|

시장보고서

상품코드

2064534

미국의 호스피스 케어 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)United States Hospice Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

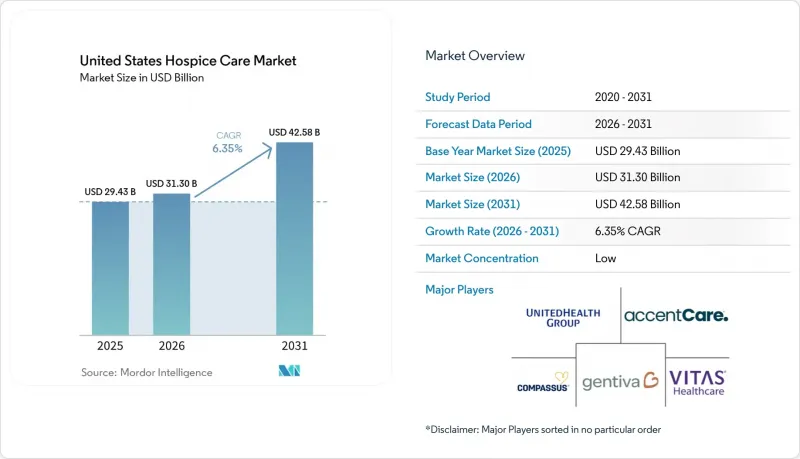

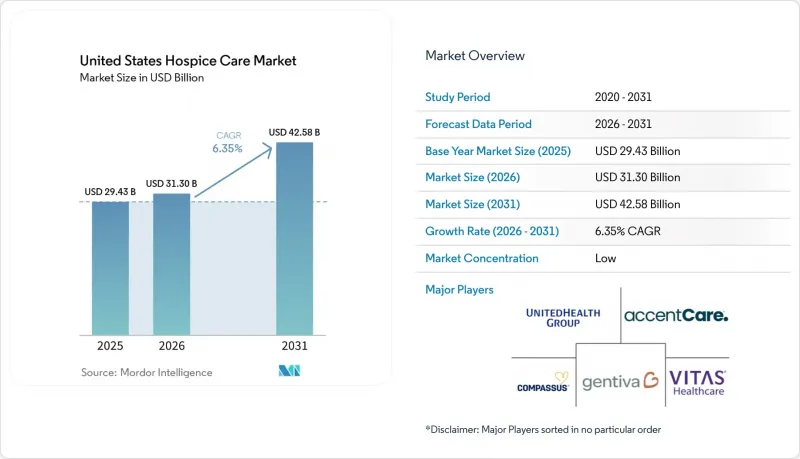

Mordor Intelligence에 의하면, 미국의 호스피스 케어 시장 규모는 2025년에 294억 3,000만 달러로 평가되었고, 2026년에 313억 달러로 추정되고, 2031년까지 425억 8,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 6.35%로 성장할 전망입니다.

본 보고서는 돌봄 수준별(일상 돌봄, 지속적 돌봄, 일반 입원 치료, 입원형 임시 돌봄), 돌봄 환경별(호스피스 센터, 재택 호스피스, 병원, 특별양로원), 환자 진단별(치매 및 알츠하이머병, 순환기·심부전, 암, 호흡기 질환, 뇌졸중·신경혈관 질환, 만성 신장병, 기타), 보험자별(메디케어, 메디케이드, 민간 보험, 본인 부담)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

미국의 호스피스 케어 시장 동향 및 인사이트

고령화와 다중 질환 병존

미국의 호스피스 케어 시장은 고령 인구 증가에 힘입어 지속적인 성장을 이어가고 있으며, 65세 이상 미국인의 수는 2026년까지 6,500만 명에 달할 것으로 전망됩니다. 메디케어 수급자 중 호스피스 서비스를 이용한 비율은 2024년에 52.9%에 달했으며, 전년 대비 1.2포인트 상승했습니다. 이는 호스피스가 주류 돌봄 경로가 된 이후에도 그 보급률이 여전히 상승하고 있음을 보여줍니다. 다중 질환의 병존 또한 치료 과정의 경제성에 변화를 주고 있습니다. 2024년, 신경계 질환을 앓고 있는 환자의 호스피스 이용 일수는 평균 169일인 반면, 암 환자의 경우 평균 51일에 그쳤으며, 이로 인해 보다 복잡한 증상 양상을 관리할 수 있는 의료 제공업체들에게는 수익 구조에 실질적인 차이가 발생하고 있습니다. 이러한 격차는 치매 환자들에게서도 두드러지게 나타나는데, 치매 진단을 받은 메디케어 수급자의 43%가 호스피스 케어을 이용하고 있는 반면, 치매가 없는 수급자의 경우 45.4%에 달할 전망입니다. 이러한 점에서 대상을 좁힌 아웃리치 활동이나 조기 연계 경로를 구축할 여지가 남아 있습니다. 말기 신장 질환 수급자의 호스피스 이용률은 2024년에 31.4%를 나타낼 것으로 보이며, 미국의 연간 사망자 수는 2037년까지 360만 명을 넘어설 것으로 예측됩니다. 이에 따라 예측 기간 동안 미국 호스피스 케어 시장 수요 기반은 구조적으로 견조한 추세를 보일 것으로 전망됩니다.

재택 호스피스에 대한 관심

미국의 호스피스 케어 시장은 재택 서비스로 더욱 전환되고 있으며, 2024년에는 전체 호스피스 청구 건수의 56%가 환자의 자택에서 이루어진 반면, 병원 기반 호스피스 입원 건수는 전체 청구 건수의 3%로 감소했습니다. 이러한 변화는 운영상 중요한 의미를 지닙니다. 왜냐하면 재택 호스피스의 성장은 병상 수 증가에 의존하기보다는 환자의 거주지 주변에서의 신속한 입원 절차, 인력 간의 연계, 그리고 의뢰 건수 증가에 크게 좌우되기 때문입니다. 재택 호스피스 케어는 2031년까지 연평균 성장률(CAGR) 9.52%로 확대될 것으로 예상되며, 이는 미국 호스피스 케어 시장에서 가장 빠르게 성장하는 케어 환경이 될 것입니다. 원격 모니터링, 원격 의료를 통한 분류, 그리고 간병인과의 보다 긴밀한 소통을 재택 모델에 접목하는 의료 서비스 제공업체는 고정 인프라나 시설 운영 비용을 그만큼 늘리지 않고도 더 많은 환자를 수용할 수 있게 됩니다. 그 결과, 특히 시설 선택의 폭이 좁은 교외나 지방에서는 광범위한 소개 네트워크와 유연한 현장 운영을 결합할 수 있는 플랫폼이 점점 더 유리한 환경을 조성하고 있습니다.

본인 부담금 및 지급 상한액

미국의 호스피스 케어 시장에서는 표준 메디케어 호스피스 급여 대상에서 제외된 환자 부담으로 인한 마찰이 여전히 존재하고 있습니다. 보험에 가입하지 않았거나 급여 대상에서 제외된 서비스의 경우, 돌봄의 강도에 따라 다르지만 1일당 150달러에서 500달러의 비용이 발생할 수 있습니다. 더 근본적인 문제는 메디케어의 총액 상한선에 있습니다. 2023 회계연도에 호스피스 기관의 28%가 상한선을 초과했으며, 상한선을 초과한 제공기관의 평균 초과 지급액은 41만 달러에 달했기 때문입니다. 이러한 위험은 독립형 및 영리 기관에 집중되어 있습니다. 이들은 전체 호스피스 제공업체의 82%를 차지하는 반면, 메디케어 호스피스 환자의 60%를 수용하고 있어, 제공업체 구성과 환자 구성 사이에 불일치가 나타납니다. 이는 장기 입원 환자나 중증도가 낮은 환자에 크게 의존하고 있는 의료 제공업체들에게 부담이 됩니다. 왜냐하면, 수익 성장을 뒷받침하는 바로 그 사례 구성이 환급 위험이나 감사 강화로 이어질 가능성도 있기 때문입니다. MedPAC이 2027 회계연도 지급률 갱신을 폐지할 것을 권고한 것은 표면상으로는 현재의 수익성이 여전히 양호함에도 불구하고, 미국 호스피스 케어 시장의 향후 계획에 더 큰 불확실성을 더하고 있습니다.

부문별 분석

2025년 기준으로 일상적인 재택 간호는 미국 호스피스 간호 시장의 89.31%를 차지했으며, 이는 해당 급여 제도가 여전히 단기 시설 입소가 아닌 재택에서의 일상적인 서비스 모델을 중심으로 압도적으로 구성되어 있음을 뒷받침하고 있습니다. 이러한 우위는 메디케어의 설계에 의해 더욱 강화되었으며, 루틴 홈케어는 메디케어 대상 호스피스 이용 일수의 98.8%를 차지하고 있어 미국 호스피스 케어 업계의 재정적·운영적 중심이 되고 있습니다. CMS는 2026 회계연도의 정기 재택 간호 보수율을 1일째부터 60일째까지는 1일당 230.83달러, 61일째부터는 1일당 181.94달러로 책정했습니다. 이를 통해 장기 체류를 전제로 한 제공업체의 행동을 유도하는 단계별 지불 구조가 유지되고 있습니다. 이 수준의 간병 규모는 진단 구성에 사소한 변화만 생겨도 인력 배치에 대한 부담을 재조정해야 할 수 있음을 의미합니다. 왜냐하면 순환기계, 호흡기계, 신경계 환자들은 기존의 암 환자 집단에 비해 증상에 더 자주 대처해야 하는 경우가 많기 때문입니다. 그 결과, 서비스 제공업체는 기본적인 대응책으로 입원으로의 전환에 의존하기보다는 주요 서비스 계층 내에서 돌봄 조정, 간호사 근무표 편성, 요양보호사 배치를 조정해야 하는 상황에 놓이게 되었습니다.

지속적 재택 간호 시장은 2031년까지 연평균 성장률(CAGR) 9.38%를 나타낼 것으로 예측되며, 급성 증상이 나타나는 위기 상황에서도 집에서 지내는 환자가 늘어남에 따라 미국 호스피스 간호 시장에서 가장 빠르게 성장하고 있는 간호 수준이 되고 있습니다. CMS는 2026 회계연도의 지속적 재택 간호 요금을 24시간 간호당 1,674.29 달러로 책정했습니다. 이는 이 고급성기 중재에 수반되는 고도의 치료 강도를 반영한 것입니다. 이러한 수준의 증상은 중증 심부전, 말기 치매, 그리고 숙련된 간병이 충분히 신속하게 제공된다면 집에서 증상의 급격한 악화를 관리할 수 있는 기타 질환들과 밀접한 관련이 있습니다. 일반 입원 돌봄 및 입원 임시 돌봄은 특히 돌봄 제공업체의 부담이 커지거나 재택 관리가 제대로 이루어지지 않을 때 여전히 필수적인 안전망으로서의 역할을 수행하고 있지만, 총 이용 일수 및 수익에서 차지하는 비중은 여전히 상당히 낮은 수준입니다. 호스피스 품질 보고 프로그램의 일환으로 2025년 10월에 도입된 HOPE 평가 도구는 운영 측면의 규율을 한층 더 강화하는 것입니다. 요건을 충족하지 못할 경우 연간 지급액의 4%가 삭감될 가능성이 있으므로, 규정 준수 대응 능력이 제한적인 소규모 사업자에게는 더 큰 부담이 되기 때문입니다.

2025년 기준으로 호스피스 센터는 미국 호스피스 케어 시장의 61.24%를 차지했으며, 재택 모델이 확대되고 있음에도 불구하고 독립형 및 집중 치료 시설이 여전히 서비스 제공에서 가장 큰 비중을 차지하고 있는 것으로 나타났습니다. 시설 집중형은 역사적으로 더 강력한 감독 체계, 더 예측 가능한 인력 배치, 그리고 더 용이한 일정 관리를 제공해 왔습니다. 이것이 전용 센터가 시설 구성에서 가장 중요한 위치를 차지하고 있는 이유를 설명해 줍니다. RIHC 호스피스 케어 차트북에 따르면, 2024년 입원형 호스피스의 평균 입원 일수는 11일, 중앙값은 4일인 것으로 나타났으며, 시설 기반 케어가 여전히 케어의 최종 단계이자 보다 집중적인 단계에 집중되어 있음이 확인되었습니다. 제공업체 기반도 이러한 경향을 뒷받침하고 있습니다. 2026년에는 영리 목적의 독립형 호스피스가 전체 제공업체의 82%를 차지하고 있으며, 인력 배치, 기록 관리, 이익률 관리를 보다 엄격하게 감독할 수 있는 시설 형태에 활동을 계속 집중하고 있기 때문입니다. 그렇긴 하지만, 환자와 가족의 희망이 기존의 전용 호스피스 센터 기반보다 더 빠르게 변화하고 있기 때문에 서비스 제공 방식의 구성은 더 이상 정적인 것이 아닙니다.

재택 호스피스 케어는 2031년까지 연평균 성장률(CAGR) 9.52%로 확대될 것으로 예상되며, 케어가 시설 중심에서 환자에게 밀착된 형태로 전환됨에 따라 미국 호스피스 케어 시장에서 가장 빠르게 성장하고 있는 제공 형태로 자리 잡고 있습니다. 2024년까지 호스피스 청구 건수의 56%가 환자의 자택에서 이루어졌으며, 요양 주택이 21%를 추가로 차지하고 있는데, 이는 호스피스 케어의 상당 부분이 이미 병원 밖을 거점으로 하고 있음을 보여줍니다. 이러한 의료 제공 형태의 구성에서 병원의 비중은 꾸준히 감소하고 있으며, 2024년에는 병원 기반 호스피스 입원 건수가 청구 건수의 불과 3%에 그쳤고, 병원 기반 의료 제공업체 수는 2023년부터 2024년에 걸쳐 4.1% 감소했습니다. 이러한 전환을 통해 분산된 현장 팀을 운영하고, 근무 시간 외에도 확실한 대응을 유지하며, 증상이 입원을 요하는 상황으로 발전하기 전에 원격 분류 시스템을 활용해 지원할 수 있는 사업자가 강점을 발휘하게 될 것입니다. 시간이 지남에 따라, 이로 인해 재택 간호 역량은 단순한 부가 서비스가 아니라 미국 호스피스 간호 시장에서 핵심적인 경쟁 요건이 될 것입니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the united states hospice care market size is projected to be USD 29.43 billion in 2025, USD 31.30 billion in 2026, and reach USD 42.58 billion by 2031, growing at a CAGR of 6.35% from 2026 to 2031.

This report is Segmented by Level of Care (Routine, Continuous, General Inpatient, Inpatient Respite), Care Setting (Hospice Centers, Home Hospice, Hospitals, Snfs), Patient Diagnosis (Dementia/Alzheimer's, Circulatory/Heart Failure, Cancer, Respiratory, Stroke/Neurovascular, CKD, Other), and Payer (Medicare, Medicaid, Private Insurance, OOP). The Market Forecasts are Provided in Terms of Value (USD).

United States Hospice Care Market Trends and Insights

Aging Population and Multi-Morbidity

The US hospice care market continues to draw long-range support from the expanding older population, with the number of Americans aged 65 and over projected to reach 65 million by 2026. Hospice use among Medicare decedents reached 52.9% in 2024, up by 1.2 percentage points from the prior year, which shows that penetration is still rising even after hospice became a mainstream care pathway. Multi-morbidity is also changing episode economics, because patients with neurological conditions averaged 169 hospice days in 2024, while cancer patients averaged 51 days, creating a materially different revenue profile for providers that can manage more complex symptom patterns. The gap remains meaningful in dementia, where 43% of Medicare beneficiaries diagnosed with dementia used hospice care, versus 45.4% for beneficiaries without dementia, leaving room for targeted outreach and earlier referral pathways. Hospice utilization among beneficiaries with end-stage renal disease reached 31.4% in 2024, and annual US deaths are projected to exceed 3.6 million by 2037, which keeps the demand base for the US hospice care market structurally durable over the forecast period.

Home-Based Hospice Preference

The US hospice care market is being pulled further toward home delivery, with 56% of all hospice claims provided at the patient's residence in 2024, while hospital-based hospice stays fell to 3% of all claims. This shift matters operationally because home hospice growth depends less on adding beds and more on improving admissions velocity, workforce coordination, and referral density around the patient's place of residence. Home Hospice Care is projected to expand at a 9.52% CAGR through 2031, which makes it the fastest-growing care setting in the US hospice care market. Providers that layer remote monitoring, telehealth triage, and stronger caregiver communication into the home model can absorb more admissions without a matching increase in fixed infrastructure or facility overhead. The result is a setting mix that increasingly favors platforms able to combine broad referral reach with flexible field operations, especially in suburban and rural territories where facility alternatives remain limited.

Out-of-Pocket Burden and Payment Caps

The US hospice care market still faces friction from direct patient costs outside the standard Medicare hospice benefit, where uninsured or uncovered services can cost USD 150 to USD 500 per day depending on care intensity. The more persistent pressure point sits with the Medicare aggregate cap, because 28% of hospices exceeded the cap in FY 2023 and average excess payments among above-cap providers reached USD 410,000. Exposure is concentrated among freestanding and for-profit agencies, which represent 82% of all hospice providers but served 60% of Medicare hospice patients, showing a mismatch between provider composition and patient mix. This creates pressure for providers that depend heavily on long-stay and lower-acuity patients, because the same case mix that supports revenue growth can also trigger repayment risk and tighter audit attention. MedPAC's recommendation to eliminate the FY 2027 payment rate update adds another layer of uncertainty to forward planning in the US hospice care market, even though current margins still appear favorable on paper.

Other drivers and restraints analyzed in the detailed report include:

- Medicare and Payer Reimbursement Support

- AI-Enabled Referral Analytics

- Workforce Shortages and RN Turnover

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Routine Home Care held 89.31% of the US hospice care market in 2025, which confirms that the benefit is still overwhelmingly built around a home-based daily service model rather than short institutional episodes. Its dominance is reinforced by Medicare design, because Routine Home Care accounted for 98.8% of all Medicare-covered hospice days, making it the financial and operational center of the US hospice care industry. CMS set the FY 2026 Routine Home Care rate at USD 230.83 per day for days 1 to 60 and USD 181.94 per day for day 61 onward, preserving the stepped payment structure that shapes provider behavior around longer stays. The scale of this level of care means even small shifts in diagnosis mix can reshape staffing burden, because circulatory, respiratory, and neurological patients often require more frequent symptom response than the historical cancer cohort. As a result, providers are being pushed to adjust care coordination, nurse scheduling, and aide coverage within the dominant service tier rather than relying on inpatient escalation as the default response.

Continuous Home Care is projected to grow at a 9.38% CAGR through 2031, making it the fastest-growing level of care in the US hospice care market as more patients remain at home during acute symptom crises. CMS set the FY 2026 Continuous Home Care rate at USD 1,674.29 for 24 hours of care, which reflects the premium intensity attached to this higher-acuity intervention. Growth in this level is tied closely to advanced heart failure, late-stage dementia, and other conditions where symptom spikes can be managed at home if skilled coverage is available quickly enough. General Inpatient Care and Inpatient Respite Care still remain necessary backstop services, especially when caregiver burden rises or home management fails, but they continue to represent a much smaller share of total days and revenue. The HOPE assessment tool, implemented in October 2025 under the Hospice Quality Reporting Program, adds another layer of operational discipline because missed requirements can trigger a 4% annual payment reduction, which weighs more heavily on smaller providers with thinner compliance capacity.

Hospice Centers held 61.24% of the US hospice care market in 2025, showing that freestanding and concentrated care settings still command the largest share of service delivery even as the home model expands. Facility concentration has historically offered stronger supervision, more predictable staffing, and easier scheduling control, which explains why dedicated centers retained the largest position in the setting mix. The RIHC Hospice Care Chartbook reported that inpatient hospice generated an average stay of 11 days and a median stay of 4 days in 2024, confirming that facility-based care remains concentrated in the final and more intensive phase of care. The provider base also supports this pattern, because for-profit freestanding hospices represented 82% of all providers in 2026 and continue to concentrate activity in settings where staffing, documentation, and margin management can be monitored more tightly. Even so, the setting mix is no longer static, because patient and family preferences are shifting faster than the installed base of dedicated hospice centers.

Home Hospice Care is forecast to grow at a 9.52% CAGR through 2031, making it the fastest-rising setting in the US hospice care market as care increasingly follows the patient rather than the facility. By 2024, 56% of all hospice claims were delivered at the patient's residence, and assisted living facilities accounted for another 21%, which shows that most hospice episodes are already anchored outside hospitals. Hospitals are steadily losing relevance in this setting mix, with hospital-based hospice stays accounting for only 3% of claims in 2024 and hospital-based provider count falling 4.1% between 2023 and 2024. This transition strengthens operators that can run distributed field teams, maintain reliable after-hours response, and use remote triage to support symptoms before they become inpatient events. Over time, that makes home capability less of an add-on service and more of a core competitive requirement inside the US hospice care market.

List of Companies Covered in this Report:

- AccentCare

- Agape Care Group / ACG Hospice

- Amedisys (UnitedHealth Group)

- Bristol Hospice

- Care Dimensions

- Chapters Health System

- Compassus

- Crossroads Hospice & Palliative Care

- Elara Caring

- Empath Hospice

- Enhabit Home Health & Hospice

- Gentiva

- Heart to Heart Hospice

- LHC Group Hospice

- Ohio's Hospice

- Silverado Hospice

- St. Croix Hospice

- Traditions Health

- VITAS Healthcare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population and Multi-Morbidity

- 4.2.2 Home-Based Hospice Preference

- 4.2.3 Medicare and Payer Reimbursement Support

- 4.2.4 AI-Enabled Referral Analytics

- 4.2.5 PE-Backed Micro-Market Roll-Ups

- 4.2.6 Non-Cancer Disease-Specific Programs

- 4.3 Market Restraints

- 4.3.1 Out-Of-Pocket Burden and Payment Caps

- 4.3.2 Workforce Shortages and RN Turnover

- 4.3.3 Heightened Compliance and Survey Scrutiny

- 4.3.4 Interoperability And Claims Friction

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Level of Care

- 5.1.1 Routine Home Care

- 5.1.2 Continuous Home Care

- 5.1.3 General Inpatient Care

- 5.1.4 Inpatient Respite Care

- 5.2 By Care Setting

- 5.2.1 Hospice Centers

- 5.2.2 Home Hospice Care

- 5.2.3 Hospitals

- 5.2.4 Skilled Nursing Facilities

- 5.3 By Patient Diagnosis

- 5.3.1 Dementia and Alzheimer's Disease

- 5.3.2 Circulatory and Heart Failure

- 5.3.3 Cancer

- 5.3.4 Respiratory Disease

- 5.3.5 Stroke and Neurovascular Disease

- 5.3.6 Chronic Kidney Disease

- 5.3.7 Other Terminal Diagnoses

- 5.4 By Payer

- 5.4.1 Medicare

- 5.4.2 Medicaid

- 5.4.3 Private Insurance

- 5.4.4 Out-of-Pocket and Other Payers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AccentCare

- 6.3.2 Agape Care Group / ACG Hospice

- 6.3.3 Amedisys (UnitedHealth Group)

- 6.3.4 Bristol Hospice

- 6.3.5 Care Dimensions

- 6.3.6 Chapters Health System

- 6.3.7 Compassus

- 6.3.8 Crossroads Hospice & Palliative Care

- 6.3.9 Elara Caring

- 6.3.10 Empath Hospice

- 6.3.11 Enhabit Home Health & Hospice

- 6.3.12 Gentiva

- 6.3.13 Heart to Heart Hospice

- 6.3.14 LHC Group Hospice

- 6.3.15 Ohio's Hospice

- 6.3.16 Silverado Hospice

- 6.3.17 St. Croix Hospice

- 6.3.18 Traditions Health

- 6.3.19 VITAS Healthcare

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment