|

시장보고서

상품코드

2064502

미국 경장 영양 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)United States Enteral Nutrition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

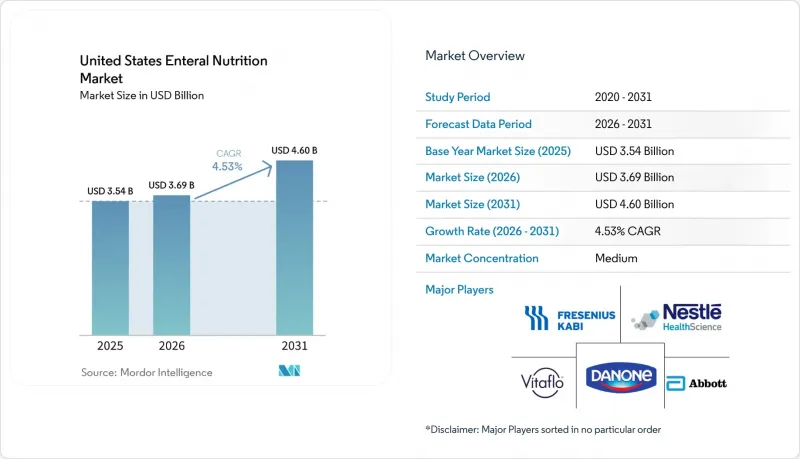

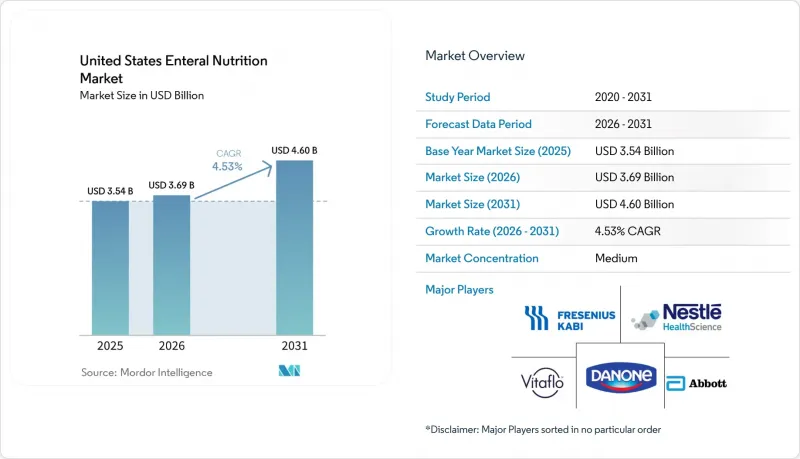

Mordor Intelligence에 의하면, 미국의 경장 영양 시장 규모는 2025년에 35억 4,000만 달러로 평가되었고, 2026년 36억 9,000만 달러로 추정되고, 2031년까지 46억 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.53%를 나타낼 전망입니다.

본 보고서는 급식 방법별(관영양, 경구영양), 제형 유형별(폴리머계, 펩타이드계, 필수 영양소, 질환 특이적), 형태별(액체, 분말), 연령대별(성인, 소아), 적응증별(소화기, 종양, 신경 질환, 당뇨병, 만성 신장 질환, 알레르기, 대사성 질환), 최종 사용자별(병원, 재택치료, 장기 요양 시설, 전문 클리닉), 지역별(미국)로 분류되어 있습니다. 시장 예상치는 금액(달러)으로 표시되어 있습니다.

미국의 경장 영양 시장 동향 및 인사이트

노화에 따른 연하 장애와 만성 질환의 부담

미국의 인구 고령화는 2020년대 말까지 미국 경장 영양 시장에서 지속적인 수요의 기반을 계속 형성하고 있습니다. 이러한 수요는 단순히 연령에 의해서만 주도되는 것은 아닙니다. 삼킴 장애는 치매, 뇌졸중, 파킨슨병, 만성 신장병, 두경부암 등과 동반되는 경우가 많아, 이로 인해 치료의 복잡성이 증가하고 영양제 사용량이 늘어나기 때문입니다. 미국 인구조사국의 예측에 따르면, 2030년까지 7,300만 명의 미국인이 65세 이상이 될 것으로 예상되며, 이로 인해 경구용 증점제, 특수 경장 영양제 또는 경관 영양 요법이 필요한 환자층이 크게 확대될 것으로 보입니다. 따라서 미국의 경장 영양 시장은 환자 수 증가뿐만 아니라, 신장 질환, 종양학, 신경학 분야 수요로 인해 수요가 보다 전문적인 제품으로 이동하는 등, 더욱 다양한 증례 구성의 이점도 누리고 있습니다. 이러한 경향은 표준 제품군이 여전히 큰 시장 점유율을 차지하고 있음에도 불구하고, 질환 특이적 제형이 범용 폴리머 제품보다 더 빠르게 성장하고 있는 이유를 설명하는 한 가지 요인이 되고 있습니다.

급성기 이후 단계에서의 재택 장내 영양 관리 확대

병원들이 비용 효율적인 회복 경로와 입원 기간 단축을 모색하는 가운데, 미국의 경장 영양 시장의 중심은 입원 환자 중심에서 재택 중심으로 이동하고 있습니다. 해당 장내영양 제품 및 소모품에 대한 CMS(미국 의료보험 및 의료보조 서비스 센터)의 환급 코드는 의료 제공업체에게 체계적인 지급 경로를 제시하며, 이를 통해 퇴원 후 재택 장내영양 관리가 용이해지고 있습니다. 메디케어 어드밴티지의 확대에 따라 플랜 차원의 처방전 선정 기준도 더욱 엄격해지고 있으며, 우선 공급업체 지위를 획득한 기업은 퇴원 후 네트워크 전반에 걸쳐 지속적인 유통상의 우위를 확보할 수 있습니다. 휴대용 펌프 기술과 ENFit 호환 시스템의 지속적인 도입으로 인해, 병원 내 투여와 재택 투여 간의 사용 편의성 격차가 줄어들면서, 환자가 재택 치료를 시작할 때의 장벽이 낮아지고 있습니다. 재택 간호 채널이 확대됨에 따라, 간병인의 업무 부담을 줄여주는 ‘매달아 사용할 수 있는 액상 제제’나 ‘폐쇄형 시스템’에 대한 지출도 늘어나고 있습니다.

재택 장내 영양 공급에 대한 보험 급여 및 문서 작성상의 장애물

상환 문제는 여전히 미국 경장 영양 시장에서 가장 중요한 구조적 제약 요인으로 남아 있습니다. 왜냐하면 행정상의 마찰이 재택 환자에 대한 서비스 제공에 대한 공급자의 의욕에 직접적인 영향을 미치기 때문입니다. CMS는 2024년 규정 준수 심사에서 경장 영양 공급업체의 부적정 지급률을 23.8%로 보고했으며, 불충분한 문서화가 불승인 사례의 48.8%를 차지했습니다. 이는 임상적 필요성이 실제로 존재하는 경우라 하더라도, 얼마나 많은 수익이 손실될 가능성이 있는지를 보여줍니다. CMS의 LCD L38955에서는 의료적 필요성을 입증할 수 있는 상세하고 최신의 증거를 요구하고 있으며, 전담 규정 준수 팀을 갖추지 못한 소규모 재택 간호 사업자에게는 그 부담이 더욱 무겁게 다가옵니다. 이러한 비용이 상승함에 따라 독립 판매업체들은 이익률 압박에 직면하고 있으며, 일부는 이 분야에서 철수하고 있습니다. 그 결과, 환자 수요는 늘어나고 있는 반면, 공급 기반은 점차 축소되고 있습니다. 그 결과, 미국의 경장 영양 시장에서는 뚜렷한 불일치가 발생하고 있습니다. 왜냐하면, 대상 환자층이 확대되고 있음에도 불구하고, 여전히 규모와 관리 체제의 확충을 중시하는 보험 지급 경로를 통해 서비스가 제공되고 있기 때문입니다.

부문별 분석

2025년 기준으로, 경관영양 제품은 미국 경장 영양 시장 점유율의 64.57%를 차지했으며, 이는 급성기 의료 및 시설 내 환경에서 경관영양을 통한 투여가 여전히 수요의 기반을 이루고 있음을 뒷받침합니다. 이러한 상황은 중환자실, 신경과, 종양학과 및 수술 후 회복기 환자들 중 경구 섭취가 불가능하거나 영양 상태를 유지하기에 불충분한 경우가 많아, 경관 영양 공급이 지속적으로 이루어지고 있음을 반영하고 있습니다. 미국의 장내 영양 시장은 여전히 비강 위관, 비강 십이지장관 및 PEG(경피적 위루)를 이용한 투여 방식에 의존하고 있습니다. 이는 흡인 위험, 연하 장애 또는 심각한 쇠약으로 인해 경구 섭취가 제한되는 경우, 이러한 방법들이 여전히 표준 치료법이기 때문입니다. 또한, 병원이나 장기 요양 서비스 제공업체들은 중증 환자에게 예측 가능한 양의 칼로리와 단백질을 공급할 수 있다는 점에서 경관영양을 중시하고 있습니다.

그러나 경장 영양 제품은 2031년까지 연평균 성장률(CAGR) 5.46%를 나타낼 것으로 예측되며, 이에 따라 이 부문은 미국 장내 영양 시장 전체에서 특히 높은 성장률을 보일 것으로 전망됩니다. 퇴원 후 영양 관리 지침에 따르면, 급성기 치료를 마친 환자, 특히 완전한 경관 영양 의존 상태에서 부분적 또는 완전한 경장 영양으로 전환이 가능한 환자의 경우, 경장 영양 보충제가 더 많이 사용되고 있습니다. 또한, 매니지드 케어 모델 역시 조기 퇴원을 촉진하고 있으며, 장기간 입원 중의 경관 영양 공급보다는 지역사회에서의 회복에 더 적합한 휴대용 소량 음용형 제품이 선호되고 있습니다. 이는 경관 영양 제품의 임상적 중요성을 약화시키는 것은 아니지만, 환자의 회복 과정이 병원 밖으로 옮겨감에 따라 추가적인 수요가 경장 영양 보충제로 이동하고 있음을 보여줍니다. 그 결과, 경관 영양은 안정적인 기반을 유지하는 한편, 경구용 제품은 더욱 급속한 성장을 이루고 있으며, 이는 시설 돌봄에서 재택 및 외래 지원으로의 광범위한 채널 전환을 반영하고 있습니다.

2025년 기준으로 표준 및 폴리머 제제는 미국 경장 영양 시장 규모의 56.81%를 차지했으나, 질환 특이적 제제는 2031년까지 연평균 성장률(CAGR) 5.27%로 확대될 것으로 예측됩니다. 폴리머 제제는 연령대, 적응증, 치료 환경에 관계없이 폭넓게 적용할 수 있으며, 많은 병원의 처방 목록에서 여전히 비용 대비 효과가 높은 주력 제품으로 자리 잡고 있어 여전히 시장을 독점하고 있습니다. 미국의 장내 영양 시장이 이처럼 대규모의 고분자 제제 기반을 유지하고 있는 이유는 고도로 전문화된 조성이 요구되지 않는 다양한 환자 집단에서 표준 제제를 도입하기가 더 쉽기 때문입니다. 이러한 폭넓은 역할 덕분에, 새로운 카테고리가 점진적으로 시장 점유율을 확대해 가는 상황 속에서도 판매량 측면에서 주도적인 위치를 유지하고 있습니다.

당뇨병, 신장 질환, 종양학 및 소화기 질환 관리 분야에서 특정 대사적 또는 장기 관련 요구 사항에 맞추어 설계된 영양 프로파일에 대한 수요가 증가함에 따라, 질환별 맞춤형 포뮬러의 입지가 확대되고 있습니다. 프레제니우스 카비가 2026년에 ‘Renalive HP’를 출시한 것은 이 공급업체가 경쟁사의 제품 라인업 축소로 인해 발생한 임상적 공백을 공략하며 신장 특화 영양 분야로의 진출을 더욱 확대하고 있음을 보여줍니다. 펩타이드 기반 및 세미엘레멘탈 제제는 소화 및 흡수 기능에 장애가 있는 환자에게 여전히 필수적이지만, 엘레멘탈 제제나 아미노산 기반 제품은 호산구성 위장 장애나 선천성 대사 이상증 등 가장 복잡한 증례에 대응하고 있습니다. 2025년 『Nutrients』지에 게재된 리뷰 역시 소아 호산구 식도염 및 관련 식품 단백질 매개 질환에서 아미노산 기반 분유의 역할 확대를 뒷받침하고 있으며, 이에 따라 주 메디케이드 프로그램에서 이러한 제품에 대한 보험 적용 근거가 강화되고 있습니다. 따라서 미국의 경장 영양 업계는 규모 면에서는 폴리머 계열의 조제식에 계속 의존하고 있는 반면, 고부가가치의 성장 분야는 전문 제품이 주도하고 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the united states enteral nutrition market size was valued at USD 3.54 billion in 2025 and is estimated to grow from USD 3.69 billion in 2026 to reach USD 4.60 billion by 2031, at a CAGR of 4.53% during the forecast period (2026-2031).

This report is Segmented by Feeding Method (Tube Feeding, Oral Feeding), Formula Type (Polymeric, Peptide-Based, Elemental, Disease-Specific), Form (Liquid, Powder), Age Group (Adults, Pediatrics), Indication (GI, Oncology, Neurology, Diabetes, CKD, Allergy, IEM), End User (Hospitals, Homecare, Long-Term Care, Specialty Clinics), and Geography (United States). Forecasts are in Value (USD).

United States Enteral Nutrition Market Trends and Insights

Aging-Related Dysphagia and Chronic Disease Burden

The aging of the U.S. population continues to create a durable demand floor for the United States enteral nutrition market through the end of the decade. This demand is not driven by age alone, because dysphagia often overlaps with dementia, stroke, Parkinson's disease, chronic kidney disease, and head and neck cancer, which raises both treatment complexity and formula intensity. The U.S. Census Bureau projects that 73 million Americans will be age 65 or older by 2030, and that scale materially enlarges the patient base that can require oral thickened support, specialized oral nutrition, or tube feeding therapy. The United States enteral nutrition market, therefore, benefits not only from higher patient numbers but also from a richer case mix where renal, oncology, and neurologic needs push demand toward more specialized products. That pattern helps explain why disease-specific formulas are expanding faster than broad polymeric products even while the standard base remains large.

Home-Enteral Care Expansion Across Post-Acute Pathways

The center of gravity in the United States enteral nutrition market is moving from inpatient use toward the home as hospitals seek lower-cost recovery pathways and shorter lengths of stay. CMS reimbursement codes for eligible enteral products and supplies give providers a structured payment route, which makes home enteral nutrition easier to operationalize after discharge. Medicare Advantage growth is also raising plan-level formulary gatekeeping, so companies that win preferred supplier status can secure lasting distribution advantages across discharge networks. Portable pump technology and continued ENFit-compatible system adoption have narrowed the usability gap between hospital delivery and home administration, which lowers the barrier to starting patients on home regimens. As the homecare channel expands, spending also shifts toward ready-to-hang liquids and closed systems that reduce the handling burden for caregivers.

Reimbursement and Documentation Barriers for Home Enteral Nutrition

Reimbursement remains the most important structural constraint on the United States enteral nutrition market because administrative friction directly affects supplier willingness to serve home patients. CMS reported a 23.8% improper payment rate for enteral nutrition suppliers in its 2024 compliance review, and insufficient documentation accounted for 48.8% of denials, which shows how much revenue can be exposed even when clinical need is real. CMS LCD L38955 requires detailed and current proof of medical necessity, and that burden is harder for smaller homecare providers to manage without dedicated compliance teams. As those costs rise, independent distributors face tighter margins, and some exit the space, which narrows the supply base even as patient need grows. The result is a clear mismatch in the United States enteral nutrition market, because a broader eligible population is being served through a reimbursement channel that still favors scale and administrative depth.

Other drivers and restraints analyzed in the detailed report include:

- Disease-Specific Formula Adoption in Diabetes, Renal, and GI Care

- Real-Food and Blenderized Tube-Feeding Innovation

- High Affordability Pressure on Specialized Formulas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tube Feeding Products accounted for 64.57% of the United States enteral nutrition market share in 2025, which confirms that tube-based delivery still anchors demand across acute care and institutional settings. This position reflects persistent use in intensive care, neurology, oncology, and post-surgical recovery, where the oral route is often unavailable or insufficient for maintaining nutritional status. The United States enteral nutrition market still depends on nasogastric, nasoduodenal, and PEG-based regimens because they remain the standard of care when aspiration risk, swallowing impairment, or severe weakness limit oral intake. Hospitals and long-term care providers also value tube feeding because it provides predictable calorie and protein delivery in high-acuity patients.

Oral Feeding Products, however, are projected to grow at a 5.46% CAGR through 2031, which gives this segment the growth premium within the broader United States enteral nutrition market. Post-discharge nutrition protocols are using more oral nutritional supplements for patients leaving acute care, especially when they can transition from full tube dependence to partial or complete oral support. Managed care models are also encouraging earlier discharge, and that favors portable sip-feed formats that fit community recovery better than prolonged inpatient tube feeding. This does not weaken the clinical importance of tube products, but it does shift incremental demand toward oral supplementation as patient recovery moves outside the hospital. The result is a stable base in tube feeding and a faster expansion path for oral products, which mirrors the broader channel shift from institutional care to home and outpatient support.

Standard/Polymeric Formulas accounted for 56.81% of the United States enteral nutrition market size in 2025, while Disease-Specific Formulas are projected to expand at a 5.27% CAGR through 2031. Polymeric products still dominate because they are broadly applicable across age groups, indications, and care settings, and they remain the cost-effective workhorse of many hospital formularies. The United States enteral nutrition market retains this large polymeric base because standard formulas are easier to deploy across mixed patient populations where highly specialized composition is not required. That broad role helps preserve volume leadership even as newer categories take a larger share of incremental growth.

Disease-specific formulas are gaining ground because diabetes, renal disease, oncology, and gastrointestinal care increasingly demand nutrition profiles designed for defined metabolic or organ-related needs. Fresenius Kabi's 2026 launch of Renalive HP shows how suppliers are targeting clinical gaps left by competitor portfolio reductions and pushing deeper into renal-specific nutrition. Peptide-based and semi-elemental formulas remain essential for patients with impaired digestion or absorption, while elemental and amino acid-based products serve the highest-complexity cases such as eosinophilic gastrointestinal disorders and inborn errors of metabolism. A 2025 review in Nutrients also supported the expanding role of amino acid-based formulas in pediatric eosinophilic esophagitis and related food protein-mediated disorders, which strengthens the reimbursement case for these products in state Medicaid programs. The United States enteral nutrition industry, therefore, continues to rely on polymeric formulas for scale, while specialized products carry the higher-value growth layer.

List of Companies Covered in this Report:

- Abbott Laboratories

- Ajinomoto Cambrooke

- B. Braun

- Cardinal Health

- Danone

- Fresenius

- Functional Formularies

- Global Health Products

- Hormel Health Labs / Lyons Health Labs

- Kate Farms

- Kent Precision Foods Group (Thick-It)

- Medline Industries

- Medtrition

- Moog Medical

- Nestle Health Science

- Real Food Blends

- Reckitt / Mead Johnson Nutrition

- SimplyThick

- Solace Nutrition

- Vitaflo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging-Related Dysphagia and Chronic Disease Burden

- 4.2.2 Home-Enteral Care Expansion Across Post-Acute Pathways

- 4.2.3 Disease-Specific Formula Adoption in Diabetes, Renal, And GI Care

- 4.2.4 Real-Food and Blenderized Tube-Feeding Innovation

- 4.2.5 Enfit-Compatible Convenience Formats Improving Home Adherence

- 4.2.6 Pediatric Elemental and Metabolic Nutrition Demand Expansion

- 4.3 Market Restraints

- 4.3.1 Reimbursement and Documentation Barriers for Home Enteral Nutrition

- 4.3.2 High Affordability Pressure on Specialized Formulas

- 4.3.3 Supplier Attrition and Access Gaps in HEN Distribution

- 4.3.4 Product Shortages and SKU Discontinuations in Critical Formulas

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Feeding Method

- 5.1.1 Tube Feeding Products

- 5.1.2 Oral Feeding Products

- 5.2 By Formula Type

- 5.2.1 Standard / Polymeric Formulas

- 5.2.2 Peptide-Based / Semi-Elemental Formulas

- 5.2.3 Elemental / Amino Acid-Based Formulas

- 5.2.4 Disease-Specific Formulas

- 5.3 By Form

- 5.3.1 Liquid

- 5.3.2 Powder

- 5.4 By Age Group

- 5.4.1 Adults

- 5.4.1.1 Adult 18-64

- 5.4.1.2 Geriatric 65+

- 5.4.2 Pediatrics

- 5.4.2.1 Infants

- 5.4.2.2 Children

- 5.4.2.3 Adolescents

- 5.4.1 Adults

- 5.5 By Indication

- 5.5.1 Gastrointestinal Disorders and Malabsorption

- 5.5.1.1 Short Bowel Syndrome

- 5.5.1.2 Inflammatory Bowel Disease

- 5.5.1.3 Severe Malabsorption / Diarrhea

- 5.5.2 Oncology

- 5.5.3 Neurology

- 5.5.3.1 Stroke Recovery

- 5.5.3.2 Dementia / Alzheimer's Disease

- 5.5.3.3 Cerebral Palsy and Neurodevelopmental Disorders

- 5.5.4 Diabetes

- 5.5.5 Chronic Kidney Disease

- 5.5.6 Food Allergy and Eosinophilic GI Disorders

- 5.5.7 Inborn Errors of Metabolism / Ketogenic Therapy

- 5.5.8 General Malnutrition / Surgical Recovery / Critical Care

- 5.5.1 Gastrointestinal Disorders and Malabsorption

- 5.6 By End User

- 5.6.1 Hospitals

- 5.6.1.1 ICU / Critical Care

- 5.6.1.2 Med-Surg / Oncology Units

- 5.6.1.3 Neonatal / Pediatric Units

- 5.6.2 Homecare Settings

- 5.6.3 Long-term Care Centers / Skilled Nursing Facilities

- 5.6.4 Specialty Clinics / Outpatient Care

- 5.6.1 Hospitals

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott Nutrition

- 6.3.2 Ajinomoto Cambrooke

- 6.3.3 B. Braun Medical

- 6.3.4 Cardinal Health

- 6.3.5 Danone

- 6.3.6 Fresenius Kabi USA

- 6.3.7 Functional Formularies

- 6.3.8 Global Health Products

- 6.3.9 Hormel Health Labs / Lyons Health Labs

- 6.3.10 Kate Farms

- 6.3.11 Kent Precision Foods Group (Thick-It)

- 6.3.12 Medline Industries

- 6.3.13 Medtrition

- 6.3.14 Moog Medical

- 6.3.15 Nestle Health Science

- 6.3.16 Real Food Blends

- 6.3.17 Reckitt / Mead Johnson Nutrition

- 6.3.18 SimplyThick

- 6.3.19 Solace Nutrition

- 6.3.20 Vitaflo

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment