|

시장보고서

상품코드

2064501

미국 흉부 카테터 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Thoracic Catheter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

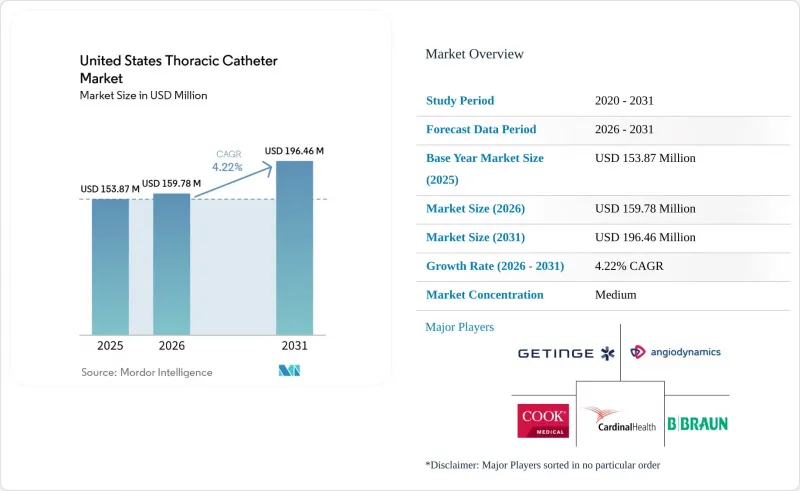

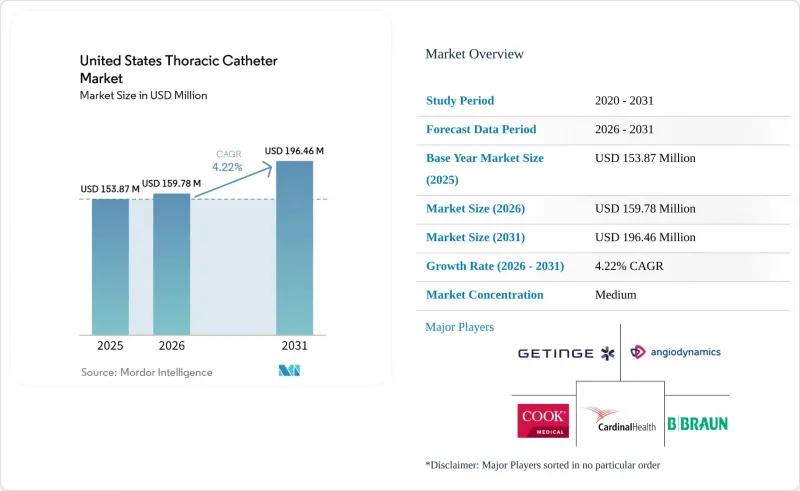

Mordor Intelligence에 의하면, 미국의 흉부 카테터 시장 규모는 2025년 1억 5,387만 달러로 평가되었고, 2026년에는 1억 5,978만 달러로 추정되고, 2031년까지 1억 9,646만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 4.22%로 성장할 전망입니다.

본 보고서는 제품 유형별(흉강 배액 튜브, 흉막 배액 카테터, 기타), 용도별(흉수, 기타), 시술 및 접근법별(셀딩거법, 외과적, 트로카법, 터널법), 모니터링 방식별(기존 아날로그, 디지털 배액), 최종 사용자별(병원, 외래수술센터(ASC), 전문 클리닉, 재택 간호)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 흉부 카테터 시장 동향 및 분석

악성 및 재발성 흉수의 부담 증가

악성 흉수는 대규모의 반복적인 치료 수요를 지속적으로 발생시키고 있기 때문에 흉수 관련 수요는 여전히 미국 흉부 카테터 시장의 핵심을 이루고 있습니다. 미국에서는 매년 약 15만 명의 환자가 악성 흉수 진단을 받고 있으며, 이로 인해 입원 환자에 대한 배액술과 장기적인 외래 관리 접근법 모두에 대한 수요가 증가하고 있습니다. 또한, 암 치료로 인한 생존 기간의 연장도 사례 수 증가에 기여하고 있습니다. 환자들은 질환을 앓고 있음에도 더 오래 생존하게 되었으며, 그 결과 증상 조절이나 반복적인 흉수 관리가 필요한 기간이 길어지고 있기 때문입니다. 흉수 관리 데이터베이스의 증거 역시 시간이 지남에 따라 새로운 악성 흉수 진단 사례가 증가하고 있음을 보여주고 있으며, 이는 미국 흉부 카테터 시장에서 설명된 수요 압박 추세를 뒷받침하는 것입니다. 이러한 치료 기간의 장기화로 인해, 흉막 유착술이나 카테터 제거가 이루어지기 전에 다시 배액이 필요해질 가능성이 높아짐에 따라, 환자 1인당 카테터 사용 횟수가 증가하고 있습니다. 그 결과, 재발성 흉수 관리는 미국 흉부 카테터 시장에서 터널형 흉막 시스템 및 관련 부속품 수요를 견인하는 가장 뚜렷한 요인 중 하나로 자리 잡고 있습니다.

체내 삽입형 흉막 카테터에 대한 1차 선택 지침 채택

고정형 흉막 카테터는 더 이상 최후의 수단으로만 간주되지 않게 되었기 때문에 가이드라인에 포함된 것은 미국 흉부 카테터 시장의 직접적인 성장 동력이 되고 있습니다. 미국흉부학회(ATS), 영국흉부학회(BTS), 유럽호흡기학회(ERS)의 지침에 따르면, 현재 재발성 악성 흉수 관리에 있어 장기 삽입형 흉막 카테터는 다른 1차 치료법과 동등한 위치에 놓여 있습니다. 폐의 팽창 능력이 저하된 환자의 경우, 지침에서 이러한 상황에서는 활석 흉막 유착술보다 삽입형 흉막 카테터를 우선적으로 권장하고 있으므로, 치료의 우선순위는 더욱 명확합니다. 또한, 현재의 의료 격차도 중요한 요인입니다. 미국에서는 적격 환자의 불과 24%만이 지침에 따른 근치적 치료를 받고 있어, 이로 인해 흉막 중재술에 대한 접근성을 확대하는 프로그램에 있어 큰 전환의 기회가 남아 있습니다. 임상 경험 또한 이 모델을 뒷받침하고 있습니다. 한 전향적 코호트 연구에 따르면, 삽입형 흉막 카테터를 사용한 환자의 44%에서 자연적인 흉막 유착이 보고되었으며, 흉수의 pH 값과 단백 수치가 높을수록 성공률이 높은 것으로 나타났습니다. 가이드라인에 따른 강력한 지지와 임상 현장에서의 미활용이 결합됨에 따라, 미국의 흉부 카테터 시장은 새로운 적응증에 전적으로 의존하지 않고도 성장할 여지가 있습니다.

예산 압박과 GPO 주도의 상품화

예산 압박은 미국 흉부 카테터 시장에 여전히 실질적인 걸림돌로 작용하고 있습니다. 이는 병원이 규모의 경제와 낮은 단가를 중시하는 계약을 통해 표준 배액 제품을 계속해서 대량으로 구매하고 있기 때문입니다. 이는 제품 차별화가 제한적이며, 조달 팀이 대규모 의료 시스템 전반에 걸친 가격 일관성을 중시하는 기존 흉강 배액관이나 기본적인 배액 키트에서 가장 두드러지게 나타납니다. 그 결과, 시장은 양극화되고 있습니다. 표준 제품은 지속적인 가격 압박에 직면하고 있는 반면, 디지털 통합 시스템이나 특수한 삽입형 흉막 카테터 플랫폼은 임상적 가치가 명확하다면 프리미엄 가격을 유지할 가능성이 높아지고 있습니다. 이러한 격차로 인해 도입이 지연되고 있습니다. 왜냐하면 병원 위원회는 승인된 구매 목록에 새로운 시스템을 추가하기 전에, 더 강력한 운영상 및 임상적 타당성을 요구하는 경우가 많기 때문입니다. 또한, 이는 공급업체의 행동에도 변화를 가져오고 있습니다. 제조업체들은 단순히 기본 카테터 자체만으로 경쟁하는 것이 아니라, 시술에 특화된 키트나 모니터링 플랫폼 형태로 제품을 구성해야 하는 압박을 받고 있기 때문입니다. 그 결과, 미국의 흉부 카테터 시장은 성장을 이어가고 있지만, 혁신 기술이 가격에 민감한 의료 기관에 도달하는 속도는 첨단 흉부 의료 센터에 도달하는 속도보다 더 느립니다.

부문별 분석

2025년 기준으로, 흉막 배액 카테터는 미국 흉부 카테터 시장 규모의 47.23%를 차지했으며, 제품 구성 중 가장 큰 제품군을 형성했습니다. 이러한 주도적인 위상은 재발성 종양성 흉수의 관리부터 응급 및 계획적 입원 치료 시의 단기 배액에 이르기까지 폭넓은 역할을 수행하고 있음을 반영합니다. 터널식 삽입형 흉막 카테터는 임상 지침에 따른 지지도가 높아지고, 외래 치료가 보편화됨에 따라 시술에서 차지하는 비중이 더욱 커지고 있습니다. 비터널형 피그테일 카테터는 진단적 배액, 일시적 흉막 감압, 특정 기흉 사례에서 널리 사용되고 있기 때문에 여전히 수요가 많은 중요한 역할을 담당하고 있습니다. 미국의 흉부 카테터 산업에서 이러한 조합을 통해 흉수 배액 카테터는 광범위한 판매 기반과 프리미엄화 간의 견고한 연계성을 동시에 확보하고 있습니다.

흉강 배액관은 외상, 농흉, 수술 후 관리에서 여전히 중요하지만, 통증 완화와 관절 가동 범위가 중시되는 적응증의 경우, 더 얇은 직경의 제품이 지지를 얻으면서 변화의 방향이 점차 명확해지고 있습니다. 미국의 흉부 카테터 시장에서는 특정 의료 현장에서 더 얇은 직경의 카테터가 불편감을 줄이고, 사용 후 제거 과정을 간소화하면서도 충분한 치료 효과를 가져올 수 있기 때문에 점차 대체되고 있습니다. 트로카르 카테터는 삽입 속도가 여전히 실용적인 이점으로 작용하는 응급 의료 분야의 이용 사례에 힘입어, 2031년까지 연평균 성장률(CAGR)이 5.46%에 달할 전망이며, 가장 빠르게 성장하고 있는 제품 유형입니다. 이 부문에서는 번들로 제공되는 시술 키트도 중요합니다. 이는 병원의 재고 관리를 간소화하고, 편의성과 가격 측면 모두에서 공급업체가 계약상의 지위를 유지하는 데 도움이 되기 때문입니다. 제품 개발은 여전히 신중하게 진행되고 있습니다. PVC에서 폴리우레탄이나 실리콘으로 소재를 변경하는 등의 경우, 새로운 적합성 평가 작업이 필요하며, 이는 의료기기 규정 준수 기준 하에서 중견 기업의 혁신 주기를 지연시킬 가능성이 있기 때문입니다.

2025년 기준으로, 흉수는 미국 흉부 카테터 시장 규모의 36.83%를 차지했으며, 국내 최대 적응증 범주로서의 위상을 유지했습니다. 이 부문의 규모는 악성 흉수 사례 수와 밀접한 관련이 있으며, 미국에서는 연간 약 15만 건의 진단이 이루어지고 있는 만큼, 그 부담은 여전히 높은 수준을 유지하고 있습니다. 흉수 관리에 있어, 악성 사례와 비악성 사례에서는 구매 기준이 다릅니다. 악성 질환의 경우 삽입형 시스템이나 재택 배액용 부속품에 대한 의존도가 높은 반면, 비악성 흉수의 경우 여전히 반복적인 천자나 단기적인 카테터 사용이 일반적이기 때문입니다. 이 때문에 일부 부적응증에서는 고성능 시스템이 선호되는 반면, 다른 적응증에서는 표준 제품이 선호되는 경향이 있어, 미국 흉부 카테터 시장의 성장은 표면적인 수치가 나타내는 것보다 더 불균일한 양상을 보이고 있습니다. 주요 터널식 시스템의 승인 이력 또한 시간이 지남에 따라 그 적용 범위를 확대해 왔습니다. 이는 적용 대상이 종양학을 넘어 특정 재발성 비악성 흉수증 사례까지 확대되었기 때문입니다.

기흉은 2031년까지 연평균 성장률(CAGR)이 5.27%로 전망되며, 가장 빠르게 성장하고 있는 적응증 부문이며, 이러한 급속한 성장의 주된 원인은 진료 지침의 변경에 있습니다. 유럽호흡기학회(ERS), 유럽심흉부외과학회(EACTS), 유럽흉부외과학회(EST)가 2024년에 발표한 공동 지침은 첫 발병 원발성 자연 기흉의 관리에 있어 최소 침습적 접근법을 권장하며, 적절한 환자의 경우 외래 치료를 조건부로 지지하고 있습니다(PUBMED). 이러한 변화는 일부 치료 경로에서 기존 방식인 대구경 카테터 삽입법보다 소구경 카테터의 사용을 권장한다는 점에서 중요합니다. 혈흉과 수술 후 배액술은 역학적 요인보다 외상이나 수술 건수와 더 밀접한 관련이 있기 때문에 여전히 확고한 수요 기반을 제공합니다. 농흉은 금액 기준으로는 여전히 규모가 작지만, 감염성 또는 합병증이 동반된 흉수 축적의 경우 보다 적극적인 치료 접근이 필요한 경우가 많기 때문에 미국 흉부 카테터 시장에서 대구경 배액관의 중요성은 여전히 유지되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the united states thoracic catheter market size is expected to increase from USD 153.87 million in 2025 to USD 159.78 million in 2026 and reach USD 196.46 million by 2031, growing at a CAGR of 4.22% over 2026-2031.

This report is Segmented by Product Type (Thoracostomy Tubes, Pleural Drainage Catheters, and More), Application (Pleural Effusion, and More), Procedure/Access Technique (Seldinger, Surgical, Trocar, Tunneled), Monitoring Modality (Conventional Analog, Digital Drainage), and End User (Hospitals, Ascs, Specialty Clinics, Homecare). The Market Forecasts are Provided in Terms of Value (USD).

United States Thoracic Catheter Market Trends and Insights

Rising Malignant and Recurrent Pleural Effusion Burden

Pleural effusion demand remains central to the US thoracic catheter market because malignant pleural effusion continues to create a large and recurring treatment need. Around 150,000 patients receive a malignant pleural effusion diagnosis each year in the United States, which keeps demand high for both inpatient drainage and longer-term outpatient management approaches. The case burden is also being reinforced by longer survival in cancer care, since patients are living longer with disease and therefore spend a longer period needing symptom control and repeat pleural management. Evidence from pleural care databases has also shown a rise in new malignant pleural effusion diagnoses over time, which supports the same direction of demand pressure described in the US thoracic catheter market. This longer care window increases catheter use per patient because repeat drainage episodes become more likely before pleurodesis or catheter removal can be achieved. As a result, recurrent effusion care is becoming one of the clearest volume drivers for tunneled pleural systems and related accessories in the US thoracic catheter market.

First-Line Guideline Acceptance of Indwelling Pleural Catheters

Guideline acceptance has become a direct growth lever for the US thoracic catheter market because indwelling pleural catheters are no longer treated only as a late fallback option. Guidance from the American Thoracic Society, the British Thoracic Society, and the European Respiratory Society now places indwelling pleural catheters alongside other frontline options for recurrent malignant pleural effusion management. In patients with non-expandable lung, the treatment preference is even clearer because guideline recommendations favor indwelling pleural catheters over talc pleurodesis in this setting. The current care gap also matters because only 24% of eligible United States patients receive guideline-consistent definitive management, which leaves a sizable conversion opportunity for programs that expand pleural intervention access. Clinical experience also supports the model, since one prospective cohort reported spontaneous pleurodesis in 44% of indwelling pleural catheter patients, with higher pleural fluid pH and protein associated with success. That combination of stronger guideline backing and underuse in practice gives the United States thoracic catheter market room to grow without depending entirely on new indications.

Budget Pressure and GPO-Led Commoditization

Budget pressure remains a real brake on the United States thoracic catheter market because hospitals continue to buy large volumes of standard drainage products through contracts that reward scale and low unit cost. This matters most for conventional thoracostomy tubes and basic drainage kits, where product differentiation is limited, and procurement teams focus heavily on price consistency across large systems. The effect is a split market where standard products face ongoing price compression, while digitally integrated systems and specialized indwelling pleural catheter platforms have a better chance of defending premium pricing if clinical value is clear. That gap slows adoption because hospital committees often want stronger operational and clinical justification before they add new systems to approved purchasing lists. It also changes supplier behavior, since manufacturers are pushed to package products into procedure-specific kits and monitoring platforms rather than compete only on the base catheter itself. The result is that the United States thoracic catheter market keeps growing, but innovation reaches price-sensitive providers more slowly than it reaches advanced thoracic centers.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Thoracic and Cardiothoracic Surgeries

- ERAS-Led Adoption of Digital Drainage Workflows

- Catheter Blockage, Infection, and Dislodgement Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pleural drainage catheters held 47.23% of the US thoracic catheter market size in 2025, which made them the largest product group in the product mix. This leadership reflects their role across both recurrent oncologic effusion management and short-duration drainage in urgent and planned hospital care. Tunneled indwelling pleural catheters continue to gain procedural weight as clinical guidance becomes more supportive and outpatient care pathways become more common. Non-tunneled pigtail catheters still hold an important high-volume role because they are widely used for diagnostic drainage, temporary pleural decompression, and selected pneumothorax cases. In the US thoracic catheter industry, this combination gives pleural drainage catheters both a broad volume base and a strong link to premiumization.

Thoracostomy tubes remain important in trauma, empyema, and postoperative care, but the direction of change is becoming clearer as smaller-bore options gain support in indications where pain reduction and mobility matter. The United States thoracic catheter market is seeing gradual substitution in selected settings because smaller catheters can deliver acceptable outcomes while reducing discomfort and simplifying removal after use. Trocar catheters are the fastest-growing product type, with a 5.46% CAGR through 2031, supported by emergency use cases where placement speed remains a practical advantage. Bundled procedure kits also matter in this segment because they reduce stock complexity for hospitals and help suppliers defend contract positions through convenience as well as price. Product development still moves carefully, since material changes such as movement from PVC to polyurethane or silicone can trigger new qualification work that slows mid-tier innovation cycles under device compliance standards.

Pleural effusion accounted for 36.83% of the US thoracic catheter market size in 2025, which kept it as the largest application category in the country. The size of this segment is tied closely to malignant pleural effusion volume, and that burden remains high with around 150,000 diagnoses each year in the United States. Within pleural effusion care, malignant and non-malignant cases follow different purchasing logic because malignant disease leans more heavily toward indwelling systems and home drainage accessories, while non-malignant fluid often still involves repeat aspiration or shorter-term catheter use. This makes application growth in the US thoracic catheter market more uneven than the headline number suggests, since some sub-indications support premium systems while others continue to favor standard products. The approval history of major tunneled systems has also widened addressable use over time by extending relevance beyond oncology into selected recurrent non-malignant effusion settings.

Pneumothorax is the fastest-growing application segment with a 5.27% CAGR through 2031, and guideline changes are a major reason for that faster rise. The 2024 joint guidance from the European Respiratory Society, the European Association for Cardio-Thoracic Surgery, and the European Society of Thoracic Surgeons supports less invasive approaches for initial primary spontaneous pneumothorax management and conditionally supports ambulatory care in suitable patients PUBMED. That shift is important because it favors small-bore catheter use over older large-bore insertion patterns in part of the treatment pathway. Hemothorax and postoperative drainage still provide a dependable base of demand because they are tied more to trauma and surgical procedure volume than to epidemiology. Empyema remains smaller in value terms, but it keeps large-bore drainage relevant in the US thoracic catheter market because infected or complex pleural collections often require a more aggressive management approach.

List of Companies Covered in this Report:

- AngioDynamics

- Argon Medical Devices

- B. Braun

- Beckton Dickinson

- Cardinal Health

- Centese, Inc.

- Cook Group

- Getinge

- ICU Medical

- Medela

- Mediplus Ltd.

- Medtronic

- Merit Medical Systems

- Polymedicure Limited

- Redax S.p.A.

- Rocket Medical plc

- Smiths Group

- Teleflex

- Utah Medical Products

- Vygon

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Malignant and Recurrent Pleural Effusion Burden

- 4.2.2 Growth In Thoracic and Cardiothoracic Surgeries

- 4.2.3 Shift Toward Minimally Invasive Small-Bore Drainage

- 4.2.4 First-Line Guideline Acceptance of Indwelling Pleural Catheters

- 4.2.5 ERAS-Led Adoption of Digital Drainage Workflows

- 4.2.6 Expansion of Outpatient and Home-Based Pleural Management

- 4.3 Market Restraints

- 4.3.1 Catheter Blockage, Infection, And Dislodgement Risk

- 4.3.2 Budget Pressure and GPO-Led Commoditization

- 4.3.3 Polymer Qualification and Supply Revalidation Bottlenecks

- 4.3.4 Training Variability in Placement and Drainage Protocols

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Thoracostomy Tubes

- 5.1.2 Pleural Drainage Catheters

- 5.1.2.1 Tunneled Indwelling Pleural Catheters

- 5.1.2.2 Non-tunneled Pigtail Pleural Catheters

- 5.1.3 Trocar Catheters

- 5.1.4 Thoracostomy Procedure Kits and Trays

- 5.2 By Application

- 5.2.1 Pleural Effusion

- 5.2.1.1 Malignant Pleural Effusion

- 5.2.1.2 Non-malignant Pleural Effusion

- 5.2.2 Pneumothorax

- 5.2.2.1 Spontaneous Pneumothorax

- 5.2.2.2 Iatrogenic Pneumothorax

- 5.2.2.3 Traumatic Pneumothorax

- 5.2.3 Hemothorax

- 5.2.4 Postoperative Chest Drainage

- 5.2.4.1 Thoracic Surgery

- 5.2.4.2 Cardiac Surgery

- 5.2.5 Empyema and Complicated Pleural Infection

- 5.2.1 Pleural Effusion

- 5.3 By Procedure / Access Technique

- 5.3.1 Seldinger-guided Small-bore Placement

- 5.3.2 Surgical Thoracostomy Placement

- 5.3.3 Trocar-assisted Placement

- 5.3.4 Tunneled Indwelling Placement

- 5.4 By Monitoring Modality

- 5.4.1 Conventional Analog and Water-seal Drainage

- 5.4.2 Digital Drainage-compatible Solutions

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.1.1 Academic Medical Centers

- 5.5.1.2 Community Hospitals

- 5.5.1.3 Trauma Centers

- 5.5.2 Ambulatory Surgical Centers

- 5.5.3 Specialty Clinics

- 5.5.3.1 Interventional Pulmonology Clinics

- 5.5.3.2 Oncology and Palliative Care Clinics

- 5.5.4 Homecare Settings

- 5.5.1 Hospitals

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AngioDynamics, Inc.

- 6.3.2 Argon Medical Devices, Inc.

- 6.3.3 B. Braun Melsungen AG

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 Cardinal Health, Inc.

- 6.3.6 Centese, Inc.

- 6.3.7 Cook Medical

- 6.3.8 Getinge AB

- 6.3.9 ICU Medical, Inc.

- 6.3.10 Medela AG

- 6.3.11 Mediplus Ltd.

- 6.3.12 Medtronic plc

- 6.3.13 Merit Medical Systems, Inc.

- 6.3.14 Polymedicure Limited

- 6.3.15 Redax S.p.A.

- 6.3.16 Rocket Medical plc

- 6.3.17 Smiths Medical

- 6.3.18 Teleflex Incorporated

- 6.3.19 Utah Medical Products, Inc.

- 6.3.20 Vygon SA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment