|

시장보고서

상품코드

2064468

원뿔형 막대형 변성증 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cone Rod Dystrophy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

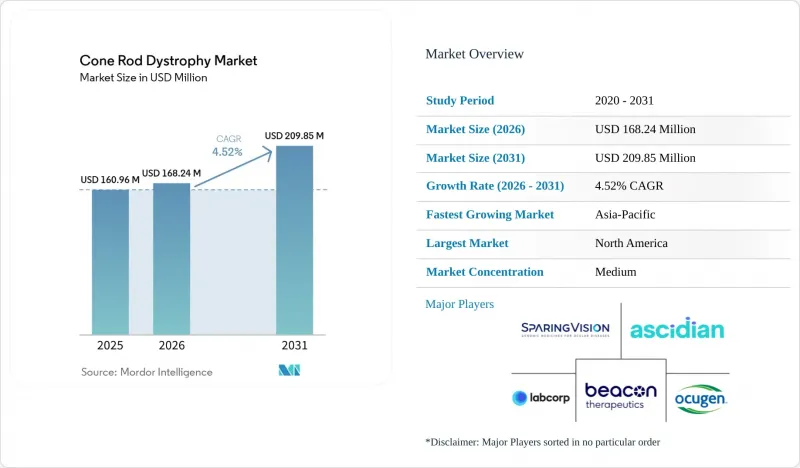

Mordor Intelligence에 의하면, 원뿔형 막대형 변성증 시장 규모는 2025년 1억 6,096만 달러로 평가되었고, 2026년에는 1억 6,824만 달러로 추정되고, 2031년까지 2억 985만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 4.52%로 성장할 전망입니다.

본 보고서는 모달리티별(진단(분자진단 등), 치료(망막 이식 및 신경 자극 등)), 유전 양상별(상염색체 열성, 상염색체 우성, X-연관), 최종 사용자별(병원, 안과 전문센터, 기타), 지역별(북미, 유럽, 아시아태평양, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 원뿔형 막대형 변성증 시장 동향 및 인사이트

유전자 치료의 발전과 희귀질환 치료제(오펀 드럭)에 대한 인센티브가 CRD(원뿔형 막대형 변성증)의 개발 경제 구조를 재편하고 있습니다.

희귀질환 치료제 인센티브 덕분에 소규모 망막 질환 프로그램의 자금 조달이 용이해짐에 따라, 시장은 다른 개발 경로를 따르고 있습니다. 미국에서는 희귀질환 치료제로 지정됨에 따라 7년간 시장 독점권, 주요 수수료 면제, 환자 수가 제한적이라 하더라도 후기 단계의 지출을 정당화할 수 있는 심사 관련 잠재적 가치가 제공됩니다. 비콘 테라퓨틱스(Beacon Therapeutics)는 라루조바(laru-zova)에 대해 이미 FDA로부터 RMAT(망막 질환 치료) 및 패스트 트랙 지정을, EMA로부터는 PRIME 지위를 획득했으며, 이 회사의 VISTA 임상시험은 2025년 6월에 환자 등록을 완료했습니다. 이러한 조합을 통해, 인접한 망막 질환 분야에서 원뿔형 막대형 변성증 시장에 진출하는 기업들의 자금 조달 위험이 줄어듭니다. 또한, 최초로 승인된 치료법이 이 부문의 다른 치료법에 대한 가격 책정 및 보험 급여 기대치를 형성할 가능성도 높아집니다.

분자진단의 보급과 다중 모달리티 망막 영상 기술 덕분에 진단이 가능한 환자층이 확대되고 있습니다.

패널 기반 시퀀싱 및 영상 기술의 발전으로 인해 질환 진행 초기 단계의 환자들도 조기에 진단을 받을 수 있게 되면서, 원추세포·막대세포 이영양증 시장의 진단 가능 환자층이 확대되고 있습니다. 최적화된 학술 환경에서는 유전성 망막 질환의 진단율이 이전의 40%-50%대에서 60%-80%로 향상되었습니다. 이 변화는 중요합니다. 분자진단이 확정되면, 원뿔형 막대형 변성증 시장에서 유전자 특이적 치료법을 결정하거나 유전 상담을 실시하는 데 소요되는 기간이 연장되기 때문입니다. 또한, OCT와 안저 자가형광은 자연 경과 연구에서 유용한 진행 지표로 부상하고 있어, 기능적 측정에만 의존하는 상황을 완화하고 있습니다. 일본에서는 여전히 진단 격차가 나타나고 있으며, 보고된 분자진단률은 40%에 불과하고, 지정 유전자 검사 시설은 12곳에 그치고 있어 지역 간 접근성 격차가 여전히 존재함을 보여주고 있습니다. 또한, 일본은 2023년에 PrismGuide IRD 패널 시스템을 승인했는데, 이 패널에는 X-연관 피라미드-봉세포 이영양증과 관련된 RPGR ORF15 영역이 포함되어 있습니다.

환자 수가 적고 유전적 분산이 크다는 점이 임상 검사의 검출력과 상업적 수익을 제한하고 있습니다.

원뿔형 막대형 변성증 시장은 환자 수가 극히 적고 유전적으로 분산되어 있다는 제약에 여전히 직면해 있습니다. 유병률은 3만 명당 1명에서 4만 명당 1명으로 추정되며, 게다가 30개 이상의 원인 유전자가 존재하기 때문에 이 부문은 단일한 대규모 환자 집단이라기보다는 수많은 초희귀질환 시장과 유사한 특성을 보이고 있습니다. 이러한 분열로 인해, 개발사들은 원뿔형 막대형 변성증 시장에서 통계적 유의성을 확보하기 위해 여러 국가에서 피험자를 등록해야 하는 경우가 많아, 피험자 모집 비용이 급증합니다. 임상 현장에서는 분자진단을 통해 규명되는 사례가 여전히 50%에서 75%에 그치고 있어, 많은 환자가 돌연변이 특이적 프로그램에 참여할 수 없습니다. 2025년 파키스탄의 데이터 세트가 보여주듯이, 상염색체 열성 유전으로 밝혀진 사례의 95.9%를 차지하는 등, 근친혼 집단에는 집중된 코호트가 존재할 가능성이 있지만, 규제 당국은 지역에 따라 이러한 데이터를 동등하게 취급하지 않을 수도 있습니다.

부문별 분석

원뿔형 막대형 변성증 시장에서 진단 부문은 2031년까지 연평균 성장률(CAGR) 6.38%를 나타낼 것으로 예측되며, 이는 성장률이 가장 높은 검사 부문이 될 것입니다. 이러한 증가는 NGS 패널의 이용 확대, 안과 전문센터의 ERG(망막전위도) 검사 역량 강화, 모니터링 분야에서 OCT(광간섭단층촬영) 및 안저 자가형광 검사의 일상적인 활용 증가를 반영한 것입니다. ERG는 막대세포의 소실을 상회하는 원추세포의 기능 장애를 나타내며, 망막색소변성증과의 감별 진단을 돕기 때문에 여전히 임상상의 표준으로 자리 잡고 있습니다. 타원체대의 폭과 같은 구조적 지표는 광수용체의 건전성을 정량적으로 평가할 수 있기 때문에 현재는 ERG와 함께 사용되고 있습니다.

2025년 원뿔형 막대형 변성증 시장에서 치료 부문이 58.31%의 점유율을 차지했습니다. 이는 임상 검사 실시, 망막 이식 수술, 신경 자극 요법, 약물 요법이 여전히 지출의 대부분을 차지하고 있기 때문입니다. 망막 이식와 신경 자극 요법은 보다 성숙한 치료 분야를 형성하고 있는 반면, 원뿔형 막대형 변성증 분야에서 유전적 원인이 밝혀지지 않은 환자를 위한 치료 옵션으로서 지지 요법과 저시력 보조 기구가 주목받고 있습니다. 시각 주기의 조절 및 항산화 요법을 포함한 약리학적 및 영양 보조제 기반 접근법은 첨단 유전자 치료의 투여 인프라에 의존하지 않기 때문에 폭넓은 환자층으로부터 지지를 받고 있습니다. 이러한 구조로 인해, 원뿔형 막대형 변성증 시장에서 진단 부문의 성장이 가속화되고 있음에도 불구하고, 현재까지도 치료 부문의 규모가 더 큽니다.

지역별 분석

2025년, 북미는 원뿔형 막대형 변성증 시장의 38.24%를 차지했으며, 최대 지역 부문이 되었습니다. 이 지역은 안과 전문의들의 네트워크가 밀집되어 있고, 유전성 망막 질환에 대한 연구가 활발하며, 첨단 망막 치료를 제공할 수 있는 치료 센터가 집중되어 있다는 장점이 있습니다. 또한, 미국은 개발 기업의 자금 조달에서도 중심적인 역할을 하고 있으며, Opus Genetics는 2026년 4월, OPGx-RDH12를 포함한 3개의 유전자 치료 프로그램을 임상시험 단계로 진행하기 위해 최대 1억 5,500만 달러의 자금을 확보했습니다. 캐나다와 멕시코도 어느 정도 기여하고 있지만, 유전성 망막 질환에 대한 유전자 치료의 상업화 승인이 가까워짐에 따라, 예측 기간 동안 미국이 지배적인 지위를 유지할 가능성이 높을 것으로 보입니다.

유럽은 원뿔형 막대형 변성증 시장에서 2위를 차지하는 지역 블록이며, 진단 및 임상 검사 분야에서 독일, 영국, 프랑스가 주도적인 역할을 하고 있습니다. 비콘사의 laru-zova는 EMA PRIME 지위를 획득했으며, 이를 통해 해당 프로그램은 FDA의 RMAT와 유사한 목적을 가진 규제 절차 간소화 지원을 받을 수 있습니다. 또한 유럽에서는 스웨덴 규제 당국의 승인을 받아 스웨덴과 EU 내 시설에서 실시된 AAV8-RLBP1의 1상 및 2상 임상시험을 통해, 인간 대상 첫 임상시험 수행 능력도 입증되었습니다. 의료 기술 평가의 시기나 보험 급여 방식은 각국의 제도에 따라 다르기 때문에 접근 상황은 여전히 국가마다 차이가 있습니다.

아시아태평양은 원뿔형 막대형 변성증 시장에서 2031년까지 연평균 성장률(CAGR) 6.92%를 기록하며 성장할 것으로 예상되어, 가장 빠르게 성장하는 지역이 될 전망입니다. 일본은 이미 안과 유전자 치료에 대한 접근 경로를 마련해 놓았으며, 2025년에는 아시아 최초의 유전성 망막 유전자 치료 3상 임상시험으로서, 보레티겐 네팔보벡의 1년 후 3상 임상시험 결과가 발표되었습니다. 또한 일본은 2025년 2월, Restore Vision과 게이오기주쿠 대학병원을 통해 유전적 원인과 관계없이 광수용체 상실 환자를 대상으로 한 최초의 광유전학 임상 검사를 시작했습니다. 중국은 지역별 변이 양상을 규명하는 코호트 연구와 유전성 망막 질환에 대한 CRISPR 용도에 관한 연구 성과를 발표함으로써 그 역할을 강화하고 있습니다. 한국, 호주, 인도, 중동 및 아프리카, 남미는 규모는 작지만 기여하고 있으며, GCC(걸프협력회의)의 임상 검사 자금 지원과 브라질 및 아르헨티나의 희귀질환 등록제가 추가적인 지원을 제공합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the cone rod dystrophy market size is expected to increase from USD 160.96 million in 2025 to USD 168.24 million in 2026 and reach USD 209.85 million by 2031, growing at a CAGR of 4.52% over 2026-2031.

This report is Segmented by Modality (Diagnosis [Molecular Diagnosis, and More], Treatment [Retinal Implant and Neurostimulation, and More]), Inheritance Pattern (Autosomal Recessive, Autosomal Dominant, X-Linked), End User (Hospitals, Ophthalmology Specialty Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Cone Rod Dystrophy Market Trends and Insights

Gene Therapy Progress and Orphan Drug Incentives Are Reshaping CRD Development Economics

The market is seeing a different development path because orphan incentives have made small retinal programs easier to finance. In the United States, Orphan Drug Designation offers 7 years of market exclusivity, major fee waivers, and potential review-related value that can justify late-stage spending even with a limited patient base. Beacon Therapeutics has already secured RMAT and Fast Track designations from the FDA and PRIME status from the EMA for laru-zova, and its VISTA trial completed enrollment in June 2025. This combination lowers funding risk for companies entering the cone rod dystrophy market from nearby retinal indications. It also raises the odds that the first approved therapy will shape pricing and reimbursement expectations for the rest of the field.

Wider Molecular Diagnosis and Multimodal Retinal Imaging Are Expanding the Diagnosable Patient Pool

The cone rod dystrophy market is expanding its diagnosable pool because panel-based sequencing and better imaging now reach patients earlier in the disease course. In optimized academic settings, inherited retinal disease diagnostic yield has moved from the earlier 40% to 50% range toward 60% to 80%. That shift matters because a confirmed molecular diagnosis extends the window for gene-specific treatment decisions and genetic counseling within the cone rod dystrophy market. OCT and fundus autofluorescence have also emerged as useful progression markers in natural history work, which reduces reliance on functional measures alone. Japan still shows a diagnosis gap, with a reported 40% molecular diagnosis rate and 12 designated genetic testing facilities, which points to persistent regional access inequalities. Japan also approved the PrismGuide IRD Panel System in 2023, and the panel includes the RPGR ORF15 region that is relevant to X-linked cone rod dystrophy.

Tiny Fragmented Patient Pools Constrain Trial Power and Commercial Returns

The cone rod dystrophy market remains constrained by a very small and genetically split patient population. Prevalence estimates of 1 in 30,000 to 1 in 40,000, combined with more than 30 causative genes, make the field behave like many ultra-rare markets rather than one large pool. This fragmentation raises recruitment cost because developers often need multi-country enrollment to reach statistical power in the cone rod dystrophy market. Molecular diagnosis still resolves only 50% to 75% of cases in clinical settings, so many patients cannot enter mutation-specific programs. Concentrated cohorts can exist in consanguineous populations, as shown by the 2025 Pakistani dataset where autosomal recessive inheritance represented 95.9% of solved cases, but regulators may not treat these data equally across regions.

Other drivers and restraints analyzed in the detailed report include:

- Genotype Prescreening and Natural-History Cohorts Are Enabling More Efficient CRD Trials

- Mutation-Agnostic Retinal Therapies Are Shifting the Addressable Market Boundary

- One-Time Therapy Pricing and Reimbursement Uncertainty Depress Near-Term Uptake

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Diagnostics is projected to grow at a 6.38% CAGR in the cone rod dystrophy market through 2031, which makes it the fastest-growing modality segment. This rise reflects wider use of NGS panels, growing ERG capacity in ophthalmology specialty centers, and more routine use of OCT with fundus autofluorescence for monitoring. ERG remains the clinical standard because it shows cone dysfunction exceeding rod loss and helps distinguish the condition from retinitis pigmentosa. Structural measures such as ellipsoid zone width are now used alongside ERG because they offer a quantifiable view of photoreceptor integrity.

Treatment represented 58.31% of the cone rod dystrophy market share in 2025 because trial administration, retinal implant procedures, neurostimulation, and pharmacologic care still account for most spending. Retinal implants and neurostimulation form a more mature treatment pocket, while supportive care and low-vision aids are picking up as options for patients who remain genetically unresolved in the cone rod dystrophy industry. Pharmacologic and nutraceutical approaches, including visual cycle modulation and antioxidant regimens, appeal to a broad patient group because they do not depend on advanced gene therapy delivery infrastructure. This mix keeps treatment larger today, even though diagnostics is gaining faster in the cone rod dystrophy market.

Geography Analysis

North America held 38.24% of the cone rod dystrophy market share in 2025, which made it the largest regional segment. The region benefits from a dense ophthalmology specialty network, active inherited retinal disease research support, and a concentration of treatment delivery centers that can support advanced retinal interventions. The United States also remains central to developer financing, as Opus Genetics secured up to USD 155 million in April 2026 to advance 3 more gene therapy programs, including OPGx-RDH12, into clinical testing. Canada and Mexico add smaller contributions, while the United States is likely to stay dominant through the forecast period as inherited retinal gene therapy filings move closer to commercialization.

Europe is the second-largest regional block in the cone rod dystrophy market, led by Germany, the United Kingdom, and France for diagnostics and trial participation. Beacon's laru-zova holds EMA PRIME status, which gives the program accelerated regulatory support that is similar in purpose to FDA RMAT. Europe also demonstrated first-in-human capability through the Phase 1 and Phase 2 AAV8-RLBP1 study run across Swedish and EU centers with Swedish regulatory approvals. Access still varies by country because health technology assessment timing and reimbursement pathways differ across national systems.

Asia-Pacific is projected to grow at a 6.92% CAGR through 2031 in the cone rod dystrophy market, which makes it the fastest-growing region. Japan has already established an ophthalmic gene therapy access pathway, and 1-year Phase 3 outcomes for voretigene neparvovec were published in 2025 as Asia's first Phase 3 inherited retinal gene therapy trial. Japan also opened its first optogenetics trial in February 2025 through Restore Vision and Keio University Hospital for patients with photoreceptor loss regardless of genetic cause. China is strengthening its role through cohort studies that map local mutation patterns and through published work on CRISPR applications for inherited retinal disease. South Korea, Australia, India, the Middle East and Africa, and South America contribute smaller volumes, while GCC trial funding and rare disease registries in Brazil and Argentina provide incremental support.

- 4D Molecular Therapeutics

- Ascidian Therapeutics

- Beacon Therapeutics

- Biogen

- Blueprint Genetics

- Fulgent Genetics

- GenSight Biologics

- Invitae

- jCyte

- Johnson & Johnson Innovative Medicine

- LabCorp

- MeiraGTx

- Ocugen

- Opus Genetics

- PreventionGenetics

- ProQR Therapeutics

- Santen Pharmaceutical

- SparingVision

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Gene Therapy Progress and Orphan Incentives

- 4.2.2 Wider Molecular Diagnosis and Multimodal Retinal Imaging

- 4.2.3 Rising Supportive-Care and Low-Vision Technology Adoption

- 4.2.4 Genotype Prescreening and Natural-History Cohorts

- 4.2.5 Mutation-Agnostic Retinal Therapies

- 4.3 Market Restraints

- 4.3.1 Tiny Fragmented Patient Pools

- 4.3.2 One-Time Therapy Pricing and Reimbursement Uncertainty

- 4.3.3 Weak Endpoint and Biomarker Standardization

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of new entrants

- 4.7.2 Bargaining power of suppliers

- 4.7.3 Bargaining power of buyers

- 4.7.4 Threat of substitutes

- 4.7.5 Intensity of rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Modality

- 5.1.1 Diagnosis

- 5.1.1.1 Molecular diagnosis

- 5.1.1.2 Electroretinography

- 5.1.1.3 OCT and fundus autofluorescence

- 5.1.2 Treatment

- 5.1.2.1 Retinal implant and neurostimulation

- 5.1.2.2 Pharmacological and nutraceutical therapy

- 5.1.2.3 Supportive care and low-vision aids

- 5.1.1 Diagnosis

- 5.2 By Inheritance Pattern

- 5.2.1 Autosomal recessive cone rod dystrophy

- 5.2.2 Autosomal dominant cone rod dystrophy

- 5.2.3 X-linked cone rod dystrophy

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ophthalmology specialty centers

- 5.3.3 Academic and research institutes

- 5.3.4 Home-based low-vision rehabilitation

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 4D Molecular Therapeutics

- 6.3.2 Ascidian Therapeutics

- 6.3.3 Beacon Therapeutics

- 6.3.4 Biogen

- 6.3.5 Blueprint Genetics

- 6.3.6 Fulgent Genetics

- 6.3.7 GenSight Biologics

- 6.3.8 Invitae

- 6.3.9 jCyte

- 6.3.10 Johnson & Johnson Innovative Medicine

- 6.3.11 Labcorp

- 6.3.12 MeiraGTx

- 6.3.13 Ocugen

- 6.3.14 Opus Genetics

- 6.3.15 PreventionGenetics

- 6.3.16 ProQR Therapeutics

- 6.3.17 Santen Pharmaceutical

- 6.3.18 SparingVision

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

(주말 및 공휴일 제외)