|

시장보고서

상품코드

2064499

미국의 환자 참여 솔루션 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Patient Engagement Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

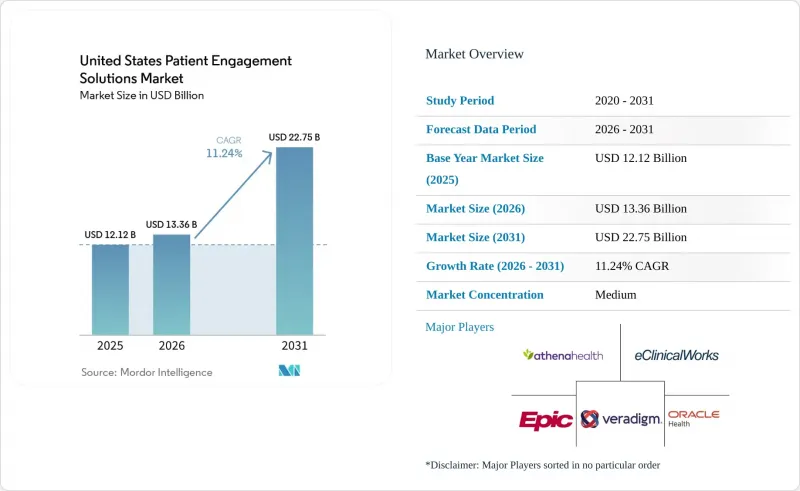

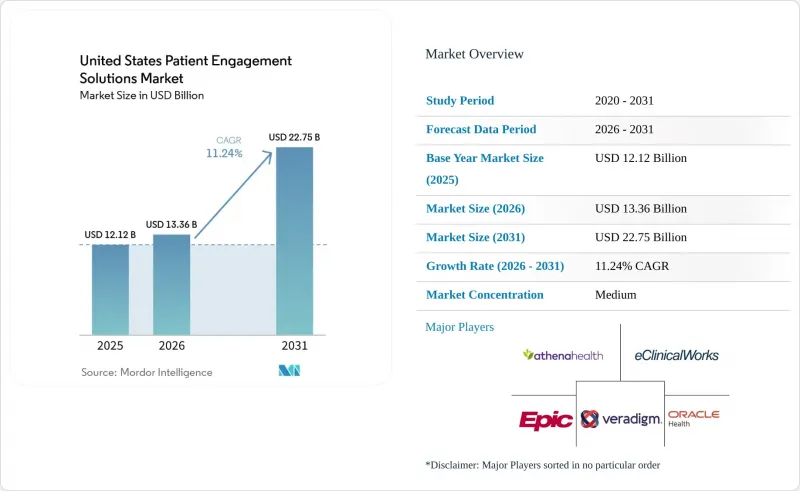

Mordor Intelligence에 의하면, 미국의 환자 참여 솔루션 시장 규모는 2025년에 121억 2,000만 달러로 평가되었습니다. 2026년에 133억 6,000만 달러에서 2031년까지 227억 5,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 11.24%를 나타낼 것으로 전망됩니다.

본 보고서는 구성 요소(소프트웨어, 서비스, 하드웨어), 솔루션 유형(AI 기반, 포털, 원격의료, RPM, 집단 건강 관리), 제공 모델(웹/클라우드, On-Premise), 기능, 용도, 치료 분야(만성 질환, 여성 대상, 행동·정신 질환, 기타), 최종 사용자(의료 제공업체, 보험사, 약국, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 환자 참여 솔루션 시장 동향 및 인사이트

가치 기반이자 환자 중심의 치료로 전환

미국의 환자 참여 솔루션 시장은 진료 횟수뿐만 아니라, 측정 가능한 임상적 개선에 대해 의료 제공업체 및 보험사에 보상을 제공하는 가치 기반 지불 구조의 혜택을 받고 있습니다. 메디케어 대체 지급 모델(AMP)의 인센티브 지급률은 프로그램 초기 5%에서 2026년에는 1.88%로 하락했습니다. 이로 인해, 과거에는 비효율적인 의료 서비스 조정을 쉽게 감당할 수 있었던 재정적 여유가 줄어들었습니다. 이러한 변화로 인해 계약 이행 및 보고 과정에서 디지털을 활용한 대외 소통, 케어 플랜 후속 조치, 복약 순응도 추적, 그리고 환자 보고를 통한 참여 기록의 중요성이 커지고 있습니다. 또한, CMS의 ACCESS 모델은 의료 제공업체가 혈압 강하나 통증 관리 등 측정 가능한 목표를 달성한 경우, 기술을 활용한 치료에 대해 성과 연계형 지불을 지원하고 있습니다. 미국의 환자 참여 솔루션 시장도 디지털 참여가 가입자의 이용 안내, 치료 격차 해소, 그리고 유지율 향상을 지원하게 되면서 보험사들의 투자가 더욱 활발해지고 있습니다. 유나이티드 헬스케어는 2026년 3월, 회원용 앱 내에 생성형 AI 챗봇 ‘Avery’를 출시함으로써, 대형 보험사가 고객 참여 기능을 핵심적인 혜택 제공의 일부로 자리매김하게 되었음을 보여주고 있습니다.

만성 질환과 고령화로 인한 막대한 부담

미국의 환자 참여 솔루션 시장에는 만성 질환 및 정신 건강 질환이 의료 자금 조달, 제공, 모니터링 방식에 계속해서 영향을 미치고 있기 때문에 지속적인 수요 기반이 존재합니다. CDC(미국 질병통제예방센터)에 따르면, 국내 연간 의료비 4조 9,000억 달러의 90%는 만성 질환이나 정신 건강 문제를 앓고 있는 사람들에게서 비롯된 것으로, 이로 인해 의료 시스템은 진료 간격 동안의 관리 체계를 개선해야 한다는 압박을 지속적으로 받고 있습니다. 여러 가지 만성 질환을 관리하는 환자는 일반적으로 단일 질환에 대한 치료를 받는 환자군보다 더 많은 알림, 교육, 추적 관리 및 기록이 필요합니다. 이러한 추세에 따라, 약물 관리, 증상 모니터링, 케어 플랜 갱신을 통해 지속적인 아웃리치를 유지할 수 있는 플랫폼의 전략적 가치가 높아지고 있습니다. 따라서 미국의 환자 참여 솔루션 시장은 질병 유병률뿐만 아니라, 만성 질환 관리가 의료 제공업체 및 보험사의 업무 흐름 내에서 만들어내는 정기적인 상호작용의 빈도에서도 혜택을 받고 있습니다.

EHR, 보험사 및 포인트 솔루션 스택 간의 상호 운용성 격차

미국의 환자 참여 솔루션 시장은 환자 데이터가 종종 서로 연동되지 않은 의료 제공업체, 보험사 및 전문 워크플로 시스템에 분산되어 존재하기 때문에 여전히 구조적인 제약에 직면해 있습니다. 『Frontiers in Health Services』 저널의 2025년 체계적 문헌고찰에서는 HL7 FHIR과 SNOMED CT 구현에 있어 의미론적 불일치, 시스템 간 교환의 제한, 환자 생성 건강 데이터의 통합 부족 등 뿌리 깊은 장벽들이 지적되었습니다. 이는 표준 규격을 채택하는 것만으로는 환자 참여 플랫폼 내에서 실용적인 종단적 기록이 보장되지 않는다는 것을 의미합니다. 미국 보건복지부(HHS)의 한 고위 관계자는 2025년 『JAMA』지에 실린 기사에서 환자 경험 향상을 위한 EHR 데이터의 잠재력을 최대한 발휘하기 위해서는 여전히 데이터 교환 및 구현에 대한 보다 통일된 접근 방식이 필요하다고 밝혔습니다. 포털, 알림, 보험사와의 접점에서 정보가 불완전하거나 일관성이 없는 것처럼 보일 경우, 환자는 디지털 채널을 신뢰하기 어려워집니다. 따라서 미국의 환자 참여 솔루션 시장은 공급업체가 지원한다고 내세우는 인터페이스의 수뿐만 아니라, 운영상의 통합 수준에 의해서도 계속해서 제약을 받고 있습니다.

부문별 분석

2025년, 미국의 환자 참여 솔루션 시장에서 소프트웨어는 58.66%를 차지하며, 지출 구성에서 서비스 및 하드웨어를 크게 앞질렀습니다. 이 리드는 단일 디지털 레이어 내에서 이루어지는 커뮤니케이션, 일정 관리, 접수, 알림, 교육, 케어 조정에 대한 플랫폼 수요의 규모를 반영하고 있습니다. 통합 솔루션은 공급업체의 난립을 억제하고, 확립된 임상 워크플로우에 쉽게 적응할 수 있기 때문에 대규모 의료 시스템에 있어 여전히 선호되는 선택지입니다. 독립형 용도는 접수 업무 최적화, 환자 대상 자금 조달, 행동 지원과 같은 제한적인 이용 사례에서 여전히 중요한 역할을 수행하고 있는데, 이는 이러한 분야에서 구매자가 보다 상세한 설정을 원하는 경우가 많기 때문입니다. 미국의 환자 참여 솔루션 시장에서는 워크플로우에 대한 폭넓은 지원 범위와 신속한 도입, 그리고 의료진이 쉽게 도입할 수 있는 점을 모두 갖춘 공급업체가 계속해서 높은 평가를 받고 있습니다.

서비스 부문은 2031년까지 연평균 성장률(CAGR) 12.39%로 가장 빠른 성장세를 보일 것으로 예상되며, 이는 플랫폼이 고도화됨에 따라 도입의 복잡성이 증가하고 있음을 보여줍니다. AI 에이전트나 FHIR 기반 연결이 보편화됨에 따라, 의료 시스템 분야에서는 도입 지원, 통합 작업, 직원 교육, 지속적인 최적화, 규정 준수 지도에 대한 수요가 높아지고 있습니다. Phreesia는 2026년도 이해관계자 서한에서 2025년에 1억 8,000만 건 이상의 환자 내원을 가능하게 했다고 밝혔으며, AccessOne 인수를 통해 사업 범위를 확대하고 플랫폼 제공 서비스에 환자 대상 대출 기능을 추가했습니다. 하드웨어는 여전히 핵심 지출 분야라기보다는 보조적인 수준에 머물러 있지만, 키오스크, 병상용 기기, 태블릿, 신원 확인 도구는 외래 및 입원 환경에서 여전히 중요한 역할을 수행하고 있습니다. Oracle Health의 CLEAR 통합은 신원 확인이 디지털 접수 및 종이 없는 체크인 워크플로우에 통합되어 있음을 보여주며, 소프트웨어가 가장 큰 비중을 차지하는 상황에서도 특정 하드웨어 관련 기능의 중요성이 여전히 유지되고 있음을 시사합니다.

AI를 활용한 환자 참여 솔루션은 2025년에 솔루션 유형별 부문의 30.51%를 차지하며, 미국의 환자 참여 솔루션 시장에서 가장 큰 카테고리가 되었습니다. 이러한 우위는 지능형 아웃리치, 대화형 일정 관리, 분류 지원, 치료 공백 해소 도구에서 비롯된 것으로, 현재 기업 현장에서 일상적으로 활용되고 있습니다. 도입 기반이 탄탄한 플랫폼은 시간이 지남에 따라 방대한 행동 데이터 세트를 구축합니다. 이를 통해 개인 맞춤화가 향상되며, 새로운 상호작용이 이루어질 때마다 제품의 유용성이 높아집니다. 이러한 우위는 중요합니다. 왜냐하면 환자의 반응 패턴, 선호하는 채널, 타이밍과 관련된 행동은 신규 시장 진출기업이 신속하게 재현하기 어려운 방식으로 아웃리치의 질을 좌우하기 때문입니다. 따라서 미국의 환자 참여 솔루션 시장에서는 솔루션 간의 경쟁이 개별 기능에서 데이터에 기반한 워크플로우의 성과로 점차 전환되고 있습니다.

원격 환자 모니터링 시장은 2031년까지 연평균 성장률(CAGR) 11.95%로 확대될 것으로 예상되며, 예측 기간 동안 가장 빠르게 성장하는 솔루션 유형이 될 것입니다. 이러한 성장은 만성 질환의 유병률, 진료 간격에 따른 모니터링의 보급, 그리고 고위험군에 대한 원격 생리학적 모니터링 활동에 대한 보험 급여 지원과 밀접한 관련이 있습니다. 환자 포털은 여전히 솔루션 수요의 상당 부분을 차지하고 있지만, ONC의 데이터에 따르면 자원이 부족한 병원들 사이에서는 도입 현황과 기능 이용 현황에 차이가 있는 것으로 나타났습니다. 또한, 원격의료 솔루션도 여전히 참여 스택에 통합된 상태입니다. 이는 가상 진료가 현재 많은 의료 현장에서 접근성, 사후 관리, 편의성에 대한 기대를 충족시키고 있기 때문입니다. 집단건강관리 도구, 복약 알림, 접수 플랫폼 및 재무 참여 시스템은 서로 병행하여 지속적으로 판매되고 있으며, 이는 보다 광범위한 플랫폼 생태계 내에서 다중 솔루션 구매를 촉진하고 있습니다.

웹 기반 및 클라우드 기반 제공 형태는 2025년에 67.35%의 점유율을 차지했으며, 2031년까지 연평균 성장률(CAGR) 13.33%를 기록하며 가장 빠르게 성장하는 모델이기도 합니다. 이러한 조합은 미국의 환자 참여 솔루션 시장에서 주요 제공 모델이 성장 둔화 단계에 접어드는 것이 아니라 여전히 성장세를 이어가고 있음을 보여줍니다. 의료 시스템은 클라우드 도입을 선호하고 있습니다. 그 이유는 더 신속한 업그레이드, 더 유연한 확장성, 그리고 여러 거점에 걸쳐 AI 기능을 쉽게 배포할 수 있기 때문입니다. Change Healthcare에 대한 사이버 공격으로 인해, 2024년 이후 많은 조직이 인프라의 내결함성, 공급업체에 대한 의존도, 그리고 복구 체계를 더욱 시급하게 재검토해야 할 상황에 놓이게 되었습니다. 또한, 현대의 참여 플랫폼은 정기적인 워크플로우 조정, 보안 업데이트 및 모델 변경이 필요하기 때문에 빈번한 릴리스 주기도 클라우드 환경에 더 적합합니다.

On-Premise 방식의 제공은 연방 정부 환경, 규제가 엄격한 전문 분야, 그리고 보다 엄격한 네트워크 분리 요건을 가진 조직에서 여전히 일정한 역할을 수행하고 있습니다. 내부 거버넌스가 보수적이거나 레거시 인프라가 깊게 뿌리내린 경우, 일부 의료 서비스 제공업체는 여전히 도입 및 데이터 흐름에 대한 현지 관리를 선호합니다. HITRUST나 FedRAMP와 같은 조달 기준 역시 기밀성이 높은 프로그램이나 공공 자금을 지원하는 프로그램에 서비스를 제공하는 클라우드 공급업체에 대한 진입 장벽을 높이고 있으며, 이로 인해 소규모 신규 업체 시장 진입이 지연될 가능성이 있습니다. Oracle Health의 QHIN 및 CMS Aligned Network에서의 활동을 통해, 상호 운용성에 대한 기대와 제공 아키텍처가 개별적으로가 아니라 통합적으로 계획되는 경향이 강해지고 있음을 알 수 있습니다. 따라서 미국의 환자 참여 솔루션 시장은 특정 기업 환경에서는 On-Premise 방식이 여전히 중요하지만, 기본적으로 클라우드 우선 도입 방식으로 전환되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the united states patient engagement solutions market size is projected to be USD 12.12 billion in 2025, USD 13.36 billion in 2026, and reach USD 22.75 billion by 2031, growing at a CAGR of 11.24% from 2026 to 2031.

This report is Segmented by Component (Software, Services, Hardware), Solution Type (AI-Driven, Portals, Telehealth, RPM, Population Health), Delivery Model (Web/Cloud, On-Premise), Functionality, Application, Therapeutic Area (Chronic, Women's, Behavioral & Mental, Others), and End User (Providers, Payers, Pharmacies, Others). The Market Forecasts are Provided in Terms of Value (USD).

United States Patient Engagement Solutions Market Trends and Insights

Shift to Value-Based and Patient-Centric Care

The United States patient engagement solutions market is benefiting from value-based payment structures that reward providers and payers for measurable clinical improvement rather than visit volume alone. The Medicare Alternative Payment Model incentive payment rate fell to 1.88% in 2026 from 5% in earlier program years, which reduced the financial cushion that once made inefficient care coordination easier to absorb. That change is making digital outreach, care plan follow-up, adherence tracking, and patient-reported engagement records more important for contract performance and reporting. CMS's ACCESS model also supports outcome-aligned payments for technology-enabled care when providers achieve measurable targets such as blood pressure reduction or pain management. The United States patient engagement solutions market is also drawing stronger payer investment, as digital engagement now supports member navigation, care gap closure, and retention. UnitedHealthcare launched Avery in March 2026 as a generative AI companion inside its member app, showing that large payers now treat engagement capability as part of core benefit delivery.

High Chronic Disease and Aging Burden

The United States patient engagement solutions market has a durable demand base because chronic and mental health conditions continue to shape how care is financed, delivered, and monitored. CDC states that 90% of the nation's USD 4.9 trillion in annual healthcare spending is attributable to people with chronic and mental health conditions, which keeps pressure on health systems to improve between-visit management. Patients managing multiple long-duration conditions typically require more reminders, more education, more follow-up, and more documentation than episodic care populations. That pattern increases the strategic value of platforms that can keep outreach continuous across medication use, symptom monitoring, and care plan updates. The United States patient engagement solutions market, therefore, benefits not just from disease prevalence, but from the recurring interaction frequency that chronic care creates inside provider and payer workflows.

Interoperability Gaps Across EHR, Payer, and Point-Solution Stacks

The United States patient engagement solutions market still faces a structural limit because patient data often sits across disconnected provider, payer, and specialized workflow systems. A 2025 systematic review in Frontiers in Health Services found persistent barriers, including semantic misalignment across HL7 FHIR and SNOMED CT implementations, limited cross-system exchange, and weak integration of patient-generated health data. That means standards adoption alone does not guarantee a usable longitudinal record inside patient engagement platforms. HHS leadership wrote in a 2025 JAMA article that unlocking the potential of EHR data for patient experience improvement still requires a more unified approach to exchange and implementation. When information appears incomplete or inconsistent across portals, reminders, and payer touchpoints, patients are less likely to trust the digital channel. The United States patient engagement solutions market, therefore, remains constrained by operational integration quality, not just by the number of interfaces a vendor can claim to support.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Digital Front-Door and AI Engagement Adoption

- CMS Interoperability and Prior Authorization API Rollout

- Data Privacy, Cybersecurity, and HIPAA Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 58.66% of the United States patient engagement solutions market in 2025, which kept it well ahead of services and hardware in the spending mix. That lead reflects the scale of platform demand for communication, scheduling, intake, reminders, education, and care coordination inside one digital layer. Integrated suites remain the preferred choice for large health systems because they reduce vendor sprawl and fit more easily inside established clinical workflows. Standalone applications still hold an important role in narrower use cases such as intake optimization, patient financing, and behavioral outreach, where buyers often want deeper configuration. The United States patient engagement solutions market continues to reward software vendors that can combine workflow breadth with faster implementation and easier clinician adoption.

Services are projected to record the fastest component growth at a 12.39% CAGR through 2031, which shows that deployment complexity is rising with platform sophistication. Health systems increasingly need implementation support, integration work, staff training, ongoing optimization, and compliance guidance as AI agents and FHIR-based connectivity become more common. Phreesia stated in its FY2026 stakeholder letter that it enabled more than 180 million patient visits in 2025 and expanded its scope through the AccessOne acquisition, which added patient financing capability to its platform offering. Hardware remains a supporting layer rather than the core spending center, but kiosks, bedside devices, tablets, and identity tools still matter in ambulatory and inpatient settings. Oracle Health's CLEAR integration shows how identity verification is being folded into digital intake and paper-free check-in workflows, which keeps certain hardware-linked functions relevant even as software takes the largest share.

AI-driven engagement held 30.51% of the solution type segment in 2025, making it the largest category inside the United States patient engagement solutions market. Its lead comes from intelligent outreach, conversational scheduling, triage support, and care gap closure tools that are now moving into routine enterprise use. Platforms with larger installed bases also build richer behavioral datasets over time, which improves personalization and makes the product more useful with each new interaction. That advantage matters because patient response patterns, channel preferences, and timing behavior can shape outreach quality in ways that are difficult for newer entrants to replicate quickly. The United States patient engagement solutions market is, therefore, seeing solution competition move from isolated features toward data-backed workflow performance.

Remote patient monitoring is forecast to expand at an 11.95% CAGR through 2031, which makes it the fastest-growing solution type over the forecast period. Its growth is tied to chronic disease prevalence, wider use of between-visit monitoring, and reimbursement support for remote physiologic monitoring activities in higher-risk populations. Patient portals still account for a meaningful share of solution demand, but ONC data shows that adoption and capability use remain uneven among lower-resourced hospitals. Telehealth solutions also remain embedded in the engagement stack because virtual care now supports access, follow-up, and convenience expectations across many care settings. Population health tools, medication reminders, intake platforms, and financial engagement systems continue to sell alongside one another, which is encouraging multi-solution purchasing inside broader platform ecosystems.

Web-based and cloud-based delivery held 67.35% share in 2025 and is also the fastest-growing model at a 13.33% CAGR through 2031. That combination shows that the dominant delivery model in the United States patient engagement solutions market is still gaining ground rather than moving into a slow-growth phase. Health systems favor cloud deployment because it supports faster upgrades, more flexible scaling, and easier rollout of AI-enabled features across multiple sites. The Change Healthcare attack pushed many organizations to review infrastructure resilience, vendor dependencies, and recovery preparedness with greater urgency after 2024. Frequent release cycles also suit cloud environments better, since modern engagement platforms need regular workflow tuning, security updates, and model changes.

On-premise delivery still retains a role in federal settings, highly regulated specialty environments, and organizations with stricter network isolation requirements. Some providers continue to prefer local control over deployment and data flows when internal governance is more conservative or when legacy infrastructure remains deeply embedded. Procurement standards such as HITRUST and FedRAMP have also raised the bar for cloud vendors serving sensitive or publicly funded programs, which can slow smaller entrants. Oracle Health's QHIN and CMS Aligned Network activity shows that interoperability expectations and delivery architecture are increasingly being planned together rather than separately. The United States patient engagement solutions market is therefore moving toward cloud-first deployment as the default, even though on-premise options still matter in selected enterprise environments.

List of Companies Covered in this Report:

- athenahealth

- eClinicalWorks

- Epic Systems

- Experian Health

- Get Well

- Luma Health

- Mckesson

- Meditech

- NextGen Healthcare

- Oracle

- Phreesia, Inc.

- Press Ganey

- Salesforce

- Solutionreach, Inc.

- TeleVox

- TruBridge, Inc.

- Veradigm

- WellSky

- Xealth

- Yosi Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift To Value-Based and Patient-Centric Care

- 4.2.2 High Chronic Disease and Aging Burden

- 4.2.3 Rapid Digital Front-Door and AI Engagement Adoption

- 4.2.4 Consumer Demand for Self-Service Access and Communication

- 4.2.5 CMS Interoperability and Prior Authorization API Rollout

- 4.2.6 CMS Healthtech Ecosystem and Medicare App Library Discovery Layer

- 4.3 Market Restraints

- 4.3.1 Interoperability Gaps Across EHR, Payer, And Point-Solution Stacks

- 4.3.2 Data Privacy, Cybersecurity, and HIPAA Compliance Burden

- 4.3.3 Portal And App Fragmentation Reducing Longitudinal Engagement

- 4.3.4 AI Governance and ROI Scrutiny Slowing Enterprise Rollouts

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Integrated patient engagement platforms

- 5.1.1.2 Standalone patient engagement applications

- 5.1.2 Services

- 5.1.2.1 Implementation and integration services

- 5.1.2.2 Training and education services

- 5.1.2.3 Support and maintenance services

- 5.1.2.4 Consulting and optimization services

- 5.1.3 Hardware

- 5.1.3.1 Bedside engagement devices

- 5.1.3.2 Self-service kiosk and check-in devices

- 5.1.3.3 Patient tablets and remote devices

- 5.1.1 Software

- 5.2 By Solution Type

- 5.2.1 AI-driven engagement

- 5.2.2 Patient portals

- 5.2.3 Telehealth solutions

- 5.2.4 Remote patient monitoring solutions

- 5.2.5 Population health and outreach solutions

- 5.2.6 Appointment and medication reminder solutions

- 5.2.7 Patient intake and registration solutions

- 5.2.8 Financial engagement solutions

- 5.3 By Delivery Model

- 5.3.1 Web-based and cloud-based

- 5.3.2 On-premise

- 5.4 By Functionality

- 5.4.1 Communication and messaging

- 5.4.2 Scheduling and access

- 5.4.3 Clinical enablement

- 5.4.4 Financial and administrative workflow

- 5.4.5 Analytics and personalization

- 5.5 By Application

- 5.5.1 Health management

- 5.5.2 Home and remote care management

- 5.5.3 Care coordination and communication

- 5.5.4 Social and behavioral management

- 5.5.5 Financial health management

- 5.6 By Therapeutic Area

- 5.6.1 Chronic diseases

- 5.6.1.1 Diabetes

- 5.6.1.2 Cardiovascular diseases

- 5.6.1.3 Respiratory diseases

- 5.6.1.4 Oncology

- 5.6.1.5 Obesity and metabolic disorders

- 5.6.1.6 Other chronic diseases

- 5.6.2 Women's health

- 5.6.3 Behavioral and mental health

- 5.6.4 Other therapeutic areas

- 5.6.1 Chronic diseases

- 5.7 By End User

- 5.7.1 Providers

- 5.7.2 Payers

- 5.7.3 Pharmacies

- 5.7.4 Other End Users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 athenahealth

- 6.3.2 eClinicalWorks

- 6.3.3 Epic Systems Corporation

- 6.3.4 Experian Health

- 6.3.5 Get Well

- 6.3.6 Luma Health

- 6.3.7 McKesson Corporation

- 6.3.8 MEDITECH

- 6.3.9 NextGen Healthcare, Inc.

- 6.3.10 Oracle

- 6.3.11 Phreesia, Inc.

- 6.3.12 Press Ganey

- 6.3.13 Salesforce

- 6.3.14 Solutionreach, Inc.

- 6.3.15 TeleVox

- 6.3.16 TruBridge, Inc.

- 6.3.17 Veradigm LLC

- 6.3.18 WellSky

- 6.3.19 Xealth

- 6.3.20 Yosi Health

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment