|

시장보고서

상품코드

2064528

제조업용 인력 관리(WFM) 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Workforce Management (WFM) In Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

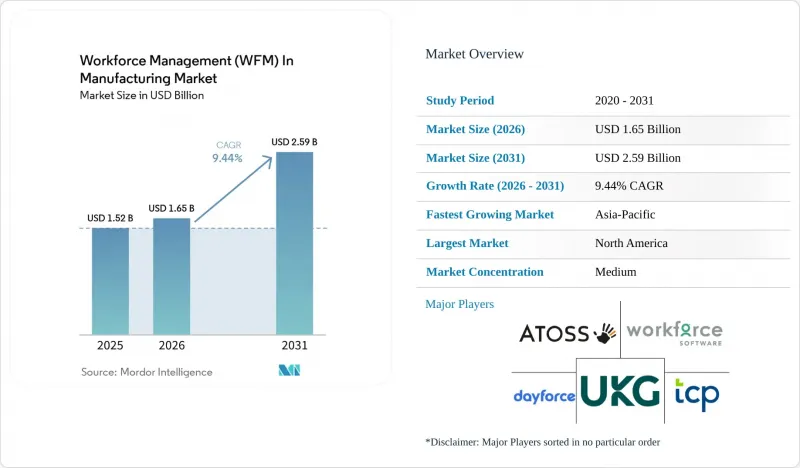

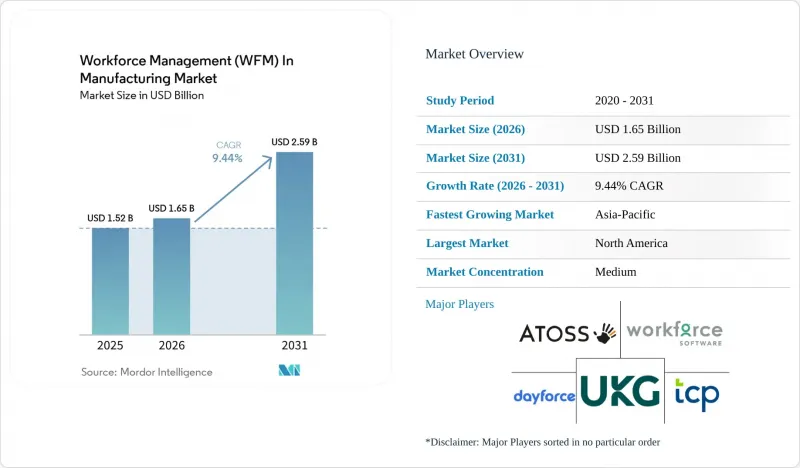

Mordor Intelligence에 의하면, 제조업용 인력 관리(WFM) 시장은 2025년에 15억 2,000만 달러로 평가되었고, 2026-2031년 CAGR 9.44%로 성장을 지속할 전망이며, 2031년에는 25억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제공 내용별(소프트웨어, 서비스), 배포 방식별(클라우드, 온프레미스, 하이브리드), 최종 사용자 기업 규모별(대기업 및 중소기업), 최종 사용자 산업별(자동차, 일렉트로믹스 및 반도체, 산업기계 및 설비 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 제조업용 인력 관리 시장 동향 및 인사이트

숙련 노동자 부족과 현장 노동력의 고령화

제조업용 인력 관리(WFM) 시장에서는 인력 부족으로 인해 인력 계획이 일상적인 생산 관리와 밀접하게 연관되어 있습니다. 제조업체들은 숙련된 인력의 장기적인 후임자 확보에 어려움을 겪고 있으며, 2033년까지 미국에서 380만 개의 일자리가 발생할 것으로 예상되는데, 그중 190만 개는 채워지지 않을 가능성이 있다는 예측이 있습니다. 이러한 압박으로 인해 중요한 직책의 후임자 확보가 어려운 상황에서는 공장이 비공식적인 스케줄링 결정에 의존할 수 없기 때문에 기술 매핑, 교대 근무 대체 현황의 가시화, 그리고 교차 교육 워크플로의 가치가 높아지고 있습니다. 제조업 분야의 인력 관리에서는 생산에 차질이 생기기 전에 누가 자격 요건을 충족하는지, 누가 근무 가능한지, 그리고 어디에 특정 기술 격차가 존재하는지 파악하기 위해 이러한 도구가 점점 더 많이 활용되고 있습니다. 이러한 필요성은 교대 근무 체제의 다층 가동에서 가장 두드러지는데, 이는 한 자리만 비어 있어도 초과근무 위험이 높아지고 생산량의 안정성이 위협받기 때문입니다. 이것이 바로 제조업의 WFM(인력 관리)이 단순한 백오피스 업무에 그치지 않고, 사업 연속성 계획, 인재 유지 전략, 공장 차원의 리스크 관리에 깊이 통합되고 있는 이유입니다.

역동적인 인력 조정이 필요한 인더스트리 4.0 프로그램

제조업용 인력 관리(WFM) 시장에서 스마트 팩토리에 대한 투자가, 기계 및 생산 신호에 실시간으로 대응할 수 있는 인력 관리 시스템에 대한 수요를 견인하고 있습니다. IIoT 데이터, 생산 라인상의 이벤트 또는 엣지 알림이 혼란을 나타낼 경우, 디지털 스케줄링 도구는 스프레드시트 기반 계획보다 더 신속하게 유능한 인력을 배치할 수 있습니다. 2025년에 발표된 조사에 따르면, 클라우드 및 엣지 인프라에서 AI를 활용한 스케줄링을 실시함으로써 산업용 모바일 기기의 충전 빈도가 최대 31.35% 감소한 것으로 나타났으며, 이는 더욱 향상된 오케스트레이션이 복잡한 생산 환경에서 시간 낭비를 어떻게 없앨 수 있는지를 입증하고 있습니다. 또한, 제조 환경에서의 실시간 인력 스케줄링을 실현하기 위해 IIoT, AI, 빅데이터, 클라우드 컴퓨팅을 기반으로 한 선구적인 공장용 인력 관리 솔루션도 출시되었습니다. 제조업용 인력 관리 시장에서 이러한 연동을 통해 인력의 가용성, 자격 인증 현황, 생산 변경 신호를 단일 운영 계층으로 통합하는 플랫폼에 대한 구매자들의 관심이 높아지고 있습니다. 또한, 많은 제조업체들이 운영 제어의 일부를 공장 근처에 유지하면서 분석 및 사용자 액세스는 클라우드에서 수행하려고 하고 있기 때문에 하이브리드 아키텍처에 대한 관심이 높아지는 것도 이를 뒷받침하고 있습니다.

기존 공장 시스템과의 통합의 어려움

제조업용 인력 관리 시장에서 통합은 여전히 도입의 가장 큰 걸림돌로 남아 있습니다. 많은 공장에서 ERP, MES 및 사내 근태 관리 시스템이 서로 연동되지 않은 채 운영되고 있기 때문입니다. 2025년 보고서에 따르면, 제조 기업의 75%가 여전히 수동 방식의 일정 수립 기법에 의존하고 있으며, 시스템 간 데이터 분절화로 인해 생산 이벤트 이후 계획이 변경될 경우 재작업 비율은 30%에 달했습니다. 이 문제로 인해 프로젝트 비용이 증가합니다. 왜냐하면 현장이 자동 스케줄링의 결과를 신뢰할 수 있게 될 때까지, 공급업체는 맞춤형 인터페이스 구축, 데이터 정제, 단계적 도입이 필요한 경우가 많기 때문입니다. 제조업용 인력 관리 시장에서 가장 어려운 환경은 대개 가장 복잡한 공장입니다. 왜냐하면 그곳에서는 최적화를 통해 얻을 수 있는 이점이 가장 큰 반면, 기술 기반의 분산화도 가장 심하기 때문입니다. 구매 기업은 급여 계산 규칙, 생산 이벤트, 기술 기록이 모든 사업장에서 통일될 때까지 광범위한 도입을 미루는 경우가 많으며, 그 결과 도입 주기가 길어지고 공급업체의 수익 창출이 지연됩니다. 이러한 제약은 제조업용 인력 관리 시장에서 서비스가 소프트웨어보다 더 빠르게 성장하고 있는 이유도 설명해 줍니다. 왜냐하면 진정한 도입 성공을 위해서는 통합 및 설정 작업이 여전히 필수적이기 때문입니다.

부문별 분석

2025년, 제조업용 인력 관리(WFM) 시장 점유율의 72.18%를 소프트웨어가 차지했으며, 공장 전체의 구매 결정 과정에서 계속해서 중심적인 위치를 차지하고 있습니다. 근태 관리는 소프트웨어 총매출의 28.31%를 차지하는 최대 하위 부문으로, 급여 계산의 감사 가능성과 출근 관리가 많은 제조업체들이 해결을 최우선 과제로 삼고 있는 과제임을 반영하고 있습니다. 제조업용 인력 관리 시장에서 이 부문은 모든 근무 교대, 모든 직원 기록, 모든 급여 계산 주기에 영향을 미치기 때문에 종종 가장 먼저 도입 자금이 배정됩니다. 초과근무 규정, 휴식 시간 추적, 피로 관련 관리 등도 규제가 엄격한 제조 환경에서 핵심적인 근태 관리 시스템의 중요성을 더욱 높이고 있습니다. 이러한 기반이 마련되면, 제조업체는 일반적으로 직원 근무표 작성, 수요 예측, 결근 관리, 인력 분석, 업무 관리, 셀프 서비스형 커뮤니케이션으로 기능을 확장합니다. 이러한 기능들은 단일한 노동 데이터 기반을 공유함으로써 더욱 효과적으로 작동하기 때문입니다.

서비스 분야는 2031년까지 연평균 성장률(CAGR) 13.12%를 나타낼 것으로 예측되며, 제조업용 인력 관리 시장에서 가장 빠르게 성장하는 서비스 유형이 될 것입니다. 이러한 성장은 구형 공장에서의 도입이 복잡하다는 점을 반영한 것입니다. 이러한 공장에서는 소프트웨어만으로는 커넥터 설계, 공장 규정 설정, 노조 운영 논리, 또는 변경 관리 요구 사항에 대응할 수 없습니다. 제조업용 인력 관리 시장에서는 소프트웨어와 제조업에 특화된 서비스 팀을 결합할 수 있는 벤더일수록 도입 위험을 줄이고 가치 실현까지 걸리는 시간을 단축할 수 있는 유리한 입장에 있습니다. 2024년 10월의 인수는 평소보다 더 세밀한 설정 지원이 필요한 데스크리스, 시급제, 노조원 및 여러 거점에 분산된 인력에 대한 대응을 강화함으로써 이 점을 뒷받침했습니다. 또한, 제조업용 인력 관리 시장에서는 단순한 서비스 환경에서만 작동하는 기초적인 도입 모델을 판매하는 것이 아니라, 제품의 기능과 공장 내 실제 운영에 부합하는 실행력을 겸비한 공급업체가 높은 평가를 받는 추세입니다.

2025년에는 클라우드 도입이 시장의 61.47%를 차지한 것으로 평가되었으며, 현재 SaaS 기반 서비스가 제조업용 인력 관리(WFM)의 신규 도입을 위한 주요 경로로 자리 잡고 있는 것으로 나타났습니다. 제조업체들이 클라우드 시스템에 매력을 느끼는 이유는 규정 준수 업데이트, 모바일 액세스, 직원의 셀프 서비스, 그리고 여러 거점에 걸친 통합 모니터링이 간소화되기 때문입니다. 2025년 상반기, 클라우드 및 구독 매출은 전년 동기 대비 30% 증가한 4,410만 유로(4,760만 달러)를 기록했으며, 소프트웨어 총매출에서 클라우드가 차지하는 비중은 12개월 동안 39%에서 48%로 상승했습니다. 이 결과는 고객들이 광범위한 엔터프라이즈 기술에 대한 지출에 신중한 태도를 유지하고 있음에도 불구하고, 지속적인 클라우드 수익의 중요성이 커지고 있음을 보여줍니다. 제조업용 인력 관리 시장에서도 클라우드는 공급업체가 지리적으로 분산된 모든 사업 거점에서 일관된 규칙, 직원용 도구 및 분석 기능을 제공할 수 있도록 지원하고 있습니다.

하이브리드 방식은 2031년까지 연평균 성장률(CAGR) 14.37%를 나타낼 것으로 예측되며, 제조업 WFM 시장의 다양한 도입 방식 중 가장 높은 성장률을 보이고 있습니다. 그 매력은 균형에 있습니다. 제조업체는 기밀성이 높은 워크플로 로직과 로컬 데이터 처리를 공장 근처에서 유지하면서, 셀프 서비스, 대시보드 및 광범위한 계획에 대한 접근에는 클라우드를 활용할 수 있습니다. 이 모델은 온프레미스 시스템을 완전히 폐지할 수는 없지만, 인력 관리와 사용자 경험을 현대화하고자 하는 공장에 적합합니다. 제조업에서 하이브리드 도입은 중요한 프로세스에 대한 현지 거버넌스를 희생하지 않으면서도 현대적인 운영 유연성을 추구하는 구매자가 나타난다는 점에서 종종 성숙 단계의 징후로 여겨집니다.

지역별 분석

2025년 기준으로 북미는 제조업용 인력 관리 시장의 39.12%를 차지했으며, 이 시장에서 가장 큰 비중을 차지하는 지역입니다. 이 지역은 노동력 부족, 엄격한 임금 및 근로시간 규제의 시행, 그리고 디지털 제조에 대한 성숙한 투자 기반의 혜택을 누리고 있습니다. 미국의 제조업은 여전히 인력 부족에 직면해 있으며, 2033년까지 380만 개의 일자리가 발생할 것으로 예상되는데, 그중 190만 개는 채워지지 않을 가능성이 있다는 예측이 있습니다. 따라서 제조업용 인력 관리(WFM) 시장은 급여 계산의 정확성뿐만 아니라, 인력 배치 계획, 교차 교육의 가시화, 그리고 초과 근무 관리 측면에서도 계속해서 중요한 역할을 수행하고 있습니다. 남미 시장은 여전히 규모가 작지만, 브라질의 자동차 산업 기반은 여전히 집중적인 수요를 창출하고 있으며, 다국적 기업의 기준에 따라 현지 공급업체들은 더욱 엄격한 일정 관리 및 노동 관리 관행을 도입하고 있습니다.

유럽은 독일, 영국, 프랑스를 필두로 제조업용 인력 관리 시장에서 구조적으로 중요한 지역으로 자리매김해 왔습니다. 2025년에는 클라우드의 성장세가 더욱 가속화되어, 2025년 상반기 클라우드 및 구독 매출은 4,410만 유로(4,760만 달러)에 달했으며, 소프트웨어 매출에서 클라우드가 차지하는 비중은 48%로 상승했습니다. 또한, 유럽의 제품 설계는 자동화된 인력 배치 의사 결정에 대한 투명성과 설명 가능성에 대한 기대가 높아짐에 따라 형성되고 있으며, 현지 규정 준수에 정통한 공급업체가 유리한 입지를 점하고 있습니다. 제조업용 인력 관리 시장에서 유럽에서는 범용적인 스케줄링 기능 세트보다 각국 고유의 노동 관련 전문 지식이나 감사에 대응할 수 있는 룰 엔진이 더 중요하게 여겨지고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 15.23%로 확대될 것으로 예상되며, 제조업용 WFM 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 이러한 성장은 중국의 공장 디지털화, 인도의 산업 확대, 그리고 일본과 한국의 인구 동학적 압박에 의해 주도되고 있습니다. 2026년 2월, 디지털 인사·근태 관리 시스템을 도입한 제조업체들은 직원 데이터 수집에서 99% 이상의 정확도를 달성했다고 보고되었으며, 이는 규정 준수 의식이 높은 일본 제조업계의 시스템 도입을 뒷받침하고 있습니다. 중국공급업체들도 혁신을 추진하고 있으며, GaiaWorks는 IIoT, AI, 빅데이터, 클라우드 컴퓨팅을 연계하여 실시간 근로 스케줄링을 실현하는 ‘라이트하우스 팩토리’용 인력 관리 솔루션을 출시했습니다. 중동 및 아프리카는 제조업용 인력 관리 시장에서 장기적인 성장 기회로 남아 있습니다. 이러한 지역에서는 도입이 공장 건설이나 산업 확장을 주도하기보다는 이에 뒤따르는 형태가 될 가능성이 높다고 볼 수 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the workforce management (WFM) market in the manufacturing industry was USD 1.52 billion in 2025 and is forecast to reach USD 2.59 billion by 2031, at a CAGR of 9.44% during 2026-2031.

This report is Segmented by Offering (Software and Services), Deployment Mode (Cloud, On-Premise, and Hybrid), End-User Enterprise Size (Large Enterprises and Small and Medium-Sized Enterprises), End-User Industry (Automotive, Electronics and Semiconductors, Industrial Machinery and Equipment, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Workforce Management (WFM) In Manufacturing Market Trends and Insights

Skilled Labor Shortages and Aging Shop-Floor Workforce

In the workforce management (WFM) in the manufacturing market, labor scarcity is pushing workforce planning closer to daily production control. Manufacturers are facing a long replacement cycle for skilled roles, and it is projected that 3.8 million positions will open in U.S. manufacturing through 2033, with 1.9 million potentially unfilled. That pressure makes skill mapping, shift coverage visibility, and cross-training workflows more valuable because plants cannot rely on informal scheduling decisions when critical roles are hard to backfill. In the workforce management in the manufacturing market, these tools are increasingly used to show who is qualified, who is available, and where single-point skill gaps sit before they disrupt production. The need is strongest in multi-shift operations where every uncovered position raises overtime risk and puts output stability under pressure. This is why the WFM in manufacturing market is being drawn deeper into continuity planning, retention efforts, and plant-level risk control, rather than remaining limited to back-office administration.

Industry 4.0 Programs Requiring Dynamic Labor Orchestratio

In the manufacturing workforce management (WFM) market, smart-factory investments are driving demand for labor systems that can respond to machine and production signals in real time. When IIoT data, line events, or edge alerts indicate a disruption, digital scheduling tools can move qualified labor faster than spreadsheet-based planning. Research published in 2025 showed that AI-driven scheduling on cloud-edge infrastructure reduced the recharging frequency of industrial mobile equipment by up to 31.35%, demonstrating how better orchestration can eliminate wasted time in complex production settings.A lighthouse factory workforce management solution was also launched, built around IIoT, AI, big data, and cloud computing for real-time labor scheduling in manufacturing environments. In the workforce management market for manufacturing, that linkage is driving buyer interest in platforms that combine labor availability, certification status, and production change signals into a single operating layer. It also supports the growing interest in hybrid architectures, as many manufacturers seek to run analytics and user access in the cloud while keeping parts of operational control close to the plant.

Legacy Plant Systems and Difficult Integrations

In the manufacturing workforce management market, integration remains the biggest barrier to adoption because many plants still operate across disconnected ERP, MES, and local attendance systems. In 2025, it was reported that 75% of manufacturing enterprises still relied on manual scheduling methods, with data fragmentation across systems leading to a 30% rework rate when plans changed after production events. That problem increases project costs because vendors often need custom interfaces, data cleanup, and staged deployments before a site can trust automated scheduling outputs. In the manufacturing workforce management market, the hardest environments are usually the most complex plants, since they offer the greatest optimization upside but also the most fragmented technology estates. Buyers often delay wider rollouts until payroll rules, production events, and skill records are aligned across sites, which lengthens implementation cycles and slows revenue conversion for vendors. This restraint also explains why services are growing faster than software in the workforce management market for manufacturing, because integration and configuration work remain essential for real deployment success.

Other drivers and restraints analyzed in the detailed report include:

- Tighter Overtime, Break, Fatigue and Payroll Compliance

- Demand for Real-Time Labor Visibility and Cost Control

- High Change-Management Burden in Unionized Multisite Plants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 72.18% of the workforce management (WFM) in manufacturing market share in 2025, keeping it at the center of purchasing decisions across factories. Time and attendance management was the largest software sub-segment at 28.31% of total software revenue, reflecting that payroll auditability and attendance control remain the first pain points many manufacturers seek to address. In workforce management in the manufacturing market, this layer is often funded first because it affects every shift, every employee record, and every payroll cycle. Overtime rules, break tracking, and fatigue-related controls have also made core time systems more important in regulated manufacturing settings. Once this base is in place, manufacturers usually expand into employee scheduling, forecasting, absence management, workforce analytics, task management, and self-service communication, as these functions work more effectively when they share a single labor data backbone.

Services are projected to grow at a 13.12% CAGR through 2031, making it the fastest-growing offering type in the workforce management in manufacturing market. That growth reflects the implementation complexity in older plants, where software alone cannot address connector design, plant-rule configuration, union logic, or change-management needs. In the workforce management in the manufacturing market, vendors that can pair software with manufacturing-specific service teams are better placed to reduce deployment risk and improve time to value. An October 2024 acquisition underlined this point by strengthening coverage for deskless, hourly, unionized, and multi-site workforces that usually require deeper configuration support. This is also where workforce management in manufacturing industry rewards providers that combine product capability with plant-ready execution rather than selling a light implementation model that works only in simpler service environments.

Cloud deployment accounted for 61.47% of the market in 2025, indicating that SaaS-based delivery is now the primary route for new workforce management (WFM) in manufacturing market rollouts. Manufacturers are drawn to cloud systems because they simplify compliance updates, mobile access, employee self-service, and centralized oversight across multiple sites. Cloud and subscription revenues grew 30% year over year to EUR 44.1 million, or USD 47.6 million, in H1 2025, while cloud's share of total software revenue increased from 39% to 48% over 12 months. That result shows that recurring cloud revenue is becoming increasingly important even as customers remain cautious about broader enterprise technology spending. In the manufacturing workforce management market, cloud also helps vendors deliver consistent rules, employee-facing tools, and analytics across geographically dispersed operations.

Hybrid deployment is projected to grow at a 14.37% CAGR through 2031, the fastest among deployment modes in the WFM in manufacturing market. Its appeal lies in balance: manufacturers can keep sensitive workflow logic or local data processing near the plant while using the cloud for self-service, dashboards, and broader planning access. This model fits plants that cannot fully retire on-premise systems but still want to modernize workforce control and user experience. In the manufacturing industry, hybrid adoption often signals a maturity phase in which buyers seek modern operating flexibility without sacrificing local governance over critical processes.

Geography Analysis

North America held 39.12% of the workforce management in manufacturing market share in 2025, making it the largest regional contributor. The region benefits from labor scarcity, strict wage-and-hour enforcement, and a mature base of digital manufacturing investment. U.S. manufacturing continues to face open roles, with projections showing that 3.8 million positions will open through 2033, and 1.9 million of those positions may remain unfilled. That keeps the workforce management (WFM) in manufacturing market relevant not only for payroll accuracy but also for coverage planning, cross-training visibility, and overtime control. South America remained smaller, but Brazil's automotive base still generated focused demand, driving multinational standards that pushed local suppliers toward stronger scheduling and labor governance practices.

Europe remained a structurally important region in the workforce management in the manufacturing market, led by Germany, the United Kingdom, and France. Strong cloud momentum was reported in 2025, with cloud and subscription revenues reaching EUR 44.1 million (USD 47.6 million) in H1 2025 and cloud's share of software revenue rising to 48%. European product design is also being shaped by tighter expectations for transparency and explainability in automated workforce decisions, favoring vendors with deeper local compliance. In the workforce management market for manufacturing, country-specific labor expertise and audit-ready rule engines are more important in Europe than a generic scheduling feature set alone.

Asia-Pacific is projected to expand at a 15.23% CAGR through 2031, making it the fastest-growing region in the WFM in manufacturing market. Growth is being driven by factory digitalization in China, industrial expansion in India, and demographic pressure in Japan and South Korea. In February 2026, it was reported that manufacturers using digital HR and attendance systems achieved more than 99% accuracy in employee data collection, which supports adoption in Japan's compliance-sensitive manufacturing base. Chinese vendors are also pushing innovation, with GaiaWorks launching a lighthouse factory workforce management solution that links IIoT, AI, big data, and cloud computing for real-time labor scheduling. The Middle East and Africa remain longer-horizon opportunities in the workforce management in the manufacturing market, where adoption is likely to follow factory build-outs and industrial expansion rather than lead them.

- UKG Inc.

- Dayforce, Inc.

- WorkForce Software, LLC

- ATOSS Software SE

- TimeClock Plus, LLC

- Humanforce Pty Ltd.

- Shiftboard, Inc.

- Deputy Corporation

- Connecteam Ltd.

- WorkJam Inc.

- SISQUAL Workforce Management, Lda.

- Worklinq A/S

- Flash Romeo Inc.

- Legion Technologies, Inc.

- Paycor HCM, Inc.

- Paylocity Holding Corporation

- isolved HCM, LLC

- Zellis UK Limited

- Ramco Systems Limited

- LumApps SAS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Skilled Labor Shortages and Aging Shop-Floor Workforce

- 4.2.2 Industry 4.0 Programs Requiring Dynamic Labor Orchestration

- 4.2.3 Tighter Overtime, Break, Fatigue and Payroll Compliance

- 4.2.4 Demand for Real-Time Labor Visibility and Cost Control

- 4.2.5 Edge and IoT-Triggered Rescheduling from Production Events

- 4.2.6 Growth of Contractor, Agency and Cross-Trained Labor Pools

- 4.3 Market Restraints

- 4.3.1 Legacy Plant Systems and Difficult Integrations

- 4.3.2 High Change-Management Burden in Unionized Multisite Plants

- 4.3.3 Data Residency and Algorithmic Transparency Limits for AI Scheduling

- 4.3.4 Weak Digital Readiness in Mid-Market Plants

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.1.1 Employee Scheduling and Labor Optimization

- 5.1.1.2 Time and Attendance Management

- 5.1.1.3 Workforce Analytics and Forecasting

- 5.1.1.4 Leave and Absence Management

- 5.1.1.5 Task and Execution Management

- 5.1.1.6 Employee Self-service and Communication

- 5.1.2 Services

- 5.1.1 Software

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Electronics and Semiconductors

- 5.4.3 Industrial Machinery and Equipment

- 5.4.4 Pharmaceuticals and Chemicals

- 5.4.5 Food and Beverage

- 5.4.6 Aerospace and Defense

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 UKG Inc.

- 6.4.2 Dayforce, Inc.

- 6.4.3 WorkForce Software, LLC

- 6.4.4 ATOSS Software SE

- 6.4.5 TimeClock Plus, LLC

- 6.4.6 Humanforce Pty Ltd.

- 6.4.7 Shiftboard, Inc.

- 6.4.8 Deputy Corporation

- 6.4.9 Connecteam Ltd.

- 6.4.10 WorkJam Inc.

- 6.4.11 SISQUAL Workforce Management, Lda.

- 6.4.12 Worklinq A/S

- 6.4.13 Flash Romeo Inc.

- 6.4.14 Legion Technologies, Inc.

- 6.4.15 Paycor HCM, Inc.

- 6.4.16 Paylocity Holding Corporation

- 6.4.17 isolved HCM, LLC

- 6.4.18 Zellis UK Limited

- 6.4.19 Ramco Systems Limited

- 6.4.20 LumApps SAS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment