|

시장보고서

상품코드

2064523

소매업용 인력 관리(WFM) 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Workforce Management (WFM) In Retail - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

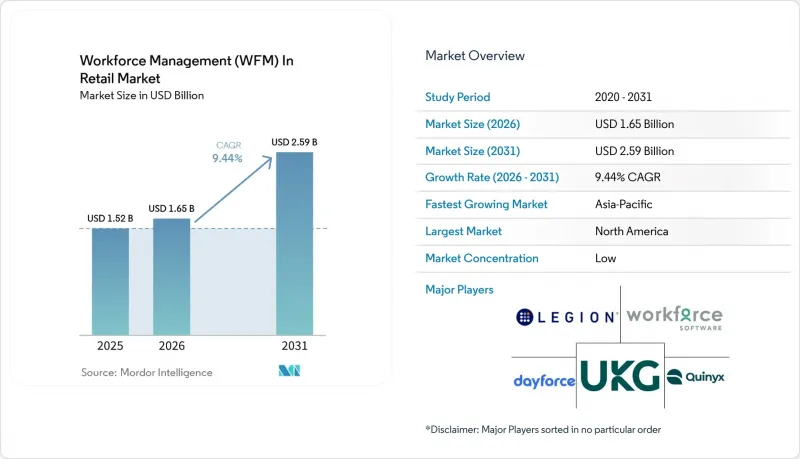

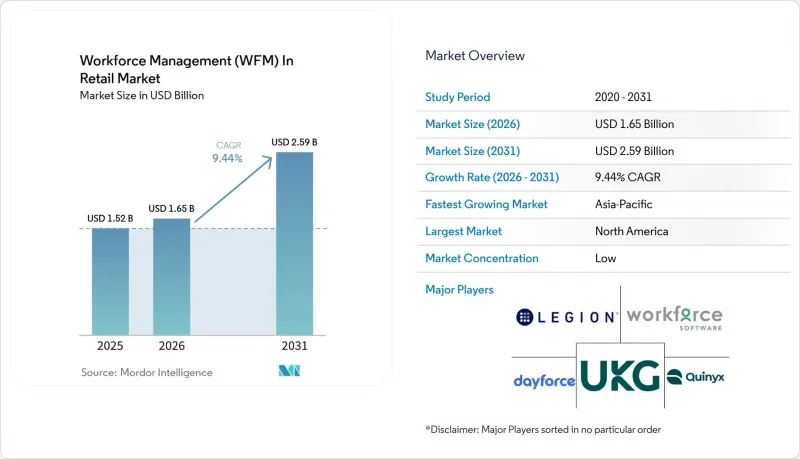

Mordor Intelligence에 의하면, 소매업용 인력 관리(WFM) 시장 규모는 2025년에 15억 4,000만 달러로 평가되었고, 2026년 17억 3,000만 달러로 추정되고, 2031년까지 30억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 12.30%를 나타낼 전망입니다.

본 보고서는 구성 요소별(소프트웨어, 서비스), 배포 방식별(클라우드, 온프레미스 등), 기업 규모별(대기업, 중소기업), 소매 업태별(식료품·슈퍼마켓, 패션 및 의류, 가전 양판점, 백화점, 전문 소매점 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 소매업용 인력 관리(WFM) 시장 동향 및 인사이트

클라우드 기반 및 AI 네이티브 스케줄링 도입

클라우드 전환은 소매업용 인력 관리(WFM) 시장에서 여전히 가장 강력한 단기적 성장 동력으로 작용하고 있습니다. AI 스케줄링 도구는 방문객 수, 현지 기상 상황, 프로모션 일정, 그리고 직원의 근무 가능 시간을 15분 또는 30분 단위로 처리할 수 있어, 기존 시스템으로는 충분히 처리할 수 없었던 세부적인 계획 수립을 소매업체가 가능하게 합니다. 근로자 측의 도입에 대한 거부감도 완화되고 있으며, 소매업 종사자의 77%가 AI가 자신의 희망에 맞는 근무 일정을 제안해 줄 것이라고 믿고 있다는 보고도 있습니다. 2025 회계연도, 클라우드 및 구독 매출은 28% 증가한 9,270만 유로(1억 10만 달러)를 기록하며, 그룹 총매출의 49%를 차지했습니다. 이는 기업 구매 담당자들이 예산을 구독 중심 모델로 전환하고 있음을 보여줍니다. 이러한 기능이 표준적인 요구 사항으로 자리 잡음에 따라, 소매업용 인력 관리(WFM)는 기본적인 디지털화 단계에서 실시간 인력 조정 단계로 전환되고 있습니다.

옴니채널 소매의 복잡화와 인력 최적화에 대한 요구

옴니채널 소매로 인해 인력 계획이 현저히 복잡해지고 있으며, 이러한 복잡성이 소매업용 인력 관리(WFM)에 대한 수요를 촉진하고 있습니다. 매장 팀은 현재 매장 내 서비스, 클릭 앤 콜렉트, 커브사이드 픽업, 온라인 주문 상품 피킹, 상품 보충 등의 업무에 시간을 할애하고 있으며, 한 교대 근무 동안 여러 가지 유형의 업무를 처리하는 것이 일반화되어 있습니다. 업계 리더는 소매업체가 전담 주문 처리 담당자를 배치하거나 시간대를 설정함으로써 매장 내 주문 처리가 가장 효과적으로 이루어질 수 있다고 강조하고 있습니다. 이는 정적인 주간 근무표가 아니라, 작업 단위의 일정 편성을 직접 의미합니다. 문제는 더 이상 인건비뿐만이 아닙니다. 부적절한 일정 관리는 주문 처리 능력, 수령 속도, 그리고 고객 서비스의 모든 측면을 동시에 저해하게 됩니다. 주문 변동 패턴에 맞추어 인력을 배치할 수 있는 소매업체는 이익률과 주문 처리 수익을 모두 확보하는 데 유리한 입장에 있으며, 첨단 인력 관리 도구는 옴니채널 성공의 핵심 요소가 됩니다.

POS, 급여 계산, HRIS, EC 시스템 간의 통합이 지닌 복잡성

통합에 따른 부담은 소매업용 인력 관리(WFM)의 가장 큰 구조적 제약 요인으로 남아 있습니다. 스케줄링 엔진은 이론적으로는 인력 배치를 최적화할 수 있지만, POS 시스템, 급여 계산 시스템, HRIS 플랫폼, 주문 관리 도구와 데이터를 원활하게 교환할 수 없다면 그 가치는 사라지게 됩니다. Shopify는 EY의 분석 결과를 인용하여, 통합된 소매 인프라를 통해 도입 비용을 11%, 미들웨어 비용을 27% 절감할 수 있음을 보여주었습니다. 이는 상호 연동되지 않은 기술 환경이 초래하는 숨겨진 비용을 여실히 드러내고 있습니다. 이 문제는 GDPR(EU 개인정보보호규정), CCPA, 그리고 직원 25명 이상을 고용한 고용주를 대상으로 2026년 1월부터 시행되는 온타리오주의 AI 투명성 요건 등, 개인정보 보호 및 AI 공개와 관련된 규제로 인해 시스템 간 데이터 마이그레이션이 엄격하게 관리되어야 하는 경우 더욱 심각해집니다. 따라서 각 벤더사는 ATOSS가 DATEV 인증 인터페이스나 SAP 인증 모듈을 예로 든 것처럼, 인증된 급여 시스템 연동, 기성 커넥터, 도입의 유연성 측면에서 더욱 치열한 경쟁을 펼치고 있습니다.

부문별 분석

2025년, 소매업용 인력 관리(WFM) 시장에서 소프트웨어가 71.24%의 점유율을 차지했으며, 직원 근무표 작성 및 인력 최적화는 시장 전체의 32.52%를 차지하며 계속해서 가장 큰 소프트웨어 하위 부문으로 자리매김했습니다. 이러한 상황은 근무 조의 질이 매장의 커버율, 인건비 및 매출 손실에 얼마나 직접적인 영향을 미치는지를 반영하고 있습니다. Logile의 보고서에 따르면, 직원의 77%는 부적절한 스케줄 수립으로 인해 매장에서 정기적으로 매출 손실이 발생하고 있다고 생각하며, 74%는 고객 동선 패턴을 기반으로 한 AI 기반 스케줄 수립에 긍정적인 반응을 보이고 있습니다. 근태 관리, 분석·예측, 휴가 관리는 일정 수립을 급여 계산의 정확성과 인력 현황 파악으로 이어주기 때문에 여전히 중요합니다. 소매업용 인력 관리(WFM) 업계에서 소프트웨어는 인력 계획과 일상적인 매장 운영을 연결하는 제어 계층의 역할을 하고 있습니다.

서비스 분야는 2031년까지 연평균 성장률(CAGR) 14.12%를 나타낼 것으로 예측되며, 소매업용 인력 관리(WFM) 분야 중에서도 가장 두드러진 성장세를 보이고 있습니다. 이는 플랫폼의 가치가 대규모 매장 네트워크 전반에 걸친 도입의 질, 지역별 규칙 설정, 그리고 변경 관리에 달려 있다는 사실을 반영하고 있습니다. UKG에 따르면, 현장 근로자의 57%가 고용주와의 소통을 모바일로만 하는 것을 선호한다고 답했으며, 70%는 고용주로부터 온디맨드 급여를 제공받지 못하고 있다고 답했습니다. 이는 도입 범위가 핵심인 스케줄링을 넘어, 직원 참여 및 급여 관련 기능으로 확대되고 있음을 보여줍니다. 소매 업계의 인력 관리가 플랫폼 주도형으로 전환됨에 따라, 소매업체가 수백 곳의 지점에서 고급 기능을 원활하게 운영하기 위해서는 지속적인 지원이 필요하기 때문에 서비스의 중요성이 커지고 있습니다.

2025년 소매업용 인력 관리(WFM) 시장 규모 중 클라우드가 66.38%를 차지했으며, 이는 대규모 온프레미스형 인프라에서 클라우드로의 전환이 지속되고 있음을 반영합니다. 소매업체들이 클라우드를 선호하는 이유는 초기 기술적 부담을 줄이고, 새로운 AI 기능이나 규정 준수 기능에 더 빠르게 접근할 수 있기 때문입니다. Quinyx사는 WFM 도입 사례의 65% 이상이 현재 클라우드 기반이라고 밝히며, 스케줄링 개선, 초과근무 시간 단축, 관리 업무 경감을 통해 3년 만에 초기 투자액의 10배 이상의 수익을 얻을 수 있다고 지적했습니다. 또한, 규정을 각 매장에 개별적으로 적용하는 것이 아니라 일원적으로 적용할 수 있기 때문에 클라우드는 소매업의 노무 관리에 있어 규제상의 현실에도 부합합니다. 온프레미스형 시스템은 데이터 주권, 내부 통제 또는 노동조합의 요건으로 인해 기밀 데이터를 로컬 인프라 근처에 보관해야 하는 경우, 여전히 일정한 의미를 지닙니다.

하이브리드 도입은 2031년까지 연평균 성장률(CAGR) 13.23%로 확대될 것으로 예측되며, 소매 업계의 인력 관리 시장에서 가장 빠르게 성장하는 도입 형태가 될 전망입니다. 이러한 경향은 클라우드의 민첩성을 추구하면서도 급여 계산 및 인사 데이터에 대한 보다 엄격한 관리가 필요한 대형 소매업체들에게 있어 현실적인 타협점임을 반영하고 있습니다. ATOSS Software SE의 2025년도 결산에서는 거버넌스상의 제약을 안고 있는 기업 고객을 지원함과 동시에, AI 주도 기능을 통해 클라우드의 본격적인 도입을 촉진한다는 두 가지 접근 방식이 제시되었습니다. 많은 소매업체들이 여전히 핵심 급여 계산 및 HRIS 기능을 구식 시스템으로 운영하고 있으며, 혼합 아키텍처가 지연 시간, 데이터 중복, 통합 시 발생하는 마찰과 같은 위험을 완화해 주기 때문에 하이브리드 방식의 성장은 타당합니다.

지역별 분석

2025년, 북미는 소매업용 인력 관리(WFM) 시장의 38.92%를 차지했으며, 여전히 최대 지역 기여자로서의 위상을 유지했습니다. 이 지역은 기업용 소프트웨어에 대한 지출 규모가 크고, AI 기반 노동 관리 도구의 도입이 빠르며, 예측형 스케줄링 규칙의 보급이 가장 활발하다는 점 등의 이점을 누리고 있습니다. UKG는 NRF 상위 100대 소매 기업 중 69곳에 서비스를 제공하고 있다고 밝혔으며, 이는 기업용 인력 관리 플랫폼이 이미 북미 소매 업계에 얼마나 깊이 뿌리내리고 있는지를 보여줍니다. Legion이 Dollar Tree의 9,000개 이상의 매장과 18개 물류 센터에서 서비스를 제공하고 있는 사례는 현재 북미에서 이 솔루션이 어느 정도 규모로 도입되고 있는지를 보여줍니다. 시애틀, 뉴욕, 시카고, 샌프란시스코, 포틀랜드, 로스앤젤레스 카운티 등의 도시에서는 규정 준수 자동화가 단순한 선택적 부가 기능이 아니라 실무상 필수 요건이 되었기 때문에 규제 환경이 계속해서 수요를 뒷받침하고 있습니다.

유럽은 노동 규제, 근태 기록, 데이터 거버넌스 요건이 시스템 업데이트 주기를 가속화하고 있기 때문에 소매업용 인력 관리(WFM)에 있어 구조적으로 중요한 지역으로 남아 있습니다. ATOSS Software SE는 OBI, C&A, Decathlon, Primark와 같은 소매업체 고객을 예로 들었는데, 이는 해당 지역이 기업들의 강력한 수요와 장기적인 도입 주기를 모두 갖추고 있음을 보여줍니다. EU 임금 투명성 지침을 국내법에 반영해야 하는 기한인 2026년 6월 7일은 워크포스 애널리틱스에 있어 보고 및 감사에 대한 압박을 더욱 가중시키는 요인이 되고 있습니다. 남미, 중동 및 아프리카에서는 도입이 아직 초기 단계이지만, 체계적인 소매업의 확대와 노동 감독 강화로 인해 다국어·다국 지원이 가능한 클라우드 네이티브 벤더들에게 새로운 시장 개척의 기회가 생겨나고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 13.02%를 나타낼 것으로 예측되며, 2031년까지 소매 업계의 WFM 시장 규모 측면에서 가장 빠르게 성장하는 지역이 될 전망입니다. GaiaWorks사는 34개국에서 1,800개 이상의 기업에 서비스를 제공하고 있다고 밝혔으며, 한 3C 소매업체의 사례에서는 고객 유동량을 기반으로 한 근무 일정 수립을 통해 매출 전환율을 10.8% 향상시키고, 불필요한 근무 시간을 28% 줄이는 데 성공했습니다. 중국 편의점 체인을 대상으로 한 또 다른 GaiaWorks 사례 연구에 따르면, 매장 수준 수요 모델과 연동된 AI 스마트 스케줄링 시스템을 도입한 후 인건비가 20% 절감된 것으로 보고되었습니다. 이 지역의 성장은 홍콩의 ‘468 전환’과 같은 노동 규제 개정과, 조직화된 소매업이 급속히 확대되고 있는 인도 등 시장에서 AI 주도형 소매 업무의 보급에 의해서도 뒷받침되고 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the workforce management (WFM) in retail market size was valued at USD 1.54 billion in 2025 and is estimated to grow from USD 1.73 billion in 2026 to reach USD 3.09 billion by 2031, at a CAGR of 12.30% during the forecast period (2026-2031).

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premises, and More), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Retail Format (Grocery and Supermarkets, Fashion and Apparel, Electronics Retail, Department Stores, Specialty Retail, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Workforce Management (WFM) In Retail Market Trends and Insights

Cloud-Based and AI-Native Scheduling Adoption

Cloud migration remains the strongest near-term force behind the workforce management (WFM) in retail market. AI scheduling tools can process foot traffic, local weather, promotion calendars, and employee availability in 15-minute or 30-minute intervals, giving retailers a planning depth that older systems could not handle well. Adoption friction is also easing on the labor side, with reports showing that 77% of retail associates would trust AI to recommend schedules that match their preferences. Cloud and subscription revenue rose 28% in FY2025 to EUR 92.7 million (USD 100.1 million), equal to 49% of total group revenue, which shows that enterprise buyers are shifting budget toward subscription-led models. As these capabilities become standard expectations, the workforce management in retail market is moving away from basic digitization and toward real-time labor orchestration.

Omnichannel Retail Complexity and Labor Optimization Needs

Omnichannel retail has made labor planning significantly more complex, and that complexity is fueling demand in the WFM in retail market. Store teams now divide their time across in-store service, click-and-collect, curbside handoff, e-commerce picking, and replenishment, meaning a single shift often carries multiple task types. Industry leaders have emphasized that in-store fulfillment works best when retailers create dedicated fulfillment roles or time blocks, which points directly to task-level scheduling rather than static weekly rosters. The challenge is no longer just labor cost. Poor scheduling now undermines order throughput, pickup speed, and customer service simultaneously. Retailers that can align labor deployment with order-wave patterns are better positioned to protect both margin and fulfillment revenue, making advanced workforce management tools central to omnichannel success.

Integration Complexity Across POS, Payroll, HRIS, and E-commerce Systems

Integration burden remains the largest structural restraint on the WFM in retail market. A scheduling engine can optimize labor on paper, but it loses value when it cannot exchange data smoothly with point-of-sale systems, payroll engines, HRIS platforms, and order management tools. Shopify cited EY analysis showing that unified retail infrastructure can reduce implementation costs by 11% and middleware expenses by 27%, which highlights the hidden cost of disconnected technology estates. The problem is sharper where privacy and AI disclosure rules require controlled data movement across systems, including GDPR, CCPA, and Ontario's January 2026 AI transparency requirement for employers with 25 or more staff. That is why vendors are competing harder on certified payroll links, prebuilt connectors, and deployment flexibility, as shown by ATOSS references to DATEV-certified interfaces and SAP-certified modules.

Other drivers and restraints analyzed in the detailed report include:

- Rising Retail Wage Costs and Margin Pressure

- Fair Workweek and Labor Compliance Automation Demand

- Data Privacy and Employee Monitoring Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 71.24% of the workforce management in retail market share in 2025, and employee scheduling and labor optimization remained the largest software sub-segment at 32.52% of the total market. This position reflects how directly schedule quality affects store coverage, labor cost, and lost sales. Logile reported that 77% of associates believe stores regularly lose sales due to poor scheduling, while 74% are open to AI-driven scheduling based on traffic patterns. Time and attendance, analytics and forecasting, and leave management remain important because they connect scheduling decisions to payroll accuracy and labor visibility. Within the workforce management in retail industry, software has become the control layer that ties labor planning to daily store execution.

Services are forecast to grow at a 14.12% CAGR through 2031, making them the fastest-growing component of the workforce management (WFM) in retail market. This reflects the fact that platform value depends on rollout quality, local rule configuration, and change management across large store networks. UKG stated that 57% of frontline workers prefer employer communication only through mobile, and 70% said their employer does not offer on-demand pay, which shows how implementation scope is widening beyond core scheduling into engagement and pay-adjacent functions. As the workforce management in retail industry becomes more platform-led, services are gaining weight because retailers need sustained support to make advanced features work across hundreds of locations.

Cloud accounted for 66.38% of the workforce management (WFM) in retail market size in 2025, which reflects the continued shift away from heavy on-premises infrastructure. Retailers favor cloud because it lowers upfront technology burden and speeds access to new AI and compliance features. Quinyx stated that more than 65% of WFM deployments are now cloud-based and pointed to returns above 10 times the original investment over 3 years through better scheduling, lower overtime, and reduced administration. Cloud also fits the regulatory reality of retail labor management, because rule updates can be pushed centrally instead of patched location by location. On-premises systems still retain some relevance where data sovereignty, internal control, or union requirements keep sensitive data closer to local infrastructure.

Hybrid deployment is projected to grow at a 13.23% CAGR through 2031, making it the fastest-growing deployment mode in the workforce management in retail market. This pattern reflects a practical compromise for large retailers that want cloud agility but still need tighter control over payroll or HR data. ATOSS Software SE's FY2025 results showed a two-track approach that supports enterprise clients with governance constraints while still encouraging fuller cloud adoption through AI-led capabilities. Hybrid growth also makes sense because many retailers still run core payroll or HRIS functions on older systems, and a mixed architecture reduces the risk of latency, data duplication, and integration friction.

Geography Analysis

North America held 38.92% of workforce management in retail market share in 2025, which kept it as the largest regional contributor. The region benefits from higher enterprise software spending, earlier adoption of AI-led labor tools, and the widest spread of predictive scheduling rules. UKG stated that it serves 69 of the NRF Top 100 retailers, which shows how deeply enterprise workforce platforms are already embedded in the North American retail base. Legion's rollout with Dollar Tree across more than 9,000 stores and 18 distribution centers shows the scale at which large North American deployments now operate. The regulatory environment continues to support demand, because cities such as Seattle, New York, Chicago, San Francisco, Portland, and Los Angeles County have turned compliance automation into a practical requirement rather than an optional add-on.

Europe remains a structurally important region for the workforce management (WFM) in retail market because labor regulation, time recording, and data governance requirements are forcing upgrade cycles. ATOSS Software SE highlighted retail customers such as OBI, C&A, Decathlon, and Primark, which shows that the region combines deep enterprise demand with long implementation cycles. The June 7, 2026 deadline for national transposition of the EU Pay Transparency Directive is adding another layer of reporting and audit pressure to workforce analytics. South America, the Middle East, and Africa are still earlier in adoption, but organized retail expansion and tighter labor oversight are creating greenfield openings for cloud-native vendors with multilingual and multi-country support.

Asia-Pacific is forecast to grow at a 13.02% CAGR, making it the fastest-growing geography in the WFM in retail market size through 2031. GaiaWorks stated that it serves more than 1,800 enterprises across 34 countries, and one 3C retail case delivered a 10.8% improvement in sales conversion and a 28% reduction in wasted labor hours through traffic-based scheduling. A separate GaiaWorks case study on a Chinese convenience chain reported a 20% reduction in labor costs after deployment of AI smart scheduling tied to store-level demand models. The region's growth is also supported by labor-rule updates such as Hong Kong's 468 transition and by the wider spread of AI-led retail execution in markets such as India, where organized retail is scaling fast.

- UKG Inc.

- Dayforce

- WorkForce Software, LLC

- Quinyx AB

- Legion Technologies, Inc.

- Deputechnologies Pty Ltd.

- ATOSS Software SE

- TimeClock Plus, LLC

- Planday A/S

- Rota Geek Limited

- SISQUAL Workforce Management, Lda.

- Swt Software Limited

- Logile, Inc.

- Orquest S.L.

- Icron Technologies

- Agendrix Inc.

- Tommy Associates Pty Ltd.

- TimeForge Labor Management

- StoreForce Solutions Inc.

- Evolia

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-Based and AI-Native Scheduling Adoption

- 4.2.2 Omnichannel Retail Complexity and Labor Optimization Needs

- 4.2.3 Rising Retail Wage Costs and Margin Pressure

- 4.2.4 Fair Workweek and Labor Compliance Automation Demand

- 4.2.5 Task-Level Labor Planning for Click-and-Collect and Micro-Fulfillment

- 4.2.6 Cross-Store Labor Pooling and Gig-Like Shift Flexibility

- 4.3 Market Restraints

- 4.3.1 Integration Complexity Across POS, Payroll, HRIS, and E-commerce Systems

- 4.3.2 Data Privacy and Employee Monitoring Concerns

- 4.3.3 Forecast Drift from Promotion-Led Demand Spikes and Returns Surges

- 4.3.4 Frontline Manager Override Bias and Low Trust in AI Schedules

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Employee Scheduling and Labor Optimization

- 5.1.1.2 Time and Attendance Management

- 5.1.1.3 Workforce Analytics and Forecasting

- 5.1.1.4 Leave and Absence Management

- 5.1.1.5 Task and Execution Management

- 5.1.1.6 Employee Self-service and Communication

- 5.1.2 Services

- 5.1.1 Software

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By Enterprises Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By Retail Format

- 5.4.1 Grocery & Supermarkets

- 5.4.2 Fashion & Apparel

- 5.4.3 Electronics Retail

- 5.4.4 Department Stores

- 5.4.5 Specialty Retail

- 5.4.6 Convenience Stores

- 5.4.7 E-commerce Retailers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Southeast Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 UKG Inc.

- 6.4.2 Dayforce

- 6.4.3 WorkForce Software, LLC

- 6.4.4 Quinyx AB

- 6.4.5 Legion Technologies, Inc.

- 6.4.6 Deputechnologies Pty Ltd.

- 6.4.7 ATOSS Software SE

- 6.4.8 TimeClock Plus, LLC

- 6.4.9 Planday A/S

- 6.4.10 Rota Geek Limited

- 6.4.11 SISQUAL Workforce Management, Lda.

- 6.4.12 Swt Software Limited

- 6.4.13 Logile, Inc.

- 6.4.14 Orquest S.L.

- 6.4.15 Icron Technologies

- 6.4.16 Agendrix Inc.

- 6.4.17 Tommy Associates Pty Ltd.

- 6.4.18 TimeForge Labor Management

- 6.4.19 StoreForce Solutions Inc.

- 6.4.20 Evolia

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

(주말 및 공휴일 제외)