|

시장보고서

상품코드

2064470

미국의 복강경 기기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Laparoscopic Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

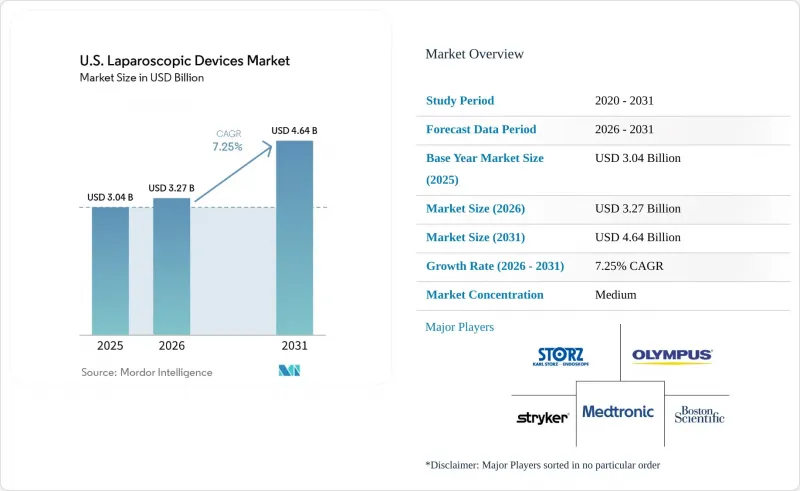

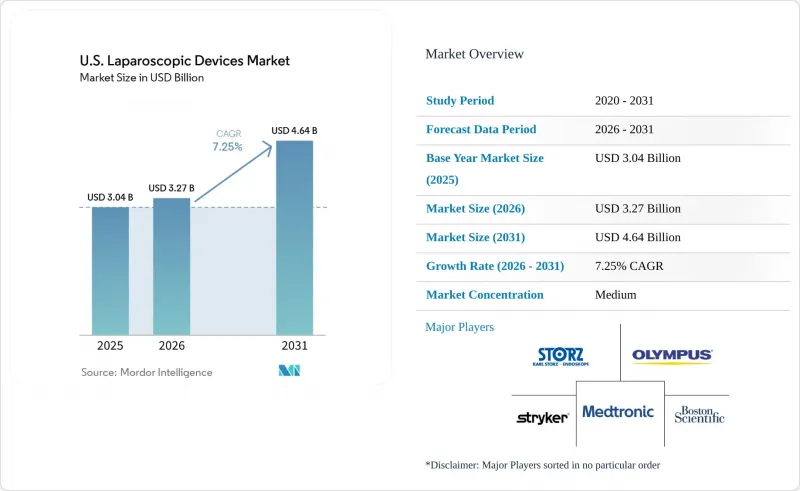

Mordor Intelligence에 의하면, 미국의 복강경 기기 시장 규모는 2025년 30억 4,000만 달러로 평가되었고, 2026년 32억 7,000만 달러로 추정되고, 2031년까지 46억 4,000만 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 7.25%를 나타낼 것으로 예측됩니다.

본 보고서는 제품별(시각화 시스템, 접근 기기, 공기 공급 및 연기 관리, 수동 기구, 에너지 기기, 봉합 및 스테이플링 기기, 회수 기기, 로봇 지원 플랫폼), 용도별(일반, 비만 외과, 산부인과, 기타), 최종 사용자별(병원, 외래수술센터(ASC), 전문 클리닉, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 복강경 기기 시장 동향 및 분석

병원과 ASC로의 전환이 의료기기의 교체 주기를 재편하고 있습니다.

2026년, CMS의 OPPS 및 ASC 최종 규정에 따라 ASC 대상 시술 목록에 547개의 코드가 추가되어, 외래 의료기관에서 보상 대상 시술의 범위가 확대되었습니다. 또한 CMS는 ‘입원 전용 목록’을 3년에 걸쳐 단계적으로 폐지하기 시작했으며, 2026년에 285개 서비스를 삭제함으로써 수술 건수를 비용 대비 효과가 높은 외래 시설로 더욱 전환하고 있습니다. 이러한 전환에 따라, 미국의 복강경 기기 시장은 재편되고 있습니다. ASC에서는 기존 입원 수술실의 구성보다 콤팩트한 시스템, 간소한 설치 절차, 수술실 회전율 향상을 우선시하고 있기 때문입니다. 메드트로닉사의 로봇 보조 수술 시스템 ‘Hugo’는 외래 환경에 적용 가능한 모듈식 아키텍처를 채택하여 이러한 변화를 반영하고 있습니다.

로봇 보조 수술이 고부가가치 의료기기 시장을 재편하고 있습니다.

로봇 수술의 부상으로 인해, 미국의 복강경 기기 시장은 일회용 장비 투자보다는 재사용이 가능한 고부가가치 기구 및 액세서리로 방향을 전환하고 있습니다. 인튜이티브사는 2025년 4분기 다빈치 수술 건수가 17% 증가했으며, 2026년 1분기 기기 및 액세서리 매출이 16억 9,000만 달러에 달했다고 보고했는데, 이는 전년 동기 대비 23% 성장한 수치입니다. 각 로봇 수술에는 호환 가능한 기기가 필요하며, 대부분의 경우 기존 복강경 기구를 대체하고 있습니다. 메드트로닉의 ‘Hugo’와 존슨앤드존슨의 ‘OTTAVA’ 플랫폼은 경쟁이 치열해지고 있음을 보여주고 있으며, 시장 역학은 더 이상 플랫폼의 가용성뿐만 아니라 자금 조달, 수술실 공간, 견고한 기기 생태계로 초점이 이동하고 있습니다.

자본 비용의 집중이 지역 의료 현장에서 플랫폼 보급을 제한하고 있습니다.

높은 설비 투자 비용으로 인해 미국 시장에서 복강경 플랫폼의 도입이 크게 제한되고 있습니다. 인튜이티브사의 보고에 따르면, 다빈치 시스템의 표준 판매 또는 리스 가격은 60만 달러에서 310만 달러이며, 연간 서비스 요금은 9만 5,000달러에서 22만 5,000달러, 수술 1건당 비용은 900달러에서 3,700달러입니다. 대규모 학술 기관이나 주요 의료 네트워크라면 이러한 비용을 감당할 수 있지만, 예산이 제한된 지역 병원이나 소규모 외과 센터에게는 문제가 됩니다. 이러한 비용 격차로 인해 소규모 시설에서의 로봇 기술 도입은 지연되고 있으며, 일부 의료기관은 첨단 로봇 기술에 투자하는 반면, 다른 의료기관은 비용 대비 효과가 높은 일회용 제품이나 단계적인 업그레이드를 선택함으로써 수요의 양극화가 발생하고 있습니다. 신규 진출기업들이 선보이는 모듈식 시스템이 장래에는 이러한 격차를 해소할 가능성이 있지만, 현재의 가격 정책은 여전히 급속한 성장을 가로막는 장애물로 작용하고 있습니다.

부문별 분석

2025년, 에너지 기기는 미국 복강경 기기 시장에서 29.45%의 점유율을 차지했으며, 제품 카테고리를 선도했습니다. 이는 기존의 전기 수술법에서 저침습 수술을 효율화하는 첨단 혈관 봉합 및 조직 관리 기술로의 전환을 반영한 것입니다. 이러한 기기들은 일반외과, 산부인과, 대장항문 치료, 비만 수술 분야에서 널리 사용되고 있으며, 안정적인 수요가 확보되어 있습니다.

수기 기구, 폐쇄·스테이플링 기기, 접근 기기, 시각화 시스템은 여전히 필수적이지만, 일회용 제품, 통합된 워크플로우, 첨단 영상 기능에 중점을 두고 발전하고 있습니다. 일회용 의료기기는 외래 진료의 물류 과정을 간소화하는 한편, 고해상도 영상 시스템은 3D, 4K 또는 형광 기능을 통해 점차 보급이 확대되고 있습니다. 로봇 보조 복강경 수술 플랫폼 및 기구는 메드트로닉의 ‘Hugo’, 존슨앤드존슨의 ‘OTTAVA’, 인튜이티브의 도입 대수 증가에 힘입어 2031년까지 연평균 성장률(CAGR) 8.12%로 성장할 것으로 전망됩니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the u.S. laparoscopic devices market size is projected to expand from USD 3.04 billion in 2025 and USD 3.27 billion in 2026 to USD 4.64 billion by 2031, registering a CAGR of 7.25% between 2026 to 2031.

This report is Segmented by Product (Visualization Systems, Access Devices, Insufflation and Smoke Management, Hand Instruments, Energy Devices, Closure and Stapling, Retrieval Devices, Robotic-Assisted Platforms), Application (General, Bariatric, Gynecological, and More), and End User (Hospitals, Ascs, Specialty Clinics, Others). Market Forecasts are Provided in Terms of Value (USD).

U.S. Laparoscopic Devices Market Trends and Insights

Hospital and ASC Migration Rewriting Capital Equipment Cycles

In 2026, the CMS OPPS and ASC final rule added 547 codes to the ASC Covered Procedures List, expanding the range of reimbursable procedures in ambulatory settings. Additionally, CMS began a three-year phaseout of the Inpatient-Only list, removing 285 services in 2026, further shifting surgical volumes to cost-effective outpatient sites. This transition is reshaping the United States laparoscopic devices market, as ASCs prioritize compact systems, simpler setups, and faster room turnovers over traditional inpatient OR configurations. Medtronic's Hugo robotic-assisted surgery system reflects this shift with its modular architecture, adaptable to outpatient environments.

Robotic-Enabled Surgery Reshaping the High-Value Instrument Tier

The rise of robotic surgery is driving the United States laparoscopic devices market toward premium instruments and accessories, focusing on recurring use rather than one-time capital investments. Intuitive reported a 17% increase in da Vinci procedures in Q4 2025 and USD 1.69 billion in instruments and accessories revenue in Q1 2026, reflecting a 23% year-over-year growth. Each robotic procedure requires compatible devices, often replacing traditional laparoscopic tools. Medtronic's Hugo and Johnson & Johnson's OTTAVA platforms signal growing competition, with market dynamics now centered on capital access, OR footprint, and robust instrument ecosystems rather than platform availability alone.

Capital Cost Concentration Limiting Platform Penetration in Community Settings

High capital costs significantly limit the adoption of laparoscopic platforms in the United States market. Intuitive reported that the standard sale or lease of a da Vinci system costs between USD 0.6 million and USD 3.1 million, with annual service fees ranging from USD 95,000 to USD 225,000 and per-procedure costs between USD 900 and USD 3,700. While large academic institutions and major health networks can absorb these costs, community hospitals and smaller surgical centers with limited budgets face challenges. This cost disparity slows the adoption of robotic technology in smaller facilities, creating a divided demand where some providers invest in advanced robotics while others opt for cost-effective disposables and incremental upgrades. Modular systems from newer entrants may address this gap over time, but current pricing remains a barrier to faster growth.

Other drivers and restraints analyzed in the detailed report include:

- OR Staffing Constraints Driving Demand for Integrated Workflow Platforms

- Energy and Stapling Premiumization Expanding Per-Procedure Revenue

- CMS Reimbursement Compression Narrowing Margin Headroom for Common Procedures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Energy Devices held a 29.45% share of the United States laparoscopic devices market, leading the product category. This reflects a shift from traditional electrosurgical methods to advanced vessel-sealing and tissue-management technologies, streamlining minimally invasive procedures. These devices are widely used in general surgery, gynecology, colorectal treatments, and bariatric surgery, ensuring consistent demand.

Hand Instruments, Closure and Stapling Devices, Access Devices, and Visualization Systems remain essential but are evolving with a focus on disposables, integrated workflows, and enhanced imaging. Single-use access products simplify logistics in outpatient settings, while advanced visualization stacks gain traction for their 3D, 4K, or fluorescence capabilities. Robotic-Assisted Laparoscopy Platforms and Instruments are projected to grow at an 8.12% CAGR through 2031, driven by Medtronic's Hugo, Johnson & Johnson's OTTAVA, and Intuitive's expanding installed base.

List of Companies Covered in this Report:

- Aesculap

- Applied Medical Resources

- Asensus Surgical US, Inc.

- Beckton Dickinson

- Boston Scientific

- Conmed

- The Cooper Companies

- ERBE USA, Inc.

- Ethicon, Inc.

- Intuitive Surgical, Inc.

- KARL STORZ Endoscopy-America, Inc.

- LivsMed USA Inc.

- Mediflex Surgical Products Corporation

- Medtronic

- Olympus

- Richard Wolf Medical Instruments Corporation

- Smiths Group

- Stryker

- Teleflex

- Virtual Incision Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hospital Outpatient and ASC Migration for Routine Laparoscopy

- 4.2.2 High Obesity Burden Sustaining Bariatric and General Surgery Demand

- 4.2.3 Premiumization of Energy, Powered Stapling, and 4K/3D Imaging

- 4.2.4 Robotic-Enabled Minimally Invasive Surgery Expansion in General Surgery

- 4.2.5 OR Staffing Variability Favoring Integrated Workflow Platforms

- 4.2.6 Smoke Evacuation and Stable Low-Pressure Insufflation Adoption

- 4.3 Market Restraints

- 4.3.1 High Capital and Disposable Cost Burden

- 4.3.2 Robotic Substitution of Conventional Laparoscopic Categories

- 4.3.3 Reimbursement Compression in Common Laparoscopic Procedures

- 4.3.4 FDA Quality and Supply Chain Scrutiny on Device Availability

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Visualization Systems and Laparoscopes

- 5.1.1.1 Rigid Laparoscopes

- 5.1.1.2 Flexible / Deflectable Laparoscopes

- 5.1.1.3 Camera Heads and Video Processors

- 5.1.1.4 Light Sources

- 5.1.1.5 3D / 4K / Fluorescence Imaging Platforms

- 5.1.2 Access Devices

- 5.1.2.1 Trocars and Cannulas

- 5.1.2.2 Veress Needles

- 5.1.2.3 Others

- 5.1.3 Insufflation and Smoke Management

- 5.1.3.1 Insufflators

- 5.1.3.2 Tubing Sets

- 5.1.3.3 Smoke Evacuation Systems

- 5.1.4 Hand Instruments

- 5.1.4.1 Graspers

- 5.1.4.2 Dissectors

- 5.1.4.3 Scissors

- 5.1.4.4 Needle Holders

- 5.1.4.5 Retractors

- 5.1.4.6 Others

- 5.1.5 Energy Devices

- 5.1.5.1 Advanced Bipolar Vessel Sealing

- 5.1.5.2 Ultrasonic Energy Devices

- 5.1.5.3 Others

- 5.1.6 Closure and Stapling Devices

- 5.1.6.1 Endoscopic Linear Staplers

- 5.1.6.2 Circular Staplers Used in Laparoscopic Procedures

- 5.1.6.3 Reloads and Buttressing Materials

- 5.1.6.4 Sutures and Ligation Clips

- 5.1.7 Suction, Irrigation, and Retrieval Devices

- 5.1.7.1 Suction-Irrigation Systems

- 5.1.7.2 Specimen Retrieval Bags

- 5.1.7.3 Cholangiography and Ancillary Devices

- 5.1.8 Robotic-Assisted Laparoscopy Platforms and Accessories

- 5.1.8.1 Multiport Robotic Platforms

- 5.1.8.2 Miniaturized / Table-Mounted Robotic Platforms

- 5.1.8.3 Robotic-Compatible Access and Insufflation Accessories

- 5.1.8.4 Robotic Stapling and Energy Instruments

- 5.1.1 Visualization Systems and Laparoscopes

- 5.2 By Application

- 5.2.1 General Surgery

- 5.2.2 Bariatric Surgery

- 5.2.3 Gynecological Surgery

- 5.2.4 Urological Surgery

- 5.2.5 Colorectal Surgery

- 5.2.6 Thoracic and Other Laparoscopic-Adjacent MIS Procedures

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialty Clinics and Office-Based Surgical Centers

- 5.3.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Aesculap, Inc.

- 6.3.2 Applied Medical Resources Corporation

- 6.3.3 Asensus Surgical US, Inc.

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 Boston Scientific Corporation

- 6.3.6 CONMED Corporation

- 6.3.7 CooperSurgical, Inc.

- 6.3.8 ERBE USA, Inc.

- 6.3.9 Ethicon, Inc.

- 6.3.10 Intuitive Surgical, Inc.

- 6.3.11 KARL STORZ Endoscopy-America, Inc.

- 6.3.12 LivsMed USA Inc.

- 6.3.13 Mediflex Surgical Products Corporation

- 6.3.14 Medtronic plc

- 6.3.15 Olympus Corporation

- 6.3.16 Richard Wolf Medical Instruments Corporation

- 6.3.17 Smith & Nephew plc

- 6.3.18 Stryker Corporation

- 6.3.19 Teleflex Incorporated

- 6.3.20 Virtual Incision Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment