|

시장보고서

상품코드

2064441

종합 보상 플랫폼 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Total Rewards Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

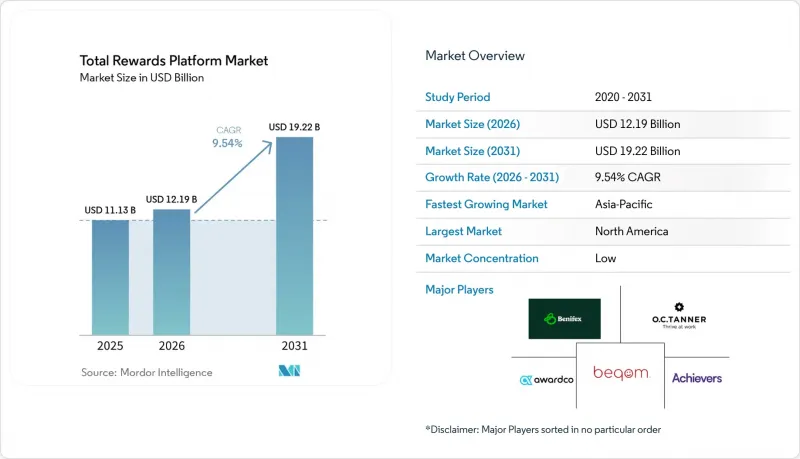

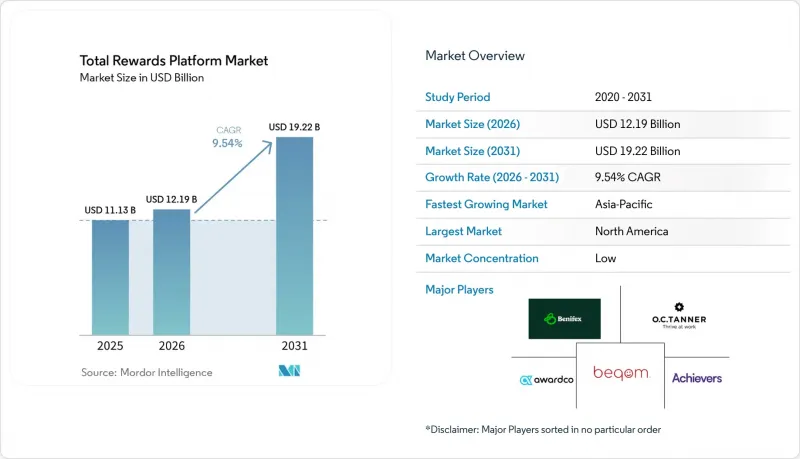

Mordor Intelligence에 의하면, 종합 보상 플랫폼 시장 규모는 2025년에 111억 3,000만 달러로 평가되었고, 2026-2031년 CAGR 9.54%로 성장을 지속할 전망이며, 2031년에는 192억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 도입 형태별(클라우드 기반 및 온프레미스형), 플랫폼 모듈별(평가 및 보상, 보상 관리, 복리후생 관리, 기타), 조직 규모별(대기업 및 중소기업), 최종 사용자 산업별(은행/금융서비스/보험, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 종합 보상 플랫폼 시장 동향 및 인사이트

높아지는 임금 투명성 및 임금 평등 규정 준수 수요

임금 투명성에 관한 법적 규제는 단순한 평판 문제에서 사업 운영상의 필수 요건으로 전환되면서, 종합 보상 플랫폼 시장 전체에 대한 직접 투자를 촉진하고 있습니다. 2026년 4월 현재, EU 회원국 4개국에서는 부분적인 국내법 반영이 시행되고 있으며, 또한 9개국이 법안 초안을 공표한 상태였으나, 직원 150명 이상을 고용한 고용주는 2027년 6월에 제출이 의무화되는 보고서를 위해 2026년 성별 임금 격차 데이터를 수집해야 했습니다. 프랑스, 덴마크, 리투아니아를 포함한 최소 7개 회원국에서는 기준치 하향 조정 및 고용주의 의무 범위 확대를 통해 지침의 최소 요건을 초과하는 조치를 취해 왔습니다. 이러한 차이로 인해 다국적 기업들은 HRIS에서 데이터를 추출하거나 수작업으로 보고서를 작성하는 등의 임시방편에 의존하기보다는 국가별 논리를 적용할 수 있는 임금 격차 시정 모듈을 도입하는 방향으로 나아가고 있습니다. 미국에서는 캘리포니아주가 2026년 1월 1일부터 임금 격차 분석에 주식 보상을 포함하도록 의무화함에 따라, 기본적인 급여 계산 시스템으로는 적절히 처리할 수 없는 보상 데이터 관리의 새로운 단계가 추가되었습니다. 이로 인해 유럽과 북미에서 규정 준수를 중시하는 조달 수요가 더욱 시급해지고 있으며, 종합 보상 플랫폼 시장의 단기적 수요가 강화되고 있습니다.

보상, 복리후생, 급여 전반에 걸친 AI 주도형 맞춤화 및 의사결정 지원

AI는 종합 보상 플랫폼 시장에서 자동화된 임금 격차 모니터링, 맞춤형 복리후생 안내, 시나리오 기반 보상 계획 분야에서 가장 뚜렷한 효과를 발휘하고 있습니다. 머서(Mercer)는 AI가 일상적인 문의 및 표준 복리후생 관리 업무를 포함한 보상 관련 거래 업무의 52%를 처리할 수 있다고 밝혔습니다. 또한 대기업에서는 시장 벤치마크, 내부 형평성 데이터, 실적 동향을 동시에 종합적으로 검토하여 인상안을 검증하는 에이전트형 시스템도 도입되고 있으며, 2026년에는 그 도입률이 48%를 나타낼 것으로 전망됩니다. AI를 활용한 성과 평가 도구를 도입한 조직에서는 연간 평가 주기를 8-12주에서 2주로 단축하고 있습니다. 그러나 이러한 시스템은 거버넌스상의 위험도 초래하고 있습니다. 왜냐하면 검증 과정이 불충분할 경우, 편향된 과거 급여 데이터가 향후 권고 사항에 계속해서 반영될 가능성이 있기 때문입니다. 따라서 보상 결정의 근거를 알기 쉬운 언어로 설명하고, 종합 보상 플랫폼 시장 전반에 걸친 인적 감독을 지원할 수 있는 ‘설명 가능한 AI’ 도구에 대한 새로운 수요가 생겨나고 있습니다.

기존 인사, 급여, 보험, 협업 시스템 통합의 복잡성

통합 과정에서 발생하는 마찰은 종합 보상 플랫폼 시장의 도입에 있어 여전히 가장 큰 운영상의 장벽으로 남아 있습니다. Bindbee에 따르면, 68%의 조직이 서로 연동되지 않은 HR 플랫폼을 운영하고 있으며, 그 결과 통합 환경에 비해 관리 업무에 소요되는 시간이 23% 증가하고 오류율이 31% 높아지고 있습니다. Lift HCM의 조사에 따르면, 직원 150명을 둔 조직이 매달 51시간을 중복되는 관리 업무에 소비하고 있으며, 이로 인해 연간 2만 1,420달러의 간접비가 발생하고 있는 것으로 나타났습니다. 더 큰 과제는 지속적인 유지보수입니다. 20건 이상의 맞춤형 통합을 수행하고 있는 조직은 연간 50만 달러 이상을 지출하며, 통합 관련 IT 지출의 60%-70%를 유지 관리에 할애하고 있기 때문입니다. 보안 검토 및 사용자 정의 필드 매핑으로 인해 진행 속도가 늦어지기 때문에 통합에 소요되는 기간은 여전히 Workday의 경우 1-3주, SAP SuccessFactors의 경우 2-4주, 자체 HRIS 시스템의 경우 4-8주입니다. 이러한 부담은 전담 통합 팀을 갖추지 못한 중견 기업들에게 특히 큰 부담이 되고 있으며, 종합 보상 플랫폼 시장에서의 플랫폼 통합 진전을 늦추고 있습니다.

부문별 분석

2025년 기준으로 온프레미스 방식은 종합 보상 플랫폼 시장 점유율의 62.81%를 차지했으며, 이는 현재 주류를 이루고 있는 자가 관리형 시스템에 대한 선호보다 장기적인 기업 계약의 비중이 더 크다는 점을 반영하고 있습니다. 이 도입 기반은 긴 조달 주기를 거쳐 구축된 것으로, 많은 대기업들은 급여 계산, 보상, 직원 마스터 데이터가 고도로 맞춤화되어 있어 이전이 어려웠기 때문에 온프레미스 환경을 계속 유지해 왔습니다. 클라우드 기반 도입은 2031년까지 연평균 성장률(CAGR) 12.36%를 나타낼 것으로 예측되며, 총 보상 플랫폼 시장에서 가장 빠르게 성장하는 배포 모델이 될 전망입니다. SAP의 2025년 12월 호환성 지원 종료 및 2030년 지원 종료 예정으로 인해, 전환을 미뤄왔던 고용주들에게 구체적인 업데이트 시기가 다가오고 있으므로, 이번 시기는 매우 중요합니다. 또한, 공급업체가 140개국 이상에서 규정 준수 업데이트를 적용할 수 있으므로, 각 고용주가 현지 규제 변경 사항을 수동으로 관리할 필요가 없으며, 클라우드 인프라의 신뢰성도 높아지고 있습니다.

핵심 직원 기록은 온프레미스에 보관하면서, 표창 제도, LSA(노동기준법) 관리, 임금 격차 분석을 클라우드 모듈로 실행하는 하이브리드 도입 방식을 선택하는 고용주가 늘고 있습니다. 이러한 경향은 최신 기능을 추구하는 한편, 기밀 데이터의 보관에 대해서는 보다 엄격한 관리가 필요한 규제 산업에서 특히 두드러집니다. 또한, 이는 종합 보상 플랫폼 산업이 온프레미스에서 풀 클라우드로 일직선으로 나아가고 있는 것은 아니라는 것을 의미합니다. 왜냐하면, 선택적인 클라우드 도입을 통해 규정 준수 및 운영상의 요구 사항을 동시에 충족할 수 있기 때문입니다. 유럽과 아시아태평양 일부 지역에서는 클라우드 도입이 계속 확대되고 있음에도 불구하고, GDPR(EU 개인정보보호규정) 및 데이터 주권 관련 규제로 인해 하이브리드 모델이 계속해서 중요하게 여겨질 것으로 보입니다.

2025년에는 표창 및 보상이 36.41%의 점유율을 차지했으며, 총 보상 플랫폼 시장에서 가장 큰 모듈이 되었습니다. 이는 고용주가 디지털화 대상으로 가장 먼저 선택하는 기능이 되는 경우가 많기 때문입니다. 고용주가 일반적으로 가장 먼저 표창 제도를 도입하는 이유는 급여 시스템과 긴밀하게 연계되지 않아도 운영을 시작할 수 있고, 참여 및 몰입도 관련 활동이 즉시 가시화되기 때문입니다. 또한, 2026년 미국의 평균 성과 연동 임금 인상 예산이 3.2%-3.6%로 안정세를 보이는 등, 급여 예산이 압박받는 상황에서도 표창 제도는 저비용의 직원 유지 방안으로서 여전히 매력적인 수단으로 남아 있습니다. 인력 분석 및 임금 격차 해소 시장은 2031년까지 연평균 성장률(CAGR) 11.21%를 나타낼 것으로 예측되며, 이 모듈 그룹 내에서 가장 빠른 성장세를 보이고 있습니다. 이러한 추세는 EU의 임금 투명성 규정에 따른 보고 요건과 미국 각 주 차원의 광범위한 임금 관련 법규에 의해 주도되고 있습니다.

보수 관리와 복리후생 관리는 여전히 중요한 중간 단계로 자리매김하고 있습니다. 이는 고용주가 성과 평가 계획, 가입 절차, 커뮤니케이션 도구 등에서 별도의 시스템으로 분산되지 않고 동일한 데이터 모델을 사용하기를 원하기 때문입니다. 또한, 구매 담당자들이 보수, 복리후생, 표창이 서로 연계된 형태로 운영되기를 바라는 경향이 강해지고 있어, 조달 방식도 번들형으로 전환되고 있습니다. 나머지 모듈들(토탈 리워드 내역, 영업 실적 관리, 근무 일정 관리, 기타)도 계속해서 성장하고 있습니다. 이는 현장의 관리직이 채용이나 인재 유지를 위한 의사결정을 내릴 때, 최신 급여 관련 지침이 필요하기 때문입니다. 이러한 모듈 전반에 걸쳐 워크플로가 보상 데이터와 건강보험 급여 데이터 모두에 걸쳐 있기 때문에 보안 및 감사 관리는 사후 IT 검토가 아닌 제품 선정 단계부터 고려되도록 되어 있습니다.

지역별 분석

2025년, 북미는 종합 보상 플랫폼 시장 점유율의 35.49%를 차지했으며, 최대 지역 블록이 되었습니다. 미국은 여전히 핵심 시장이며, 2026년에는 국내 노동력의 30% 이상이 현행 임금 투명성법의 적용 대상이 되었습니다. 더 많은 주에서 임금 범위 공개 및 임금 격차 보고 의무를 법제화함에 따라, 그 법적 적용 범위는 확대되고 있습니다. 캐나다와 멕시코도 소규모이긴 하지만 수요를 끌어올리고 있으며, 캐나다의 연방 임금 평등 체계는 규제 대상 고용주들 사이에서 보상 분석 도입을 지속적으로 뒷받침하고 있습니다. 현재, 단일 컴플라이언스 도구에서 보상, 복리후생, 표창, 분석을 하나의 워크플로우 내에 통합한 종합적인 솔루션으로의 명확한 전환이 지역별로 진행되고 있습니다.

유럽에서는 독일, 영국, 프랑스가 중심을 이루고 있으며, 이 3개국은 여전히 해당 지역에서 가장 큰 기업용 HCM 시장입니다. EU의 임금 투명성 지침은 임금 격차 보고 의무, 5%를 초과하는 격차에 대한 공동 임금 평가, 임금 비밀 유지에 관한 보다 엄격한 규정을 도입함으로써 단기적인 조달 수요를 창출하고 있습니다. 독일에서는 공급업체가 현지 기업 고객을 확보하기 위해 DSGVO(일반 데이터 보호 규정) 준수, DATEV 급여 계산 시스템과의 통합, 직원 대표 위원회(워크 카운슬)에 대응하는 프로세스가 필요하기 때문에 이에 따른 현지화 단계가 추가로 더해지고 있습니다. 영국에서는 직원 250명 이상의 고용주가 EU의 규제 범위 밖에서도 성별 임금 격차 보고 의무의 대상이 되기 때문에 여전히 독자적인 수요가 유지되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 11.67%를 기록하며 성장할 것으로 예상되며, 총보상 플랫폼 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 인도의 HR 소프트웨어 시장은 2026년에 10억 달러를 넘어설 것으로 예상되는 반면, 중국에서는 대기업의 디지털화 프로그램을 통해 클라우드 기반 보상 및 표창 도구가 계속해서 도입되고 있습니다. 일본의 HR 기술 시장은 2026년에 18억 2,000만 달러에 달할 것으로 예상되며, SmartHR가 2025년 6월에 급여 계산 기능을 출시한 것은 일본이 수작업 프로세스에서 연동형 HCM 시스템으로 전환하고 있음을 보여줍니다. 남미, 중동 및 아프리카는 여전히 도입 초기 단계에 있는 지역으로, 브라질이 복리후생 관리 수요를 주도하고 있으며, 사우디아라비아와 아랍에미리트가 표창 제도의 성장을 뒷받침하고, 남아프리카공화국과 나이지리아는 다국적 기업의 진출을 위한 발판이 되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the total rewards platform market size was valued at USD 11.13 billion in 2025 and is projected to reach USD 19.22 billion by 2031, at a CAGR of 9.54% from 2026 to 2031.

This report is Segmented by Deployment Mode (Cloud-Based, and On-Premises), Platform Module (Recognition and Rewards, Compensation Management, Benefits Administration, and More), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Banking, Financial Services, and Insurance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Total Rewards Platform Market Trends and Insights

Rising Pay Transparency and Pay Equity Compliance Demand

Pay transparency legislation has moved from a reputational topic to an operating requirement, pushing direct investment across the total rewards platform market. As of April 2026, 4 EU member states had partial transpositions in force, and 9 more had published draft legislation, yet employers with 150 or more staff had to capture 2026 gender pay data for reporting due in June 2027. At least 7 member states, including France, Denmark, and Lithuania, were also moving beyond the Directive's minimum terms by lowering thresholds or widening employer obligations. That variation is pushing multinational employers toward pay equity modules that can apply country-specific logic, rather than relying on HRIS exports and manual reporting workarounds. In the United States, California's January 1, 2026, requirement to include equity awards in pay equity analysis has added another layer of compensation data management that basic payroll systems do not handle well. This is making compliance-led procurement more urgent in Europe and North America and is strengthening near-term demand in the total rewards platform market.

Artificial Intelligence-Driven Personalization and Decision Support Across Rewards, Benefits, and Compensation

AI is having its clearest effect in automated pay equity monitoring, personalized benefits guidance, and scenario-based compensation planning in the total rewards platform market. Mercer stated that AI can absorb 52% of transactional rewards workloads, including routine inquiries and standard benefits administration tasks. Large employers are also using agentic systems that test merit increase proposals against market benchmarks, internal equity data, and performance trends simultaneously, with adoption reaching 48% in 2026. Organizations using AI-assisted merit tools are shortening annual review cycles from 8-12 weeks to 2 weeks. The same systems create governance risk because biased historical pay data can continue to flow into future recommendations if testing controls are weak.That is creating fresh demand for explainable AI tools that can justify reward decisions in plain language and support human oversight across the total rewards platform market.

Legacy HR, Payroll, Carrier, and Collaboration-System Integration Complexity

Integration friction remains the clearest operating barrier to adoption in the total rewards platform market. Bindbee stated that 68% of organizations run disconnected HR platforms, leading to 23% more administrative time and 31% higher error rates than in unified environments. Lift HCM showed that a 150-employee organization can spend 51 hours each month on duplicate administrative work, which adds USD 21,420 in yearly overhead. The larger challenge is ongoing maintenance, because organizations with 20 or more custom integrations can spend more than USD 500,000 each year and direct 60%-70% of integration IT spend to upkeep. Integration timelines still run 1-3 weeks for Workday, 2-4 weeks for SAP SuccessFactors, and 4-8 weeks for proprietary HRIS estates, due to security reviews and custom field mapping that slow progress. This burden falls hardest on mid-market employers without dedicated integration teams, slowing platform consolidation in the total rewards platform market.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Migration of HR and Rewards Workflows

- Hybrid and Distributed Workforces Increasing Need for Digital Recognition and Self-Service Rewards Access

- Data Privacy, Artificial Intelligence Governance, and Cross-Border Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-premises held 62.81% of the total rewards platform market share in 2025, reflecting the weight of long-running enterprise contracts over the current preference for self-managed systems. That installed base was built over long procurement cycles, and many large employers kept on-premises environments because payroll, rewards, and employee master data were deeply customized and difficult to move. Cloud-based deployment is projected to grow at a 12.36% CAGR through 2031, making it the fastest-growing deployment model in the total rewards platform market. The timing is important because SAP's December 2025 compatibility support expiry and its 2030 end-of-support path are creating specific renewal windows for employers that had delayed migration. Cloud infrastructure is also gaining credibility because vendors can push compliance updates across more than 140 countries without requiring each employer to manually manage local rule changes.

A growing number of employers are choosing a hybrid deployment, where core employee records remain on-premises while recognition, LSA administration, and pay equity analytics run in cloud modules. This pattern is especially visible in regulated sectors that want modern functionality but still need tighter control over sensitive data stores. It also means the total rewards platform industry is not moving in a straight line from on-premises to full cloud, because selective cloud adoption addresses compliance and operational needs simultaneously. In Europe and parts of Asia-Pacific, GDPR and data sovereignty rules will keep hybrid models relevant even as cloud adoption continues to rise.

Recognition and rewards held a 36.41% share in 2025, making it the largest module in the total rewards platform market, as it is often the first capability employers choose to digitize. Employers usually launch recognition first because it can go live without deep payroll integration and quickly show visible participation and engagement activity. Compressed salary budgets, with average US merit increase budgets stabilizing at 3.2%-3.6% for 2026, also kept recognition attractive as a lower-cost retention lever. People analytics and pay equity are projected to grow at a 11.21% CAGR through 2031, marking the fastest expansion within this module group. That pace is being driven by reporting requirements under EU pay transparency rules and by broader state-level pay legislation in the United States.

Compensation management and benefits administration remain important middle layers because employers want merit planning, enrollment, and communication tools to use the same data model rather than being split across separate systems. Procurement patterns are also shifting toward bundles, since buyers increasingly want compensation, benefits, and recognition to interact rather than sit in disconnected applications. The remaining module group, including total rewards statements, sales performance management, and workforce scheduling links, is growing, where frontline managers need current pay guidance during hiring and retention decisions. Across these modules, security and audit controls are becoming part of the product decision rather than a later IT review because the workflows span compensation and health benefits data.

Geography Analysis

North America held 35.49% of the total rewards platform market share in 2025, which made it the largest regional block. The United States remained the anchor market, with more than 30% of the national workforce covered by active pay transparency laws in 2026. That legal coverage is widening as more states finalize pay range disclosure and pay equity reporting mandates. Canada and Mexico added demand on a smaller scale, with Canada's federal pay equity framework continuing to support the adoption of compensation analytics among regulated employers. A clear regional shift is now underway from single-use compliance tools toward broader suites that integrate compensation, benefits, recognition, and analytics within a single workflow.

Europe is centered on Germany, the United Kingdom, and France, which remain the largest enterprise HCM markets in the region. The EU Pay Transparency Directive is creating a near-term procurement trigger by introducing mandatory pay gap reporting, joint pay assessments for gaps above 5%, and tighter rules on pay secrecy. Germany adds another layer of localization, as vendors need DSGVO compliance, DATEV payroll integration, and works council-ready processes to win local enterprise accounts. The United Kingdom still supports its own demand because employers with 250 or more workers remain subject to gender pay gap reporting outside the EU framework.

Asia-Pacific is projected to grow at a 11.67% CAGR through 2031, making it the fastest-growing geography in the total rewards platform market. India's HR software market is set to exceed USD 1 billion in 2026, while China continues to absorb cloud compensation and recognition tools through large-enterprise digitalization programs. Japan's HR technology market is expected to reach USD 1.82 billion in 2026, and SmartHR's June 2025 payroll calculation launch showed how the country is moving from manual processes to connected HCM systems. South America, the Middle East, and Africa remain earlier-stage adoption areas, with Brazil leading benefits administration demand, Saudi Arabia and the UAE supporting recognition growth, and South Africa and Nigeria serving as footholds for multinational rollout.

- Globoforce Limited (Workhuman)

- O.C. Tanner Company

- Achievers Solutions Inc.

- Awardco, Inc.

- Smartly, Inc.

- Bucketlist Rewards Inc.

- Kudos, Inc.

- Motivosity Inc.

- beqom SA

- Benifex Limited

- Perkbox Limited

- Benepass, Inc.

- Twic, Inc. DBA Forma

- Nayya Health, Inc.

- Bargain Technologies Private Limited

- Guusto Gifts Inc.

- WHAPPS LLC

- Benefitfocus.com, Inc.

- Businessolver

- Semos Cloud

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Pay Transparency and Pay Equity Compliance Demand

- 4.2.2 Cloud Migration of HR and Rewards Workflows

- 4.2.3 Hybrid and Distributed Workforces Increasing Need for Digital Recognition and Self-service Rewards Access

- 4.2.4 Artificial Intelligence-driven Personalization and Decision Support Across Rewards, Benefits, and Compensation

- 4.2.5 Shift From Fragmented Point Tools to Unified Total Rewards Visibility Layers

- 4.2.6 Lifestyle Spending Accounts and Flexible Benefits Wallets Expanding Platform Scope

- 4.3 Market Restraints

- 4.3.1 Legacy HR, Payroll, Carrier, and Collaboration-system Integration Complexity

- 4.3.2 Data Privacy, Artificial Intelligence Governance, and Cross-border Compliance Burden

- 4.3.3 Multicountry Tax Treatment and Reward-fulfillment Localization Complexity

- 4.3.4 Native Human Capital Management Suite Bundling and Pure-play Displacement Risk

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premises

- 5.2 By Platform Module

- 5.2.1 Recognition and Rewards

- 5.2.2 Compensation Management

- 5.2.3 Benefits Administration

- 5.2.4 People Analytics and Pay Equity

- 5.2.5 Other Platform Modules

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 Information Technology and Telecommunications

- 5.4.2 Banking, Financial Services, and Insurance

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and E-commerce

- 5.4.5 Manufacturing

- 5.4.6 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Globoforce Limited (Workhuman)

- 6.4.2 O.C. Tanner Company

- 6.4.3 Achievers Solutions Inc.

- 6.4.4 Awardco, Inc.

- 6.4.5 Smartly, Inc.

- 6.4.6 Bucketlist Rewards Inc.

- 6.4.7 Kudos, Inc.

- 6.4.8 Motivosity Inc.

- 6.4.9 beqom SA

- 6.4.10 Benifex Limited

- 6.4.11 Perkbox Limited

- 6.4.12 Benepass, Inc.

- 6.4.13 Twic, Inc. DBA Forma

- 6.4.14 Nayya Health, Inc.

- 6.4.15 Bargain Technologies Private Limited

- 6.4.16 Guusto Gifts Inc.

- 6.4.17 WHAPPS LLC

- 6.4.18 Benefitfocus.com, Inc.

- 6.4.19 Businessolver

- 6.4.20 Semos Cloud

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment