|

시장보고서

상품코드

2064525

냉장 진열장 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Refrigerated Display Cases - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

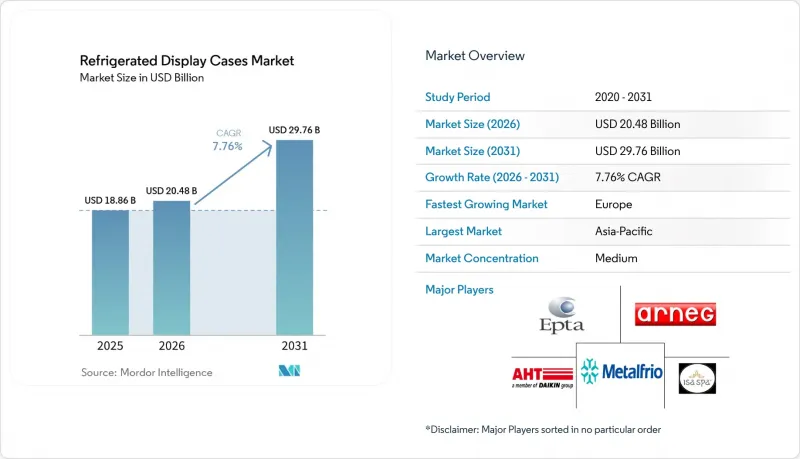

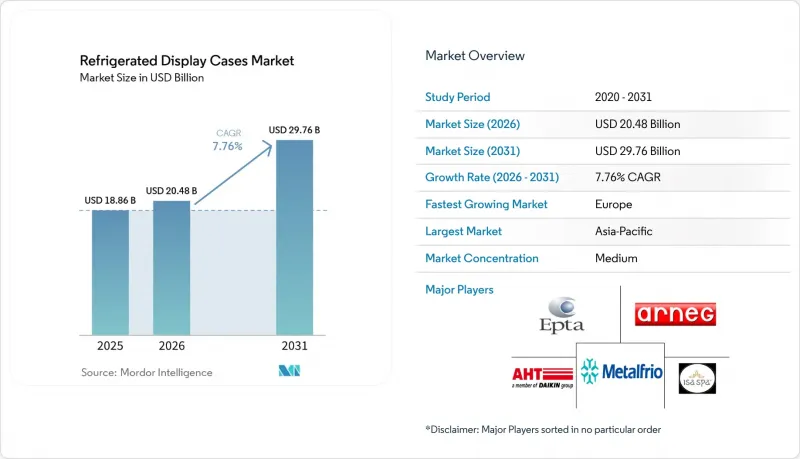

Mordor Intelligence에 의하면, 냉장 진열장 시장 규모는 2025년 188억 6,000만 달러로 평가되었고, 2026년 204억 8,000만 달러로 추정되고, 2031년까지 297억 6,000만 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 7.76%를 나타낼 것으로 예측됩니다.

본 보고서는 냉동 방식별(플러그인, 세미 플러그인, 리모트), 제품 설계별(수직형, 수평형, 하이브리드, 세미 수직형), 용도별(소매점, 레스토랑 및 호텔 등), 최종 사용자별(슈퍼마켓 및 하이퍼마켓, 편의점, 전문점, 할인점 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 냉장 진열장 시장 동향 및 인사이트

소매 체인의 리모델링 및 편의점 확장

소매점 현대화 프로그램으로 인해 냉장 진열장에 대한 수요가 일반적인 교체 주기를 넘어 확대되고 있습니다. 편의점에서는 조리 식품, 포장 음료, 냉장 식품의 진열 공간을 확대하고 있으며, 이에 따라 리모델링된 각 매장에서 필요한 쇼케이스의 수가 증가하고 있습니다. 편의점의 푸드서비스 매출은 2005년 11.9%에서 2025년에는 28.5%로 증가하여 점포 총이익의 38.9%를 차지했으며, 이는 사업자들이 냉장 식품의 가시성을 중시하여 점포 설계를 진행하고 있는 이유를 뒷받침하고 있습니다. 러브스 트래블 스톱스(Love's Travel Stops)는 2026년, ‘로드 어헤드 플랜(Road Ahead Plan)’의 일환으로 20개 점포의 신규 출점과 35개 점포의 기존 점포 리모델링에 7억 달러를 투자하며, 이 프로그램의 핵심으로 알찬 식음료 메뉴를 내세웠습니다. 냉장 진열장 시장에서 이러한 경향은 중요한 의미를 지닙니다. 왜냐하면 식품 중심의 편의점 형태는 기존의 연료 판매 중심 레이아웃에 비해 일반적으로 냉장 진열 공간을 더 많이 필요로 하기 때문입니다. 이로 인해 신규 점포 개설과 점포 리모델링 모두에서 수요가 활발하게 유지되고 있습니다.

천연 냉매 및 에너지 절약 개조 사이클

냉장 진열장 시장에서는 자발적인 지출이 아닌, 냉매 규제에 따른 교체 열풍이 일고 있습니다. 규정(EU) 2024/573이 2024년 3월에 발효됨에 따라, 유럽연합(EU) 전역에서 불소계 온실가스의 단계적 감축 일정이 더욱 엄격해졌습니다. 미국에서는 새로운 연방 규제에 따라 신규 상업용 냉동 설비에서 지구 온난화 지수가 낮은 냉매로의 전환이 촉진되고 있으며, 그 결과 구형 HFC 계열 시스템의 교체 시기가 앞당겨지고 있습니다. 또한, EPA는 2024년에 독립형 쇼케이스의 R290 충전량 상한선을 상향 조정했습니다. 이로 인해 기존보다 설치 면적이 더 넓은 프로판 기반 플러그인 시스템의 이용 사례가 확대되었습니다. 2025-2029년 미국의 식품 소매업체들은 1,470곳의 신규 트랜스크리티컬 CO₂ 매장을 설치하고 1만 3,400곳의 기존 시스템을 교체할 계획이며, 이를 통해 전환 계획이 얼마나 대규모인지 알 수 있습니다. 냉장 진열장 시장에서는 사업자가 설비 결정을 무기한으로 미룰 수 없기 때문에 이러한 규제 준수 기한이 수요의 하한선으로 작용하고 있습니다.

높은 초기 개보수 및 설치 비용

자본 비용은 냉장 진열장 시장에서 도입을 가로막는 직접적인 걸림돌로 계속 작용하고 있으며, 특히 소규모 사업자에게는 더욱 그러합니다. 신규 건설의 경우, 초임계 CO₂ 시스템은 기존의 HFC 시스템보다 10-20% 더 비쌀 가능성이 있으며, 개보수 프로젝트에서는 대개 추가적인 인프라 공사가 필요하기 때문에 그 차이는 더욱 벌어집니다. 사업자가 동일한 계획 주기 내에서 매장 리모델링, 에너지 효율화 및 냉매 규제 대응에도 자금을 투입하고 있는 경우, 그 부담을 감당하기는 더욱 어려워집니다. 뉴욕주는 브롱크스 지역의 키 푸드(Key Food) 매장 2곳이 R290 시스템으로 전환할 수 있도록 지원하기 위해 35만 달러를 지원했습니다. 이는 공공 지원이 이미 소규모 소매업체의 경제적 부담을 덜어주고 있음을 보여줍니다. 냉장 진열장 시장에서 이는 전환 비용을 더 대규모의 매장 네트워크나 장기적인 자본 계획에 분산할 수 있는 대형 체인점에 유리하게 작용합니다. 또한, 점포가 규모에 따른 구매력을 갖추지 못한 세분화된 소매 환경에서는 전환 속도를 늦추는 요인이 됩니다.

부문별 분석

2025년 기준으로 플러그인형 냉장 진열장는 시장 점유율의 58.37%를 차지했으며, 냉장 진열장 시장에서 가장 큰 비중을 차지하는 부문으로서의 위상을 유지했습니다. 이러한 경쟁력은 편의점, 베이커리, 전문 소매점 및 소규모 식료품점에 널리 보급된 독립형 유닛의 풍부한 도입 실적을 반영한 것입니다. 플러그인 시스템은 설치가 간편하고 중앙 집중식 냉동 설비가 필요하지 않기 때문에 많은 개보수 프로젝트에서 여전히 표준적인 선택지로 자리 잡고 있습니다. 2024년에 R290 내장형 케이스에 대한 EPA의 충전량 제한이 상향 조정됨에 따라, 프로판 기반 플러그인 유닛이 적용 가능한 점포 형태의 범위가 확대되었으며, 중소규모 점포의 교체 근거가 강화되었습니다.

원격 시스템은 2026-2031년 연평균 성장률(CAGR) 8.34%를 나타낼 것으로 예측되며, 냉장 진열장 시장에서 가장 빠르게 성장하는 시스템 구성이 될 전망입니다. 이러한 성장은 보다 광범위한 온도 제어와 시스템 통합을 가능하게 하는 중앙 집중식 CO₂ 랙을 선호하는 신규 슈퍼마켓 건설 및 대규모 리모델링 프로그램에 힘입어 이루어지고 있습니다. 푸드 라이온이 2025년 하반기 샬럿 지역에서 실시한 리모델링 프로그램에서는 일부 매장에 CO2 기반 냉각 시스템이 도입되었습니다. 이는 대형 체인점이 매장 리모델링과 냉매 교체를 어떻게 병행하여 진행하고 있는지를 보여줍니다. 세미 플러그인 시스템은 특히 유럽 소매 업계에서 여전히 중간적인 위치를 차지하고 있습니다. 이 지역에서는 열 회수 및 워터 루프의 배치가, 완전한 원격 설치보다 더 높은 유연성을 요구하는 중규모 매장을 뒷받침하고 있습니다. 따라서 냉장 진열장 업계는 개보수에 적합한 플러그인 유닛과 체인 주도형 원격 설치 방식 사이에서 더욱 명확하게 양분화되고 있습니다.

2025년에는 세로형 케이스가 55.12%의 점유율을 차지했으며, 냉장 진열장 시장 전체에서 계속해서 핵심적인 디자인 형태로 자리매김했습니다. 이러한 위상은 선반의 가시성과 폭넓은 SKU 진열이 필수적인 유제품, 신선식품, 음료 및 매장 주변 상품 진열에서 효과적으로 활용된 데서 비롯됩니다. 2026년에 출시된 Epta사의 ‘Zenith’ 시리즈는 기존 모델에 비해 최대 36%의 에너지 절감을 실현하는 동시에 진열 면적을 최대 13% 확대함으로써, 수직형 캐비닛이 효율과 판매 실적 모두를 어떻게 향상시킬 수 있는지 보여주었습니다. 소매업체들이 기존 매장 면적에서 더 높은 생산성을 추구하는 가운데, 이러한 조합은 수직형 포맷의 우위를 유지하는 데 기여하고 있습니다.

하이브리드 구성은 2031년까지 연평균 성장률(CAGR) 8.56%로 확대될 것으로 예상되며, 냉장 진열장 시장에서 가장 빠르게 성장하는 디자인 부문이 될 전망입니다. 소매업체들은 에너지 관리를 개선하는 동시에, 단일 진열 라인 내에서 개방형과 폐쇄형 진열을 결합할 수 있는 혼합형 진열 방식에 더 큰 관심을 보이고 있습니다. 수평형 케이스는 여전히 냉동 가슴형 냉장고 및 아이스크림 용도로 사용되고 있으며, 2024년 하반기에 AHT가 출시한 ‘KIGALI XL’은 이 시장 부문에서 가시성과 R290 기반 성능에 중점을 둔 제품 개발이 지속되고 있음을 보여주었습니다. 하이브리드형 성장 방식이 중요시되는 이유는 매장 전체에서 독립된 진열대를 줄이고 카테고리 배치의 유연성을 높이는 등 소매업체의 요구를 반영하고 있기 때문입니다. 냉장 진열장 업계의 설계 경쟁은 단순한 형태보다는 각 캐비닛의 레이아웃이 에너지 절약과 상품 진열의 질을 모두 어떻게 뒷받침할 수 있는지에 초점이 맞추어지고 있습니다.

지역별 분석

2025년, 유럽은 냉장 진열장 시장 점유율의 39.41%를 차지했으며, 가장 큰 기여를 한 지역이 되었습니다. 이 지역의 경쟁력은 슈퍼마켓의 높은 밀집도와 다른 많은 시장보다 엄격한 환경 규제에 힘입어 CO₂ 냉동 시스템으로 조기에 전환한 점을 반영하고 있습니다. 규정(EU) 2024/573은 불소계 온실가스의 단계적 폐지 계획을 강화하고, 유럽연합(EU) 전역의 사업자들에게 시스템 업데이트 계획을 앞당기도록 요구하고 있습니다. 이러한 정책적 배경은 매장 리뉴얼 활동을 통해 더욱 힘을 얻고 있습니다. 그 예로, 웨이트로즈 콜즈던 지점의 2025년 냉장 설비 교체 및 매장 리모델링 프로젝트를 들 수 있는데, 이곳에서는 시스템 교체가 보다 광범위한 현대화 공사와 연계하여 진행되었습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 8.73%로 성장할 것으로 예상되며, 냉장 진열장 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 도시화, 편의점의 확산, 그리고 콜드체인 인프라에 대한 지속적인 투자가 중국, 인도, 한국 및 동남아시아 전역에서 수요를 견인하고 있습니다. 한국의 편의점 업계는 품질 향상 단계에 접어들었으며, 사업자들이 구형 장비를 인버터식 고효율 진열장으로 교체한 비율은 70%를 넘어섰습니다. 인도 역시 강력한 수요 거점으로 부상하고 있으며, 조직화된 소매업의 확대와 엘란프로(Elanpro)의 2025년 체험 센터 구상 등 공급업체들의 투자가 국내 상업용 냉동·냉장 기기 시장의 성장을 뒷받침하고 있습니다.

북미는 여전히 2위 지역 시장이며, 냉장 진열장 시장에서 천연 냉매 도입의 주요 쟁점이 되고 있습니다. 미국에서는 2025년 1월, 독립형 설비에 사용되는 고GWP 냉매에 대한 새로운 연방 규제가 발효되었고, 2026년 1월에는 적용 범위가 원격 응축형 응용 분야로 확대됨에 따라 더욱 엄격한 준수 단계에 접어들었습니다. 크로거, 알디, 홀푸드, 월마트 등 대형 소매업체들은 이미 신규 매장의 냉장 전략을 CO₂ 트랜스크리티컬 방식 도입에 맞추어가고 있어, 해당 지역의 방향성이 더욱 명확해지고 있습니다. 남미는 체계적인 소매업의 확대와 수입된 플러그인식 유닛에 힘입어 성장하고 있는 반면, 중동은 표준 CO₂ 초임계 설계에 그다지 적합하지 않은 고온 다습한 환경 조건으로 인해 여전히 제약을 받고 있습니다. 아프리카는 콜드체인 발전 측면에서 아직 초기 단계에 있지만, 프리고글라스(Frigoglass)의 이집트 사업 확장(프레시 S.A.E.와의 제휴를 통해 연간 10만 대 생산을 목표로 하고 있음)은 이 지역의 냉장 진열장 시장에서 장기적인 성장 가능성을 시사하고 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the refrigerated display cases market size is projected to expand from USD 18.86 billion in 2025 and USD 20.48 billion in 2026 to USD 29.76 billion by 2031, registering a CAGR of 7.76% between 2026 and 2031.

This report is Segmented by Refrigeration Architecture (Plug-In, Semi Plug-In, and Remote), Product Design (Vertical, Horizontal, Hybrid, and Semi-Vertical), Application (Retail Stores, Restaurants and Hotels, and More), End User (Supermarkets and Hypermarkets, Convenience Stores, Specialty Stores, Discount Stores, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Refrigerated Display Cases Market Trends and Insights

Retail Chain Refurbishment and Convenience Store Expansion

Retail modernization programs are extending demand for refrigerated display cases beyond a typical replacement cycle. Convenience stores are allocating more floor space to prepared meals, packaged beverages, and chilled foodservice, which raises the number of cases needed in each remodeled outlet. C-store foodservice accounted for 28.5% of total in-store sales in 2025, up from 11.9% in 2005, and contributed 38.9% of in-store gross profit, underscoring why operators are redesigning stores around chilled food visibility. Love's Travel Stops committed USD 700 million in 2026 to open 20 locations and remodel 35 existing sites under its Road Ahead Plan, with a stronger food-and-beverage offer at the center of the program. In the refrigerated display cases market, that pattern matters because a food-led convenience format typically needs more linear chilled frontage than a legacy fuel-centered layout. This is keeping demand active in both new openings and store refresh work.

Natural Refrigerant and Energy-Efficiency Retrofit Cycle

The refrigerated display case market is undergoing a replacement wave driven by refrigerant rules rather than discretionary spending. Regulation (EU) 2024/573 took effect in March 2024 and tightened the phasedown path for fluorinated greenhouse gases across the European Union. In the United States, newer federal rules have pushed the sector toward lower-global-warming-potential refrigerants in new commercial refrigeration equipment, thereby shortening the replacement window for older HFC-based systems. The EPA also raised the R290 charge limit for self-contained display cases in 2024, which widened the use case for propane-based plug-in systems in larger footprints than before. Between 2025 and 2029, U.S. food retailers planned to install 1,470 new transcritical CO2 stores and replace 13,400 existing systems, which shows how large the transition pipeline has become. In the refrigerated display cases market, these compliance deadlines are serving as a floor for demand, as operators cannot indefinitely defer equipment decisions.

High Upfront Retrofit and Installation Costs

Capital costs remain a direct brake on adoption in the refrigerated display case market, especially for smaller operators. Transcritical CO2 systems can cost 10-20% more than conventional HFC systems in new builds, and retrofit projects often require additional infrastructure work, widening the gap further. That burden becomes harder to absorb when operators are also funding store remodels, energy upgrades, and refrigerant compliance in the same planning cycle. New York State awarded USD 350,000 to support 2 Bronx Key Food stores in shifting to R290 cases, demonstrating that public support is already helping smaller retailers cover the economic costs. In the refrigerated display cases market, this favors large chains that can spread transition costs across bigger store networks and longer capital programs. It also slows conversion in fragmented retail environments where stores lack scale purchasing power.

Other drivers and restraints analyzed in the detailed report include:

- Fresh, Frozen, and Grab-and-Go Food Merchandising Growth

- Smart Monitoring and Predictive Maintenance Adoption

- Energy and Lifecycle Service Cost Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plug-in refrigerated display cases held 58.37% of the market share in 2025, maintaining their position as the largest architecture segment in the refrigerated display cases market. Their lead reflects the deep installed base of self-contained units across convenience stores, bakeries, specialty retailers, and smaller grocery formats. Plug-in systems remain the default choice in many retrofit projects because they are easier to install and do not require a centralized refrigeration plant. The 2024 increase in EPA charge limits for R290 self-contained cases widened the range of store formats that propane-based plug-in units can serve, which strengthened the case for replacement in smaller and medium-sized outlets.

Remote systems are projected to grow at a 8.34% CAGR from 2026 to 2031, making them the fastest-growing architecture in the refrigerated display cases market. Growth is being driven by new supermarket builds and large remodel programs that favor centralized CO2 racks for broader temperature control and system integration. Food Lion's late-2025 remodel program in the Charlotte region included CO2-based cooling systems in select stores, which shows how large chains are pairing store renewal with refrigerant transition. Semi plug-in systems continue to occupy the middle ground, especially in European retail, where heat recovery and waterloop layouts support medium-format stores that need more flexibility than a full remote setup. The refrigerated display cases industry is therefore splitting more clearly between retrofit-friendly plug-in units and chain-led remote builds.

Vertical cases accounted for 55.12% share in 2025 and remained the core design format across the refrigerated display cases market. Their position comes from strong use in dairy, fresh food, beverage, and perimeter merchandising, where shelf visibility and broad SKU display are critical. Epta's Zenith line, launched in 2026, delivered up to 36% energy savings compared to prior models while expanding the display area by up to 13%, demonstrating how vertical cabinets improve both efficiency and sales performance. That combination helps vertical formats defend their lead as retailers look for higher productivity from existing floor space.

Hybrid configurations are projected to expand at a 8.56% CAGR through 2031, making them the fastest-growing design segment in the refrigerated display cases market. Retailers are showing more interest in mixed-display formats that can combine open and closed presentation within a single run while improving energy control. Horizontal cases continue to serve freezer chest and ice cream applications, and AHT's KIGALI XL launch in late 2024 demonstrated continued product development focused on visibility and R290-based performance in that market segment. Hybrid growth is important because it reflects retailer demand for fewer separate case lines across the store and better flexibility in category placement. In the refrigerated display case industry, design competitions are now centered less on simple form factors and more on how each cabinet layout supports both energy savings and merchandising quality.

Geography Analysis

Europe held 39.41% of the refrigerated display cases market share in 2025, making it the largest regional contributor. The region's lead reflects a dense supermarket base and an earlier move into CO2 refrigeration, supported by tighter environmental rules than in most other markets. Regulation (EU) 2024/573 strengthened the phase-out path for fluorinated greenhouse gases and is forcing operators across the European Union to bring forward system replacement plans. That policy backdrop is being reinforced by store refresh activity, including projects such as Waitrose Coulsdon's 2025 refrigeration replacement and store update, which linked system renewal with broader modernization work.

Asia-Pacific is projected to grow at a 8.73% CAGR through 2031, making it the fastest-growing region in the refrigerated display cases market. Urbanization, the expansion of convenience retail, and continued investment in cold chain infrastructure are driving broader demand across China, India, South Korea, and Southeast Asia. South Korea's convenience store base has entered a quality-upgrade phase, with operators replacing older units with inverter-based, high-efficiency display cases at conversion rates above 70%. India is also emerging as a stronger demand center, with domestic commercial refrigeration growth supported by organized retail expansion and supplier investments such as Elanpro's 2025 experience center initiative.

North America remained the second-largest regional market and a key battleground for natural refrigerant adoption in the refrigerated display cases market. The United States entered a more binding compliance phase when new federal restrictions on higher-GWP refrigerants in self-contained installations took effect in January 2025 and were further extended to remote condensing applications in January 2026. Large retailers, including Kroger, ALDI, Whole Foods, and Walmart, have already aligned their new-store refrigeration strategy with CO2 transcritical adoption, which is tightening the direction of travel for the region. South America is supported more by organized retail expansion and imported plug-in units, while the Middle East remains constrained by high ambient conditions that are less favorable to standard CO2 transcritical designs. Africa is still at an earlier stage of cold chain development, but Frigoglass's Egypt expansion, with a target of 100,000 units of annual production through its partnership with Fresh S.A.E, points to a longer-term growth position for the refrigerated display cases market in the region

- Epta S.p.A.

- Arneg S.p.A.

- ISA S.p.A.

- AHT Cooling Systems GmbH

- Metalfrio Solutions S.A.

- Frigoglass Services Single Member S.A.

- True Manufacturing Co., Inc.

- Zero Zone, Inc.

- Turbo Air Inc.

- Beverage-Air Corporation

- Structural Concepts Corporation

- Hill PHOENIX, Inc.

- TEFCOLD A/S

- Ugur Cooling Inc. Co.

- Migali Industries Inc.

- Qingdao Hiron Commercial Cold Chain Co., Ltd.

- Gram Professional ApS

- Fagor Professional, S.Coop.

- Liebherr-Hausgerate GmbH

- Hoshizaki America, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Retail Chain Refurbishment and Convenience Store Expansion

- 4.2.2 Natural Refrigerant and Energy-Efficiency Retrofit Cycle

- 4.2.3 Fresh, Frozen, and Grab-and-Go Food Merchandising Growth

- 4.2.4 Smart Monitoring and Predictive Maintenance Adoption

- 4.2.5 Omnichannel Grocery Pickup and Micro-Fulfillment Chilled Staging

- 4.2.6 Premium Fresh Food Perimeter Remodeling

- 4.3 Market Restraints

- 4.3.1 High Upfront Retrofit and Installation Costs

- 4.3.2 Energy and Lifecycle Service Cost Burden

- 4.3.3 Technician Shortage for CO2, R290, and A2L Systems

- 4.3.4 High-Ambient and Grid-Volatility Performance Risk

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Refrigeration Architecture

- 5.1.1 Plug-In

- 5.1.2 Semi Plug-In

- 5.1.3 Remote

- 5.2 By Product Design

- 5.2.1 Vertical

- 5.2.2 Horizontal

- 5.2.3 Hybrid

- 5.2.4 Semi-Vertical

- 5.3 By Application

- 5.3.1 Retail Stores

- 5.3.2 Restaurants and Hotels

- 5.3.3 Other Applications

- 5.4 By End User

- 5.4.1 Supermarkets and Hypermarkets

- 5.4.2 Convenience Stores

- 5.4.3 Specialty Stores

- 5.4.4 Discount Stores

- 5.4.5 Fuel Station Stores

- 5.4.6 Restaurants and Cafes

- 5.4.7 Bakeries

- 5.4.8 Hotels

- 5.4.9 Other End User Outlets

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Epta S.p.A.

- 6.4.2 Arneg S.p.A.

- 6.4.3 ISA S.p.A.

- 6.4.4 AHT Cooling Systems GmbH

- 6.4.5 Metalfrio Solutions S.A.

- 6.4.6 Frigoglass Services Single Member S.A.

- 6.4.7 True Manufacturing Co., Inc.

- 6.4.8 Zero Zone, Inc.

- 6.4.9 Turbo Air Inc.

- 6.4.10 Beverage-Air Corporation

- 6.4.11 Structural Concepts Corporation

- 6.4.12 Hill PHOENIX, Inc.

- 6.4.13 TEFCOLD A/S

- 6.4.14 Ugur Cooling Inc. Co.

- 6.4.15 Migali Industries Inc.

- 6.4.16 Qingdao Hiron Commercial Cold Chain Co., Ltd.

- 6.4.17 Gram Professional ApS

- 6.4.18 Fagor Professional, S.Coop.

- 6.4.19 Liebherr-Hausgerate GmbH

- 6.4.20 Hoshizaki America, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment