|

시장보고서

상품코드

2064479

남성 유방암 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Male Breast Cancer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

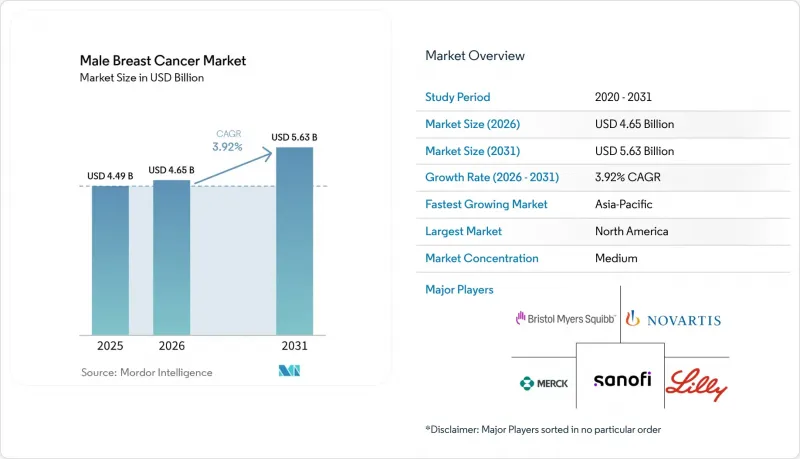

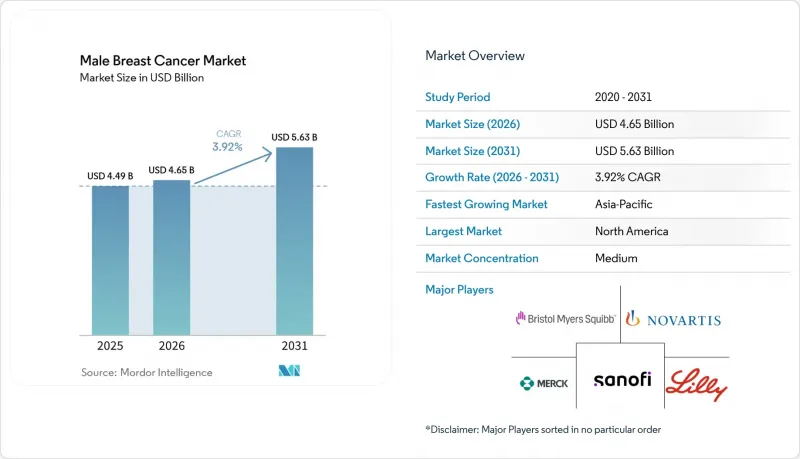

Mordor Intelligence에 의하면, 남성 유방암 시장 규모는 2025년 44억 9,000만 달러로 평가되었고, 2026년에는 46억 5,000만 달러로 추정되고, 2026-2031년 CAGR 3.92%로 성장을 지속할 전망이며, 2031년에는 56억 3,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 암 유형별(침윤성 유관암, 비침윤성 유관암, 파제트병, 염증성 유방암, 침윤성 소엽암), 진단별(영상 검사, 기타), 치료법별(국소 요법, 전신 요법, 지지 요법), 최종 사용자별(병원, 전문 클리닉, 학술 기관, 외래수술센터(ASC)), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 남성 유방암 시장 동향 및 인사이트

진단 건수와 인지도 상승

남성 유방암은 오랫동안 여성 유방암에 비해 발견이 늦어지고 있으며, 발표된 연구 결과에 따르면 남성의 평균 진단 지연 기간은 14-21개월인 반면, 여성은 1-4개월인 것으로 나타났습니다. 이러한 지연은 남성 유방암 시장에 직접적인 상업적 영향을 미칩니다. 왜냐하면, 발견이 늦어지면 증상이 이미 진행된 후에 환자가 더 많은 자원이 필요한 치료 과정으로 내몰리게 되기 때문입니다. 임상 보고에 따르면, 남성의 증례는 여전히 체계적인 검사보다는 자가 검진을 통해 발견되는 경우가 많으며, 따라서 영상 검사나 생검에 대한 수요는 일반 시민 및 일선 의사를 대상으로 한 계몽 활동과 밀접하게 연관되어 있습니다. 더 많은 일반 개업의들이 이 질환을 조기에 인식하게 된다면, 발표 건수는 영상 검사, 병리 검사, 내분비 치료로 더 신속하게 이어질 것이며, 그 결과 특정 의료 현장뿐만 아니라 남성 유방암 시장 전체 수요가 확대될 것입니다. 조기 진단은 시간이 지남에 따라 치료 방식도 변화시킵니다. 왜냐하면, 광범위한 전이가 확산되기 전에 발견된 환자는 의사의 지시에 따라 장기간 전신 치료를 받고 경과 관찰을 받을 가능성이 높아지기 때문입니다.

CDK4/6, PARP, HER2를 표적으로 하는 치료 옵션의 확대

실세계 데이터가 처음으로 HR 양성·HER2 음성 전이성 질환을 앓고 있는 남성 환자에 대한 CDK4/6 억제제 사용 확대에 기여한 이래, 남성 유방암 시장의 치료 선택지는 점차 확대되고 있습니다. 그 후, 2024년 9월 고위험 조기 유방암에 대한 보조요법으로 리보시클리브가 FDA 승인을 받으면서, 이 약물은 조기 유방암에 대한 적용 범위를 더욱 확대했습니다. 이 적응증 표기에는 NATALEE 검사의 대상 집단에 남성이 명시적으로 포함되어 있었습니다. 튀르키예에서 수집된 실제 임상 데이터 역시 남성 환자군에서 이 약물군의 유효성을 뒷받침하고 있으며, 전이성 HR 양성·HER2 음성 질환의 1차 치료에서 팔보시크리브의 전체 반응률은 84.0%, 리보시크리브는 76.2%였습니다. PARP 억제제는 성장에 또 다른 동력을 더하게 될 것입니다. 독일 등록부에 따르면, 조기 유방암 남성 환자의 12.6%가 OlympiA 프레임워크에 따른 올라파리브 보조요법 적격 기준을 충족하고 있으며, 이는 희귀질환의 맥락에서 매우 의미 있는 결과입니다. 2024년 10월의 이나보리시브와 2025년 1월의 다포타맙·델크스테칸과 같은 신규 승인은 남성 유방암 시장이 이미 여성 유방암 치료를 형성하고 있는 것과 동일한 표적 치료 체계에 점차 접근할 수 있게 되고 있음을 보여줍니다.

환자 수가 적어 임상 검사와 투자 대비 효과를 제한하고 있습니다.

이 질환의 희귀성은 남성 유방암 시장에 여전히 구조적인 걸림돌로 작용하고 있습니다. 왜냐하면 2026년 미국의 남성 신규 환자 수는 2,670건에 그칠 것으로 예상되는 반면, 여성 환자 수는 31만 6,950건에 달할 것으로 전망되기 때문입니다. 이러한 격차로 인해 남성만을 대상으로 한 중재 연구의 피험자 모집이 어려워지며, 그 결과 규제 당국, 보험사, 지침 작성자가 활용할 수 있는 성별별 증거의 양이 제한될 수밖에 없습니다. 독일의 레지스트리 분석에 따르면, 그 격차가 얼마나 큰지가 드러나고 있습니다. 레지스트리에 등록된 남성의 12.6%에서 47.6%가 임상시험 참가 기준을 충족했음에도 불구하고, 주요 보조 요법 시험 참가자 중 남성의 비율은 고작 0.3%에서 0.6%에 그쳤기 때문입니다. 이 때문에 남성 유방암 시장은 남성을 대상으로 한 직접적인 3상 임상시험이 아닌, 여성 데이터를 외삽하거나 실제 임상 데이터에 의존할 수밖에 없으며, 그 결과 신약의 보험 급여 결정이 지연될 가능성이 있습니다. 이와 유사한 제약은 PARP 억제제, 차세대 내분비 요법제, 새로운 병용 요법에서 특히 두드러지며, 2026년 현재에도 남성 특유의 예후에 관한 근거는 여전히 제한적입니다.

부문별 분석

2025년 기준으로 침윤성 유관암은 76.23%의 점유율을 차지했으며, 암 유형별로는 남성 유방암 시장의 주요 수익 기반이 되고 있습니다. 이러한 집중도는 침윤성 유관암이 남성 유방암 사례의 대부분을 차지하며, 일반적으로 에스트로겐 수용체 양성이라는 점을 보여주는 광범위한 임상 문헌과 일치합니다. 이 아형은 일반적으로 호르몬 의존성이기 때문에 남성 유방암 시장의 치료 양상은 화학요법 단독이 아닌 내분비 요법, CDK4/6 억제제, 그리고 장기적인 추적 관찰 기간과 밀접한 관련이 있습니다. 유관암이 주를 이루고 있다는 점은 병리 검사 및 수용체 검사의 중요성을 더욱 높여주고 있습니다. 왜냐하면 치료법 선택은 진단 시 ER, PR, HER2의 상태를 명확히 파악하는 데 달려 있기 때문입니다. 염증성 유방암이나 파제트병과 같은 희귀한 아형은 수익 규모는 작지만, 침습성이 더 높은 임상 경과를 보이는 경우가 많기 때문에 치료 강도가 높은 사례에 해당합니다.

비침윤성 유관암은 2031년까지 연평균 성장률(CAGR) 4.48%로 확대될 것으로 예측되며, 남성 유방암 시장에서 가장 빠르게 성장하는 암 유형이 될 전망입니다. 그 주된 이유는 BRCA 유전자 보유자에 대한 생식세포 계통 검사 및 모니터링이 확대됨에 따라, 침윤성 암으로 진행되기 전에 발견될 가능성이 높아지고 있기 때문입니다. 이러한 초기 단계의 사례 구성은 영상 검사, 생검, 계획적 수술 증가로 이어지며, 남성 유방암 치료 분야의 일부를 진행기 단계의 생명 연장 치료에서 관리형 조기 개입으로 점차 전환시키고 있습니다. 침윤성 소엽암은 정상 남성의 유방 해부학적으로 소엽 조직이 희박하기 때문에 남성에게서 여전히 드물며, 남성 유방암 시장에서 차지하는 상업적 비중은 제한적입니다. 그럼에도 불구하고, 이러한 비교적 드문 형태들은 특정 환자에게 있어 전문적인 병리학적 검토나 호르몬 요법을 중심으로 한 관리의 필요성을 확대하기 때문에 임상적으로는 여전히 중요합니다.

2025년에는 영상 검사가 진단 부문의 38.28%를 차지했으며, 남성 유방암 시장의 진단 관련 지출에서 가장 큰 비중을 차지했습니다. 실제로 유방촬영술과 초음파 검사는 여전히 주요 1차 검사 수단이며, 미국 외과 종양학 지침에서는 만져지는 종괴의 성질이 불분명한 25세 이하 남성에게는 초음파 검사를, 25세 이상 남성에게는 유방촬영술을 권장하고 있습니다. 이러한 구조 덕분에 영상 촬영 건수는 안정적으로 유지되고 있습니다. 왜냐하면 대부분의 환자는 체계적인 선별검사를 통해가 아니라, 덩어리나 국소적인 변화를 발견한 후에 진료를 받기 때문입니다. PET나 MRI의 활용 비율은 낮지만, 진행성 암의 병기 분류나 치료 효과 평가, 특히 임상의가 더 광범위한 병변의 전체적인 상황을 파악해야 하는 경우에는 여전히 중요합니다. 인지도가 높아짐에 따라, 남성 유방암 분야에서 영상 검사 수요는 전이 검사뿐만 아니라 조기 검진에 의해서도 지속적으로 뒷받침될 것으로 보입니다.

병리 검사는 2031년까지 연평균 성장률(CAGR) 5.22%를 기록하며 가장 빠른 성장이 전망되는 진단 분야로, 남성 유방암 시장 전체에서 바이오마커 기반의 의사 결정으로의 전환을 반영하고 있습니다. ER, PR, HER2 수용체 프로파일링은 현재 치료법 선택에 있어 필수적인 요소가 되었으며, 생식세포 계통 BRCA 검사도 선택적 사용에서 새로 진단받은 남성을 대상으로 한 표준 권장 사항으로 전환되고 있습니다. 또한, PIK3CA 돌연변이 검출용 이나볼리시브와 함께 FoundationOne Liquid CDx가 승인된 사실에서도 알 수 있듯이, 동반 진단은 환자 1인당 수익을 확대되고 있습니다. 2026년 1월 CMS가 TruSight Oncology Comprehensive에 대해 내린 결정은 메디케어 수급자들이 더 광범위한 유전체 프로파일링 서비스를 이용하기 쉽게 만들었으며, 남성 유방암 시장에 추가적인 활력을 불어넣었습니다. 장기적으로 보면, 이는 진단에서 가치가 주로 영상 검사뿐만 아니라 해석과 분자 수준에서의 계층화를 통해 창출되게 될 것임을 의미합니다.

지역별 분석

2025년, 북미는 남성 유방암 시장 규모의 42.39%를 차지했으며, 모든 지역 중 1위를 유지했습니다. 이 지역의 강점은 확립된 종양학 인프라, 첨단 치료법에 대한 광범위한 보험 급여, 그리고 남성만을 대상으로 한 무작위 배정 연구 데이터가 여전히 제한적인 상황에서도 남성에게의 적용을 뒷받침하는 견고한 실제 임상 데이터(REW) 생태계에 있습니다. 2024년 ASCO 및 외과종양학회 발표를 통해, 남성 유방암 환자를 대상으로 한 보편적인 생식세포계 유전자 검사에 관한 최신 정보도 미국 남성 유방암 시장의 부문에서 보다 일관된 바이오마커를 규명하고, 이를 바탕으로 한 치료법 활용을 뒷받침하고 있습니다. POLARIS 임상시험에서 도출된 실제 임상 데이터는 이러한 근거를 더욱 강화하는 것으로, 팔보시클리브로 치료받은 남성 환자의 경우 실제 임상에서 무재발 생존 기간의 중앙값이 19.8개월로 나타났습니다. 캐나다에서는 남성 환자를 대상으로 한 리보시클리브 관련 생식세포계 검사에 대한 권고 사항과 규제상 지원 체계가 잘 갖춰져 있어, 이에 따라 북미는 남성 유방암 시장에서 가장 발전된 지역 클러스터로서의 위상을 유지하고 있습니다.

유럽은 독일, 프랑스, 영국, 이탈리아를 필두로 남성 유방암 시장에서 여전히 2위 지역 그룹의 위치를 유지하고 있습니다. 이 지역은 남성을 명시적으로 대상으로 한 임상시험 프로그램을 거쳐, 리보시크리브가 유럽에서 조기 유방암의 보조 요법으로 승인됨에 따라 큰 탄력을 받았으며, 이로 인해 조기 유방암 남성 환자들의 치료 접근성에 대한 신뢰도가 높아졌습니다. 독일의 등록 데이터에 따르면, 조기 유방암 남성 환자의 47.6%가 NATALEE 임상시험의 리보시클리브 적격 기준을 충족하고 있으며, 이는 해당 지역의 남성 유방암 시장에서 미치료 또는 치료가 불충분한 환자층에 큰 기회가 존재함을 시사합니다. 이러한 진전이 있음에도 불구하고, 유럽에서는 여전히 임상 검사의 타당성과 일상적인 치료로의 도입 사이에 격차가 존재하며, 성장은 신규 승인뿐만 아니라 시행 체계의 철저함에도 크게 좌우될 것입니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 5.87%를 기록하며 성장할 것으로 예상되며, 남성 유방암 시장에서 가장 빠르게 확대될 지역이 될 전망입니다. 중국이 주요 원동력으로 작용하고 있으며, 2021년에는 남성 신규 환자 1만 6,956명이 기록되었고, 지난 30년 동안 세계 평균을 훨씬 웃도는 속도로 발생률이 증가하고 있습니다. 또한, 동아시아에서는 남성 유방암의 HER2 양성률이 17%로 보고되고 있는데, 이는 서유럽에서 보고된 8% 수준을 크게 상회하여 HER2 표적 치료에 대한 지역적 수요를 더욱 높이고 있습니다. 일본에서는 BRCA1 및 BRCA2 생식세포 계통 검사에 대한 국민건강보험 적용과, 진료 지침에 남성 환자의 질환을 포함시키는 등의 조치를 통해 치료의 보급이 촉진되고 있습니다. 중동 및 아프리카와 남미는 현재로서는 시장 규모가 작지만, GCC(걸프협력회의) 국가들의 인프라 투자, 인식 제고 프로그램, 보험 제도의 확충으로 인해, 자원이 부족한 지역에서는 여전히 진행 단계에서 진료를 받는 경우가 많지만, 진단 및 치료에 대한 접근성이 서서히 개선되고 있어 남성 유방암 시장의 장기적인 성장 기반 중 일부를 이루고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the male breast cancer market size is expected to grow from USD 4.49 billion in 2025 to USD 4.65 billion in 2026 and is forecast to reach USD 5.63 billion by 2031 at 3.92% CAGR over 2026-2031.

This report is Segmented by Cancer Type (Infiltrating Ductal, DCIS, Paget Disease, Inflammatory, Invasive Lobular, Diagnosis, Imaging, and More), by Treatment Modality (Local Therapy, Systemic Therapy, Supportive Care), End User (Hospitals, Specialty Clinics, Academic Centers, Ascs) and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Male Breast Cancer Market Trends and Insights

Rising Diagnosis And Awareness

Male breast cancer has long been identified later than female breast cancer, and published evidence placed average diagnostic delay in men at 14 to 21 months compared with 1 to 4 months in women. That delay has direct commercial implications for the male breast cancer market because late recognition pushes patients into more resource-intensive treatment pathways after symptoms have already advanced. Clinical reports also showed that male presentation is still often triggered by self-detection rather than structured examination, which keeps imaging and biopsy demand closely tied to awareness efforts among the public and frontline physicians. As more general practitioners recognize the disease earlier, referral volumes move faster into imaging, pathology, and endocrine therapy, and that broadens demand across the male breast cancer market rather than in one care setting alone. Earlier diagnosis also changes the treatment mix over time, because patients identified before wide metastatic spread are more likely to receive longer courses of guided systemic care and monitored follow-up.

Expansion Of CDK4/6, PARP, And HER2-Targeted Options

The treatment range in the male breast cancer market has widened since real-world evidence first helped extend CDK4/6 inhibitor use to men with HR-positive, HER2-negative metastatic disease. Ribociclib then moved further into early disease after the September 2024 FDA approval for adjuvant use in high-risk early breast cancer, and that label explicitly included men in the NATALEE trial population. Real-world clinical data from Turkey also supported class performance in men, with overall response rates of 84.0% for palbociclib and 76.2% for ribociclib in first-line treatment of metastatic HR-positive, HER2-negative disease. PARP inhibitors add another growth layer because a German registry found that 12.6% of men with early breast cancer met adjuvant olaparib eligibility criteria under the OlympiA framework, which is meaningful in a rare-disease setting. New approvals, such as inavolisib in October 2024 and datopotamab deruxtecan in January 2025, show that the male breast cancer market is gradually gaining access to the same targeted treatment architecture that already shapes female breast cancer care.

Tiny Patient Pool Constrains Trials And ROI

The rare nature of the disease remains a structural drag on the male breast cancer market because the United States is expected to record only 2,670 new male cases in 2026, compared with 316,950 female cases. That gap makes male-only interventional trials difficult to recruit, and weak recruitment then limits the amount of sex-specific evidence available for regulators, payers, and guideline writers. A German registry analysis showed how wide that gap remains, since men represented only 0.3% to 0.6% of participants in major adjuvant trials even though 12.6% to 47.6% of men in the registry would have met trial eligibility criteria. This keeps the male breast cancer market dependent on extrapolated female data and real-world evidence rather than direct male Phase III programs, which can slow reimbursement decisions for newer drugs. The same limitation is especially relevant for PARP inhibitors, next-generation endocrine agents, and newer combination approaches, where male-specific outcome evidence is still limited as of 2026.

Other drivers and restraints analyzed in the detailed report include:

- Wider Germline BRCA And Tumor Biomarker Testing

- Better Oncology Access In Emerging Markets

- Stigma And Low Clinical Suspicion Delay Diagnosis

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Infiltrating ductal carcinoma accounted for 76.23% share in 2025, which made it the central revenue base for the male breast cancer market by cancer type. That concentration is consistent with broader clinical literature showing that infiltrating ductal tumors make up most male breast cancer cases and are usually estrogen receptor positive. Because this subtype is usually hormone-driven, the care pattern in the male breast cancer market stays closely tied to endocrine therapy, CDK4/6 inhibitors, and long follow-up periods rather than to chemotherapy alone. The dominance of ductal disease also makes pathology and receptor testing more important, because treatment selection depends on defining ER, PR, and HER2 status clearly at diagnosis. Rare subtypes such as inflammatory breast cancer and Paget disease represent small revenue pools, but they still create high-intensity treatment episodes because they often present with more aggressive clinical behavior.

Ductal carcinoma in situ is forecast to expand at 4.48% CAGR through 2031, making it the fastest-growing cancer type within the male breast cancer market. The key reason is that wider germline testing and surveillance in BRCA carriers are increasing the chance of detection before invasive transformation. This earlier-stage mix supports more imaging, biopsy, and planned surgery, and it gradually shifts part of the male breast cancer industry toward controlled early intervention rather than late-stage rescue treatment. Invasive lobular carcinoma remains uncommon in men because lobular tissue is sparse in normal male breast anatomy, so its commercial weight stays limited in the male breast cancer market. Even so, these less common forms still matter clinically because they broaden the need for specialized pathology review and hormone-focused management in selected patients.

Imaging captured 38.28% of the diagnosis segment in 2025, which gave it the largest position within diagnostic spending in the male breast cancer market. In practice, mammography and ultrasound remain the main first-line tools, and U.S. surgical oncology guidance supports ultrasound first for men under 25 with indeterminate palpable masses and mammography for men aged 25 or older. That structure keeps imaging volume steady because most patients still present after noticing a lump or local change rather than through organized screening. PET and MRI occupy smaller positions, but they remain important for staging and treatment response assessment in advanced disease, especially when clinicians need a broader disease map. As awareness improves, imaging demand in the male breast cancer industry will continue to be supported by earlier referral rather than only by metastatic workup.

Pathology is the fastest-growing diagnostic category at 5.22% CAGR through 2031, reflecting the move toward biomarker-led decisions across the male breast cancer market. Receptor profiling for ER, PR, and HER2 is now fundamental to therapy choice, and germline BRCA testing has also shifted from selective use to a standard recommendation for newly diagnosed men. Companion diagnostics are also deepening revenue per patient episode, as shown by the approval of FoundationOne Liquid CDx alongside inavolisib for PIK3CA mutation detection. The January 2026 CMS decision on TruSight Oncology Comprehensive gave the male breast cancer market another push by making broader genomic profiling more accessible to Medicare beneficiaries. Over time, this means more of the value in diagnosis will come from interpretation and molecular stratification rather than from imaging alone.

Geography Analysis

North America accounted for 42.39% share of the male breast cancer market size in 2025, which kept it in the lead among all regions. The region's strength comes from established oncology infrastructure, broad reimbursement for advanced therapies, and a stronger real-world evidence ecosystem that supports male use even when randomized male-only data remain limited. The 2024 ASCO and Society of Surgical Oncology update on universal germline testing for men with breast cancer also supports more consistent biomarker identification and downstream treatment use in the U.S. segment of the male breast cancer market. Real-world evidence from the POLARIS study further strengthened this base, with male patients treated with palbociclib showing a median real-world progression-free survival of 19.8 months. Canada adds to the region's depth through aligned germline testing recommendations and regulatory support for ribociclib in male patients, which keeps North America the most developed regional cluster in the male breast cancer market.

Europe remained the second-largest regional grouping in the male breast cancer market, led by Germany, France, the United Kingdom, and Italy. The region gained an important boost when ribociclib was approved in Europe for adjuvant early breast cancer after a trial program that explicitly included men, which improved the credibility of male access in earlier-stage disease. Germany's registry data also showed that 47.6% of men with early breast cancer met ribociclib eligibility criteria under NATALEE, which points to sizable untreated or undertreated opportunity within the regional male breast cancer market. Even with this progress, Europe still faces a translation gap between trial eligibility and routine uptake, which means growth depends as much on implementation discipline as on new approvals.

Asia-Pacific is projected to grow at 5.87% CAGR through 2031, making it the fastest-expanding regional block in the male breast cancer market. China is the main driver because it recorded 16,956 new male cases in 2021 and has seen incidence rise much faster than the global average over the last 3 decades. East Asia also has a reported HER2 positivity rate of 17% in male breast cancer, which is materially higher than the 8% level reported for Europe and the United States, and that creates stronger regional demand for HER2-directed therapy. Japan supports uptake through national insurance coverage for BRCA1 and BRCA2 germline testing and through clinical guidance that includes male disease in practice frameworks. Middle East and Africa as well as South America are smaller today, but they remain part of the longer runway for the male breast cancer market as GCC infrastructure investment, awareness programs, and insurance expansion gradually improve diagnosis and treatment access despite persistent late-stage presentation in several lower-resource settings.

- AstraZeneca

- Bristol-Myers Squibb

- Daiichi Sankyo

- Eisai

- Eli Lilly and Company

- Exact Sciences

- F. Hoffmann-La Roche Ltd / Genentech, Inc.

- GE HealthCare Technologies Inc.

- Gilead Sciences

- Hologic

- Illumina

- Merck

- Novartis

- Pfizer

- Sanofi

- Siemens Healthineers

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

- Thermo Fisher Scientific

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Diagnosis and Awareness

- 4.2.2 Expansion of CDK4/6, PARP, And HER2-Targeted Options

- 4.2.3 Wider Germline BRCA and Tumor Biomarker Testing

- 4.2.4 Better Oncology Access in Emerging Markets

- 4.2.5 Male-Inclusion Pressure in Breast Cancer Trials

- 4.2.6 Real-World-Evidence Label Expansion for Men

- 4.3 Market Restraints

- 4.3.1 Tiny Patient Pool Constrains Trials and ROI

- 4.3.2 Stigma And Low Clinical Suspicion Delay Diagnosis

- 4.3.3 Tamoxifen Side Effects and Poor Adherence

- 4.3.4 Women-Centric Reimbursement and Evidence Pathways

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Cancer Type

- 5.1.1 Infiltrating Ductal Carcinoma

- 5.1.2 Ductal Carcinoma In Situ

- 5.1.3 Paget Disease of the Nipple

- 5.1.4 Inflammatory Breast Cancer

- 5.1.5 Invasive Lobular Carcinoma

- 5.2 By Diagnosis

- 5.2.1 Imaging

- 5.2.1.1 Mammography

- 5.2.1.2 Ultrasound

- 5.2.1.3 Magnetic Resonance Imaging

- 5.2.1.4 Computed Tomography

- 5.2.1.5 Positron Emission Tomography

- 5.2.2 Pathology

- 5.2.2.1 Core Needle Biopsy

- 5.2.2.2 Fine Needle Aspiration Biopsy

- 5.2.2.3 Excisional Biopsy

- 5.2.3 Biomarker and Genetic Testing

- 5.2.3.1 Estrogen Receptor / Progesterone Receptor Testing

- 5.2.3.2 HER2 Testing

- 5.2.3.3 Germline BRCA and Hereditary Cancer Panel Testing

- 5.2.3.4 Tumor Genomic Profiling

- 5.2.1 Imaging

- 5.3 By Treatment Modality

- 5.3.1 Local Therapy

- 5.3.1.1 Surgery

- 5.3.1.1.1 Mastectomy

- 5.3.1.1.2 Breast-Conserving Surgery

- 5.3.1.1.3 Sentinel Lymph Node Biopsy

- 5.3.1.1.4 Axillary Lymph Node Dissection

- 5.3.1.2 Radiation Therapy

- 5.3.1.1 Surgery

- 5.3.2 Systemic Therapy

- 5.3.2.1 Endocrine Therapy

- 5.3.2.1.1 Tamoxifen

- 5.3.2.1.2 Aromatase Inhibitor Plus GnRH Analogue

- 5.3.2.1.3 Fulvestrant

- 5.3.2.2 Chemotherapy

- 5.3.2.2.1 Neoadjuvant Chemotherapy

- 5.3.2.2.2 Adjuvant Chemotherapy

- 5.3.2.2.3 Metastatic-Line Chemotherapy

- 5.3.2.3 Targeted Therapy

- 5.3.2.3.1 CDK4/6 Inhibitors

- 5.3.2.3.2 HER2-Targeted Therapy

- 5.3.2.3.3 PARP Inhibitors

- 5.3.2.3.4 PI3K / AKT / mTOR-Pathway Therapies

- 5.3.2.4 Immunotherapy

- 5.3.2.1 Endocrine Therapy

- 5.3.3 Supportive Care

- 5.3.1 Local Therapy

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Cancer Specialty Clinics

- 5.4.3 Academic and Research Centers

- 5.4.4 Ambulatory Surgical Centers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AstraZeneca PLC

- 6.3.2 Bristol Myers Squibb Company

- 6.3.3 Daiichi Sankyo Company, Limited

- 6.3.4 Eisai Co., Ltd.

- 6.3.5 Eli Lilly and Company

- 6.3.6 Exact Sciences Corporation

- 6.3.7 F. Hoffmann-La Roche Ltd / Genentech, Inc.

- 6.3.8 GE HealthCare Technologies Inc.

- 6.3.9 Gilead Sciences, Inc.

- 6.3.10 Hologic, Inc.

- 6.3.11 Illumina, Inc.

- 6.3.12 Merck & Co., Inc.

- 6.3.13 Novartis AG

- 6.3.14 Pfizer Inc.

- 6.3.15 Sanofi S.A.

- 6.3.16 Siemens Healthineers AG

- 6.3.17 Sun Pharmaceutical Industries Ltd.

- 6.3.18 Teva Pharmaceutical Industries Ltd.

- 6.3.19 Thermo Fisher Scientific Inc.

- 6.3.20 Viatris Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment