|

시장보고서

상품코드

2064491

패시브 온도 제어 포장 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Passive Temperature Controlled Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

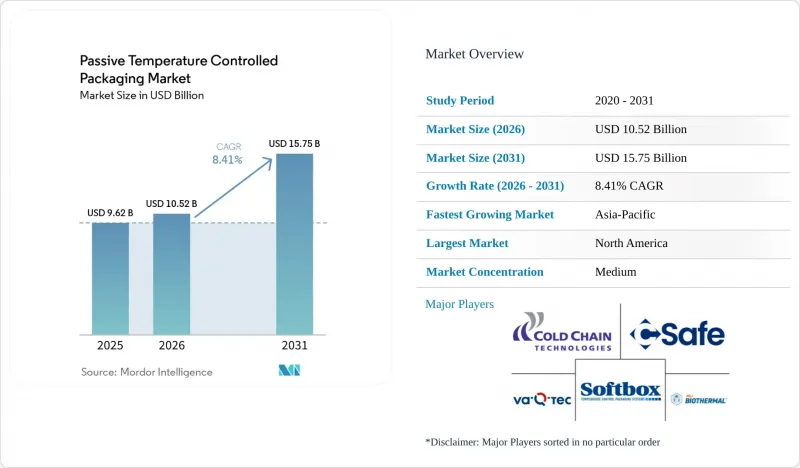

Mordor Intelligence에 의하면, 패시브 온도 제어 포장 시장 규모는 2025년 96억 2,000만 달러로 평가되었고, 2026년 105억 2,000만 달러로 추정되고, 2031년까지 157억 5,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 8.41%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형별(단열 운송용기, 단열 컨테이너, 기타), 소재 유형별(플라스틱, 종이 및 판지, 기타), 사용 방식별(일회용, 재사용 가능), 온도 범위별(상온, 냉동, 기타), 최종 사용자 산업별(제약 및 생명공학, 화학, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 패시브 온도 제어 포장 시장 동향 및 인사이트

바이오의약품 및 특수 의약품 출하량 증가

바이오의약품 출하량 증가는 패시브 온도 제어 포장 시장을 뒷받침하는 출하 구성을 변화시키고 있습니다. 많은 새로운 치료법은 열에 노출되거나 의도치 않게 동결되는 것에 모두 민감하기 때문에 포장 설계 및 운송 경로의 적합성 평가에서 2°C에서 8°C 범위가 여전히 핵심적인 역할을 하고 있습니다. 이와 같은 추세로 인해 경로별 검증의 중요성이 커지고 있습니다. 이는 운송 과정에서 바이오의약품이 기존 저분자 의약품보다 더 엄격한 관리가 필요하기 때문입니다. Cencora는 2025년 11월, 2027년까지 전 세계적으로 출시될 예정인 의약품의 약 50%가 콜드체인 보관이 필요할 것이라고 밝혔으며, 이는 10년 전의 37%에서 증가한 수치입니다. 이는 의약품 파이프라인 전반에 걸쳐 콜드체인에 대한 의존도가 급속히 확대되고 있음을 보여줍니다. 이러한 제품들이 전문 유통망이나 직접 조제 채널을 통해 유통되기 시작함에 따라, 패시브 온도 제어 포장 시장은 정기적인 출하량 증가와 더욱 반복적인 포장 요건의 혜택을 누리고 있습니다. 이에 따라 검증된 적재물 보호 기능, 다양한 온도 유지 기간 옵션, 계절에 따라 변화하는 조건에서의 적합성을 입증하는 문서를 제공할 수 있는 공급업체가 유리해집니다.

GLP-1 및 환자에게 직접 배송되는 냉장 소포의 유통량 증가

GLP-1 요법은 수동 온도 관리 포장 시장에서 소포 단위로 막대한 수요 흐름을 창출하고 있습니다. 이러한 제품은 전문 약국, 원격 의료 채널, 택배에 의존하는 배송 모델에 적합하며, 팔레트 시스템이 아닌 콤팩트한 단열 포장의 필요성을 강조하고 있습니다. Nordic Cold Chain Solutions는 2026년 3월에 GLP-1 및 소형 제형 포장을 위한 혁신 연구소를 설립했는데, 이는 공급업체들이 현재 이를 독자적인 검증된 구성이 필요한 명확한 포장상의 과제로 인식하고 있음을 보여줍니다. 템퍼팩(TemperPack)은 2025년, GLP-1 운송에 사용된 스티로폼 쿨러 박스가 미국에서는 분당 12개씩 매립지로 버려지고 있다고 보고했습니다. 이는 이 치료 분야가 라스트 마일 콜드체인에 관한 논의에서 지속가능성에 대한 우려를 불러일으키고 있는 이유를 여실히 보여주고 있습니다. 이처럼 높은 출하 빈도와 폐기물 가시화가 진행되고 있는 상황이 맞물리면서, 구매 담당자들은 포장 크기와 단열재 선택을 동시에 재검토하도록 촉구하고 있습니다. 또한, 이로 인해 패시브 온도 제어 포장 시장은 처방전 수량 증가에 따라 확장 가능한, 표준화되어 포장하기 쉬운 쉬퍼 형태에 대한 의존도를 높이고 있습니다.

장거리이며 변동이 심한 배송 노선에서 제한된 보관 시간과 능동형 시스템의 비교

보관 시간 제한은 여전히 패시브 온도 제어 포장 시장에서 실질적인 제약 요인으로 남아 있습니다. 패시브 방식은 많은 지역 내 노선이나 단일 구간의 국제 노선에서는 효과적이지만, 통관 지연, 환승 실패, 또는 경유지에서 장시간 체류가 발생할 경우 그 신뢰성은 떨어집니다. Peli BioThermal은 2025년에 고성능 수동형 구성의 경우 96시간에서 168시간 동안 보호가 가능하다고 밝혔습니다. 이는 많은 이용 사례에서 충분한 성능을 발휘하지만, 능동형 시스템과 비교하면 여전히 한계가 있습니다. 경로가 서로 다른 기후대에 걸쳐 있는 경우, 이러한 제약은 더욱 두드러집니다. 왜냐하면, 같은 화물이라 하더라도 고온기와 저온기라는 계절별 특성에 따라 각각 별도의 검증이 필요할 가능성이 있기 때문입니다. 이로 인해 전 세계에 걸쳐 다중 거점 네트워크로 사업을 전개하고 있으며, 운송 경로에 신뢰할 수 있는 환적 거점을 보유하지 않은 화주에게는 유연성이 떨어지게 됩니다. 그 결과, 패시브 온도 제어 포장 시장은 중단거리 노선에서 가장 확고한 입지를 유지하는 한편, 가장 혹독한 대륙 간 운송 분야에서는 능동형 또는 하이브리드형 접근 방식이 계속해서 중요한 역할을 할 것으로 보입니다.

부문별 분석

2025년 기준으로 단열 포장은 46.65%의 점유율을 차지했으며, 패시브 온도 제어 포장 시장에서 가장 큰 제품 카테고리를 형성하고 있습니다. 이러한 주도적인 지위는 소포 크기의 의약품 운송 및 식품 전자상거래 주문과의 높은 적합성에서 비롯된 것으로, 이러한 부문에서는 매우 큰 적재 용량보다 포장 용이성과 폭넓은 온도 범위 대응 능력이 더 중요하게 여겨집니다. 이 제품은 소량의 적재량, 표준화된 포장, 배송 거점에서의 신속한 처리가 가능하기 때문에 환자에게 직접 배송하는 프로그램과 특히 잘 어울린다고 할 수 있습니다. Cencora는 2030년까지 10억 달러를 투자해 미국의 배송 네트워크를 확장하고 현대화하겠다고 발표했습니다. 여기에는 앨라배마주의 전문 시설 내 대규모 냉장·냉동 창고 증설도 포함되어 있으며, 소포 및 특수 콜드체인 운송의 성장을 뒷받침할 기반이 되는 물류 인프라를 강화하는 것입니다. 물류 네트워크가 냉장 창고 및 전문적인 취급 능력을 확충해 나가는 가운데, 단열 시퍼는 대량 배송에 대응하기 쉽다는 장점 덕분에 많은 정기 배송 프로그램에서 여전히 실용적인 선택지로 자리 잡고 있습니다.

단열 컨테이너는 의약품의 대량 운송이나 대규모 콜드체인 운송에서 여전히 중요한 역할을 하며, 특히 출하 가치에 걸맞은 더욱 견고한 포장 시스템과 더욱 엄격하게 관리되는 재사용 주기가 요구되는 상황에서 그 가치를 발휘합니다. 단열 라이너와 커버는 여전히 시장 점유율이 가장 낮은 제품군이지만, 패시브 온도 제어 포장 업계에서는 이를 저가 부속품이 아닌, 운송 경로의 유연성을 높이는 관리 자산으로 간주하는 경향이 강해지고 있습니다. CSafe는 2025년 10월, 라이프사이클 관리 및 통합 추적 기능을 갖추고, 2℃-8℃와 15℃-25℃의 온도 범위를 지원하는 재사용형 보온 팔레트 커버 ‘Silverskin RE’를 출시했습니다. 이는 이 하위 부문이 얼마나 서비스 지향적으로 변해가고 있는지를 보여줍니다. 냉매 및 냉각제 시장은 2031년까지 연평균 성장률(CAGR) 9.26%를 나타낼 것으로 예측되며, 이러한 성장세는 기본적인 젤 팩에서 열 안정성이 더 뛰어나고 규제 대상 운송 경로를 위한 재현성이 높은 기록 기능을 제공하는 PCM(상변화 물질) 형태로의 광범위한 전환을 반영하고 있습니다. 냉매와 관련된 패시브 온도 제어 포장재 시장 점유율은 출하당 부품 원가(BOM)가 높아지는 점에서도 혜택을 보고 있습니다. 이는 보다 복잡한 생물학적 제제나 GLP-1 제품의 포장 과정에서 범용 냉각원이 아닌 신중하게 조정된 냉각제 구성이 필요한 경우가 늘어나고 있기 때문입니다.

2025년 기준으로, 패시브 온도 제어 포장 시장의 41.58%를 플라스틱이 차지했으며, 이는 의약품 및 식품 운송 분야에서 발포 폴리스티렌(EPS)과 폴리우레탄이 오랫동안 사용되어 온 사실을 반영하고 있습니다. 이러한 자재들이 여전히 그 위치를 유지하고 있는 이유는 포장 업체들에게 친숙하고 널리 구할 수 있으며, 이미 검증된 수많은 포장 구성에 포함되어 있기 때문입니다. EPS는 많은 표준 냉장 운송 경로에서 여전히 효과적인 방식으로 열 성능과 비용의 균형을 맞추고 있기 때문에 소포 운송 분야에서 계속해서 널리 사용되는 소재로 자리 잡고 있습니다. 또한, 폴리우레탄은 구조나 단열 성능이 더욱 가혹한 운송 조건에 대응해야 하는 고사양 시스템에서도 중요한 역할을 하고 있습니다. 이로 인해 고객의 취향이 변화하기 시작했음에도 불구하고, 플라스틱 계열 소재는 여전히 탄탄한 시장 기반을 유지하고 있습니다.

바이오 단열재는 지속가능성에 대한 요구와 성능 입증의 진전에 힘입어 2031년까지 연평균 성장률(CAGR) 9.18%로 성장할 것으로 전망됩니다. TemperPack에 따르면, 이 회사의 GreenCell Foam 플랫폼은 2°C-8°C, 15°C-25°C, -20°C의 온도 프로파일에서 60종 이상의 사전 인증된 운송 용기를 지원하며, 이는 구매자들이 퇴비화 가능한 단열재를 더 이상 경량 작업 용도로만 한정된 틈새 시장 선택지로만 여기지 않고 있음을 보여줍니다. Landpack 역시 천연섬유 소재를 기반으로 한 사전 인증을 받은 생명과학용 냉각 솔루션을 추진하고 있으며, 이는 바이오 유래 대체재가 식품 배송에 국한되지 않고 유럽의 규제 대상 이용 사례로 진출하고 있음을 시사합니다. 따라서 패시브 온도 제어 포장 시장에서는 중저 성능 부문에서 점진적인 대체가 진행되고 있습니다. 이 부문에서는 구매자들이 인증의 신뢰성을 훼손하지 않으면서도 발포 폴리스티렌(EPS)에 대한 의존도를 낮추고자 합니다. 이러한 전환은 여전히 선택적인 성격으로 남아 있습니다. 왜냐하면 구매자가 교체를 승인하기 위해서는 해당 자재가 기존 단열재와 동등한 단열 성능을 충족해야 하기 때문입니다.

지역별 분석

2025년 기준 북미는 41.38%의 점유율을 차지했으며, 패시브 온도 제어 포장 시장의 주요 지역으로 자리매김하고 있습니다. 미국은 정교한 의약품 유통 시스템과 환자에 대한 직접 배송의 활성화, 대규모 콜드체인 전자상거래 인프라를 결합함으로써 그 규모의 상당 부분을 주도하고 있습니다. Cencora가 2025년 11월에 발표한, 2030년까지 미국 유통 네트워크에 10억 달러를 투자하겠다는 계획(앨라배마주의 냉장·냉동 시설 대폭 확대를 포함)은 의약품 콜드체인 유통을 뒷받침하는 인프라 구축이 지속될 것임을 시사합니다. 이번 투자는 냉장 창고 접근성, 처리 능력, 표준화된 전문 유통 경로 등 패시브 솔루션의 확장을 뒷받침하는 실질적인 여건을 마련하는 것입니다. 또한, 해당 지역에서는 소포 형태의 의약품 배송이 널리 보급되어 있어, 단열 운송 용기, 인증 냉매, 소형 솔루션에 대한 수요가 높은 수준을 유지하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 9.25%를 나타낼 것으로 예측되며, 패시브 온도 제어 포장 시장에서 가장 빠르게 성장하는 지역 부문이 될 전망입니다. 이 지역의 성장은 의약품 생산 확대, 콜드체인 물류 개선, 그리고 몇몇 대규모 소비 시장에서 식품 전자상거래의 확산과 밀접한 관련이 있습니다. 호주 및 뉴질랜드는 소포형 콜드체인 체계를 조기에 도입한 주요 국가인 반면, 중국과 인도는 해당 지역의 포장 수요를 높이는 광범위한 제조 및 수출 기반을 뒷받침하고 있습니다. Nordic Cold Chain Solutions가 GLP-1 및 소형 제형 혁신에 주력하고 있다는 점은 북미 이외의 지역에서도 관련성이 있습니다. 왜냐하면, 이와 유사한 소포 기반 치료 모델이 다른 선진 의료 시스템으로도 확산되고 있기 때문입니다. 이로 인해 아시아태평양에는 의료와 식품이라는 두 가지 수요 요인이 공존하게 되었으며, 단일 부문의 확장 주기보다 더 균형 잡힌 지역 성장 양상이 나타나고 있습니다.

2025년에도 유럽은 패시브 온도 제어 포장 시장의 주요 수익 기반이 계속되었습니다. 이는 독일, 영국, 프랑스, 이탈리아, 스페인에서 제약 제조의 집적도와 규제된 물류 기준에 힘입은 결과입니다. 랜드팩(Landpack)의 사전 인증을 받은 생명과학 솔루션과 유럽에서 천연섬유 단열재로 광범위하게 전환되고 있는 추세는 온도 성능뿐만 아니라 지속가능성에 관한 규제가 상업용 포장재 선택에 어떤 영향을 미치기 시작했는지를 보여줍니다. 남미 시장은 여전히 발전 단계에 있지만, 2026년 3월 Peli BioThermal이 브라질의 Polar Group과 체결한 유통 제휴는 해당 지역의 의약품 콜드체인 확장에 공급업체의 참여가 증가하고 있음을 보여줍니다. 중동 및 아프리카는 여전히 초기 단계에 있지만, 의료 물류 네트워크가 더욱 체계화되고 규정 준수를 중시하는 경향이 강해짐에 따라, 걸프 지역의 운송 허브와 튀르키예, 남아프리카공화국, 나이지리아가 주요 도입 거점으로 부상하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the passive temperature controlled packaging market size is projected to expand from USD 9.62 billion in 2025 and USD 10.52 billion in 2026 to USD 15.75 billion by 2031, registering a CAGR of 8.41% between 2026 and 2031.

This report is Segmented by Product Type (Insulated Shippers, Insulated Containers, and More), Material Type (Plastic, Paper and Paperboard, and More), Usability (Single-Use, and Reusable), Temperature Range (Ambient, Frozen, and More), End-User Industry (Pharmaceuticals and Biotechnology, Chemical, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Passive Temperature Controlled Packaging Market Trends and Insights

Rising Biologics and Specialty Pharma Shipments

Rising biologics volumes are changing the shipment mix that supports the passive temperature controlled packaging market. Many newer therapies are sensitive to both heat exposure and unintended freezing, which keeps the 2°C to 8°C range central to packaging design and lane qualification. The same trend is increasing the value of route-specific validation, as biologics require tighter control than traditional small-molecule drugs during transit. Cencora stated in November 2025 that nearly 50% of drugs expected to launch globally through 2027 would require cold chain storage, up from 37% a decade earlier, which shows how quickly cold chain dependence is widening across drug pipelines. As more of these products move through specialty distribution and direct dispensing channels, the passive temperature controlled packaging market benefits from larger recurring shipment volumes and more repeatable pack-out requirements. This favors suppliers that can offer validated payload protection, multiple duration options, and documentation that supports qualification across changing seasonal conditions.

Growth In GLP-1 and Direct-To-Patient Refrigerated Parcel Flows

GLP-1 therapies are creating a large parcel-based demand stream for the passive temperature controlled packaging market. These products fit a delivery model that relies on specialty pharmacies, telehealth channels, and home delivery, underscoring the need for compact, insulated formats rather than pallet systems. Nordic Cold Chain Solutions launched a GLP-1 and small-format packaging innovation lab in March 2026, indicating that suppliers now see this as a distinct packaging problem that requires its own validated configurations. TemperPack reported in 2025 that 12 EPS foam coolers used for GLP-1 shipments were being discarded in US landfills every minute, underscoring why this therapy category is also drawing sustainability concerns into the last-mile cold chain discussion. That combination of high shipment frequency and rising waste visibility is prompting buyers to review both pack size and insulation choice simultaneously. It also makes the passive temperature controlled packaging market more dependent on standardized, easy-to-pack shipper formats that can scale with prescription volume growth.

Limited Hold Time Versus Active Systems on Long and Variable Lanes

Hold-time limits remain a practical constraint on the passive temperature controlled packaging market. Passive formats work well on many regional and single-leg international lanes, but they become harder to rely on when a shipment faces customs delays, missed connections, or long dwell time at transfer points. Peli BioThermal stated in 2025 that high-performance passive configurations can provide 96 to 168 hours of protection, which is strong for many use cases but still finite compared with active-powered systems. The constraint becomes sharper when the route spans different climates, as the same payload may require separate validation for hot and cold seasonal profiles. This reduces flexibility for shippers that operate across global multi-stop networks and lack reliable reconditioning points along the route. As a result, the passive temperature controlled packaging market is likely to remain strongest in short-to-medium-haul lanes, while the hardest intercontinental movements continue to play a larger role for active or hybrid approaches.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Food E-Commerce and Meal-Kit Cold Chains

- Tightening GDP, USP, and Food-Safety Compliance Standards

- High Cost of VIP and Advanced PCM Configurations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Insulated shippers held 46.65% share in 2025, making them the largest product category in the passive temperature controlled packaging market. Their lead position comes from a strong fit with parcel-sized healthcare shipments and food e-commerce orders, where ease of packing and broad temperature coverage matter more than very large payload capacity. The product is especially well aligned with direct-to-patient programs because it supports small payloads, standardized pack-outs, and fast handling at distribution sites. Cencora announced a USD 1 billion investment through 2030 to expand and modernize its US distribution network, including major refrigerated and frozen storage additions at its Alabama specialty facility, which supports the underlying logistics infrastructure that keeps parcel and specialty cold chain traffic growing. As distribution networks add more cold storage and specialized handling capacity, insulated shippers remain the practical choice for many repeat-shipment programs because they are easy to scale across large delivery volumes.

Insulated containers remain important for bulk pharmaceutical flows and larger cold chain moves, especially where shipment value justifies a stronger packaging system and a more controlled reuse cycle. Thermal liners and covers still represent the smallest product slice, but the passive temperature controlled packaging industry is treating them less as low-value accessories and more as managed assets that can add lane flexibility. CSafe launched Silverskin RE in October 2025 as a reusable thermal pallet cover with lifecycle management, integrated tracking, and support for 2°C to 8°C and 15°C to 25°C ranges, which shows how this sub-segment is becoming more service oriented. Refrigerants and coolants are projected to grow at 9.26% CAGR through 2031, and that pace reflects the wider shift from basic gel packs toward PCM formats that offer better thermal stability and more repeatable documentation for regulated shipment lanes. The passive temperature controlled packaging market share tied to refrigerants also benefits from higher bill-of-materials content per shipment because more complex biologic and GLP-1 pack-outs often require carefully matched coolant configurations rather than a generic cold source.

Plastic accounted for 41.58% of the passive temperature controlled packaging market in 2025, reflecting the long-established use of EPS and polyurethane across pharmaceutical and food shipment formats. These materials have kept their position because they are familiar to packers, widely available, and already embedded in many validated pack-outs. EPS has remained common in parcel shipping because it balances thermal performance and cost in a way that still works for many standard cold lanes. Polyurethane also plays a role in higher-specification systems where structure and insulation value need to support more demanding transport conditions. This leaves plastic-based materials with a large installed base even as customer preferences begin to shift.

Bio-based insulation materials are projected to expand at a 9.18% CAGR through 2031, driven by a mix of sustainability pressures and improving proof of performance. TemperPack said its GreenCell Foam platform supports more than 60 pre-qualified shippers across 2°C to 8°C, 15°C to 25°C, and -20°C temperature profiles, indicating that buyers no longer see compostable insulation as a niche option only for light-duty applications. Landpack also promotes pre-qualified life science cooling solutions based on natural fiber materials, indicating that bio-based alternatives are moving into regulated use cases in Europe rather than remaining limited to food delivery. The passive temperature controlled packaging market is therefore seeing a gradual replacement path at the low-to-mid performance tier, where buyers want to reduce reliance on EPS without losing qualification confidence. This transition remains selective because the material must meet the same transit expectations as incumbent insulation before the buyer will approve a switch.

Geography Analysis

North America held a 41.38% share in 2025, making it the leading region in the passive temperature controlled packaging market. The United States drives most of that scale by combining a dense pharmaceutical distribution system with strong direct-to-patient shipments and a large cold-chain e-commerce base. Cencora's November 2025 plan to invest USD 1 billion through 2030 in its US distribution network, including major refrigerated and frozen expansion in Alabama, points to continued infrastructure build-out behind pharmaceutical cold chain flows. That investment supports the practical conditions that help passive solutions scale, including access to cold storage, handling capacity, and standardized specialty distribution lanes. The region also benefits from strong adoption of parcel-format healthcare shipping, which keeps demand high for insulated shippers, qualified refrigerants, and small-format solutions.

Asia-Pacific is projected to grow at a 9.25% CAGR through 2031, making it the fastest-growing regional segment in the passive temperature controlled packaging market. The region's growth is tied to expanding pharmaceutical manufacturing, improving cold chain logistics, and stronger food e-commerce penetration across several large consumer markets. Australia and New Zealand are important early adopters in parcel cold chain formats, while China and India support the broad manufacturing and export base that is raising regional packaging needs. Nordic Cold Chain Solutions' focus on GLP-1 and small-format innovation also has relevance beyond North America because the same parcel-based therapy model is spreading into other developed healthcare systems. This leaves Asia-Pacific with both healthcare and food demand drivers, which gives the regional growth story more balance than a single-sector expansion cycle.

Europe remained a major revenue base for the passive temperature controlled packaging market in 2025, supported by pharmaceutical manufacturing density and regulated logistics standards across Germany, the United Kingdom, France, Italy, and Spain. Landpack's pre-qualified life science solutions and the broader move toward natural fiber insulation in Europe show how sustainability rules are starting to affect commercial packaging choice in addition to temperature performance. South America is still developing, but Peli BioThermal's March 2026 distribution partnership with Polar Group in Brazil indicates growing supplier commitment to pharmaceutical cold chain expansion in the region. The Middle East and Africa remains earlier stage, with Gulf transit hubs, Turkey, South Africa, and Nigeria forming the main points of adoption as healthcare logistics networks become more structured and more compliance driven.

- Cold Chain Technologies, LLC

- Pelican BioThermal LLC

- CSafe Global Cooperatief U.A.

- Softbox Systems Limited

- va-Q-tec Thermal Solutions GmbH

- Envirotainer AB

- DGP Intelsius Ltd

- Cryopak Industries Inc.

- Inmark, LLC

- Tempack Packaging Solutions, S.L.

- Temperpack Technologies, Inc.

- Temperatsure, LLC

- Sofrigam SAS

- Sealed Air Corporation

- Polar Tech Industries Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Biologics and Specialty Pharma Shipments

- 4.2.2 Expansion of Food E-Commerce and Meal-Kit Cold Chains

- 4.2.3 Tightening GDP, USP, and Food-Safety Compliance Standards

- 4.2.4 Shift Toward Reusable and Recyclable Passive Solutions

- 4.2.5 Growth in GLP-1 and Direct-to-Patient Refrigerated Parcel Flows

- 4.2.6 Adoption of Lane-Specific Pack-Out Optimization and Connected Passive Packaging

- 4.3 Market Restraints

- 4.3.1 Limited Hold Time Versus Active Systems on Long and Variable Lanes

- 4.3.2 High Cost of VIP and Advanced PCM Configurations

- 4.3.3 Reverse-Logistics Gaps Reducing Reuse Economics Outside Core Pharma Corridors

- 4.3.4 Supply Risk in Qualified VIP, PCM, and Fiber-Based Input Chains

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Insulated Shippers

- 5.1.2 Insulated Containers

- 5.1.3 Refrigerants and Coolants

- 5.1.4 Thermal Liners and Covers

- 5.2 By Material Type

- 5.2.1 Plastic

- 5.2.1.1 Polystyrene

- 5.2.1.2 Polyurethane

- 5.2.1.3 Polypropylene

- 5.2.2 Paper and Paperboard

- 5.2.3 Bio-Based Insulation Materials

- 5.2.1 Plastic

- 5.3 By Usability

- 5.3.1 Single-Use

- 5.3.2 Reusable

- 5.4 By Temperature Range

- 5.4.1 Ambient

- 5.4.2 Chilled/Refrigerated

- 5.4.3 Frozen

- 5.5 By End-User Industry

- 5.5.1 Pharmaceuticals and Biotechnology

- 5.5.2 Food and Beverage

- 5.5.3 Chemical

- 5.5.4 Other End-Use Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cold Chain Technologies, LLC

- 6.4.2 Pelican BioThermal LLC

- 6.4.3 CSafe Global Cooperatief U.A.

- 6.4.4 Softbox Systems Limited

- 6.4.5 va-Q-tec Thermal Solutions GmbH

- 6.4.6 Envirotainer AB

- 6.4.7 DGP Intelsius Ltd

- 6.4.8 Cryopak Industries Inc.

- 6.4.9 Inmark, LLC

- 6.4.10 Tempack Packaging Solutions, S.L.

- 6.4.11 Temperpack Technologies, Inc.

- 6.4.12 Temperatsure, LLC

- 6.4.13 Sofrigam SAS

- 6.4.14 Sealed Air Corporation

- 6.4.15 Polar Tech Industries Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment