|

시장보고서

상품코드

2064533

미국의 재택 의료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Home Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

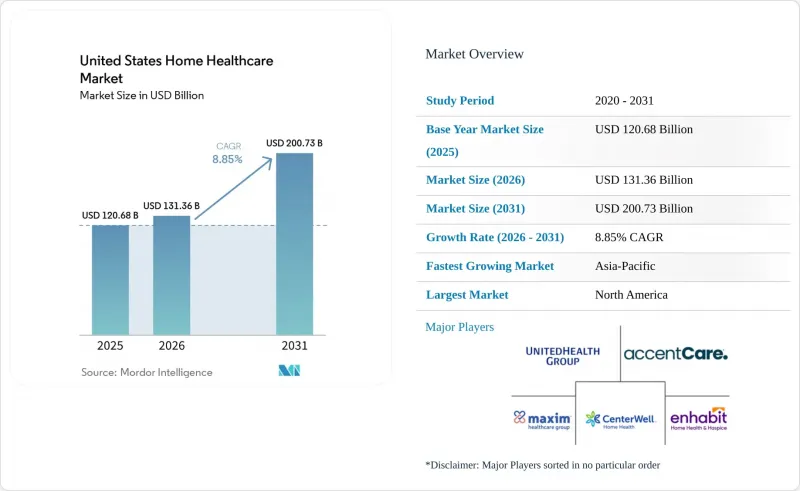

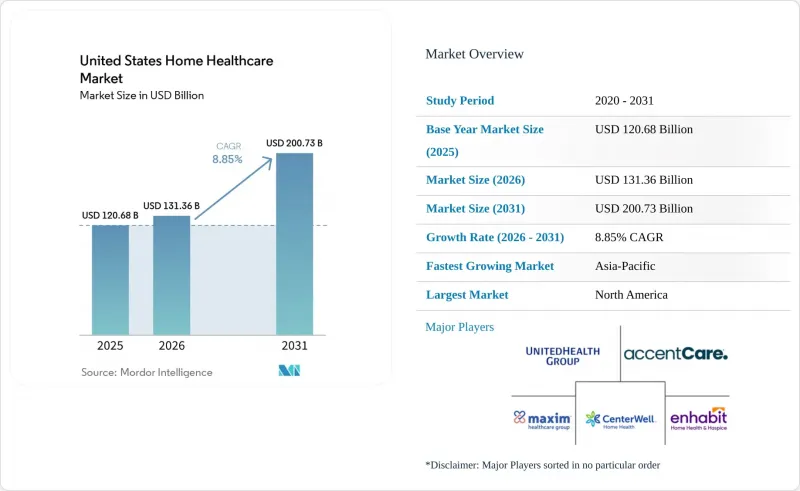

Mordor Intelligence에 의하면, 미국의 재택 의료 시장 규모는 2025년 1,206억 8,000만 달러로 평가되었습니다. 2026년에는 1,313억 6,000만 달러로 확대되어 2031년까지 2,007억 3,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 8.85%를 나타낼 전망입니다.

본 보고서는 제공 내용(기기, 서비스, 소프트웨어 플랫폼), 적응증(심혈관 질환·고혈압, 당뇨병, 호흡기 질환, 신장 질환, 암, 상처 관리, 기타 적응증) 및 지불 주체(메디케이드, 민간 보험, 본인 부담, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 재택 의료 시장 동향 및 인사이트

고령화와 다중 질환 동반으로 인한 부담

고령자는 여전히 미국의 재택 의료 시장의 주요 수요 기반이며, 이로 인해 전문 간호, 모니터링, 치료, 정맥 주사 및 개인 간호 등 각 분야에서 이 부문에 대한 지속적인 수요가 안정적으로 발생하고 있습니다. 이러한 수요 구조는 많은 소비자 주도형 의료 분야보다 더욱 견고합니다. 왜냐하면 이용은 임의 지출에 의해 좌우되는 경우가 드물고, 연령, 건강 상태, 그리고 동반된 만성 질환에 크게 좌우되기 때문입니다. 또한, 다중 질환 병존은 환자 1인당 수익성을 높입니다. 왜냐하면 심혈관 질환, 당뇨병, 신장 질환 및 운동 기능 제한은 대개 여러 가지 서비스나 기기를 동시에 필요로 하기 때문입니다. 이러한 조합을 통해 수요량을 더 쉽게 예측할 수 있게 되며, 시설 이용을 대체할 수 있는 임상적으로 관리 가능한 대안을 모색하는 지불 주체들에게 재택 간호의 매력이 높아집니다. 고령 환자층이 두터워짐에 따라, 보다 폭넓은 서비스를 제공할 수 있는 사업자는 미국의 재택 의료 시장에서 더 큰 점유율을 확보할 수 있는 입장에 있습니다.

저비용 재택 환경으로의 만성기 치료 전환

시설 내 치료와 재택 만성기 치료 간의 비용 격차는 여전히 지불 주체가 더 많은 치료를 재택으로 전환하도록 하는 강력한 이유가 되고 있습니다. 리치먼드 연방준비은행의 보고서에 따르면, 민간 요양 시설의 1인실 비용은 중앙값 기준으로 재택 간병인의 연간 비용보다 3.8배나 높습니다. 따라서 환자의 임상 상태가 안정된 경우, 재택 간호의 경제적 이점은 분명합니다. 미국 가정 정맥주사 협회(National Home Infusion Association)의 보고서에 따르면, 2025년 가정 정맥주사 청구 건수에서 면역글로불린이 가장 빠르게 성장한 분야였으며, 이러한 변화는 모든 서비스 분야에서 균등하게 일어나고 있는 것이 아니라 고부가가치의 전문 치료 분야에서 가장 두드러지게 나타나고 있는 것으로 나타났습니다. 2025년 3월에 통과된, 환자의 재택 수액 치료 접근성을 유지하기 위한 초당적 법안은 재택 치료가 이루어지는 중증 질환에 대한 보험 급여 지원이 계속해서 정책적 관심을 받고 있음을 시사합니다. 또한, CareCentrix사가 ‘Oncology at Home’ 프로그램을 확대하여 30종의 면역요법제를 포함하게 된 것은 매니지드 케어 기관이 단순히 재택 치료에 대응하는 데 그치지 않고, 재택 치료를 중심으로 한 급여 경로를 적극적으로 설계하고 있음을 보여줍니다.

숙련된 임상의 및 간병 보조원의 부족

미국의 재택 의료 시장에서 인력 확보는 여전히 운영상 가장 큰 제약 요인으로 남아 있습니다. 이는 서비스 수요가 각 기관이 안전하고 정시에 방문 직원을 배치할 수 있는 속도를 넘어서는 속도로 증가할 가능성이 있기 때문입니다. Homecare Homebase의 보고서에 따르면, 2024년에는 420만 명 이상의 환자가 인력 및 운영 능력의 제약으로 인해 의사가 권장하는 재택 의료 서비스를 받지 못했습니다. 이 소식통은 또한 재택 의료 및 개인 간병 보조원에 대한 수요가 향후 몇 년 동안 계속 증가할 것으로 예상된다고 강조했으며, 이는 접근성 문제가 당분간 완화될 기미가 보이지 않는다는 것을 의미합니다. 행정 업무의 부담이 효율적인 인력 배치 능력을 더욱 저해하고 있으며, KFF의 조사에 따르면 메디케어 어드밴티지의 급성기 후 서비스 전반에 걸쳐 사전 승인이 여전히 큰 운영상의 부담으로 작용하고 있는 것으로 나타났습니다. 이러한 상황은 이동 시간, 임금 경쟁, 업무 처리 부담 등이 모두 복합적으로 작용하여, 소개받은 환자에게 적시에 치료를 시작하기 어려운 지방이나 인구 밀도가 높은 도시 지역 시장에서 특히 심각한 영향을 미치고 있습니다.

부문별 분석

2025년 기준으로 서비스 부문은 미국의 재택 의료 시장 점유율의 52.31%를 차지했으며, 총 매출 측면에서 기기 및 소프트웨어 부문을 확실히 앞질렀습니다. 이러한 지침은 재택에서 제공되는 전문 간호, 치료, 호스피스, 개인 간호, 재택 정맥 주사 요법이 지속적이고 노동 집약적인 특성을 지닌다는 점을 반영하고 있습니다. 숙련된 간호는 급성기 이후의 전환 지원, 약물 관리, 만성 질환 관리, 그리고 환자와의 장기적인 지속적인 접촉을 뒷받침하기 위해 여전히 핵심적인 서비스로 자리 잡고 있습니다. 재활 치료 역시 ‘재택 병원(Hospital-at-Home)’ 및 ‘재택 급성기 후 관리(Post-acute-at-Home)’ 프로그램의 확대에 힘입어 혜택을 보고 있습니다. 이러한 프로그램 덕분에 급성기를 벗어난 환자나 여전히 재활 치료나 재택 경과 관찰이 필요한 환자가 증가하고 있습니다.

의료기기 분야는 CPAP 및 BiPAP 장치, 재택 투석 시스템, 원격 다중 항목 모니터, 지속 혈당 모니터에 대한 수요 증가에 힘입어, 2026년부터 2031년까지 연평균 성장률(CAGR) 9.38%를 기록하며 미국의 재택 의료 시장에서 가장 빠른 성장세를 보일 것으로 전망됩니다. 보험사와 의료 제공업체 양측 모두 재택 조기 개입 및 병원 밖에서의 실시간 환자 데이터 수집에 대한 인센티브를 강화하고 있어 수요가 증가하고 있습니다. 2025년 1월, CMS가 급성 신장 손상에 대한 재택 투석의 메디케어 적용 범위를 확대함에 따라, 신장 치료에 필요한 기기 도입을 지원하는 직접 상환의 길이 열렸습니다. 소프트웨어는 여전히 가장 규모가 작은 제품 유형이지만, 미국의 재택 의료 업계에서 의료 기관들이 보다 적절한 기록 관리, 의뢰 자동화, 입원 위험 예측 및 수익 주기 관리를 요구함에 따라 그 전략적 중요성이 커지고 있습니다. WellSky사가 2025년과 2026년에 출시할 AI를 활용한 초진 대응, 투약 관리, 환경 기록 및 개인 간호 요약 관련 제품들은 미국의 재택 의료 시장에서 디지털 도구가 지원 기능에서 운영 인프라로 전환되고 있음을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the united states home healthcare market size is expected to increase from USD 120.68 billion in 2025 to USD 131.36 billion in 2026 and reach USD 200.73 billion by 2031, growing at a CAGR of 8.85% over 2026-2031.

This report is Segmented by Offering (Equipment, Services, Software Platforms), Indication (Cardiovascular Disorders & Hypertension, Diabetes, Respiratory Diseases, Renal Disorders, Cancer, Wound Care, Other Indications), and Payer (Medicaid, Commercial/Private Insurance, Self-pay/Out-of-pocket, Others). The Market Forecasts are Provided in Terms of Value (USD).

United States Home Healthcare Market Trends and Insights

Aging Population and Multi-Morbidity Burden

Older adults remain the core demand base for the United States home healthcare market, which gives the sector a steady flow of recurring need across skilled nursing, monitoring, therapy, infusion, and personal care. This demand profile is stronger than in many consumer-led healthcare categories because utilization is tied less to discretionary spending and more to age, frailty, and coexisting chronic conditions. Multi-morbidity also raises revenue intensity per patient because cardiovascular disease, diabetes, renal disease, and mobility limits often need several services and devices at the same time. That combination makes volume more predictable and makes home-based care more attractive to payers looking for clinically manageable alternatives to facility use. As the older patient pool deepens, providers with broader service breadth are better positioned to capture a larger share of the United States home healthcare market.

Chronic-Care Migration to Lower-Cost Home Settings

The cost gap between institutional and home-based chronic care remains a powerful reason for payers to move more treatment into the home. The Federal Reserve Bank of Richmond reported that a private nursing-home room costs 3.8 times the annual cost of a home health aide at median rates, which keeps the economic case for home-based care clear when patients are clinically stable. The National Home Infusion Association reported that immune globulins were the fastest-growing category in home infusion claims during 2025, which shows that migration is strongest in higher-value specialty therapy rather than in every service line equally. March 2025 bipartisan legislation to preserve patient access to home infusion signaled that reimbursement support for serious home-treated conditions continues to draw policy attention. CareCentrix's expansion of Oncology at Home to include 30 immunotherapy drugs also showed that managed care organizations are actively designing benefit pathways around treatment at home rather than simply responding to it.

Skilled Clinician and Aide Shortages

Workforce availability remains the hardest operating constraint in the United States home healthcare market because service demand can rise faster than agencies can staff visits safely and on time. Homecare Homebase reported that more than 4.2 million patients in 2024 did not receive physician-recommended home health services because of workforce and operational capacity constraints. The same source also highlighted that demand for home health and personal care aides is expected to keep increasing for years, which means access pressure is not likely to ease quickly. Administrative workload further reduces effective staffing capacity, and KFF has shown that prior authorization remains a heavy operational burden across post-acute services in Medicare Advantage. These conditions are especially damaging in rural and high-density urban markets where travel time, wage competition, and paperwork all make it harder to convert referrals into timely starts of care.

Other drivers and restraints analyzed in the detailed report include:

- Telehealth and Remote Monitoring Reimbursement Support

- Hospital-at-Home and Post-Acute-at-Home Adoption

- PDGM-Related Reimbursement Pressure and Rate Uncertainty

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services held 52.31% of the United States home healthcare market share in 2025, which kept them clearly ahead of equipment and software in total revenue. That lead reflects the recurring and labor-intensive nature of skilled nursing, therapy, hospice, personal care, and home infusion delivered in the residence. Skilled nursing remains the central service because it supports post-acute transitions, medication oversight, chronic disease management, and repeated patient contact over time. Therapy is also benefiting from the expansion of hospital-at-home and post-acute-at-home programs, which create more patients who leave acute episodes but still need rehabilitation and home follow-up.

Equipment is projected to record the fastest growth in the United States home healthcare market size at a 9.38% CAGR from 2026 to 2031, supported by rising demand for CPAP and BiPAP devices, home dialysis systems, remote multi-parameter monitors, and continuous glucose monitors. Demand is strengthening because payers and providers both have stronger incentives to intervene earlier at home and to generate more real-time patient data outside the hospital. CMS's January 2025 expansion of Medicare coverage for home dialysis in acute kidney injury added a direct reimbursement pathway that supports equipment uptake in renal care. Software remains the smallest offering type, yet it is becoming more strategic as agencies seek better documentation, referral automation, hospitalization-risk prediction, and revenue cycle control within the United States home healthcare industry. WellSky's 2025 and 2026 product releases in AI-enabled intake, medication reconciliation, ambient documentation, and personal care summarization show that digital tools are moving from support functions to operating infrastructure in the United States home healthcare market.

List of Companies Covered in this Report:

- Abbott Laboratories

- AdaptHealth Corp.

- Amedisys (UnitedHealth Group)

- Baxter

- BAYADA Home Health Care

- CareCentrix Inc.

- CenterWell Home Health

- Coloplast

- Drive DeVilbiss Healthcare

- Enhabit Inc.

- Fresenius

- GE HealthCare Technologies Inc.

- Home Instead Inc.

- Homecare Homebase

- Honor Technology

- Koninklijke Philips

- Medtronic

- OMRON Healthcare, Inc.

- Resmed

- Sunrise Medical

- WellSky Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population and Multi-Morbidity Burden

- 4.2.2 Chronic-Care Migration to Lower-Cost Home Settings

- 4.2.3 Telehealth And Remote Monitoring Reimbursement Support

- 4.2.4 Hospital-At-Home and Post-Acute-At-Home Adoption

- 4.2.5 Home Dialysis Coverage Expansion for AKI Patients

- 4.2.6 Home-Administered Immunotherapy and Specialty Infusion Migration

- 4.3 Market Restraints

- 4.3.1 Skilled Clinician and Aide Shortages

- 4.3.2 PDGM-Related Reimbursement Pressure and Rate Uncertainty

- 4.3.3 Smart-Home IoT Cybersecurity and HIPAA Compliance Burden

- 4.3.4 Fragmented Referral-To-Start-Of-Care Workflows

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Offering

- 5.1.1 Equipment

- 5.1.1.1 Therapeutic Equipment

- 5.1.1.1.1 Insulin Delivery Devices

- 5.1.1.1.2 Home IV Pumps & Infusion Equipment

- 5.1.1.1.3 Home Dialysis Equipment

- 5.1.1.1.4 Ventilators & Nebulizers

- 5.1.1.1.5 CPAP & BiPAP Devices

- 5.1.1.1.6 Compression & Wound Therapy Equipment

- 5.1.1.2 Diagnostic & Monitoring Equipment

- 5.1.1.2.1 Blood-Glucose Monitors & CGM

- 5.1.1.2.2 Blood Pressure Monitors

- 5.1.1.2.3 Pulse Oximeters

- 5.1.1.2.4 ECG & Holter Monitors

- 5.1.1.2.5 Digital Thermometers

- 5.1.1.2.6 Multi-parameter Remote Monitoring Devices

- 5.1.1.3 Mobility & Daily Living Assist Equipment

- 5.1.1.3.1 Wheelchairs

- 5.1.1.3.2 Walkers & Rollators

- 5.1.1.3.3 Mobility Scooters

- 5.1.1.3.4 Patient Lifts & Transfer Aids

- 5.1.1.3.5 Home Medical Furniture & Safety Aids

- 5.1.1.1 Therapeutic Equipment

- 5.1.2 Services

- 5.1.2.1 Skilled Nursing

- 5.1.2.2 Physical Therapy

- 5.1.2.3 Occupational Therapy

- 5.1.2.4 Speech Therapy

- 5.1.2.5 Hospice & Palliative Care

- 5.1.2.6 Personal Care / Home Health Aide Services

- 5.1.2.7 Respiratory Therapy

- 5.1.2.8 Home Infusion Services

- 5.1.2.9 Tele-homecare / Virtual Care Coordination

- 5.1.3 Software Platforms

- 5.1.3.1 Agency Management & Scheduling

- 5.1.3.2 Clinical / EHR Platforms

- 5.1.3.3 Remote Patient Monitoring Platforms

- 5.1.3.4 Revenue Cycle & Referral Management

- 5.1.1 Equipment

- 5.2 By Indication

- 5.2.1 Cardiovascular Disorders & Hypertension

- 5.2.2 Diabetes

- 5.2.3 Respiratory Diseases

- 5.2.4 Renal Disorders

- 5.2.5 Cancer

- 5.2.6 Wound Care

- 5.2.7 Other Indications

- 5.3 By Payer

- 5.3.1 Medicare

- 5.3.2 Medicaid

- 5.3.3 Commercial / Private Insurance

- 5.3.4 Self-pay / Out-of-pocket

- 5.3.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 AdaptHealth Corp.

- 6.3.3 Amedisys (UnitedHealth Group)

- 6.3.4 Baxter International Inc.

- 6.3.5 BAYADA Home Health Care

- 6.3.6 CareCentrix Inc.

- 6.3.7 CenterWell Home Health

- 6.3.8 Coloplast A/S

- 6.3.9 Drive DeVilbiss Healthcare

- 6.3.10 Enhabit Inc.

- 6.3.11 Fresenius Medical Care AG & Co. KGaA

- 6.3.12 GE HealthCare Technologies Inc.

- 6.3.13 Home Instead Inc.

- 6.3.14 Homecare Homebase

- 6.3.15 Honor Technology Inc.

- 6.3.16 Koninklijke Philips N.V.

- 6.3.17 Medtronic plc

- 6.3.18 OMRON Healthcare, Inc.

- 6.3.19 ResMed Inc.

- 6.3.20 Sunrise Medical LLC

- 6.3.21 WellSky Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment