의 성능을 단일 솔루션으로 통합한 공급업체가 우위를 점할 가능성이 높습니다.

아마존의 북미 플라스틱 에어쿠션 단계적 폐지

아마존은 2024년 중반까지 북미에서 사용되는 플라스틱 에어쿠션의 95%를 100% 재생지로 만든 충전재로 대체했으며, 2024년 말까지 이를 완전히 폐지했습니다. 이를 통해 연간 약 20억 건의 출하에서 추정 150억 개의 플라스틱 에어쿠션이 절감되었습니다. 이는 한 대형 구매업체가 주요 물류 네트워크 전반에 걸쳐 자재 수요를 신속하게 재조정할 수 있음을 보여주며, 에어쿠션 포장 시장에 있어 중요한 제약 요인으로 작용하고 있습니다. 이러한 전환은 아마존 자체의 조달에 그치지 않고, 동일한 물류 생태계 내의 판매업체 및 서비스 파트너들에게도 자사의 포장 방식을 플랫폼 정책에 맞추도록 압력을 가하는 결과를 낳았습니다. 그 결과, 보호 포장재에 대한 광범위한 수요는 유지되었으나, 에어쿠션 포장 시장은 북미의 대량의 발포 완충재 수요 중 일부를 잃게 되었습니다. 아마존은 이미 2022년에 유럽에서 2020년에는 인도에서 플라스틱 에어쿠션을 단계적으로 폐지한 바 있으며, 이는 대형 전자상거래 업체들이 앞으로도 기존 방식의 플라스틱 에어쿠션에 대한 의존도를 계속 줄여나갈 가능성이 있다는 신호를 더욱 분명히 하는 결과가 되었습니다. 에어쿠션 포장 시장의 경우, 이는 기존의 PE 소재 에어쿠션에 의존하기보다는 재활용이 가능한 제품, 종이 하이브리드 제품 및 기타 규제 준수형 제품으로의 전환을 서둘러야 할 필요성을 더욱 높이고 있습니다.

부문별 분석

2025년, 에어쿠션은 에어쿠션 포장 시장 점유율의 55.34%를 차지하며 다른 제품 유형을 크게 앞질렀습니다. 이러한 우위는 평평하게 보관할 수 있는 효율성, 자동 인라인 충전과의 호환성, 그리고 대량 출하 시 여전히 매력적인 큐빅 피트당 낮은 비용이라는 보호 성능에서 비롯됩니다. 또한, 에어쿠션 포장 업계가 이 방식을 선호하는 이유로는 공기를 빼낸 필름 롤은 미리 부풀려 둔 재고에 비해 훨씬 적은 바닥 면적만 차지하므로, 작업자가 포장 스테이션의 보충 작업을 간소화할 수 있다는 점을 들 수 있습니다. 주요 공급업체들이 구축한 독자적인 기계 생태계는 고객들이 하드웨어, 필름, 서비스 모델을 세트로 구매하는 경우가 많기 때문에 그 입지를 더욱 공고히 하고 있습니다. 이러한 도입 기반의 우위 덕분에, 원자재 선호도가 변화하더라도 에어필로는 에어쿠션 포장 시장에서 확고한 입지를 계속해서 다지고 있습니다.

버블 쿠션 시장은 2031년까지 연평균 성장률(CAGR) 6.75%로 확대될 것으로 예상되며, 에어 쿠션 포장 시장에서 가장 빠르게 성장하는 제품 카테고리가 될 전망입니다. 그 매력은 이중적인 용도에 있다고 할 수 있습니다. 즉, 흠집 방지나 충격 흡수가 필요한 출하 과정에서 틈새 충전재로서도 표면 포장재로서도 기능을 한다는 점입니다. 에어 튜브와 팽창식 에어백은 매출 규모 면에서는 여전히 작지만, 단순한 빈 공간 채우기보다 축 방향 하중 분산이 중시되는 산업 기기 및 의료기기 운송 분야에서 그 존재감을 높여가고 있습니다. 2025년 2월 Storopack이 출시한 ‘AIRfiber’ 역시, 에어쿠션 포장 시장이 기존의 플라스틱 보호재와 재활용 가능한 종이 기반 솔루션의 경계를 모호하게 만드는 종이 기반의 하이브리드 형태로 전환되고 있음을 보여줍니다. 이러한 융합을 통해 브랜드 소유자는 완충 성능을 유지하면서 에어쿠션 포장 시장을 더욱 엄격해진 재활용성 기준에 부합하도록 만들 수 있게 됩니다.

지역별 분석

아시아태평양은 2025년에 매출 점유율 39.14%를 기록하며 에어쿠션 포장 시장을 주도했으며, 2031년까지 연평균 성장률(CAGR) 7.66%를 기록해 지역별 가장 높은 성장률을 나타낼 것으로 전망됩니다. 이 지역은 대규모 제조 거점, 활발한 수출 활동, 그리고 광범위한 전자상거래 물류 네트워크의 혜택을 누리고 있으며, 이러한 요인들이 여러 제품 카테고리에 걸친 보호 포장 수요를 지속적으로 견인하고 있습니다. 중국은 온라인 소매 물류 및 전자기기 생산 분야에서 차지하는 규모가 크기 때문에 여전히 핵심 기여국으로 자리 잡고 있으며, 표준형 충진재와 보다 전문적인 팽창형 포맷에 대한 수요를 모두 뒷받침하고 있습니다. 인도는 의약품 제조, 체계적인 소매 물류, 그리고 국내 포장 역량이 지속적으로 확대되고 있어 중요한 성장 동력으로 부상하고 있습니다. 일본과 한국은 전자기기 및 반도체 관련 운송 분야에서 정밀 보호 솔루션에 대한 안정적인 수요를 창출하고 있으며, 이에 따라 에어쿠션 포장 시장은 대량 주문 처리 수요뿐만 아니라 고부가가치 산업용 수요와도 연계된 상태를 유지하고 있습니다.

북미는 에어쿠션 포장 지역 시장으로서 여전히 2위의 규모를 유지하고 있습니다. 미국이 이 지역의 중심지이지만, 아마존이 2024년 말까지 북미 전역에서 플라스틱 에어쿠션을 단계적으로 폐지함에 따라 기존 플라스틱 완충재 수요에는 단기적인 역풍이 불었고, 재활용이 가능하며 적절한 크기의 대체재에 대한 관심이 높아졌습니다. 한편, 이 지역은 여전히 대규모 물류 거점을 보유하고 있으며, 2024년 미국, 캐나다, 멕시코 간 화물 유통량은 1조 6,000억 달러로 여전히 막대한 규모를 기록해, 이는 통합된 유통 네트워크 전반에 걸친 경량 보호 포장재의 사용을 뒷받침하고 있습니다. 또한 멕시코는 니어쇼어링의 거점으로 주목받고 있으며, 이는 에어쿠션 포장 시장에 있어 새로운 주문 처리 및 포장 수요의 거점이 되고 있습니다.

유럽은 PPWR 2025/40이 포장 디자인의 우선순위와 소재의 경제성 모두를 변화시키기 때문에 에어쿠션 포장 시장에서 규제의 영향을 가장 직접적으로 받는 지역입니다. 독일은 여전히 유럽 내 주요 수요 거점이며, 한편 영국, 프랑스, 베네룩스 국가들도 주요 공급업체들이 이미 이들 시장 전반에 걸쳐 긴밀한 서비스 및 유통망을 구축하고 있기 때문에 계속해서 중요한 시장으로 남아 있습니다. 유럽연합 집행위원회의 지침에 따르면, 완충재도 빈 공간 제한 대상에 포함된다는 점이 명확히 명시되어 있으며, 이에 따라 2026년 8월 이후 고객들은 보다 정밀한 포장 시스템이나 재활용성이 높은 방식으로 전환하게 될 것입니다. 남미, 중동 및 아프리카는 절대적인 규모 면에서는 여전히 작지만, 공급업체들이 성숙한 주요 지역을 넘어 사업 다각화를 모색하는 과정에서 적절한 성장 기회를 제공합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the air cushion packaging market size is expected to grow from USD 4.88 billion in 2025 to USD 5.17 billion in 2026 and is forecast to reach USD 6.95 billion by 2031 at 6.07% CAGR over 2026-2031.

This report is Segmented by Product Type (Air Pillows, Bubble Cushioning, and Air Tubes), Material Type (Polyethylene, Polypropylene, Polyethylene Terephthalate, and More), End-Use Industry (E-Commerce, Consumer Electronics, Food and Beverages, Pharmaceutical and Medical Devices, Personal Care and Cosmetics, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Air Cushion Packaging Market Trends and Insights

E-Commerce Parcel Growth and Damage Prevention Needs

Rising online order volumes remain the strongest demand base for the air cushion packaging market, as each additional shipment creates another need for transit protection. The pressure increases as basket sizes shrink and shipments contain fewer items, because loosely packed cartons are more prone to movement and breakage than dense multi-item orders. That makes the air cushion packaging market more relevant in categories where product damage quickly turns into returns, replacement costs, and customer service expenses. Amazon's earlier use of plastic air pillows at very large scale showed how central inflatable void-fill had become in high-throughput fulfillment before the company moved to another material path. The economic logic remains favorable for suppliers that can provide precise cushioning with low material use, because protective packaging still costs far less than reverse logistics and product loss. In the air cushion packaging market, this keeps demand tied not only to parcel growth itself but also to the cost of avoiding preventable damage in high-volume shipping networks.

Warehouse Automation and On-Demand Inflation Adoption

Warehouse automation is changing how the air cushion packaging market is deployed across fulfillment centers, not just how much material is used. A 2025 warehouse automation study indicated that 37% of surveyed logistics operators planned to implement automation as a core operational improvement, which supports continued interest in inline protective packaging systems. In practice, automated lines favor on-demand inflation because they reduce storage requirements, lower the risk of deflation before use, and allow output to more closely match carton requirements. Storopack expanded its module in September 2025 with AI-powered vision scanning that calculates void volumes before dispensing air or paper padding, which reflects the direction of the air cushion packaging market toward higher accuracy and lower waste. The air cushion packaging market also benefits from the fact that machine installations often lead to recurring consumable purchases, which strengthens supplier retention and raises switching costs after a system is in place. As more fulfillment operators automate pack stations, the air cushion packaging market is likely to reward suppliers that combine hardware reliability, software control, and film performance in a single offering.

Amazon's North America Plastic Air Pillow Phaseout

Amazon completed the replacement of 95% of plastic air pillows with 100% recycled paper filler in North America by mid-2024 and reached full elimination by the end of 2024, removing an estimated 15 billion plastic air pillows a year from around 2 billion shipments. This is a meaningful restraint on the air cushion packaging market because it shows that one large buyer can quickly reset material demand across a major fulfillment network. The transition also mattered beyond Amazon's own procurement because sellers and service partners inside the same logistics ecosystem faced pressure to align their own packaging choices with the platform's direction. The air cushion packaging market therefore lost part of a large-volume North American void-fill pool even though broader demand for protective packaging remained intact. Amazon had already phased out plastic air pillows in Europe in 2022 and in India in 2020, which reinforced the signal that large e-tailers may continue to reduce exposure to conventional plastic air formats. For the air cushion packaging market, this increases the urgency of shifting toward recyclable, paper-hybrid, and other compliance-friendly formats rather than relying on legacy PE air pillows.

Other drivers and restraints analyzed in the detailed report include:

- Recycled-Content and Recyclable Film Innovation

- Freight Weight and Cube Reduction Priorities

- EU Empty-Space and EPR Rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air pillows held 55.34% of the air cushion packaging market share in 2025, which kept them well ahead of the other product types. Their lead came from flat-pack storage efficiency, compatibility with automated inline inflation, and a low cost-per-cubic-foot protection profile that remains attractive in high-volume fulfillment. The air cushion packaging industry also favors this format because deflated film rolls use far less floor space than pre-inflated stock, which helps operators simplify pack-station replenishment. Proprietary machine ecosystems from leading suppliers strengthen that position because customers often buy the hardware, film, and service model together. This installed base advantage keeps air pillows firmly embedded in the air cushion packaging market, even as material preferences evolve.

Bubble cushioning is projected to expand at 6.75% CAGR through 2031, making it the fastest-growing product category in the air cushion packaging market. Its appeal lies in its dual-use performance: it can serve as both void fill and surface wrap for shipments that require scratch protection and impact absorption. Air tubes and inflatable air bags remain smaller in revenue terms, but they are gaining ground in industrial equipment and pharmaceutical device transport where axial load distribution matters more than simple gap filling. Storopack's AIRfiber launch in February 2025 also showed that the air cushion packaging market is moving toward paper-based hybrid formats that blur the old line between inflatable plastic protection and recyclable paper solutions. That convergence gives brand owners a way to preserve cushioning performance while adapting the air cushion packaging market to stricter recyclability expectations.

Geography Analysis

Asia-Pacific led the air cushion packaging market with 39.14% revenue share in 2025 and is also expected to post the fastest regional CAGR at 7.66% through 2031. The region benefits from a large manufacturing base, robust export activity, and a broad e-commerce fulfillment network, which continues to drive demand for protective packaging across multiple product categories. China remains the central contributor because of its scale in online retail logistics and electronics production, which supports both standard void-fill demand and more specialized inflatable formats. India is becoming an important growth engine as pharmaceutical manufacturing, organized retail logistics, and domestic packaging capability continue to expand. Japan and South Korea add stable demand for precision protective solutions in electronics and semiconductor-related shipments, which keeps the air cushion packaging market tied to higher-value industrial uses as well as volume fulfillment demand.

North America remained the second-largest regional market for air cushion packaging. The United States anchors the region, but Amazon's full North American phaseout of plastic air pillows by the end of 2024 created a near-term headwind for conventional plastic void-fill demand and redirected attention toward recyclable and right-sized alternatives. At the same time, the region still offers a large logistics base, and US, Canada, and Mexico freight flows remained substantial at USD 1.6 trillion in 2024, which supports the use of lightweight protective formats across integrated distribution networks. Mexico is also gaining attention as a nearshoring hub, which adds new fulfillment and packaging demand nodes for the air cushion packaging market.

Europe is the geography most directly shaped by regulation in the air cushion packaging market because PPWR 2025/40 changes both packaging design priorities and material economics. Germany remains a leading European demand center, while the United Kingdom, France, and the Benelux countries continue to matter because major suppliers already have dense service and distribution coverage across those markets. The Commission's guidance makes it clear that void-fill materials count toward empty-space limits, which will push customers toward more precise packaging systems and higher-recyclability formats from August 2026 onward. South America and the Middle East and Africa remain smaller in absolute scale, but they still offer moderate growth opportunities as suppliers look for diversification beyond mature core regions.

- Sealed Air Corporation

- Pregis LLC

- Storopack Hans Reichenecker GmbH

- Smurfit Westrock plc

- Intertape Polymer Group Inc.

- Veritiv Operating Company

- Macfarlane Group UK Ltd

- Airfil Protective Packaging Ltd.

- Inflatable Packaging, Inc.

- RAJAPACK SAS

- Kite Packaging Limited

- Dynaflex Private Limited

- Packman Packaging Private Limited

- Guangzhou PackBest Air Packaging Co., Ltd.

- Aeris Protective Packaging Inc.

- Shorr Packaging Corporation

- Advanced Protective Packaging Ltd.

- Polyair Inter Pack Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Parcel Growth and Damage Prevention Needs

- 4.2.2 Warehouse Automation and On-Demand Inflation Adoption

- 4.2.3 Freight Weight and Cube Reduction Priorities

- 4.2.4 Recycled-Content and Recyclable Film Innovation

- 4.2.5 Pack-Station Space Compression and SKU Rationalization

- 4.2.6 Precision Void-Fill Optimization for Right-Sized Packaging Operations

- 4.3 Market Restraints

- 4.3.1 Plastic Waste Scrutiny and Flexible-Film Recycling Gaps

- 4.3.2 Resin Price Volatility and Equipment Switching Costs

- 4.3.3 Amazon's North America Plastic Air Pillow Phaseout

- 4.3.4 EU Empty-Space and EPR Rules

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Air Pillows

- 5.1.2 Bubble Cushioning

- 5.1.3 Air Tubes

- 5.2 By Material Type

- 5.2.1 Polyethylene

- 5.2.2 Polypropylene

- 5.2.3 Polyethylene terephthalate

- 5.2.4 Polylactic Acid and Starch Blends

- 5.3 By End-Use Industry

- 5.3.1 Food and Beverages

- 5.3.2 Consumer Electronics

- 5.3.3 E-commerce

- 5.3.4 Pharmaceutical and Medical Devices

- 5.3.5 Personal Care and Cosmetics

- 5.3.6 Home Decor and Furnishings

- 5.3.7 Automotive

- 5.3.8 Other End-User Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 South Korea

- 5.4.4.4 India

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Sealed Air Corporation

- 6.4.2 Pregis LLC

- 6.4.3 Storopack Hans Reichenecker GmbH

- 6.4.4 Smurfit Westrock plc

- 6.4.5 Intertape Polymer Group Inc.

- 6.4.6 Veritiv Operating Company

- 6.4.7 Macfarlane Group UK Ltd

- 6.4.8 Airfil Protective Packaging Ltd.

- 6.4.9 Inflatable Packaging, Inc.

- 6.4.10 RAJAPACK SAS

- 6.4.11 Kite Packaging Limited

- 6.4.12 Dynaflex Private Limited

- 6.4.13 Packman Packaging Private Limited

- 6.4.14 Guangzhou PackBest Air Packaging Co., Ltd.

- 6.4.15 Aeris Protective Packaging Inc.

- 6.4.16 Shorr Packaging Corporation

- 6.4.17 Advanced Protective Packaging Ltd.

- 6.4.18 Polyair Inter Pack Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment