|

시장보고서

상품코드

2064505

메르켈 세포암 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Merkel Cell Carcinoma - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

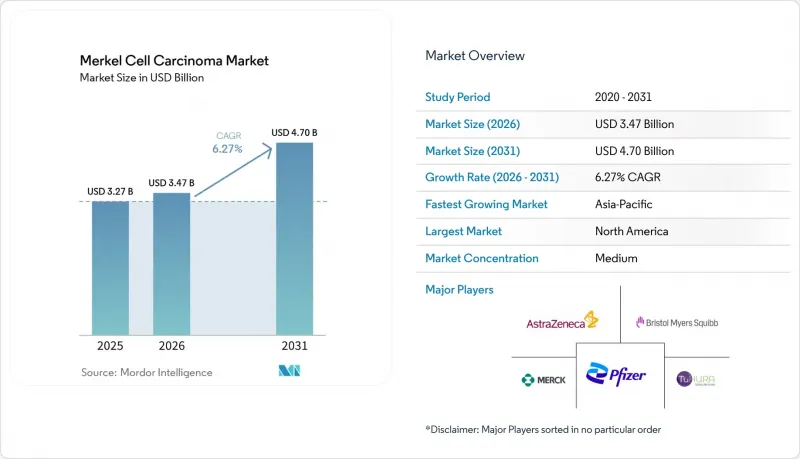

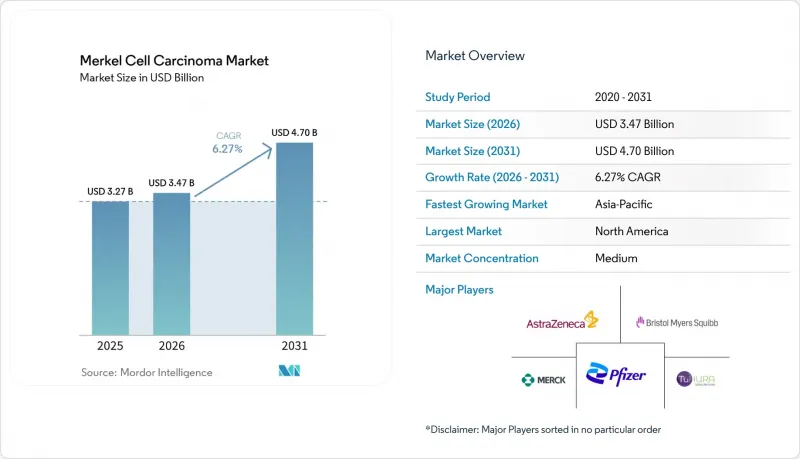

Mordor Intelligence에 의하면, 메르켈 세포암 시장 규모는 2025년에 32억 7,000만 달러로 평가되었습니다. 2026년 34억 7,000만 달러에서 2031년까지 47억 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 6.27%를 나타낼 전망입니다.

본 보고서는 질환의 병기(제1기, 제2기, 제3기), 모달리티(진단, 치료), 최종 사용자(대학 부속 암 센터, 병원 종양과, 외래 종양·정맥주사 센터, 검사 기관), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 메르켈 세포암 시장 동향 및 인사이트

고령화 및 면역억제 상태인 환자 수 증가

메르켈 세포암 시장은 특히 이 질환이 가장 많이 발생하는 고령층을 중심으로 환자 수 증가의 혜택을 보고 있습니다. 미국에서 1만 1,574건을 대상으로 한 연구에 따르면, 진단 당시의 중앙값은 77세로 보고되었으며, 2016년부터 2021년까지의 진단 사례에서 생존율이 개선된 것으로 나타나, 고령층에서의 검출 정확도가 향상되고 있음을 알 수 있습니다. 또한, 고형 장기 이식 수혜자의 위험이 23.8배, 치료받지 않은 HIV 양성자의 위험이 13.4배로 증가한 사실은 이 시장이 고위험 면역 억제 상태에 있는 집단에 의존하고 있음을 여실히 보여줍니다. 이러한 수요는 빈번한 모니터링과 전문적인 치료의 필요성에 힘입어 더욱 확대되고 있으며, 이 질환이 희귀병임에도 불구하고 시장의 지속적인 성장이 보장되고 있습니다.

치료 지침에 자리 잡은 체크포인트 억제제

체크포인트 억제제는 진행성 메르켈 세포암의 표준 치료법이 되었으며, 주요 보험 적용 환경에서 화학요법을 대체했습니다. NCCN 가이드라인에서는 절제 불가능하거나 전이성 사례에 대한 1차 치료제로 펨브롤리주맙, 아벨마브, 니볼마브, 레티판리맙이 제시되어 있습니다. 임상시험에 따르면, 펨브롤리주맙의 반응 지속 기간 중앙값은 39.8개월이며, 환자의 36%가 24개월 이상 반응을 유지하고 있습니다. 이 치료법으로의 전환을 통해 일관된 치료 패턴이 확립되었으며, 미국, 유럽 및 아시아태평양의 특정 지역에서 시장의 상업적 기반이 강화되고 있습니다.

극히 적은 대상 환자 수와 임상시험 피험자 모집의 병목 현상

메르켈 세포암 시장은 임상시험이나 전문 치료의 대상이 되는 환자 수가 제한적이라는 점에서 어려움을 겪고 있습니다. 2025년 미국의 역학 조사에 따르면, 2013년 이후의 평균 발생률은 10만 명년당 0.68이며, 그 결과 연간 환자 수는 지속적으로 낮은 수준을 유지하고 있습니다. 이로 인해 피험자 모집이 제한되고, 연구가 주요 암 센터에 집중되면서 일반적인 고형암에 비해 근거를 마련하기가 어려워지고 있습니다. TuHURA Biosciences사의 3상 IFx-2.0 임상시험은 미국 내 22-25곳의 시설에서 118명의 환자를 대상으로 진행되고 있는데, 이 사례는 소규모 임상시험이라 할지라도 막대한 인프라가 필요하다는 점을 여실히 보여주고 있습니다. 이러한 병목 현상은 파이프라인의 회전 속도를 늦추고, 혁신을 소수의 시설에 집중시킴으로써 중소기업의 사업 수행 위험을 높이고 있습니다.

부문별 분석

2025년 기준으로, 3기 메르켈세포암은 시장 규모의 44.45%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 7.28%를 나타낼 것으로 예측됩니다. 이로 인해 해당 부문은 가장 규모가 크고 가장 빠르게 성장하는 부문이 될 것입니다. 이 단계는 국소적 질환 관리와 전신 면역 요법을 연결하는 단계로, 임상적으로 림프절 전이가 확인된 환자나 병리학적으로 림프절 전이가 확인된 환자가 포함됩니다. NCCN 버전 2.2026에서는 임상적으로 림프절 전이가 없는 환자에 대한 센티넬 림프절 생검을 권장하고 있으며, 이를 통해 검출률이 향상되어 일부 사례가 3기로 분류되게 됩니다. 이러한 변화로 인해 전신 요법이 적용되는 단계에서 질환의 진단 정확도가 향상됩니다.

1기 및 2기는 나머지 병기 분류를 구성하며, 수익은 수술, 감시 림프절 생검, 방사선 치료 및 경과 관찰에 집중되어 있습니다. 이러한 병기는 보조 면역요법이 표준 치료법이 될 경우 그 가치가 높아질 가능성이 있습니다. 예측 기간 동안 결과가 기대되는 STAMP(펨브롤리주맙) 및 ADAM(아벨마브) 임상시험을 통해, 초기 병기 치료 시장의 수익이 방사선 단독 치료에서 체크포인트 억제제로 이동할 가능성이 있습니다.

지역별 분석

북미는 높은 치료 보급률, 첨단 전문 의료 인프라, 지침에 기반한 의료 서비스의 광범위한 시행에 힘입어 메르켈 세포암 시장을 독점하고 있습니다. 미국은 이 분야를 선도하고 있으며, 환자 수에 대한 가시성이 높고, 면역요법의 활용이 광범위하며, 희귀 피부암에 대한 확립된 의뢰 시스템을 갖추고 있습니다. NCCN 가이드라인은 절제 불가능하거나 전이성 질환에 대한 체크포인트 억제제 사용을 표준화하고 있으며, 2025년 개정판에서는 정기적인 추적 관찰 과정에서 분기별 ctDNA 모니터링의 중요성이 강조되었습니다. 이러한 치료 접근성과 철저한 모니터링이 맞물려, 북미는 시장에서 주도적인 입지를 확고히 다지고 있습니다.

유럽은 메르켈 세포암 시장에서 두 번째로 큰 규모를 자랑하며, 독일, 영국, 프랑스가 주요 수익원입니다. 이 지역은 전문 암 센터 및 피부과 센터에서 확립된 체크포인트 억제제 사용과 다학제적 협력을 통한 진료 경로의 혜택을 받고 있습니다. 독일 피부종양학 센터에서 제공한 실제 임상 등록 데이터는 이 희귀질환 분야의 임상적 근거를 강화하고 있습니다. 그러나 일부 시장에서 이루어지는 엄격한 상환 심사는 주요 의료 센터 이외의 곳에서의 도입을 제한하고, 생물학적 제제의 가격 결정력에 영향을 미칠 가능성이 있습니다.

아시아태평양은 메르켈 세포암 시장에서 가장 빠르게 성장하고 있는 지역이며, 일본, 중국, 호주가 다양한 수요 패턴을 통해 성장을 주도하고 있습니다. 일본에서는 치료 과정에서 체크포인트 억제제가 우선적으로 사용되며, 화학요법은 2차적인 선택지로 여겨지고 있습니다. 2025년에 일본에서 레티판리맙에 대한 규제 당국의 이해가 깊어질 것이라는 점은 희귀암에 대한 면역요법의 도입이 가속화될 가능성을 시사하고 있습니다. 북미나 유럽에 비해 현재 시장 규모는 작지만, 고령화의 진행과 도시 지역의 종양학 인프라 확충이 이 지역의 급속한 성장세를 더욱 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the merkel cell carcinoma market size was valued at USD 3.27 billion in 2025 and is estimated to grow from USD 3.47 billion in 2026 to reach USD 4.70 billion by 2031, at a CAGR of 6.27% during the forecast period (2026-2031).

This report is Segmented by Disease Stage (Stage I, Stage II, Stage III), Modality (Diagnosis, Treatment), End User (Academic Cancer Centers, Hospital Oncology Departments, Office-Based Oncology and Infusion Centers, Reference Laboratories), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Merkel Cell Carcinoma Market Trends and Insights

Rising Elderly and Immunosuppressed Patient Population

The Merkel cell carcinoma market benefits from a rising patient base, particularly among older demographics where the disease is most prevalent. A review of 11,574 cases in the United States reported a median diagnosis age of 77 years, with diagnoses from 2016 to 2021 linked to improved survival rates, indicating better detection in older groups. Additionally, a 23.8-fold increased risk in solid organ transplant recipients and a 13.4-fold risk in untreated HIV-positive individuals highlight the market's reliance on high-risk immunosuppressed populations. This demand is further driven by the need for frequent monitoring and specialist care, ensuring sustained market growth despite the disease's rarity.

Checkpoint Inhibitors Entrenched in Treatment Guidelines

Checkpoint inhibitors have become the standard treatment for advanced Merkel cell carcinoma, replacing chemotherapy in major reimbursement settings. NCCN guidelines list pembrolizumab, avelumab, nivolumab, and retifanlimab as first-line options for unresectable or metastatic cases. Clinical studies show a median response duration of 39.8 months for pembrolizumab, with 36% of patients maintaining responses beyond 24 months. This shift ensures consistent treatment patterns and strengthens the market's commercial foundation in the United States, Europe, and select Asia-Pacific regions.

Tiny Incident Population And Trial Recruitment Bottlenecks

The Merkel cell carcinoma market faces challenges due to a limited patient pool for trials and specialized treatments. A 2025 epidemiology review in the United States reported an average incidence rate of 0.68 per 100,000 person-years since 2013, resulting in consistently low annual case counts. This restricts recruitment, centralizes studies in major cancer centers, and complicates evidence generation compared to common solid tumors. TuHURA Biosciences' Phase 3 IFx-2.0 study, targeting 118 patients across 22 to 25 United States sites, highlights the significant infrastructure required for even modest trials. These bottlenecks delay pipeline turnover and concentrate innovation in a few centers, increasing execution risks for smaller companies.

Other drivers and restraints analyzed in the detailed report include:

- ctDNA-Guided Surveillance Expanding the Diagnostic Market

- Chemo-to-Immunotherapy Treatment Shift in Systemic Therapy

- High Biologic Cost And Reimbursement Scrutiny

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Stage III accounted for 44.45% of the Merkel cell carcinoma market size in 2025 and is projected to grow at a 7.28% CAGR through 2031, making it the largest and fastest-growing segment. This stage bridges local disease management and systemic immunotherapy, including patients with clinically positive nodes or nodal disease identified pathologically. NCCN Version 2.2026 recommends sentinel lymph node biopsy for clinically node-negative patients, improving detection and shifting some cases to Stage III. This shift enhances identification at a point where systemic therapy becomes relevant.

Stages I and II constitute the remaining disease-stage split, with revenue focused on surgery, sentinel node biopsy, radiation, and follow-up. These stages could gain value if adjuvant immunotherapy becomes routine. The STAMP pembrolizumab and ADAM avelumab trials, with results expected during the forecast period, may redirect early-stage revenue from radiation-only treatments to checkpoint inhibitors.

Geography Analysis

North America dominates the Merkel cell carcinoma market, driven by high treatment adoption, advanced specialist infrastructure, and widespread guideline-based care. The United States leads this region with greater case visibility, extensive immunotherapy use, and a well-established referral system for rare skin cancers. NCCN guidance has standardized checkpoint inhibitor use for unresectable or metastatic diseases, while the 2025 update emphasized quarterly ctDNA surveillance in routine follow-ups. This combination of treatment access and monitoring depth secures North America's leading position in the market.

Europe ranks as the second-largest region in the Merkel cell carcinoma market, with Germany, the United Kingdom, and France as key revenue contributors. The region benefits from established checkpoint inhibitor use and multidisciplinary care pathways in specialized oncology and dermatology centers. Real-world registry data from German dermatologic oncology centers has strengthened clinical evidence in this rare-disease segment. However, intense reimbursement reviews in some markets may limit uptake outside major centers and affect biologics' pricing power.

Asia-Pacific is the fastest-growing region in the Merkel cell carcinoma market, with Japan, China, and Australia driving growth through diverse demand patterns. Japan prioritizes checkpoint inhibitors in care pathways, with chemotherapy as a secondary option. Regulatory familiarity with retifanlimab in Japan during 2025 highlights the potential for faster adoption of rare-cancer immunotherapies. Aging populations and expanding oncology infrastructure in urban centers further support the region's rapid growth trajectory, despite its smaller current market base compared to North America and Europe.

- AstraZeneca

- BioInvent International AB

- Bristol-Myers Squibb

- EMD Serono, Inc.

- FUJIFILM Pharmaceuticals U.S.A., Inc.

- ImmunityBio, Inc.

- Immunomic Therapeutics, Inc.

- Incyte

- Kartos Therapeutics, Inc.

- MacroGenics

- Merck

- Merck

- Natera, Inc.

- Ono Pharmaceutical

- Pfizer

- Replimune Group, Inc.

- Transgene

- TuHURA Biosciences, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Elderly and Immunosuppressed Patient Pool

- 4.2.2 Checkpoint Inhibitors Entrenched in Guidelines

- 4.2.3 Additional PD-1 Option Broadening Access

- 4.2.4 Chemo-To-Immunotherapy Treatment Shift

- 4.2.5 ctDNA-Guided Surveillance Adoption

- 4.2.6 Adjuvant Immunotherapy Readouts Expanding Duration

- 4.3 Market Restraints

- 4.3.1 Tiny Incident Population and Recruitment Bottlenecks

- 4.3.2 High Biologic Cost and Reimbursement Scrutiny

- 4.3.3 Post-PD-(L)1 Refractory Treatment Gap

- 4.3.4 Immunosuppressed-Patient Treatment Trade-Offs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Disease Stage

- 5.1.1 Stage I

- 5.1.2 Stage II

- 5.1.3 Stage III

- 5.2 By Modality

- 5.2.1 Diagnosis

- 5.2.1.1 Biopsy

- 5.2.1.2 Imaging

- 5.2.1.3 Others

- 5.2.2 Treatment

- 5.2.2.1 Surgery

- 5.2.2.2 Radiation Therapy

- 5.2.2.3 Chemotherapy

- 5.2.2.4 Targeted Therapy

- 5.2.2.5 Others

- 5.2.1 Diagnosis

- 5.3 By End User

- 5.3.1 Academic Cancer Centers

- 5.3.2 Hospital Oncology Departments

- 5.3.3 Office-Based Oncology and Infusion Centers

- 5.3.4 Reference Laboratories and Molecular Diagnostics Labs

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AstraZeneca PLC

- 6.3.2 BioInvent International AB

- 6.3.3 Bristol-Myers Squibb Company

- 6.3.4 EMD Serono, Inc.

- 6.3.5 FUJIFILM Pharmaceuticals U.S.A., Inc.

- 6.3.6 ImmunityBio, Inc.

- 6.3.7 Immunomic Therapeutics, Inc.

- 6.3.8 Incyte Corporation

- 6.3.9 Kartos Therapeutics, Inc.

- 6.3.10 MacroGenics, Inc.

- 6.3.11 Merck & Co., Inc.

- 6.3.12 Merck KGaA

- 6.3.13 Natera, Inc.

- 6.3.14 Ono Pharmaceutical Co., Ltd.

- 6.3.15 Pfizer Inc.

- 6.3.16 Replimune Group, Inc.

- 6.3.17 Transgene SA

- 6.3.18 TuHURA Biosciences, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment