|

시장보고서

상품코드

2064481

케미컬 필 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Chemical Peel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

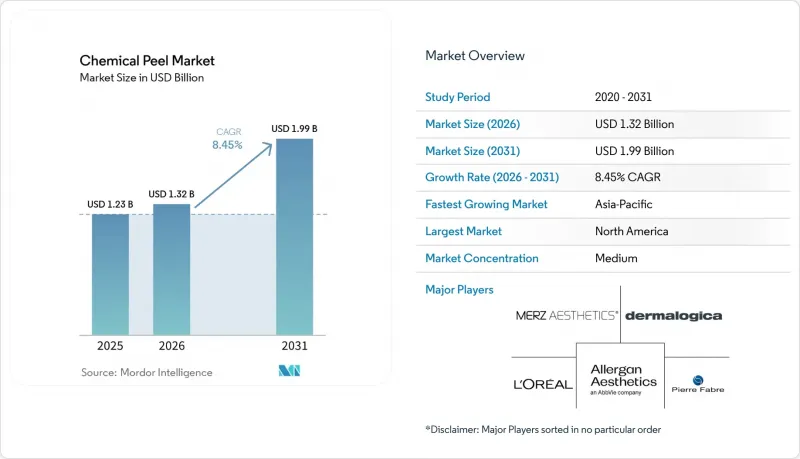

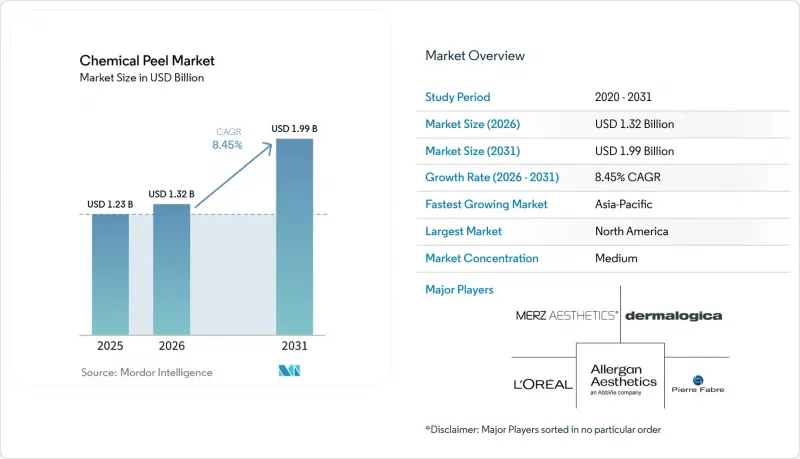

Mordor Intelligence에 의하면, 케미컬 필 시장 규모는 2025년에 12억 3,000만 달러로 평가되었고, 2026년 13억 2,000만 달러로 추정되고, 2031년까지 19억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 8.45%를 나타낼 전망입니다.

본 보고서는 제품별(글리콜산, 젖산, 기타), 필링 깊이별(표피층, 중층, 심층, 기타), 용도별(여드름 흉터, 여드름 후 색소 침착, 기타), 최종 용도별(피부과 클리닉, 기타), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 달러(USD) 기준 금액으로 제시되어 있습니다.

세계의 케미컬 필 시장 동향 및 인사이트

저침습적 피부 재생 치료에 대한 수요 증가

회복 기간이 짧은 치료에 대한 지속적인 수요로 인해, 침습성이 높은 피부 재생 치료 대신 표층 및 중층 필링을 선택하는 환자가 늘고 있습니다. 2026년 2월에 발표된 AAFPRS의 2025년 연례 조사에 따르면, 비침습적 시술이 전체 안면 시술의 80%를 차지하고 있으며, 안면 시술 건수가 19% 증가한 것으로 나타났습니다. 이는 케미컬 필 시장 전체의 시술 건수 증가를 뒷받침하는 것입니다. 이러한 변화가 중요하게 여겨지는 이유는 시술을 반복하기 쉽고, 일상생활 일정에 포함시키기 쉬우며, 클리닉에서 일반적인 치료 메뉴에 포함시키기 쉽기 때문입니다. 또한, 환자층도 젊어지고 있으며, 30세 이하의 환자들이 조기에 예방 치료를 선택하는 경향이 있어 잠재적인 치료 주기가 더 길어지고 있습니다. 이러한 추세로 인해 시술자들은 시술 건수가 적은 심층 리서페이싱에만 의존하지 않고, 경증 및 중등도 치료를 중심으로 한 재방문 프로토콜을 구축해야 할 필요에 직면해 있습니다.

여드름, 색소 침착, 광노화 사례 수 증가

케미컬 필 시장은 의료 및 미용 두 부문 모두에서 여전히 규모가 큰 여드름, 색소 침착, 광노화 등의 증상군으로부터 꾸준한 수요를 계속해서 끌어모으고 있습니다. 캘리포니아 블루쉴드는 2026년 2월 발표된 정책에서 여드름이 전 세계 13세에서 18세 청소년의 80%에게 영향을 미치고 있으며, 일광각화증이 미국 성인 인구의 11%에서 26%에게 영향을 미치고 있다고 밝혔으며, 이는 글리콜산, 살리실산, TCA 필링에 대한 지속적인 기본적인 수요를 뒷받침하고 있습니다. 2025년 4월 발간된 ‘연방 공무원 프로그램 의료 지침서’에서도 전신 항생제에 반응하지 않는 활동성 여드름에 대해서는 40%-70% 농도의 AHA 필링을 의학적으로 필요한 시술로 분류하고 있으며, 또한, 10개 이상의 일광각화증이 확인되는 경우에는 진피 필링을 의학적으로 필요한 시술로 인정하고 있습니다. 이러한 보험사의 인정을 통해 선택적 미용 시술에서 흔히 나타나는 가격 민감도가 완화되어, 피부과 클리닉 입장에서는 수요의 하한선을 더 쉽게 예측할 수 있게 됩니다. 또한, 많은 환자의 치료 경로에서 더 낮은 시술 비용으로 경쟁적인 치료 효과를 제공할 수 있기 때문에 케미컬 필은 새로운 외용제와 비교하더라도 임상적으로 의미 있는 선택지로 남아 있을 것입니다.

중층 및 심층 필링 시 발생할 수 있는 이상반응의 위험

중층 및 심층 필링은 여전히 실질적인 보급의 한계에 직면해 있습니다. 왜냐하면, 훈련을 받은 의료진이 프로토콜을 적절히 관리하지 않을 경우, 이상반응의 위험이 급격히 높아지기 때문입니다. 2026년 1월 AIME 회의에서 발표된 데이터에 따르면, 페놀·크로톤 오일을 이용한 심층 필링은 평균 8.2년의 시각적 노화 역전 효과를 가져온다는 것이 밝혀졌습니다. 그러나 부정맥의 위험을 피하기 위해서는 얼굴을 심미적인 단위로 나누고, 각 부위에 시술을 할 때 최소 15분의 간격을 두어야 합니다. 이러한 제한으로 인해 시술 건수가 감소하여, 치료는 여전히 전문 피부과나 성형외과에 집중된 상태입니다. 또한, 높은 수익률을 기대하는 시술을 희망하지만, 이에 상응하는 의료 감독 체계가 갖춰지지 않은 중견 미용 클리닉의 경우, 보험, 연수, 법적 리스크에 대처하기가 더욱 어려워지고 있습니다. 그 결과, 케미컬 필 시장에서는 표피 필링을 통한 광범위한 시술 건수가 여전히 주류를 이루고 있는 반면, 중등도 및 심층 필링은 보다 제한적이고 집중된 상태를 유지하고 있습니다.

부문별 분석

2025년 기준으로 글리콜산 필링은 케미컬 필 시장의 36.78%를 차지했으며, 본 보고서에서 가장 큰 제품 부문으로 나타났습니다. 이러한 우위는 여드름, 광노화, 색소 침착에 대한 오랜 임상 실적은 물론, 의료진이 일상적인 치료 계획 수립 과정에서 충분히 이해하고 있는 침투 특성에서 비롯됩니다. 이러한 접근성 덕분에, 피부과 클리닉이나 메디컬 스파에서 글리콜산은 강력한 1순위 치료제로서의 위상을 유지하고 있습니다. 이는 시술자가 눈에 보이는 결과만큼이나 시술 절차의 일관성을 중요하게 여기기 때문입니다. 살리실산은 친유성과 코메도 용해 작용 덕분에 여드름 관리 분야에서 꾸준한 수요를 유지하고 있습니다. 한편, TCA(트리클로로아세트산)나 페놀은 더 심도 있는 교정이 필요한 전문적인 피부 재생 치료에 한정된 용도로만 사용되고 있습니다. 케미컬 필 시장에서는 글리콜산이 여전히 기준이 되는 제품으로 여겨지고 있습니다. 이는 글리콜산이 의료 및 미용 분야 모두의 핵심에 위치해 있으며, 보다 특화된 산으로는 따라올 수 없는 광범위한 적용 범위를 가지고 있기 때문입니다.

젖산 필링 시장은 2026-2031년 연평균 성장률(CAGR) 9.16%를 기록하며 성장할 것으로 예상되며, 케미컬 필 시장에서 가장 빠르게 성장하는 제품 부문이 될 전망입니다. 이 시술의 매력은 피부 재생과 보습 지원이라는 두 가지 역할에 있기 때문에 민감성 피부를 걱정하는 환자들 사이에서 높아지고 있는 보다 순한 시술에 대한 수요에 부응하고 있습니다. 이러한 특성은 피츠패트릭 분류에서 피부 유형이 더 높은 계층의 치료 수요가 증가하는 추세와도 부합하며, 첫 치료나 유지 관리 시 내약성이 더욱 중요시되는 경향이 있습니다. 복합산과 과일산 필링은 케미컬 필 업계에서 제품 개선이 가장 활발하게 진행되고 있는 분야입니다. 각 브랜드는 내성을 높이고 다양한 피부 유형에 걸쳐 사용 범위를 넓히기 위해 완충 시스템과 피부 모방성 캐리어를 채택하고 있습니다. 이러한 시스템이 회복 기간 단축과 편의성 향상을 가져옴에 따라, 2028년까지 단일산 제제에 대한 수요의 일부를 잠식할 가능성이 있습니다.

2025년 기준으로, 표피 필링 또는 라이트 필링은 회복 기간이 최소화되어 다양한 환경과 피부 유형에 폭넓게 적용될 수 있다는 점 덕분에 케미컬 필 시장 규모에서 42.16%의 점유율을 유지했습니다. 이러한 시술들은 반복 시술이 용이하고 안전 여지도 넓기 때문에 미용 클리닉이나 가정에서의 관리에 있어 여전히 표준적인 선택지로 자리 잡고 있습니다. 딥 필링 시술은 심전도 모니터링, 엄격한 시술 간격 관리, 전문적인 훈련을 유지할 수 있는 고도의 피부과 및 성형외과 환경에서 주로 이루어지고 있습니다. 이로 인해 케미컬 필 시장에는 한쪽 끝에는 빈도가 높은 표피 필링이, 다른 쪽 끝에는 빈도는 낮지만 수익성이 높은 딥 필링이 자리 잡는 등 명확한 바벨 구조가 형성되어 있습니다. 미디엄 필링은 이 두 극단 사이의 간극을 메우는 존재가 되어, 2031년에 이르러 주요 가치 성장층으로 부상하고 있습니다.

미디엄 필링 시장은 2026-2031년 연평균 성장률(CAGR) 8.83%로 확대될 것으로 예상되며, 케미컬 필 시장에서 가장 빠르게 성장하는 깊이별 카테고리가 될 것입니다. 이러한 추세는 완충 TCA 프로토콜에 대한 시술자의 신뢰도가 높아지고, 여드름 흉터나 중등도의 광노화에 대한 중심도 치료의 적용 범위가 확대되고 있음을 반영하고 있습니다. 2026년 1월에 발표된 AIME 회의 자료 역시 피부 심층 재생 치료의 임상적 가치를 뒷받침하고 있으며, 이에 따라 교육 및 환자 선별 체계가 잘 갖춰진 클리닉에서는 선택적인 업셀링을 정당화하기가 더 쉬워졌습니다. AI를 활용한 선별 검사가 이러한 변화를 뒷받침하고 있습니다. 왜냐하면 시술자가 더 깊은 층에 대한 시술을 선택하기 전에, 금기 사항을 보다 일관성 있게 확인할 수 있게 되기 때문입니다. 그 결과, 케미컬 필 시장에서 중간층이 확대됨에 따라 시술자는 깊은 페놀 치료에 따르는 모든 위험을 감수하지 않고도 기본적인 피부 재생 치료의 범위를 넘어 시술을 진행할 수 있게 됩니다.

지역별 분석

2025년 기준으로 북미는 케미컬 필 시장 점유율의 44.21%를 차지했으며, 본 보고서에서 가장 규모가 큰 지역 부문으로 나타났습니다. 이 지역에는 피부과 클리닉, 메디컬 스파, 전문 스킨케어 브랜드가 긴밀하게 네트워크를 형성하고 있어, 반복적으로 시술을 받는 환자를 지원할 수 있기 때문에 수요는 여전히 높은 수준을 유지하고 있습니다. 2026년 2월에 발표된 AAFPRS의 2025년 연례 조사에 따르면, 비침습적 치료가 전체 안면 시술의 80%를 차지했으며, 안면 시술 건수가 19% 증가한 것으로 나타났는데, 이는 미국 내 임상 및 미용 현장에서 필링에 대한 지속적인 수요를 뒷받침하고 있습니다. 캐나다와 멕시코도 해당 지역의 시술 건수를 뒷받침하고 있으며, 특히 멕시코는 의료 관광을 통한 시술 비용이 미국의 많은 클리닉보다 저렴하기 때문에 중등도 및 심층 시술 분야에서 중요한 역할을 하고 있습니다.

유럽은 케미컬 필 시장에서 여전히 2위 지역 블록이며, 이 지역의 제품 설계는 EU 화장품 규정(EC) No 1223/2009에 의해 엄격하게 규정되어 있습니다. 해당 규정에 따르면, 글리콜산의 경우 씻어내는 유형의 제품에서는 10%, 씻어내지 않는 유형의 제품에서는 pH 3.5 이상일 때 8%로 제한되며, 살리실산의 경우 씻어내지 않는 유형의 제품에서 2%가 상한선으로 정해져 있습니다. 이러한 제한 사항으로 인해, 단일 고농도 산만을 사용하는 대신, 실험 절차 설계에 따라 결정되는 완충계 및 복합계가 선호되고 있습니다. 독일, 프랑스, 영국, 이탈리아, 스페인이 해당 지역의 물량 대부분을 차지하고 있으며, 독일의 높은 수입 의존도로 인해 시장의 일부는 환율 변동이나 공급 차질의 영향을 받기 쉬운 상황입니다.

아시아태평양은 2026-2031년 연평균 성장률(CAGR) 10.21%를 나타낼 것으로 예측되며, 이는 케미컬 필 시장에서 지역별 가장 빠른 성장 속도입니다. 이 지역은 한국이 제제 개발의 거점으로서 수행하는 역할, 중국 내 화장품 및 의료 서비스 모델 간의 긴밀한 연계, 인도 도시 지역의 피부과 네트워크 확대와 같은 혜택을 누리고 있습니다. 대상 환자군의 대부분이 피츠패트릭 분류의 IV-VI형에 해당하므로, 멜라닌에 안전한 치료 프로토콜을 개발하는 것이 매우 중요합니다. 이에 따라 색소 침착을 고려한 미백 및 피부 재생 옵션에 대한 수요가 증가하고 있으며, ‘VI Peel Precision+Peptides’는 이러한 추세를 보여주는 대표적인 사례입니다. 중동 및 아프리카에서는 GCC의 부유층에 의한 수요와 전문 미용 센터를 찾는 의료 관광의 유입이 성장을 주도하고 있습니다. 남미 역시 여전히 중요한 시장이며, 브라질은 대상 환자층이 방대할 뿐만 아니라 성숙한 미용 의료 생태계를 갖추고 있어, 해당 지역에서 전문가용 필링 브랜드에게 가장 견고한 시장으로 자리매김하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the chemical peel market size was valued at USD 1.23 billion in 2025 and is estimated to grow from USD 1.32 billion in 2026 to reach USD 1.99 billion by 2031, at a CAGR of 8.45% during the forecast period (2026-2031).

This report is Segmented by Product, Including Glycolic, Lactic, and More, by Peel Depth, Including Superficial, Medium, and Deep, by Application, Including Acne Spots and Post-Acne Marks, and More, by End Use, Including Dermatology Clinics, and More, and by Geography, Including North America, Europe, Asia-Pacific, MEA, and South America. The Market Forecasts are Provided in Terms of Value in USD.

Global Chemical Peel Market Trends and Insights

Rising Demand for Minimally Invasive Resurfacing

The sustained preference for low-downtime treatment is moving more patients toward superficial and medium-depth peels instead of more invasive resurfacing options. The AAFPRS 2025 Annual Survey, published in February 2026, stated that noninvasive procedures represent 80% of all facial procedures and also pointed to a 19% increase in facial procedure volume, which supports higher procedure flow across the chemical peel market. This shift matters because the procedure is easier to repeat, easier to fit into daily schedules, and easier for clinics to integrate into routine treatment menus. Demand is also getting younger, with patients under 30 choosing preventive care earlier, which extends the potential treatment cycle over more years. That pattern is pushing operators to build more repeat-visit protocols around light and medium treatments rather than relying on low-volume deep resurfacing alone.

Acne, Pigment, and Photoaging Case-Load Expansion

The chemical peel market continues to draw steady demand from acne, pigmentation, and photoaging case loads that remain large across both medical and aesthetic settings. Blue Shield of California stated in its February 2026 policy that acne vulgaris affects 80% of teenagers between 13 and 18 globally and that actinic keratosis affects 11% to 26% of the adult population in the United States, which supports durable baseline need for glycolic, salicylic, and TCA peels. The Federal Employee Program Medical Policy Manual from April 2025 also classified superficial 40% to 70% AHA peels as medically necessary for active acne unresponsive to systemic antibiotics and recognized dermal peels as medically necessary when more than 10 actinic keratoses are documented. That type of payer recognition reduces the usual price sensitivity seen in elective aesthetics and gives dermatology clinics a more predictable floor of demand. It also keeps chemical peels clinically relevant against newer topical options because the treatment can still deliver competitive outcomes at a lower procedural cost in many patient pathways.

Adverse-Event Risk in Medium and Deep Peels

Medium and deep peels still face a real adoption ceiling because adverse-event risk rises quickly when protocols are not handled by trained medical practitioners. Data presented at the AIME Congress in January 2026 stated that phenol-croton oil deep peels can deliver an average 8.2-year visual age reduction, but the face must be divided into aesthetic units and each application needs at least 15 minutes between sections to avoid cardiac arrhythmia risk. Those limits reduce throughput and keep the treatment concentrated in specialist dermatology and plastic surgery settings. They also make insurance, training, and legal exposure more difficult for mid-tier aesthetic clinics that want higher-margin treatments but lack the same depth of medical supervision. As a result, the chemical peel market continues to favor broad volume in superficial protocols while medium and deep peels remain narrower and more concentrated.

Other drivers and restraints analyzed in the detailed report include:

- AI-Assisted Skin Analysis and Protocol Personalization

- Melanin-Safe Formulations Broaden Eligible Patients

- FDA Scrutiny of Unsupervised High-Strength Home Peels

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Glycolic acid peel held 36.78% of the chemical peel market in 2025, which made it the largest product segment in the report. Its lead came from long clinical use across acne, photoaging, and hyperpigmentation, and from a penetration profile that practitioners understand well in daily treatment planning. That familiarity keeps glycolic acid in a strong first-line position across dermatology clinics and med spas because operators value protocol consistency as much as visible results. Salicylic acid maintains durable demand in acne care because of its lipophilic and comedolytic action, while TCA and phenol remain tied to specialist resurfacing use where deeper correction is needed. The chemical peel market still treats glycolic acid as the reference product because it sits at the center of both medical and aesthetic workflows, which gives it a reach that narrower specialty acids do not match.

Lactic acid peel is projected to grow at a 9.16% CAGR from 2026 to 2031, making it the fastest-growing product segment in the chemical peel market. Its appeal comes from a dual role in resurfacing and moisture support, which fits the growing preference for gentler protocols among patients with sensitivity concerns. That profile also aligns well with rising treatment demand from higher Fitzpatrick skin types, where tolerability matters more in first-time or maintenance care. Combination and fruit acid peels are the part of the chemical peel industry seeing the most active redesign, as brands use buffered systems and skin-mimetic carriers to improve tolerance and widen use across different skin types. As those systems improve recovery and comfort, they may pull some future demand away from single-acid formats before 2028.

Superficial or light peels retained 42.16% share of the chemical peel market size in 2025, supported by minimal downtime and broad compatibility across settings and skin types. They remain the default offer in beauty clinics and home-oriented routines because they are easier to repeat and carry a wider safety margin. Deep Peels stay concentrated in advanced dermatology and plastic surgery environments where cardiac monitoring, careful interval timing, and specialist training can be maintained. This creates a clear barbell structure in the chemical peel market, with high-volume superficial procedures at one end and low-volume high-revenue deep procedures at the other end. Medium Peels are filling the space between those two poles and are becoming the main value-growth layer through 2031.

Medium peels are projected to expand at an 8.83% CAGR from 2026 to 2031, making them the fastest-growing depth category in the chemical peel market. That pace reflects rising practitioner confidence in buffered TCA protocols and stronger comfort with medium-depth treatment for acne scarring and moderate photoaging. AIME Congress material presented in January 2026 also reinforced the clinical value of deeper resurfacing, which helps clinics justify selective upselling where training and patient screening are strong. AI-supported screening adds to this shift because it helps practitioners review contraindications more consistently before selecting a deeper procedure. The result is a broader middle tier in the chemical peel market where operators can move beyond basic resurfacing without taking on the full risk profile of deep phenol treatment.

Geography Analysis

North America accounted for 44.21% of the chemical peel market share in 2025, which made it the largest regional segment in the report. Demand remains high because the region has a dense network of dermatology clinics, med spas, and professional skincare brands that can support repeat treatment use. The AAFPRS 2025 Annual Survey published in February 2026 stated that noninvasive treatments represented 80% of all facial procedures and pointed to a 19% increase in facial procedure volume, which supports recurring peel demand across U.S. clinical and aesthetic settings. Canada and Mexico add support to regional volume, and Mexico is especially relevant in medium and deep procedures because its medical tourism offer provides lower treatment costs than many U.S. clinics.

Europe remained the second-largest regional block in the chemical peel market, and product design in the region is strongly shaped by EU Cosmetics Regulation (EC) No 1223/2009. The regulation limits glycolic acid to 10% in rinse-off products and 8% in leave-on products with a minimum pH of 3.5, while salicylic acid is capped at 2% in leave-on formats . These limits favor buffered and combination systems that rely on protocol design rather than one high-strength acid alone. Germany, France, the United Kingdom, Italy, and Spain account for most regional volume, and Germany's import dependence leaves part of the market more exposed to exchange-rate movement and supply disruption.

Asia-Pacific is forecast to expand at a 10.21% CAGR from 2026 to 2031, the fastest regional pace in the chemical peel market. The region benefits from South Korea's role as a formulation hub, China's closer links between cosmetic and medical service models, and India's expanding urban dermatology network. Melanin-safe protocol development matters strongly here because a large share of the addressable patient base falls within Fitzpatrick IV to VI skin types, which raises demand for pigment-safe brightening and resurfacing options, and VI Peel Precision + Peptides is one example of this direction. The Middle East and Africa add growth through affluent GCC demand and medical tourism flows into specialist aesthetic centers. South America also remains relevant because Brazil combines a large eligible patient pool with a mature aesthetic medicine ecosystem, which makes it the strongest structural market in the region for professional peel brands.

- Allergan Aesthetics

- Bella Medical Products

- Circadia by Dr. Pugliese

- Dermaceutic Laboratoire

- Dermalogica

- Dr. Dennis Gross Skincare

- Fixderma India Pvt. Ltd.

- IMAGE Skincare

- Jan Marini Skin Research

- L'Oreal

- Mediderma

- MedPeel

- Merz Pharma

- mesoestetic Pharma Group

- NeoStrata Company

- Obagi Medical

- PCA SKIN

- Pierre Fabre / Glytone

- Santen Pharmaceuticals

- VI Aesthetics / VI Peel

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Minimally Invasive Resurfacing

- 4.2.2 Acne, Pigment, and Photoaging Case-Load Expansion

- 4.2.3 Med Spa and Dermatology Network Expansion

- 4.2.4 Buffered And Combination-Acid Product Innovation

- 4.2.5 AI-Assisted Skin Analysis and Protocol Personalization

- 4.2.6 Melanin-Safe Formulations Broaden Eligible Patients

- 4.3 Market Restraints

- 4.3.1 Adverse-Event Risk in Medium and Deep Peels

- 4.3.2 Competition from Laser, Microneedling, and IPL

- 4.3.3 FDA Scrutiny of Unsupervised High-Strength Home Peels

- 4.3.4 Training Variability and Imported-Input Margin Pressure

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product

- 5.1.1 Glycolic Acid Peel

- 5.1.2 Lactic Acid Peel

- 5.1.3 Salicylic Acid Peel

- 5.1.4 Trichloroacetic Acid Peel

- 5.1.5 Phenol Peel

- 5.1.6 Combination and Fruit Acid Peel

- 5.2 By Peel Depth / Type

- 5.2.1 Superficial / Light Peel

- 5.2.2 Medium Peel

- 5.2.3 Deep Peel

- 5.3 By Application

- 5.3.1 Acne Spots and Post-Acne Marks

- 5.3.2 Hyperpigmentation and Melasma

- 5.3.3 Fine Lines and Wrinkles

- 5.3.4 Scars

- 5.3.5 Dark Circles

- 5.3.6 Skin Brightening and Tone Correction

- 5.4 By End Use

- 5.4.1 Dermatology Clinics

- 5.4.2 Med Spas

- 5.4.3 Hospitals

- 5.4.4 Beauty and Aesthetic Clinics

- 5.4.5 Home Care Settings

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Allergan Aesthetics

- 6.3.2 Bella Medical Products

- 6.3.3 Circadia by Dr. Pugliese

- 6.3.4 Dermaceutic Laboratoire

- 6.3.5 Dermalogica

- 6.3.6 Dr. Dennis Gross Skincare

- 6.3.7 Fixderma India Pvt. Ltd.

- 6.3.8 IMAGE Skincare

- 6.3.9 Jan Marini Skin Research

- 6.3.10 L'Oreal

- 6.3.11 Mediderma

- 6.3.12 MedPeel

- 6.3.13 Merz Aesthetics

- 6.3.14 mesoestetic Pharma Group

- 6.3.15 NeoStrata Company

- 6.3.16 Obagi Medical

- 6.3.17 PCA SKIN

- 6.3.18 Pierre Fabre / Glytone

- 6.3.19 Santen Pharmaceutical Co., Ltd.

- 6.3.20 VI Aesthetics / VI Peel

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment