|

시장보고서

상품코드

2064520

HR 데이터 및 보고 플랫폼 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)HR Data And Reporting Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

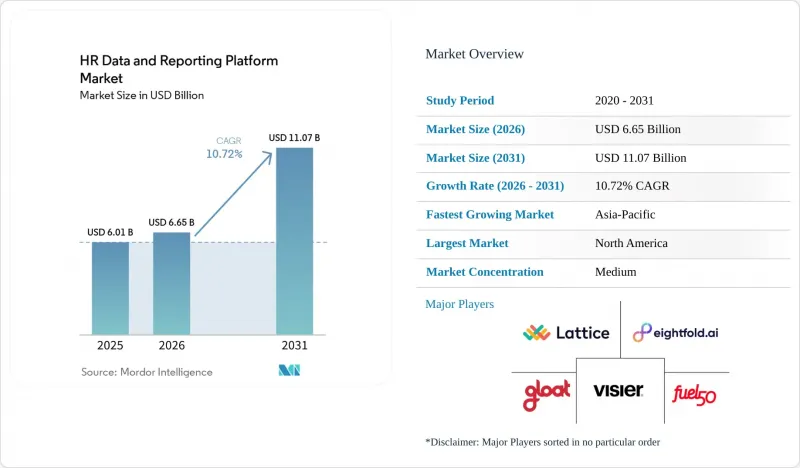

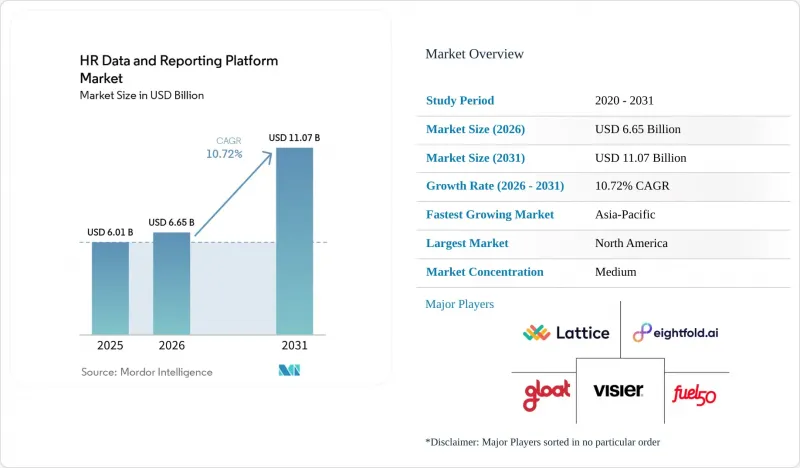

Mordor Intelligence에 의하면, HR 데이터 및 보고 플랫폼 시장 규모는 2025년 60억 1,000만 달러로 평가되었고, 2026년에는 66억 5,000만 달러로 추정되고, 2031년까지 110억 7,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 10.72%로 성장할 전망입니다.

본 보고서는 구성 요소별(소프트웨어, 서비스), 용도별(인재 분석·대시보드 등), 배포 방식별(클라우드, 온프레미스), 조직 규모별(대기업, 중소기업), 최종 사용자 산업별(IT 및 통신 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 HR 데이터 및 보고 플랫폼 시장 동향 및 인사이트

데이터 기반 인력 계획에 대한 수요 증가

HR 데이터 및 보고 플랫폼 시장은 직관에 기반한 인력 배치 결정에서 체계적인 시나리오 계획 수립으로의 명확한 전환으로 인해 혜택을 보고 있습니다. 단독으로 작성된 HR 보고서는 더 이상 이사회나 재무 부서의 의사결정을 충분히 지원할 수 없기 때문에 기업들은 현재 인건비, 기술 인력 공급, 미래의 수용 능력을 통합적으로 검토할 것을 요구하고 있습니다. 조직이 보다 신속한 대응을 필요로 하는 상황에서 데이터 피드의 지연은 계획 모델의 가치를 떨어뜨리기 때문에 공유 데이터 환경과 제로 카피 액세스의 중요성이 점점 더 커지고 있습니다. 인건비가 주요 비용인 동시에 경쟁 우위의 주요 원천이기도 한 산업, 특히 정보기술(IT) 및 금융 서비스 업계에서는 여전히 도입이 가장 활발히 이루어지고 있지만, 자동화로 인해 직무 설계 및 재배치에 대한 수요가 변화함에 따라 제조업에서도 도입이 활발해지고 있습니다. 따라서 벤더들은 HR 애널리틱스를 독립된 보고 계층으로 남겨두기보다는 인재 데이터를 보다 광범위한 비즈니스 데이터와 연계하는 통합형 인력 계획 도구로 전환하는 데 초점을 맞추었습니다. 이러한 추세는 계획 수립을 단순한 정기적인 인사 업무가 아닌 사업 운영상의 역량으로 자리매김함으로써, 인사 데이터 및 보고 플랫폼 시장에 지속적인 수요 기반을 창출하고 있습니다.

클라우드 기반 HR 분석으로의 전환 가속화

핵심 HR 시스템 전반에 걸친 클라우드 제공으로의 광범위한 전환 역시 HR 데이터 및 보고 플랫폼 시장을 견인하고 있습니다. 가장 중요한 변화는 표면적인 것이 아니라 아키텍처적인 것입니다. 클라우드 네이티브 분석 기능 덕분에, 과거에는 보고서 작성을 지연시키고 데이터를 오래된 상태로 만들었던 긴 파이프라인의 지연 없이, 실시간 또는 준실시간 데이터에 접근할 수 있게 되었기 때문입니다. Oracle은 Fusion Data Intelligence에서도 이와 유사한 방향성을 제시하고 있으며, 자연어 기반 접근 방식과 확장된 분석 기능을 통해 비즈니스 관련 질문에서 실질적인 인재 관련 답변에 이르기까지의 과정을 단축하도록 설계되었습니다. 아시아태평양에서는 디지털 문서 관리 규정, SaaS 도입 확대, 인프라 개선에 힘입어 성장하는 조직 내에서 호스팅형 모델의 도입이 정당화되기 쉬워지면서, 클라우드로의 전환이 가속화되고 있습니다. 유럽에서도 벤더가 감사 로그, 데이터 계보 추적, 거버넌스 도구를 현지 IT 팀에 맡기는 대신 플랫폼 계층에 통합할 수 있기 때문에 통합된 클라우드 관리는 매력적입니다. 그 결과, 구매자들이 단일 도입 모델을 통해 속도와 규정 준수 부담 경감을 모두 추구하는 가운데, HR 데이터 및 보고 플랫폼 시장에서는 클라우드에 대한 수요가 가장 빠르게 증가하고 있습니다.

분산된 HR 데이터 자산과 통합의 복잡성

HR 데이터 및 보고 플랫폼 시장은 여전히 근본적인 아키텍처상의 과제에 직면해 있습니다. 이는 직원 데이터가 채용, 급여, 교육, 복리후생, 근태 관리와 같은 여러 시스템에 분산되어 있으며, 이러한 시스템들은 원래 단일 레코드로 기능하도록 설계되지 않았기 때문입니다. 스키마, 업데이트 주기, 권한, 소유권 규칙이 서로 다르기 때문에 분석 작업이 시작되기 전부터 신뢰할 수 있는 직원 뷰를 생성하기가 어려워집니다. 따라서 현재 구매자들은 공급업체를 비교할 때 대시보드의 품질만으로 제품을 평가하는 것이 아니라, 네이티브 커넥터, 데이터 정규화 및 데이터 계보 관리를 신중하게 검토하고 있습니다. 통합 작업이 확대되거나 데이터 품질이 낮은 상태로 방치될 경우, 의사결정권자는 플랫폼에 대한 신뢰를 잃게 되며, 측정 가능한 가치를 얻기까지 걸리는 시간이 계획보다 길어지게 됩니다. 유럽에서는 특히 직원 데이터 처리 체계에 대한 법원의 면밀한 심사를 받은 이후, 데이터 전송 및 시스템 연동이 법적 요건과 기술적 호환성을 모두 충족해야 하기 때문에 이 문제는 더욱 심각합니다. 그 결과, HR 데이터·보고 플랫폼 시장은 성장을 이어가고 있지만, 도입 주기는 여전히 길어지고 있으며, 통합 작업이 성공의 열쇠가 되기 때문에 서비스에 대한 수요도 높은 수준을 유지하고 있습니다.

부문별 분석

2025년 기준으로 HR 데이터 및 보고 플랫폼 시장의 소프트웨어 점유율은 66.19%를 차지했으나, 서비스 부문은 2031년까지 연평균 성장률(CAGR) 12.75%로 확대될 것으로 전망됩니다. 소프트웨어 부문이 최대 규모를 유지하고 있는 이유는 정기적인 SaaS 라이선스와 임베디드 분석 모듈이 순수 소프트웨어 벤더와 대규모 HCM 제품군 제공업체 모두에게 여전히 주요 수익 기반이 되고 있기 때문입니다. 구매자들은 보다 고도화된 이용 사례를 확장하기 전에 안정적인 보고서 엔진, 거버넌스가 적용된 데이터 구조, 그리고 직원 대시보드를 위한 공통 인터페이스가 필요하기 때문에 계속해서 소프트웨어 도입을 시작하고 있습니다. 표준 대시보드 기능은 공급업체 간에 쉽게 재현될 수 있게 되었으며, 이는 소프트웨어의 경쟁력이 기본적인 시각화보다는 데이터의 심도, 거버넌스 제어 및 통합 품질에 더 많이 좌우되게 되었음을 의미합니다. 이에 따라 라이선스 수익을 넘어서는 가치에 대한 논의가 확산되고 있음에도 불구하고, 소프트웨어 계층은 HR 데이터 및 보고 플랫폼 시장의 핵심으로 자리 잡고 있습니다.

서비스 부문의 성장이 가속화되고 있는 이유는 플랫폼의 가치가 이전 보고서 도입 당시보다 통합, 모델 거버넌스, 변경 관리 및 도입 지원에 훨씬 더 크게 의존하게 되었기 때문입니다. 이는 기업이 AI 기능을 추가할 때 특히 해당됩니다. 설명 가능성, 워크플로우 재설계 및 정책의 일관성을 확보하기 위해서는 단순한 보고서 배포보다 수동 설정이 더 많이 필요하기 때문입니다. 또한, 중견 기업들도 예측적 인사이트를 필요로 하는 경우, 사내에 데이터 엔지니어링이나 인력 과학 분야의 역량이 부족한 경우가 많기 때문에 매니지드 애널리틱스 서비스에 관심을 기울이고 있습니다. SAP는 2025년 하반기 릴리스에서 이러한 변화를 강조하며, SAP Business Data Cloud상의 ‘People Intelligence’를 보상, 역량, 후계자 육성, 학습 등 다양한 분야에 걸쳐 사전 구축된 이용 사례를 갖춘, 별도의 라이선스가 필요한 분석 계층으로 자리매김했습니다. 따라서 HR 데이터 및 보고 플랫폼 시장에서는 소프트웨어 구독뿐만 아니라 지속적인 자문, 도입 및 관리형 인텔리전스 서비스를 통해 더 많은 가치가 창출되고 있습니다.

2025년 기준으로 HR 데이터 및 보고 플랫폼 시장 규모의 36.32%를 인력 분석 및 대시보드가 차지했으며, 예측 분석 시장은 2031년까지 연평균 성장률(CAGR) 11.49%로 확대될 것으로 전망됩니다. 대시보드는 직원 수, 이직률, 다양성, 보상, 리더십 지표에 관한 일반적인 보고서를 필요로 하는 많은 구매자들에게 여전히 첫 번째 단계가 되기 때문에 가장 널리 사용되는 용도으로 자리 잡고 있습니다. 또한, 대시보드는 경영진용 보고서, 공시 대응, 관리자의 셀프 서비스형 쿼리와 자연스럽게 연동되므로, 분석 성숙도가 각기 다른 조직 전체에 걸쳐 도입하기가 용이해집니다. 많은 기업에서는 보다 정교한 예측이나 자동화된 추천 기능을 신뢰할 수 있게 되기 전에 정확한 설명형 보고서가 필요하기 때문에 대시보드는 초기 도입의 기반으로서 계속해서 중요한 역할을 하고 있습니다. 따라서 HR 데이터 및 보고 플랫폼 시장에서는 인력 분석과 대시보드를 쇠퇴해 가는 구식 기능이 아니라, 보다 광범위한 도입으로 이어지는 관문으로 계속해서 인식하고 있습니다.

고용주들이 이직 위험, 기술 부족, 채용 병목 현상, 노동력 수용 능력과 관련해 미래를 내다보는 인사이트를 점점 더 필요로 함에 따라, 예측 분석 분야는 급속히 성장하고 있습니다. 2026년에 발표된 조사에 따르면, 데이터 품질과 균형이 개선된다면 고급 앙상블 모델은 직원 이직 분류에서 매우 높은 정확도를 달성할 수 있으며, 이는 HR 환경에서 더 광범위한 실제 적용을 촉진할 것으로 나타났습니다. EU의 임금 투명성 지침에 따라 고용주는 직종별 임금 격차 보고서를 보다 체계적으로 작성하고 보고 체계를 강화해야 하므로, 이러한 움직임이 규정 준수 보고의 확대로도 이어지고 있습니다. 실시간 직원 모니터링도 발전하고 있지만, 유럽 여러 국가의 GDPR(EU 개인정보보호규정)에 명시된 비례 원칙 및 협의 관련 규정에 따라 개인 단위의 모니터링 관행이 여전히 제한받고 있어, 그 발전 속도는 더욱 신중한 양상을 띠고 있습니다. 이러한 모든 이용 사례를 종합해 볼 때, HR 데이터 및 보고 플랫폼 시장은 정기적인 과거 데이터 보고에서 일상적인 업무 의사결정과 더 밀접하게 연계된 지속적인 분석으로 전환되고 있습니다.

지역별 분석

2025년, 북미는 HR 데이터 및 보고 플랫폼 시장 규모의 34.14%를 차지했으며, 최대 지역 시장이 되었습니다. 이 지역이 주도적인 입지를 차지하고 있는 이유는 피플 애널리틱스의 도입이 이미 성숙 단계에 접어들었으며, 이직 비용이 높은 수준을 유지하고 있었고, 또한 고용주들이 다른 대부분 시장보다 더 오랜 기간 동안 정보 공개 및 임금 보고에 대한 기대에 부응해 왔기 때문입니다. 미국에서는 2025년에 공시 환경이 변경되었습니다. 이는 SEC(미국 증권거래위원회)의 인적 자본 관련 규제안이 단기 의제에서 제외되었고, S&P 100 구성 기업들이 Form 10-K 제출 서류에서 DEI(다양성·공정성·포용성)에 관한 기술 범위를 축소했기 때문입니다. 이러한 변화로 인해 수요는 다양성 보고의 추가 확대가 아닌, 생산성, 역량, 보상 분석으로 전환되고 있습니다. 캐나다는 현지 분석 인력과 임금 평등 요건 덕분에 여전히 중요한 2차 시장으로 자리 잡고 있습니다. 한편, 멕시코는 니어쇼어링의 확대에 따라 국경을 초월한 인재 계획의 필요성이 높아짐에 따라 그 중요성이 커지고 있습니다.

유럽은 HR 데이터 및 보고 플랫폼 시장에서 여전히 가장 규제가 주도적인 지역 중 하나이며, 이 지역에서의 구매 결정은 규정 준수 기한에 크게 좌우됩니다. 2026년 6월 7일을 국내법 제정 기한으로 정한 EU 임금 투명성 지침에 따라, 고용주는 보다 견고한 직무 체계, 임금 격차 보고 및 급여 범위 공개 절차를 자사의 HR 데이터 워크플로우에 통합해야만 합니다. 독일, 프랑스, 네덜란드, 벨기에 등의 국가에서는 근로자 대표위원회의 개입으로 인해 상황이 더욱 복잡해지고 있으며, 리스크가 높은 HR AI에 대한 협의로 인해 조달 및 도입 일정이 장기화될 가능성이 있습니다. 영국, 독일, 프랑스가 여전히 지역 수요의 대부분을 차지하고 있지만, 제재와 지정학적 제약으로 인해 러시아는 국내 솔루션에 대한 의존도를 대폭 높이고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 11.88%를 나타낼 것으로 예측되며, HR 데이터 및 보고 플랫폼 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 이러한 성장은 광범위한 인력 규모, 클라우드 인프라의 보급, 그리고 현지 언어, 규정 준수, 가격 책정 요구 사항을 충족할 수 있는 강력한 국내 공급업체 기반에 힘입어 이루어지고 있습니다. 중국은 그 중심에 있으며, 2026년 5월 Yonyou가 해외로 진출하는 중국 기업을 대상으로 AI 기반 세계 HCM 솔루션을 출시한 것은 현지 벤더들이 국내용 보고 기능에서 다국적 대응 능력으로 진화하고 있음을 보여줍니다. 인도 및 동남아시아에서는 모바일 우선이자 다국어를 지원하는 플랫폼에 대한 수요가 꾸준히 증가하고 있는 반면, 일본에서는 노동력의 고령화에 따라 후계자 양성 및 기술 지속성에 대한 분석의 필요성이 커지고 있습니다. 호주 및 뉴질랜드는 규모는 작지만, 규정 준수를 중시하는 제도 도입 면에서는 선진적입니다. 한편, 중동과 남미에서는 노동력 현지화 프로그램, 노동 규정 준수 요구 사항, 그리고 공식적인 디지털 보고 요건의 중요성이 커짐에 따라 낮은 수준에서 수요가 확대되고 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the hR data and reporting platform market size is expected to increase from USD 6.01 billion in 2025 to USD 6.65 billion in 2026 and reach USD 11.07 billion by 2031, growing at a CAGR of 10.72% over 2026-2031.

This report is Segmented by Component (Software, and Services), Application (Workforce Analytics and Dashboarding, and More), Deployment Mode (Cloud, and On-Premises), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Information Technology and Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global HR Data And Reporting Platform Market Trends and Insights

Rising Demand for Data-Driven Workforce Planning

The HR data and reporting platform market is benefiting from a clear shift away from intuition-led headcount decisions and toward structured scenario planning. Enterprises now want labor costs, skills supply, and future capacity reviewed together, because isolated HR reports do not support board or finance decisions well enough anymore. This is making shared data environments and zero-copy access more important, since delayed data feeds reduce the value of planning models when organizations need faster responses. Adoption remains strongest in sectors where labor is both a major cost and a major source of competitive advantage, especially in information technology and financial services, while manufacturing is increasingly active as automation changes role design and redeployment needs. The vendor focus has therefore moved toward integrated workforce planning tools that connect people data with broader business data rather than leaving HR analytics as a stand-alone reporting layer. This pattern creates a durable demand base for the HR data and reporting platform market by treating planning as an operating capability rather than a periodic HR exercise.

Accelerating Shift Toward Cloud-Based HR Analytics

The broader shift toward cloud delivery across core HR systems is also boosting the HR data and reporting platform market. The most important change is architectural rather than cosmetic, because cloud-native analytics can now access live or near-live data without the long pipeline delays that used to slow and outdated people's reporting. Oracle has taken a similar direction in Fusion Data Intelligence, where natural language access and expanded analytical features are designed to shorten the path between a business question and a usable workforce answer. In the Asia-Pacific region, the cloud shift is accelerating because digital filing rules, growing SaaS adoption, and improved infrastructure are making hosted models easier to justify within expanding organizations. In Europe, centralized cloud controls are also attractive because vendors can build audit logs, lineage tracking, and governance tools into the platform layer rather than leaving those tasks to local IT teams. As a result, the HR data and reporting platform market is seeing cloud demand rise fastest, as buyers seek both speed and lower compliance effort from a single deployment model.

Fragmented HR Data Estates and Integration Complexity

The HR data and reporting platform market still faces a fundamental architecture problem because workforce data is often spread across recruiting, payroll, learning, benefits, and time systems that were never built to work as a single record. Different schemas, refresh cycles, permissions, and ownership rules make it difficult to create a trusted employee view, even before analytics work begins. This is why buyers now look closely at native connectors, data normalization, and lineage controls when comparing vendors, rather than judging products solely on dashboard quality. When integration work expands, or data quality remains weak, decision-makers lose confidence in the platform, and the time to measurable value exceeds the plan. In Europe, this issue is even harder because data transfers and system connections must meet both legal requirements and technical compatibility, especially following court scrutiny of employee data processing arrangements. The result is that the HR data and reporting platform market keeps growing, but implementation cycles remain longer, and service demand stays elevated because integration work remains central to success.

Other drivers and restraints analyzed in the detailed report include:

- Growing Use of AI for Attrition, Skills, and Capacity Forecasting

- Increasing Focus on Retention, Engagement, and Productivity Outcomes

- Employee Data Privacy and Cross-Border Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 66.19% of the HR data and reporting platform market share in 2025, while services are forecast to expand at a 12.75% CAGR through 2031. The software segment remained the largest because recurring SaaS licenses and embedded analytics modules continue to be the primary commercial base for both pure-play vendors and large HCM suite providers. Buyers continue to start with software because they need a stable reporting engine, governed data structures, and a common interface for workforce dashboards before they can scale more advanced use cases. Standard dashboarding has also become easier to replicate across vendors, which means software leadership now depends less on basic visualization and more on data depth, governance controls, and integration quality. This keeps the software layer central to the HR data and reporting platform market, even as the value conversation broadens beyond license revenue.

Services are growing faster because platform value depends more heavily on integration, model governance, change management, and adoption support than it did in earlier reporting deployments. This is especially true when enterprises add AI features, because explainability, workflow redesign, and policy alignment require more hands-on configuration than a simple reporting rollout. Mid-sized organizations are also leaning toward managed analytics offerings because they often lack in-house data engineering and workforce science skills, even when they want predictive insights. SAP highlighted this shift in its 2H 2025 release, positioning People Intelligence on SAP Business Data Cloud as a separately licensed analytics layer with prebuilt use cases across compensation, skills, succession, and learning. The HR data and reporting platform market is therefore seeing more value captured through recurring advisory, implementation, and managed intelligence work, rather than solely through software subscriptions.

Workforce analytics and dashboarding accounted for a 36.32% share of the HR data and reporting platform market size in 2025, while predictive analytics is projected to expand at an 11.49% CAGR through 2031. Dashboarding remained the largest application because it remains the first step for most buyers seeking common reporting on headcount, turnover, diversity, compensation, and leadership metrics. It also aligns naturally with executive reporting, disclosure support, and self-service manager queries, making adoption easier across organizations with varying analytical maturity. Many enterprises still need clean descriptive reporting before they can trust more advanced forecasting or automated recommendations, so dashboarding continues to anchor early deployments. For that reason, the HR data and reporting platform market continues to treat workforce analytics and dashboarding as the entry point for broader adoption rather than a fading legacy function.

Predictive analytics is growing faster as employers increasingly seek forward-looking insights into attrition risk, skills shortages, hiring bottlenecks, and labor capacity. Research published in 2026 showed that advanced ensemble models can achieve very high precision in employee attrition classification when data quality and balance improve, supporting broader production use in HR settings. The same movement is expanding compliance reporting, since the EU Pay Transparency Directive requires employers to prepare more structured pay gap reporting by work category and maintain stronger reporting discipline. Real-time workforce monitoring is also advancing, but more carefully, because GDPR proportionality and consultation rules in several European countries continue to limit person-level monitoring practices. Across these use cases, the HR data and reporting platform market is shifting from periodic historical reporting toward continuous analysis that sits closer to daily operating decisions.

Geography Analysis

North America accounted for a 34.14% share of the HR data and reporting platform market size in 2025, making it the largest regional market. The region led because people analytics adoption was already mature, turnover costs remained high, and employers had been operating under disclosure and pay reporting expectations for longer than most other markets. In the United States, the disclosure environment changed in 2025 when anticipated prescriptive SEC human capital rules were removed from the near-term agenda, and S&P 100 companies narrowed the scope of DEI wording in Form 10-K filings. That shift is moving demand toward productivity, skills, and compensation analytics rather than pushing another round of diversity-reporting expansion. Canada remains an important secondary market due to local analytics talent and pay equity requirements, while Mexico is gaining relevance as nearshoring increases the need for cross-border workforce planning.

Europe remains one of the most regulation-driven regions in the HR data and reporting platform market, and buying decisions there are heavily shaped by compliance deadlines. The EU Pay Transparency Directive, with a June 7, 2026, transposition deadline, is forcing employers to build stronger job architecture, pay gap reporting, and salary range disclosure processes into their HR data workflows. Works council involvement adds another layer in countries such as Germany, France, the Netherlands, and Belgium, where consultation on high-risk HR AI can extend procurement and deployment timelines. The United Kingdom, Germany, and France continue to account for most regional demand, while sanctions and geopolitical limits keep Russia far more dependent on domestic solutions.

Asia-Pacific is projected to grow at an 11.88% CAGR through 2031, making it the fastest-growing region in the HR data and reporting platform market. Growth is being supported by a broad workforce scale, rising cloud infrastructure, and a stronger domestic vendor base that can respond to local language, compliance, and pricing needs. China is central to that story, and Yonyou's May 2026 launch of an AI-driven global HCM solution for Chinese enterprises expanding abroad shows how local vendors are moving beyond domestic reporting into multinational capability. India and Southeast Asia are driving steady demand for mobile-first and multilingual platforms, while Japan's aging workforce is strengthening the case for succession and skills-continuity analytics. Australia and New Zealand remain smaller in scale but advanced in compliance-oriented deployment, while the Middle East and South America are growing from lower bases as workforce nationalization programs, labor compliance needs, and formal digital reporting requirements become more important.

- Visier, Inc.

- Crunchr B.V.

- One Model Inc.

- Culture Amp Pty Ltd.

- Lattice HQ, Inc.

- ChartHop, Inc.

- Gloat Ltd.

- Eightfold AI Inc.

- HiBob Ltd.

- Syndio Solutions, Inc.

- Nakisa Inc.

- PeopleInsight Analytics, Inc.

- GainInsights Solutions Pvt. Ltd.

- Perceptyx, Inc.

- Leapsome GmbH

- Knoetic, Inc.

- Humanforce Holdings Pty Ltd.

- Orgvue Ltd.

- Fuel50 Ltd.

- Panalyt Pte. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Data-Driven Workforce Planning

- 4.2.2 Accelerating Shift Toward Cloud-Based HR Analytics

- 4.2.3 Growing Use of AI for Attrition, Skills, and Capacity Forecasting

- 4.2.4 Increasing Focus on Retention, Engagement, and Productivity Outcomes

- 4.2.5 Pay Transparency Readiness and Job Architecture Standardization

- 4.2.6 Board-Level Human Capital Disclosure and Workforce Risk Reporting

- 4.3 Market Restraints

- 4.3.1 Fragmented HR Data Estates and Integration Complexity

- 4.3.2 Employee Data Privacy and Cross-Border Compliance Burden

- 4.3.3 Works Council Scrutiny of Monitoring-Oriented Analytics Deployments

- 4.3.4 Explainability and Bias Audit Burden for High-Risk HR AI

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration Services

- 5.1.2.2 Managed Services / Analytics-as-a-Service

- 5.1.2.3 Advisory and Consulting Services

- 5.2 By Application

- 5.2.1 Workforce Analytics and Dashboarding

- 5.2.2 HR Performance and KPI Reporting

- 5.2.3 Predictive Analytics

- 5.2.4 Compliance and Regulatory Reporting

- 5.2.5 Real-time Workforce Monitoring

- 5.2.6 Other Applications

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-Premises

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-Sized Enterprises

- 5.5 By End-User Industry

- 5.5.1 Information Technology and Telecommunications

- 5.5.2 Banking, Financial Services, and Insurance

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Manufacturing

- 5.5.5 Retail and Consumer Goods

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Chile

- 5.6.4.4 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Nigeria

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Visier, Inc.

- 6.4.2 Crunchr B.V.

- 6.4.3 One Model Inc.

- 6.4.4 Culture Amp Pty Ltd.

- 6.4.5 Lattice HQ, Inc.

- 6.4.6 ChartHop, Inc.

- 6.4.7 Gloat Ltd.

- 6.4.8 Eightfold AI Inc.

- 6.4.9 HiBob Ltd.

- 6.4.10 Syndio Solutions, Inc.

- 6.4.11 Nakisa Inc.

- 6.4.12 PeopleInsight Analytics, Inc.

- 6.4.13 GainInsights Solutions Pvt. Ltd.

- 6.4.14 Perceptyx, Inc.

- 6.4.15 Leapsome GmbH

- 6.4.16 Knoetic, Inc.

- 6.4.17 Humanforce Holdings Pty Ltd.

- 6.4.18 Orgvue Ltd.

- 6.4.19 Fuel50 Ltd.

- 6.4.20 Panalyt Pte. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment