|

시장보고서

상품코드

2064504

미국의 외래 진료 서비스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Ambulatory Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

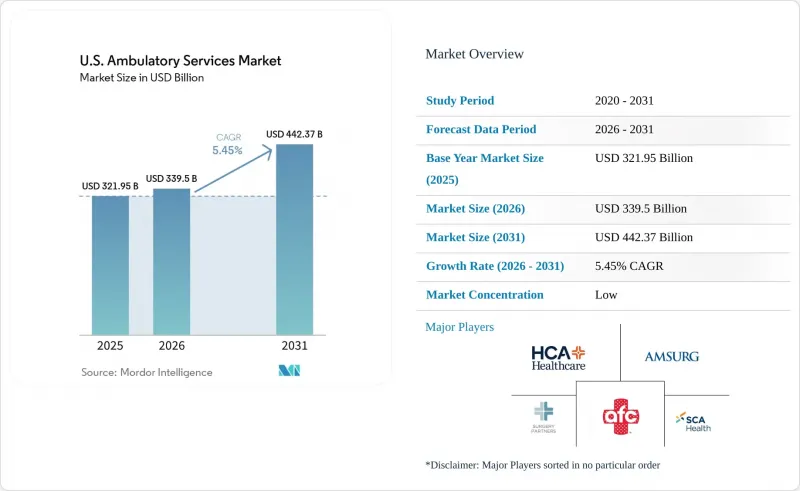

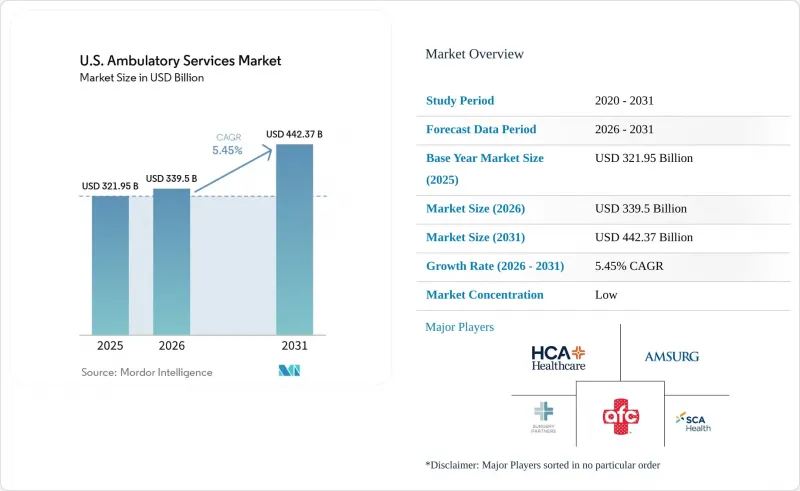

Mordor Intelligence에 의하면, 미국의 외래 진료 서비스 시장 규모는 2025년 3,219억 5,000만 달러로 평가되었습니다. 2026년에는 3,395억 달러로 확대되어 2026-2031년 CAGR은 5.45%를 나타내, 2031년까지 4,423억 7,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 의료 제공 환경(1차 진료 클리닉, 외과 전문 클리닉 등), 서비스 유형(진단, 경과 관찰·상담 등), 전문 분야(1차 진료, 정형외과, 안과, 소화기내과, 순환기내과 등), 그리고 소유 형태(의사 소유 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 외래 진료 서비스 시장 동향 및 인사이트

입원에서 외래로 진료 장소 변경

입원에서 외래로 치료 장소가 전환됨에 따라, 미국의 외래 진료 서비스 시장의 환자 수 증가세가 계속해서 이어지고 있습니다. 2026년, CMS는 ‘입원 한정 목록’에서 285건의 근골격계 시술을 삭제하고, 심장 전기생리학적 절제술 및 후방 요추 체간 고정술을 포함한 573건의 새로운 코드를 ASC 대상 시술 목록에 추가했습니다. 이러한 변경으로 인해, 기존에는 병원으로 한정되었던 시술이 외래 시설로 이전될 수 있게 되었으며, 시술의 다양화가 진행되면서 외래 진료 사업자의 비즈니스 기회가 확대되고 있습니다. 또한, 민간 메디케어 어드밴티지 플랜은 기존의 메디케어 진료 장소 패턴을 따르는 경우가 많기 때문에 지급 채널 전반에 걸쳐 CMS의 정책 변경이 미치는 영향이 확대되고 있으며, 이러한 추세가 시장의 주요 성장 요인으로 자리 잡고 있습니다.

고령화와 만성 질환의 부담

인구 동향에 따라 미국의 외래 환자 서비스 시장에는 지속적인 수요가 발생하고 있습니다. 메디케어 지출은 고령화의 영향을 반영하여 2033년까지 연평균 7.8%씩 증가할 것으로 예측됩니다. 2050년까지 50세 이상 성인 1억 4,270만 명이 적어도 한 가지 이상의 만성 질환을 앓게 될 것으로 예상되며, 이는 심혈관 질환 관리, 신장내과, 종양학 분야의 정맥 주사 요법 및 행동 의학 분야의 외래 서비스 수요를 견인할 것으로 보입니다. 특히 외래 암 치료는 매우 중요하며, 향후 10년 동안 2억 2,200만 건에 달할 것으로 예측됩니다. 이러한 추세로 인해 시장의 성장은 단기적인 경제 변동이 아닌, 장기적인 국민의 건강 수요에 힘입고 있습니다.

규제의 복잡성, 상환액의 변동, 그리고 시설 중립적인 지급에 대한 압력

미국의 외부 서비스 시장에 대한 규제 체계는 여전히 복잡하고 비용이 많이 듭니다. 사업자는 연방 정부의 지급 방침, 주 정부의 ‘필요성 증명서(Certificate of Need)’ 규정, 민간 보험사의 인증 요건 및 HIPAA(의료보험 이동성 및 책임에 관한 법률) 준수를 동시에 이행해야 합니다. 2026 회계연도 OPPS/ASC 최종 규정은 특정 병원 외래 진료 부문의 약물 투여 서비스에 대해 시설 중립형 지불 방식을 확대하는 것으로, 2026년에는 메디케어 OPPS 지출을 2억 9,000만 달러 절감할 것으로 예측됩니다. CMS는 또한 2026년에도 340B 구제 조치의 상쇄를 유지할 것이며, 2027년에는 전환 계수를 추가로 인하할 것을 시사하고 있어, 병원의 외래 진료 운영에 더 큰 재정적 부담을 주고 있습니다. 이러한 규제 변경은 소규모 사업자들에게 수익 계획의 불확실성을 초래하며, 신중한 자본 배분과 미국 해외 의료 서비스 시장 전반에 걸친 불균일한 사업 환경으로 이어지고 있습니다.

부문별 분석

2025년, 1차 진료 클리닉은 수익 점유율의 38.75%를 차지하며 미국의 외래 진료 서비스 시장에서 주도적인 위치를 유지했습니다. 이러한 우위는 정기적인 진찰, 만성 질환 관리, 의뢰 및 사후 관리에 있어 주요 접근 지점으로서의 역할을 부각시키고 있습니다. 그러나 보다 고도의 진료와 시술 빈도가 높은 환경으로의 전환이 진행되는 가운데, 기존의 클리닉은 업무 흐름의 효율화와 환자 유지율 향상을 꾀해야 하는 상황에 놓여 있습니다.

원격의료 및 가상 클리닉 시장은 2031년까지 연평균 성장률(CAGR) 7.23%를 기록하며 성장할 것으로 예상되며, 미국의 외래 진료 서비스 시장에서 가장 빠르게 성장하는 부문이 될 전망입니다. 이러한 성장은 2027년 12월까지 연장된 메디케어 원격의료에 관한 유연한 조치와, 행동 의학 및 후속 진료에 원격의료가 점차 통합되고 있는 데 기인합니다. 2025년 12월까지 정신건강 분야의 원격의료는 전문 진료의 28.2%를 차지하며, 원격 진료 모델의 급속한 확산을 반영하고 있습니다.

2025년에는 치료 서비스가 매출의 42.75%를 차지하며, 미국 해외 의료 서비스 시장에서 가장 큰 부문이 되었습니다. 이는 일반적인 진찰에 비해 시술에 대한 보험 지급률이 높다는 점을 반영한 것입니다. 외래수술센터(ASC)의 2024년 EBITDA 마진은 24.1%를 기록했으며, 2029년까지 소폭 하락할 것으로 전망됩니다. 더 많은 치료가 병원에서 외래 시설로 전환됨에 따라, 치료 중심의 시설이 우위를 유지할 것으로 예측됩니다.

진단 분야는 2026년부터 2031년까지 연평균 성장률(CAGR) 6.90%를 기록하며 성장할 것으로 예상되며, 미국의 외래 진료 서비스 시장에서 가장 빠르게 성장하는 부문이 될 전망입니다. 디지털 헬스 분야의 연간 경상이익은 2025년 3월부터 2026년 3월 사이에 9,690만 달러로 거의 두 배로 증가했으며, 이는 진단 플랫폼이 소프트웨어 기반의 수익원을 창출하는 데 있어 그 역할이 확대되고 있음을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the u.S. ambulatory services market size is expected to grow from USD 321.95 billion in 2025 to USD 339.5 billion in 2026 and is forecast to reach USD 442.37 billion by 2031 at 5.45% CAGR over 2026-2031.

This report is Segmented by Care Setting (Primary Care Clinics, Surgical Specialty Clinics, and More), Service Type (Diagnosis, Observation and Consultation, and More), Specialty (Primary Care, Orthopedics, Ophthalmology, Gastroenterology, Cardiovascular, and More), and Ownership Model (Physician-Owned, and More). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Ambulatory Services Market Trends and Insights

Inpatient-To-Outpatient Site-Of-Care Migration

The migration from inpatient to outpatient settings continues to drive volume growth in the United States ambulatory services market. In 2026, CMS removed 285 musculoskeletal procedures from the Inpatient-Only list and added 573 new codes to the ASC Covered Procedures List, including cardiac electrophysiology ablations and posterior lumbar interbody fusion. This change enables procedures previously confined to hospitals to transition to outpatient settings, expanding the procedure mix and increasing opportunities for ambulatory operators. Additionally, commercial Medicare Advantage plans often align with traditional Medicare site-of-service patterns, amplifying the impact of CMS policy changes across payer channels and solidifying this trend as a key growth driver for the market.

Aging Population And Chronic Disease Burden

Demographic trends are creating sustained demand for the United States ambulatory services market. Medicare spending is projected to grow at 7.8% annually through 2033, reflecting the impact of an aging population. By 2050, 142.7 million adults aged 50 and older are expected to have at least one chronic condition, driving demand for outpatient services in cardiovascular management, nephrology, oncology infusion, and behavioral health. Outpatient cancer care is particularly significant, with projected volumes reaching 222 million encounters over the next decade. These trends anchor the market's growth to long-term population health needs rather than short-term economic fluctuations.

Regulatory Complexity, Reimbursement Variability, And Site-Neutral Payment Pressure

The regulatory framework of the United States ambulatory services market remains intricate and costly. Operators must address federal payment policies, state Certificate of Need rules, private payer credentialing, and HIPAA compliance simultaneously. The CY 2026 OPPS/ASC Final Rule, extending site-neutral payment to drug administration services in certain off-campus hospital outpatient departments, is expected to reduce Medicare OPPS spending by USD 290 million in 2026. CMS has also retained the 340B remedy offset for 2026 and indicated a larger conversion factor reduction in 2027, adding financial strain on outpatient hospital operations. These regulatory shifts create revenue planning uncertainties for smaller operators, leading to cautious capital allocation and an uneven operating environment across the United States ambulatory services market.

Other drivers and restraints analyzed in the detailed report include:

- Minimally Invasive And Digital Technologies Broaden Outpatient Access

- Value-Based Care, Covered-Procedure Expansion, And Virtual Supervision Flexibility

- Workforce Shortages, Burnout, And Revenue-Cycle Cybersecurity Fragility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Primary Care Clinics held a 38.75% revenue share, maintaining their leadership in the United States ambulatory services market. This dominance highlights their role as the primary access point for routine evaluations, chronic disease management, referrals, and follow-up care. However, the shift toward higher acuity or procedural density settings is pressuring traditional clinics to enhance workflows and improve patient retention.

Telehealth and Virtual Clinics are projected to grow at a 7.23% CAGR through 2031, making them the fastest-growing segment in the United States ambulatory services market. Growth is driven by Medicare's telehealth flexibilities extended until December 2027 and the increasing integration of telehealth into behavioral health and follow-up consultations. By December 2025, mental health telehealth accounted for 28.2% of specialty encounters, reflecting the rapid adoption of off-site care models.

Treatment services accounted for 42.75% of revenue in 2025, making it the largest segment in the United States ambulatory services market. This reflects the higher reimbursement rates for procedures compared to routine consultations. Ambulatory surgery centers (ASCs) reported EBITDA margins of 24.1% in 2024, with only slight easing expected by 2029. As more procedures shift from hospitals to outpatient settings, treatment-heavy facilities are expected to maintain their lead.

Diagnosis is projected to grow at a 6.90% CAGR from 2026 to 2031, making it the fastest-growing segment in the United States ambulatory services market. Digital Health's annual recurring revenue nearly doubled to USD 96.9 million between March 2025 and March 2026, showcasing the growing role of diagnostic platforms in generating software-based revenue streams.

List of Companies Covered in this Report:

- American Family Care

- AMSURG

- CareNow

- CityMD

- Concentra

- CVS MinuteClinic

- DaVita Kidney Care

- Envision Healthcare

- Fast Pace Health

- Fresenius Kidney Care

- GoHealth Urgent Care

- HCA Healthcare Surgery Ventures

- Kaiser Permanente

- NextCare

- One Medical

- Physicians Endoscopy

- RadNet

- SCA Health

- Surgery Partners

- United Surgical Partners International

- WellNow Urgent Care

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Inpatient-to-Outpatient Site-of-Care Migration

- 4.2.2 Aging Population and Chronic Disease Burden

- 4.2.3 Minimally Invasive and Digital Technologies Broaden Outpatient Acuity

- 4.2.4 Value-Based Care and Payer Steerage to Lower-Cost Settings

- 4.2.5 2026 ASC Covered-Procedure Expansion and Inpatient-Only Phaseout

- 4.2.6 Permanent Virtual Supervision Expands Staffing Flexibility

- 4.3 Market Restraints

- 4.3.1 Regulatory Complexity and Reimbursement Variability

- 4.3.2 Workforce Shortages and Clinician Burnout

- 4.3.3 Clearinghouse and Cybersecurity Fragility in Revenue-Cycle Infrastructure

- 4.3.4 Site-Neutral Payment Expansion Pressures Hospital Outpatient Margins

- 4.4 Value/Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Care Setting

- 5.1.1 Primary Care Clinics

- 5.1.2 Surgical Specialty Clinics

- 5.1.3 Urgent Care Centers

- 5.1.4 Freestanding Emergency Departments

- 5.1.5 Diagnostic Imaging Centers

- 5.1.6 Specialty Clinics

- 5.1.7 Home Healthcare Agencies

- 5.1.8 Telehealth and Virtual Clinics

- 5.2 By Service Type

- 5.2.1 Diagnosis

- 5.2.2 Observation and Consultation

- 5.2.3 Treatment

- 5.2.4 Wellness and Preventive Care

- 5.2.5 Rehabilitation

- 5.3 By Specialty

- 5.3.1 Primary Care

- 5.3.2 Orthopedics

- 5.3.3 Ophthalmology

- 5.3.4 Gastroenterology

- 5.3.5 Cardiovascular

- 5.3.6 Pain Management

- 5.3.7 Nephrology and Dialysis

- 5.3.8 Dermatology

- 5.3.9 Oncology

- 5.3.10 Behavioral Health

- 5.3.11 Women's Health

- 5.3.12 Dental and Oral Surgery

- 5.4 By Ownership Model

- 5.4.1 Physician-Owned

- 5.4.2 Hospital or Health-System-Owned

- 5.4.3 Corporate or Private-Equity-Owned

- 5.4.4 Joint Ventures

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 American Family Care

- 6.3.2 AMSURG

- 6.3.3 CareNow

- 6.3.4 CityMD

- 6.3.5 Concentra

- 6.3.6 CVS MinuteClinic

- 6.3.7 DaVita Kidney Care

- 6.3.8 Envision Healthcare

- 6.3.9 Fast Pace Health

- 6.3.10 Fresenius Kidney Care

- 6.3.11 GoHealth Urgent Care

- 6.3.12 HCA Healthcare Surgery Ventures

- 6.3.13 Kaiser Permanente

- 6.3.14 NextCare

- 6.3.15 One Medical

- 6.3.16 Physicians Endoscopy

- 6.3.17 RadNet

- 6.3.18 SCA Health

- 6.3.19 Surgery Partners

- 6.3.20 United Surgical Partners International

- 6.3.21 WellNow Urgent Care

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment