|

시장보고서

상품코드

2064493

재밀봉 가능 캔 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Resealable Cans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

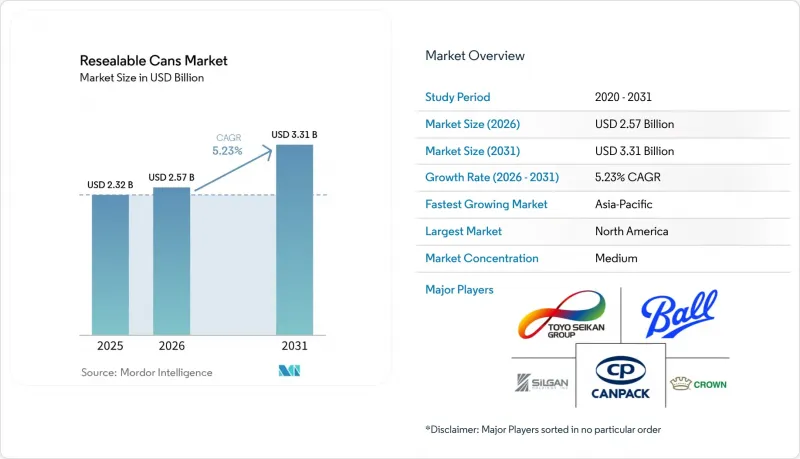

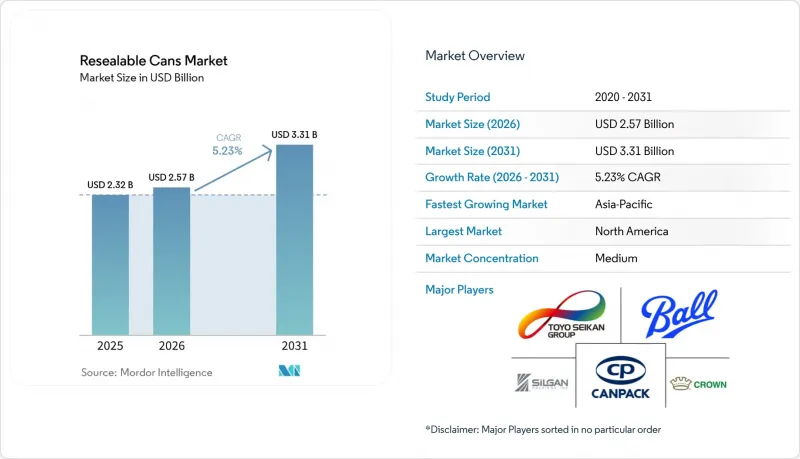

Mordor Intelligence에 의하면, 재밀봉 가능 캔 시장 규모는 2025년 23억 2,000만 달러로 평가되었습니다. 2026년 25억 7,000만 달러에서 2031년까지 33억 1,000만 달러로 확대되어 2026-2031년 CAGR은 5.23%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형(표준 재밀봉 가능 캔, 나사식 뚜껑 캔, 하이브리드/복합 소재 캔), 소재 유형(알루미늄, 강철 및 양철, 플라스틱), 용량(350ml 이하, 351-750ml, 750ml 이상), 최종 사용자 산업(식품 및 음료, 퍼스널케어 및 화장품, 의약품 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 재밀봉 가능 캔 시장 동향 및 인사이트

외출 시 음료 포장재에 대한 수요 증가

소비자들이 가정 밖이나 다양한 상황에서 음료 팩을 이용하는 기회가 늘어나고 있어, 휴대형 소비가 재밀봉 가능 캔 시장을 지속적으로 지탱하고 있습니다. 이는 특히 330ml에서 500ml 용량의 제품에서 중요하며, 모든 음료가 한 번에 소비되는 것은 아니기 때문에 쏟아지지 않는 특성이 직접적인 기능적 가치를 제공합니다. 에너지 드링크, 탄산수, 피트니스 음료는 개봉 후 액체가 새어 나올 경우 소비자의 사용 방법이나 장소를 바꿀 가능성이 있기 때문에 재밀봉 기능의 이점을 더욱 크게 누리고 있습니다. 또한, 각 브랜드 기업들은 소매점에서 차별화 요소로 재밀봉 가능한 포장을 도입하기 시작했습니다. 그 예로, Re : Lid USA가 2026년 4월 남부 캘리포니아의 Gelson’s Markets에서 사업을 시작한 사례를 들 수 있습니다. 이러한 추세가 편의점 및 즉시 소비 채널로 확대됨에 따라, 재밀봉 가능 캔 시장은 음료 포트폴리오 내에서 더욱 폭넓은 입지를 확보해 나갈 것으로 보입니다.

재활용 가능한 금속 포장재로 전환

재밀봉 가능 캔 시장은 알루미늄 음료 용기가 지닌 환경적 장점 덕분에 성장세를 보이고 있습니다. 2024년 미국 알루미늄 음료 캔의 폐쇄형 순환률은 96.7%, 평균 재활용 소재 함유율은 71%에 달하여, 유리나 PET의 동등한 수준을 크게 상회했습니다. 유럽에서는 알루미늄 음료 캔의 재활용률이 2023년에 76.3%에 달했으며, 회수 및 재활용 소재 함유율에 점점 더 중점을 두는 규제 환경 속에서 금속 포장의 매력이 더욱 부각되고 있습니다. 캡 시스템이 단일 소재 구조를 유지할 경우, 재밀봉 가능 캔 시장은 더욱 큰 혜택을 볼 것입니다. 왜냐하면, 이를 통해 포장의 복잡성이 줄어들고 재활용 적합성이 향상되기 때문입니다. 소노코사는 Interpack 2026에서 바로 그 점을 강조하며 자사의 CapOnCan 시스템을 소개하고, 식품 및 반려동물사료 용도에서의 단일 소재 강철 구조와 EPR(확대 생산자 책임) 비용 부담 경감을 어필했습니다.

표준 엔드캡에 비해 높은 캡 및 가공 비용

재밀봉 가능 캔 시장에서 가장 큰 구조적 장벽은 여전히 표준 스테이-온 탭 엔드와 비교했을 때 캡에 드는 추가 비용입니다. 재밀봉 가능 시스템에는 더 많은 부품과 더 엄격한 제조 공차가 필요하며, 경우에 따라서는 많은 음료 제조업체가 아직 도입하지 않은 충전 라인의 운영 방식 변경도 요구됩니다. 이러한 부담은 중소규모 브랜드에게 더 큰 과제가 됩니다. 왜냐하면, 그들은 생산 물량이 매우 많아 설비 및 가공 비용을 분산시킬 수 없기 때문입니다. 따라서 소매업체나 브랜드 소유자가 포장 비용에 매우 민감한 대중 시장 제품보다 프리미엄 음료 프로그램을 통해 이 시장에 진입하는 것이 더 쉽습니다. XOLUTION사가 연간 최대 9억 개의 뚜껑 생산 능력을 목표로 하는 움직임은 재밀봉 가능 캔 시장에서 규모 확대가 비용 절감의 핵심이 되는 이유를 보여줍니다.

부문별 분석

2025년 기준으로, 일반적인 재밀봉 가능 캔은 재밀봉 가능 캔 시장의 68.73%를 차지하며, 다른 제품 형태보다 훨씬 앞선 비중을 보였습니다. 이러한 장점은 기존 고속 충전·시밍 라인과의 호환성에서 비롯되며, 음료 제조업체의 추가 설비 투자 필요성을 줄여줍니다. 이러한 인프라와의 호환성 덕분에, 처리 능력이나 사용 편의성이 캡의 첨단 기능보다 여전히 더 중요하게 여겨지는 분야에서는 표준 형식이 지속적인 우위를 유지하고 있습니다. 따라서 재밀봉 가능 캔 시장은 프리미엄 틈새 시장에서 새로운 디자인이 주목을 받고 있음에도 불구하고, 여전히 표준 사양을 주요 판매 기반으로 삼고 있습니다. 이 기존 라인의 장점은 예측 기간 내내 표준 형식의 중요성을 유지해 줄 것으로 보입니다.

나사식 및 스크류 캡 캔은 고탄산 음료 시장에서 90 psi를 초과하는 압력을 장기간 유지할 수 있는 능력에 힘입어, 2031년까지 연평균 성장률(CAGR) 5.86%를 나타낼 것으로 전망됩니다. 이러한 성능 덕분에, 개봉 후 탄산 가스 유지가 필수적인 스파클링 음료, 수제 맥주 및 특정 에너지 드링크 용도에서 이 캔들은 매력적인 선택지가 되고 있습니다. 슬라이드 탭이나 스냅핏 시스템은 발전하고 있지만, 가혹한 가압 환경에서는 여전히 나사식 방식이 더 우수한 솔루션을 제공합니다. 하이브리드/다중 소재 캔은 재밀봉 가능 캔 업계에서 여전히 소규모 비중을 차지하고 있으며, 차단 성능이 추가 비용을 정당화할 수 있는 퍼스널케어, 의약품 및 기타 용도 분야에서 그 관련성이 더욱 제한적입니다. 캡의 경제성이 향상됨에 따라, 재밀봉 가능 캔 시장에서는 프리미엄 제품의 신규 출시 시 나사식 제품이 더 큰 점유율을 차지하게 될 것입니다.

2025년 기준으로 알루미늄은 재밀봉 가능 캔 시장의 41.58%를 차지했으며, 알루미늄 재밀봉 가능 캔 시장은 2031년까지 연평균 성장률(CAGR) 6.08%로 확대될 것으로 전망됩니다. 알루미늄이 주도적인 위치를 차지하고 있는 이유는 경량성, 내식성, 뛰어난 차단 성능은 물론, 브랜드 소유자가 소매업체나 소비자에게 명확하게 전달할 수 있는 확립된 재활용 실적을 갖추고 있기 때문입니다. 재밀봉 가능 캔 시장은 구조적 신뢰성이 극히 중요한 탄산음료 용도에 적합하다는 소재의 특성에도 힘입고 있습니다. 미국에서는 2025년에 알루미늄 음료 캔이 재활용 수거함에서 새로운 캔으로 재탄생하기까지 걸리는 평균 기간이 60일 미만이었으며, 이는 폐쇄형 순환 가치 제안의 속도와 가시성을 입증했습니다. 이러한 기능성과 재활용성의 조화 덕분에 알루미늄은 재밀봉 가능 캔 시장에서 계속해서 중심적인 위치를 차지하고 있습니다.

폐쇄형 순환 경제는 소재의 장기적인 매력도 높여주고 있습니다. 왜냐하면 캔에서 캔으로 재활용하는 시스템은 1차 알루미늄 생산에 비해 탄소 발자국을 90% 이상 줄일 수 있기 때문입니다. 국제알루미늄협회(IAI)도 첨단 폐쇄형 공정(closed-loop process)을 통해 혼합 합금의 재용해에 비해 최대 18% 더 많은 금속을 회수할 수 있으며, 에너지 사용량을 15% 절감할 수 있다고 밝혔습니다. 강판과 양철은 건조식품, 과자, 영양 분말, 산업용 화학약품용 3피스 캔 형태에서 여전히 중요한 역할을 하고 있습니다. 이러한 용도에서는 내압성 요구 사항이 낮고, 비용 경쟁력이 더 중요하게 여겨지기 때문입니다. 플라스틱 재밀봉 가능 용기는 저압 개인 위생 용품 및 화장품 분야에서 여전히 일정한 역할을 하고 있지만, 재활용 성능이 제품 컨셉의 일부가 되는 용도의 경우, 재밀봉 가능 용기 업계는 여전히 금속 소재와의 연계가 더욱 공고합니다.

지역별 분석

2025년 기준으로 북미는 재밀봉 가능 캔 시장의 38.53%를 차지하며, 최대의 지역 시장이 되었습니다. 이 지역은 즉석 음료의 높은 보급률, 밀집된 유통 인프라, 그리고 확립된 알루미늄 캔 제조 거점이라는 이점을 누리고 있습니다. 또한, 미국의 재밀봉 가능 캔 시장은 특히 진열대에서의 가시성과 휴대성이 중시되는 음료 부문에서 포장 차별화를 위한 브랜드의 지속적인 투자에 힘입어 성장하고 있습니다. 크라운 홀딩스는 브라질에 위치한 폰타 그로사 공장의 확장 시설이 2026년 3분기에 상업 생산을 시작할 전망이라고 발표했습니다. 이 시설의 연간 생산 능력은 36억 캔으로, 북미와 남미 전역에 걸친 광범위한 지역 공급을 뒷받침하게 될 것입니다. 북미에서는 여전히 제232조에 따른 알루미늄 관세로 인한 비용 압박에 직면해 있습니다. 이 관세는 2026년 5월까지 알루미늄 제품에 대해 50%의 세율을 유지했으며, 2026년 1월 하순에 미드웨스트 프리미엄이 1파운드당 1달러를 넘어섬에 따라 변환업체들의 불확실성을 높이고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.12%로 확대될 것으로 예상되며, 재밀봉 가능 캔 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 주요 국가들에서는 가처분 소득 증가, 급속한 도시화, 그리고 RTD(Ready-to-Drink) 부문의 확대가 이러한 성장세를 주도하고 있습니다. 볼사는 인도 음료 캔 부문의 견조한 성장과 즉석 음료 및 유제품에 대한 수요 증가를 이유로, 2024년 타로자에 5,500만 달러를 투자한 데 이어 2025년에는 스리 시티에 6,000만 달러를 투자했습니다. 크라운 홀딩스도 2026년 4월, 인도 북부에 2개 라인 규모의 신규 공장을 건설할 것이라고 발표했습니다. 2027년 하반기부터는 연간 22억 캔의 생산이 예상됩니다. 캔팩은 2025년 결산 보고서에서 인도가 판매량 증가에 크게 기여하고 있다고 지적했으며, 이는 재밀봉 가능 캔 시장에 대한 광범위한 지역 전망과 일치합니다.

2025년, 유럽은 재밀봉 가능 캔 시장에서 중요한 위치를 차지했으며, 독일, 영국, 프랑스, 이탈리아가 주요 소비 거점으로 자리 잡았습니다. 또한, 이 지역에서는 보증금 환급 제도(DRS)의 도입이 진행되고 있으며, 이러한 제도는 캔 회수의 경제성을 높이고 고급 금속 포장의 장기적인 도입 근거를 강화함으로써 해당 시장을 뒷받침하고 있습니다. 포르투갈에서는 2026년 4월 10일부터 ‘Volta DRS’ 제도가 도입되어, 3리터 미만의 알루미늄 및 강철 캔에 대해 개당 0.10달러의 보증금이 부과되고 있습니다. 스페인의 음료 용기 보증금 환불 제도에 대한 법정 기한은 2026년 11월이며, 영국에서는 20펜스의 정액 보증금을 부과하는 제도가 2027년 10월에 도입될 예정임이 확정되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the resealable cans market size is projected to expand from USD 2.32 billion in 2025 and USD 2.57 billion in 2026 to USD 3.31 billion by 2031, registering a CAGR of 5.23% between 2026 and 2031.

This report is Segmented by Product Type (Standard Resealable Cans, Threaded/Screw-Top Cans, and Hybrid/Multi-Material Cans), Material Type (Aluminum, Steel and Tinplate, and Plastic), Capacity (Up To 350 Ml, 351-750 Ml, and Above 750 Ml), End-User Industry (Food and Beverage, Personal Care and Cosmetics, Pharmaceuticals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Resealable Cans Market Trends and Insights

Rising Demand for On-The-Go Beverage Packaging

Portable consumption continues to support the resealable cans market because consumers increasingly use beverage packs outside the home and across multiple occasions. This matters most in 330 ml to 500 ml products, where not every drink is consumed at once, and spill resistance adds direct functional value. Energy drinks, sparkling water, and fitness beverages benefit more from resealability because product loss after opening can change how and where consumers use them. Brands also started using resealable packaging as a visible retail differentiator, as shown by Re: Lid USA's April 2026 launch at Gelson's Markets in Southern California. As this behavior spreads across convenience and immediate-consumption channels, the resealable cans market is likely to secure broader placement in beverage portfolios.

Shift Toward Recyclable Metal Packaging

The resealable cans market is gaining support from aluminum beverage packaging's stronger environmental position. Aluminum beverage cans in the United States had a closed-loop circularity rate of 96.7% and an average recycled content of 71% in 2024, well above comparable levels for glass and PET. In Europe, the aluminum beverage can recycling rate reached 76.3% in 2023, reinforcing the appeal of metal packaging in regulatory environments that are increasingly focused on recovery and recycled content. The resealable cans market benefits even more when closure systems preserve mono-material construction, because that lowers packaging complexity and improves recycling alignment. Sonoco positioned its CapOnCan system in exactly that way at Interpack 2026, highlighting mono-material steel construction and lower EPR fee exposure for food and pet food applications.

High Closure and Conversion Costs Versus Standard Ends

The largest structural brake on the resealable cans market remains the extra cost of the closure compared with a standard stay-on-tab end. Resealable systems require more parts, tighter manufacturing tolerances, and, in some cases, changes in filling-line handling that many beverage producers have not yet installed. That burden is more difficult for smaller and mid-sized brands because they cannot spread equipment and conversion costs across very high production runs. The market is therefore more accessible to premium beverage programs than to mass-market products, where retailers and brand owners are highly sensitive to packaging cost. XOLUTION's move toward a capacity of up to 900 million lids per year shows why scale is central to cost compression in the resealable cans market.

Other drivers and restraints analyzed in the detailed report include:

- Premiumization of Ready-To-Drink Beverages

- Innovation In User-Friendly Closure Systems

- Competition from Standard Cans and PET Bottles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standard resealable cans accounted for 68.73% of the resealable cans market in 2025, leaving them well ahead of other product formats. Their lead stemmed from compatibility with the installed base of high-speed filling and seaming lines, reducing the need for additional capital spending by beverage producers. That infrastructure fit gives standard formats a durable advantage in categories where throughput and operational simplicity still carry more weight than closure sophistication. The resealable cans market, therefore, continues to rely on standard configurations as its main volume base, even while newer designs gain attention in premium niches. This installed-line advantage should keep standard formats relevant through the forecast period.

Threaded and screw-top cans are projected to expand at a 5.86% CAGR through 2031, supported by their ability to retain pressure above 90 psi for longer periods in high-carbonation use cases. That performance makes them attractive for sparkling beverages, craft beer, and selected energy drink applications where carbonation retention after reopening is essential. Slide-tab and snap-fit systems have advanced, but threaded formats still offer a stronger solution in demanding pressure environments. Hybrid/multi-material cans remain a smaller part of the resealable cans industry, with more selective relevance in personal care, pharmaceuticals, and other applications where barrier properties justify added cost. As closure economics improve, the resealable cans market is likely to see threaded variants take a larger share of premium launch activity.

Aluminum held 41.58% of the resealable cans market share in 2025, and the aluminum resealable cans market is projected to expand at a 6.08% CAGR through 2031. Aluminum leads because it combines low weight, corrosion resistance, and strong barrier performance with an established recycling narrative that brand owners can communicate clearly to retailers and consumers. The resealable cans market is also supported by the material's suitability for carbonated beverage applications, where structural reliability is critical. In the United States, aluminum beverage cans moved from the recycling bin to a newly formed can in less than 60 days on average in 2025, reinforcing the speed and visibility of the closed-loop value proposition. This combination of functionality and circularity keeps aluminum at the center of the resealable cans market.

Closed-loop recycling also improves the material's long-term appeal because can-to-can systems can cut carbon footprint by more than 90% compared with primary aluminum production. The International Aluminum Institute also stated that advanced closed-loop processes can recover up to 18% more metal and lower energy use by 15% compared with mixed-alloy remelting. Steel and tinplate remain important in three-piece can formats for dry goods, confectionery, nutritional powders, and industrial chemicals, where pressure demands are lower and cost competitiveness matters more. Plastic resealable cans keep a role in low-pressure personal care and cosmetic uses, but the resealable cans industry remains more strongly aligned with metal in applications where recycling performance is part of the product story.

Geography Analysis

North America accounted for 38.53% of the resealable cans market in 2025, making it the largest regional market. The region benefits from strong penetration of ready-to-drink beverages, a dense distribution infrastructure, and an established aluminum can manufacturing base. The resealable cans market in the United States is also supported by ongoing brand investment in packaging differentiation, especially in beverage categories where shelf visibility and portability matter. Crown Holdings stated that its expanded Ponta Grossa plant in Brazil is expected to begin commercial production in Q3 2026, with an annual capacity of 3.6 billion cans, supporting broader regional supply across the Americas. North America still faces cost pressure from Section 232 aluminum tariffs, which maintained a 50% rate on aluminum articles through May 2026 and pushed converter uncertainty higher as the Midwest Premium moved above USD 1 per pound in late January 2026.

Asia-Pacific is projected to expand at a 6.12% CAGR through 2031, making it the fastest-growing region in the resealable cans market. Rising disposable income, rapid urbanization, and expanding ready-to-drink categories are driving that pace across major countries. Ball invested USD 60 million in Sri City in 2025, following a USD 55 million investment in Taloja in 2024, citing strong growth in India's beverage can sector and stronger demand for ready-to-drink beverages and dairy products. Crown Holdings also announced a greenfield two-line facility in Northern India in April 2026, with expected output of 2.2 billion cans annually from the second half of 2027. CANPACK reported 2025 results that pointed to India as a meaningful incremental contributor to volume growth, which fits the broader regional outlook for the resealable cans market.

Europe held a significant position in the resealable cans market in 2025, with Germany, the United Kingdom, France, and Italy serving as the main consumption centers. The region is also gaining support from deposit return systems, because those programs strengthen can recovery economics and improve the long-term case for premium metal packaging. Portugal launched the Volta DRS on April 10, 2026, covering aluminum and steel cans below 3 liters with a USD 0.10 deposit per unit. Spain's statutory deadline for a beverage container deposit return system is November 2026, and the UK's confirmed scheme is scheduled for October 2027 with a flat 20 pence deposit.

- Crown Holdings, Inc.

- Ball Corporation

- Ardagh Metal Packaging S.A.

- CANPACK S.A.

- Toyo Seikan Group Holdings, Ltd.

- Silgan Holdings Inc.

- CPMC Holdings Limited

- Nampak Limited

- Envases Universales de Mexico, S.A.P.I. de C.V.

- Kian Joo Can Factory Berhad

- Mahmood Saeed Can and End Industry Company Limited

- SWAN Industries (Thailand) Company Limited

- Showa Aluminum Can Corporation

- XOLUTION Germany GmbH

- can2close GmbH

- Top Cap Holding GmbH

- Save-ty Can Cap B.V.

- Canovation LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for On-the-Go Beverage Packaging

- 4.2.2 Shift Toward Recyclable Metal Packaging

- 4.2.3 Premiumization of Ready-to-Drink Beverages

- 4.2.4 Innovation in User-Friendly Closure Systems

- 4.2.5 Deposit Return Scheme Expansion Improving Can-to-Can Economics

- 4.2.6 Hygiene and Anti-Spiking Use Cases Favoring Covered Drinking Surfaces

- 4.3 Market Restraints

- 4.3.1 High Closure and Conversion Costs Versus Standard Ends

- 4.3.2 Competition From Standard Cans and PET Bottles

- 4.3.3 Compliance Complexity for PFAS and Bisphenol-Free Food-Contact Systems

- 4.3.4 Aluminum Tariffs and Premium Volatility

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Standard Resealable Cans

- 5.1.2 Threaded / Screw-Top Cans

- 5.1.3 Hybrid / Multi-Material Cans

- 5.2 By Material Type

- 5.2.1 Aluminum

- 5.2.2 Steel and Tinplate

- 5.2.3 Plastic

- 5.3 By Capacity

- 5.3.1 Up to 350 ml

- 5.3.2 351 ml to 750 ml

- 5.3.3 Above 750 ml

- 5.4 By End-User Industry

- 5.4.1 Food and Beverage

- 5.4.2 Personal Care and Cosmetics

- 5.4.3 Chemicals

- 5.4.4 Pharmaceuticals

- 5.4.5 Paints and Lubricants

- 5.4.6 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Crown Holdings, Inc.

- 6.4.2 Ball Corporation

- 6.4.3 Ardagh Metal Packaging S.A.

- 6.4.4 CANPACK S.A.

- 6.4.5 Toyo Seikan Group Holdings, Ltd.

- 6.4.6 Silgan Holdings Inc.

- 6.4.7 CPMC Holdings Limited

- 6.4.8 Nampak Limited

- 6.4.9 Envases Universales de Mexico, S.A.P.I. de C.V.

- 6.4.10 Kian Joo Can Factory Berhad

- 6.4.11 Mahmood Saeed Can and End Industry Company Limited

- 6.4.12 SWAN Industries (Thailand) Company Limited

- 6.4.13 Showa Aluminum Can Corporation

- 6.4.14 XOLUTION Germany GmbH

- 6.4.15 can2close GmbH

- 6.4.16 Top Cap Holding GmbH

- 6.4.17 Save-ty Can Cap B.V.

- 6.4.18 Canovation LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment