|

시장보고서

상품코드

2064540

미국의 진단 영상 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Diagnostic Imaging Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

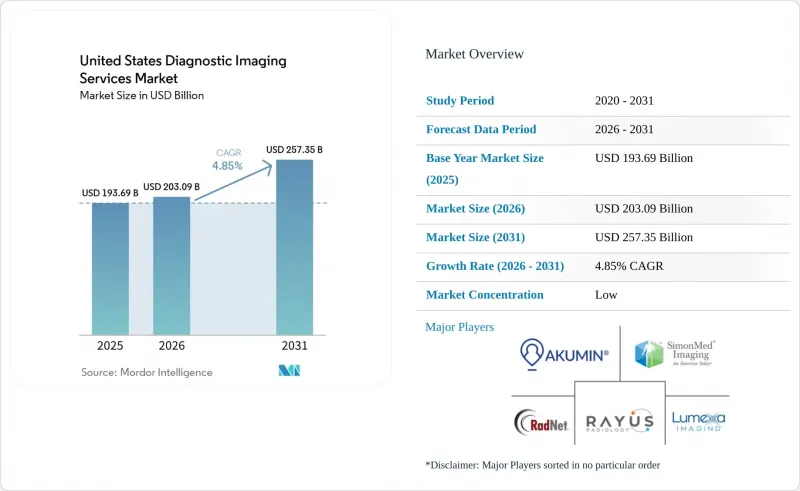

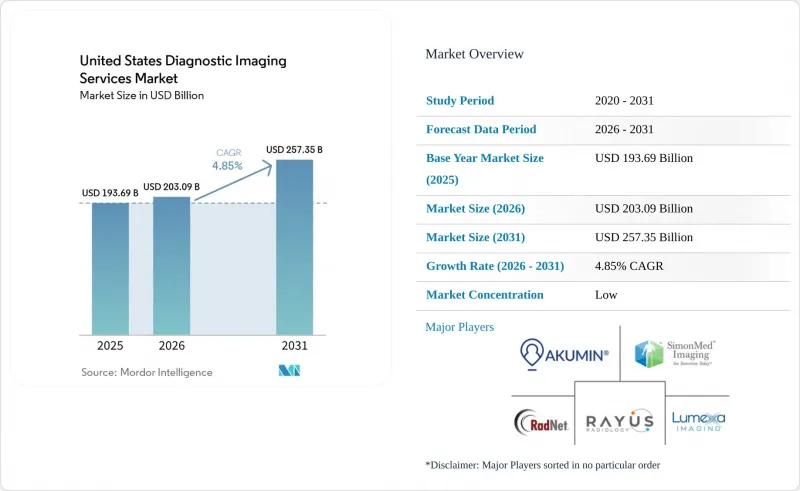

Mordor Intelligence에 의하면, 미국의 진단 영상 서비스 시장 규모는 2025년에 1,936억 9,000만 달러로 평가되었고, 2026년 2,030억 9,000만 달러로 추정되고, 2031년까지 2,573억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2026년-2031년) CAGR은 4.85%를 나타낼 전망입니다.

본 보고서는 검사 방식별(X선, CT, MRI, 초음파, 유방촬영술, 핵의학), 용도별(종양학, 심장학, 신경학, 정형외과, 산부인과, 일반), 진료 장소별(병원, 독립형, 지역 의료, 이동형), 제공 모델별(자사 운영, 합작 사업, 관리 운영, 원격 방사선 진단), 지불 주체별(민간 보험, 메디케어, 본인 부담, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 진단 영상 서비스 시장 동향 및 인사이트

고령화에 따른 만성 질환의 영상 진단 건수

미국의 진단 영상 서비스 시장에는 45세 이상 성인의 만성 질환 유병률이 여전히 높은 데다, 이러한 질환의 경우 진단, 모니터링, 경과 관찰의 각 단계에서 반복적인 영상 검사가 필요하기 때문에 견고한 수요 기반이 형성되어 있습니다. 심장병, 암, 만성 폐쇄성 폐질환(COPD), 뇌졸중은 모두 나이가 들면서 발병률이 증가하기 때문에 영상 검사 수요는 인구 고령화뿐만 아니라 고령 환자들이 동시에 여러 가지 영상 검사 과정을 거치는 경향이 있다는 점에서도 증가하고 있습니다. 이러한 추세는 CT, MRI, 핵의학 검사, 초음파 검사, X선 검사 분야의 검사 건수 증가를 뒷받침하고 있습니다. 왜냐하면, 다중 질환이 동반됨에 따라 한 번의 진료 과정에서 필요한 검사 횟수가 증가하기 때문입니다. 따라서 미국의 진단용 영상 검사 서비스 시장은 특히 종양학, 순환기학, 신경학 분야에서 초기 진단과 마찬가지로 정기적인 경과 관찰이 중요한 환자 구성의 혜택을 받고 있습니다. 이러한 수요 기반은 단순한 검사 이용이 아니라 장기적인 돌봄 수요와 밀접하게 연결되어 있기 때문에 쉽게 대체될 수 있는 것이 아닙니다.

선별검사에 기반한 조기 진단 수요

미국의 진단 영상 서비스 시장은 치료 초기 단계에서 영상 검사를 받는 환자층을 확대하는 보다 광범위한 선별 검사 경로의 보급으로부터도 혜택을 받고 있습니다. 2024년 USPSTF(미국 예방의학작업반)의 유방암 선별검사 지침 개정에서 2년마다 실시하는 유방촬영술 검사의 권장 시작 연령이 40세로 낮아졌으며, 이에 따라 향후 선별검사 대상자가 더 늘어날 것으로 기대됩니다. 또한, 2024년 『JAMA Network Open』지에 게재된 연구에 따르면, 폐암 검진 대상 연령대를 확대할 경우 연간 2만 6,124명의 사망을 예방할 수 있으며, 현재의 검진 방식에 비해 비용 대비 효과가 6배 더 높은 것으로 나타났습니다. 이는 향후 정책 주기에 따라 대상 범위가 확대될 경우, 검사 건수가 더욱 증가할 가능성을 시사하고 있습니다. 유방촬영술, CT 및 후속 영상 검사로의 의뢰는 접근성이 좋고 환자들이 모이기 쉬운 거점을 중심으로 이루어지는 경향이 있으므로, 이러한 변화는 외래 검진 체계가 잘 갖춰진 의료기관에 유리하게 작용합니다. 2025년 10월 솔리스 유방촬영술이 세인트루이스 유방센터를 인수한 것은 전문 검진 제공업체들이 검사 건수 증가를 포착하기 위해 더 많은 대도시권으로 사업을 확장하고 있음을 보여줍니다.

방사선과 전문의 및 기술자 부족

인력 부족은 미국 진단 영상 서비스 시장에서 여전히 가장 뚜렷한 구조적 제약 요인 중 하나입니다. 2025년 4월 『American Journal of Neuroradiology』에 게재된 조사에 따르면, 조사 대상이었던 NRMP 기간 동안 ACR 커리어 센터에는 3만 1,825건의 채용 공고가 게시된 반면, 진단 방사선과 레지던트 졸업 예정자는 10,180명에 그쳤으며, 수요와 수련 수료자 수 사이에 큰 불일치가 있음을 시사하고 있습니다. 이러한 압박은 고도의 영상 진단이나 세부 전문 분야의 영상 판독에서 가장 두드러지며, 지연이 발생하면 처리 능력이 저하되고 결과 보고까지 걸리는 시간이 길어져 의뢰 환자를 유지하기 어려워질 수 있습니다. 이것이 바로 미국의 진단 영상 서비스 시장이 자동화, 중앙 집중식 판독 플랫폼, 그리고 보다 광범위한 임상의 네트워크를 통해 검사 데이터를 공유할 수 있는 네트워크 모델에 점점 더 크게 의존하게 된 이유 중 하나입니다. 또한, 이러한 부족함은 더 나은 보상, 탄탄한 지원 팀, 그리고 유연한 판독 체계를 제공할 수 있는 대규모 조직에 협상상의 우위를 가져다주는 결과로 이어지고 있습니다.

부문별 분석

2025년, X선 검사는 매출의 28.31%를 차지했으며, 응급의료, 정형외과, 흉부 평가 분야에서 여전히 필수적인 역할을 하고 있어 미국 진단 영상 서비스 시장에서 가장 큰 모달리티로서의 위상을 유지했습니다. 이 부문의 규모는 높은 가격 책정이 아니라 검사 항목의 폭이 넓다는 점에 기인합니다. 즉, CT나 MRI가 1회 검사당 가치가 더 높은 경우가 많음에도 불구하고, 매출 비중은 꾸준히 유지되고 있습니다. 이처럼 광범위한 임상 적용 범위 덕분에, X선 검사는 병원 및 외래 진료 시설에서 급성기 및 일상적인 영상 진단 수요를 모두 충족시켜, 미국의 진단 영상 서비스 시장에서 안정화 역할을 수행하고 있습니다. 또한, AI 도입으로 인해 특히 보고서 작성이나 문서화 작업이 표준화될 수 있는 분야에서 이 모달리티의 처리 능력도 향상되기 시작했습니다. SimonMed Imaging이 2025년 12월 Lunit과 제휴하여 흉부 X선 소견서 생성을 위한 다중 모달 기반 모델을 도입한 것은 검사 건수가 많고 단가가 낮은 분야조차도 차세대 운영 모델의 일부가 되어가고 있음을 보여줍니다.

컴퓨터 단층촬영(CT)은 가장 빠르게 성장하고 있는 영상 진단 기법이며, 미국의 CT 진단 영상 서비스 시장 규모는 2031년까지 연평균 성장률(CAGR) 6.38%로 확대될 것으로 전망됩니다. CT는 폐암 검진, 심혈관 영상 진단, 외상 평가 및 다양한 종양학 진료 경로의 핵심을 차지하고 있어, 검사 건수 증가분에서 차지하는 비중을 확대되고 있습니다. RadNet의 보고에 따르면, 2026년 1분기 CT 검사 건수는 전년 동기 대비 17.7% 증가했으며, 동일 시설 내 CT 검사 건수도 4.7% 증가했습니다. 이는 수요가 유기적인 성장과 네트워크 확대를 통해 모두 증가하고 있음을 보여줍니다. MRI 역시 신경계, 근골격계, 심장 분야에서의 활용이 확대되고 있는 가운데, RadNet은 2026년 1분기 동일 의료기관에서의 MRI 검사 건수가 10.0% 증가했다고 밝혔습니다. 초음파 검사와 유방촬영술은 휴대성이 뛰어나고, 환자의 부담이 적으며, 예방적 선별검사로의 활용이 확대되고 있다는 장점 덕분에 여전히 중요한 성장 동력으로 작용하고 있습니다. 또한, 2025년 1월 SimonMed가 지멘스 헬스인이어스와 체결한 간 질환 선별 검사에 관한 제휴는 초음파 워크플로우에 대한 모달리티 특화형 투자가 지속되고 있음을 보여줍니다.

2025년, 종양학은 매출의 33.24%를 차지했으며, 미국 진단 영상 서비스 시장에서 가장 큰 용도 분야가 되었습니다. 이러한 주도적 지위는 암 치료의 장기적인 구조를 반영하고 있으며, 환자는 종종 병기 분류, 재병기 분류, 치료 효과 모니터링, 재발 감시 등의 과정을 거쳐 여러 치료 방식을 아우르는 치료를 받게 됩니다. 또한, 이 분야는 선별 검사의 확대가 하류 단계인 첨단 영상 진단으로 이어진다는 점에서도 혜택을 보고 있습니다. 특히, 의심스러운 소견이 CT, MRI, 초음파 또는 핵의학 검사 등의 후속 검사로 이어지는 경우가 있습니다. 따라서 종양학 검사 건수는 의료 제공업체 네트워크 전체에서 기준선 이용률과 부가가치가 더 높은 단층 촬영 검사 모두를 뒷받침하고 있습니다. 라디올로지 파트너스가 2025년 10월에 ‘Mammo Enhance Heart’를 출시한 것 또한, 선별검진 인프라를 활용하여 기존 영상진단 접점에서 얻을 수 있는 임상적 가치를 확대할 수 있음을 보여줍니다.

신경 및 척추 분야는 가장 빠르게 성장하고 있는 용도 분야이며, 이 부문의 미국 진단 영상 서비스 시장 규모는 2031년까지 연평균 성장률(CAGR) 7.52%로 확대될 것으로 예측됩니다. 뇌졸중 검사, 다발성 경화증의 경과 관찰, 척추 퇴행성 질환 및 인지 기능 저하의 평가 등은 모두 장기간에 걸친 반복적인 영상 진단에 의존하고 있기 때문에 MRI 수요가 주요 촉진요인으로 작용하고 있습니다. 심장 영상 진단은 여전히 중요한 관련 분야로서 수요를 창출하고 있지만, 2025년 초 ASNC가 보고한 Tc-99m 피로인산염공급 부족 사태는 의료 제공업체가 통제할 수 없는 공급 문제로 인해 핵의학 심장 진단이 얼마나 큰 혼란을 겪을 수 있는지를 보여주었습니다. 정형외과 및 근골격계 영상 진단은 고령 환자나 외래에서 반복적으로 시행되는 관절 수술로 인해 진단 수요가 지속되고 있어, 계속해서 높은 빈도로 수요가 발생하고 있습니다. 여성 의료 및 산과 분야도 선별 검사의 확대와 추가적인 경과 관찰 체계의 구축을 통해 혜택을 볼 것으로 예측됩니다. 한편, 일반 영상 진단은 응급실이나 1차 진료 기관에서 의뢰되는 사례가 계속해서 많은 검사 건수를 창출하고 있어, 여전히 신뢰할 수 있는 기반이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

LSH 26.06.24According to Mordor Intelligence, the united states diagnostic imaging services market size was valued at USD 193.69 billion in 2025 and is estimated to grow from USD 203.09 billion in 2026 to reach USD 257.35 billion by 2031, at a CAGR of 4.85% during the forecast period (2026-2031).

This report is Segmented by Modality (X-Ray, CT, MRI, Ultrasound, Mammography, Nuclear), Application (Oncology, Cardiology, Neurology, Orthopedics, Women's Health, General), Site of Care (Hospital, Freestanding, Community, Mobile), Delivery Model (Owned, JV, Managed, Teleradiology), Payor (Commercial, Medicare, Self-Pay, Others). The Market Forecasts are Provided in Terms of Value (USD).

United States Diagnostic Imaging Services Market Trends and Insights

Aging Chronic-Disease Imaging Volumes

The US diagnostic imaging services market has a durable demand floor because chronic disease prevalence remains high in adults age 45 and older, and those conditions often require repeated imaging across diagnosis, monitoring, and follow-up care. Heart disease, cancer, COPD, and stroke all become more common with age, which means imaging demand rises not only because the population is aging, but also because older patients tend to move through several imaging pathways at the same time. This pattern supports study growth across CT, MRI, nuclear imaging, ultrasound, and X-ray, because multimorbidity increases the number of scans attached to a single episode of care. The US diagnostic imaging services market therefore benefits from a patient mix where recurring surveillance matters as much as first diagnosis, especially in oncology, cardiology, and neurology. That demand base is difficult to displace because it is linked to long-cycle care needs rather than discretionary procedure use.

Screening-Led Early Diagnosis Demand

The US diagnostic imaging services market is also benefiting from broader screening pathways that enlarge the pool of patients entering imaging earlier in the care journey. The 2024 USPSTF breast cancer screening update lowered the recommended start age to 40 for biennial mammography, which should support a larger screening population over time. A 2024 JAMA Network Open study also showed that broader age-based lung cancer screening could prevent 26,124 deaths annually and be 6 times more cost-effective than current screening approaches, which points to further procedure upside if eligibility expands in future policy cycles. These changes favor operators with strong outpatient screening capacity, because mammography, CT, and follow-on imaging referrals tend to build around dense, convenient access points. Solis Mammography's October 2025 acquisition of the St. Louis Breast Center shows how specialized screening providers are expanding into additional metropolitan areas to capture that volume growth.

Radiologist And Technologist Shortages

Workforce shortage remains one of the clearest structural constraints on the US diagnostic imaging services market. Research published in the American Journal of Neuroradiology in April 2025 reported 31,825 ACR Career Center listings against 10,180 anticipated diagnostic radiology residency graduates through the NRMP period reviewed, which implies a large mismatch between demand and training output. The pressure is most visible in advanced imaging and subspecialty reads, where delays can reduce throughput, stretch turnaround times, and weaken referral retention. This is one reason the US diagnostic imaging services market is leaning more heavily on automation, centralized reading platforms, and network models that can move studies across a broader clinician base. The shortage also tilts bargaining power toward larger organizations that can offer better compensation, deeper support teams, and more flexible reading arrangements.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Workflow and Scan Productivity

- Virtual Direct Supervision for Contrast Imaging

- Reimbursement And Margin Pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

X-ray accounted for 28.31% of revenue in 2025, which kept it as the largest modality in the US diagnostic imaging services market because it remains essential across emergency care, orthopedics, and chest evaluation. The segment's scale rests on procedure breadth rather than on high ticket pricing, which means revenue share remains strong even though CT and MRI often generate more value per exam. This wide clinical footprint gives X-ray a stabilizing role in the US diagnostic imaging services market because it supports both acute and routine imaging demand across hospitals and outpatient sites. AI adoption is also beginning to improve throughput in this modality, especially where report generation and documentation can be standardized. SimonMed Imaging's December 2025 partnership with Lunit to deploy multimodal foundation models for chest X-ray report generation shows that even high-volume, lower-ticket categories are becoming part of the next operating model.

Computed Tomography is the fastest-growing modality, with the US diagnostic imaging services market size for CT projected to expand at a 6.38% CAGR through 2031. CT is gaining share of incremental study growth because it sits at the center of lung screening, cardiovascular imaging, trauma evaluation, and many oncology pathways. RadNet reported a 17.7% year-on-year increase in CT procedural volumes in Q1 2026, while same-center CT volumes rose 4.7%, which indicates that demand is growing both organically and through network expansion. MRI is also expanding on the back of neurological, musculoskeletal, and cardiac use, and RadNet stated that same-center MRI volume rose 10.0% in Q1 2026. Ultrasound and mammography remain important growth supports because they benefit from portability, lower patient friction, and stronger preventive screening use, while SimonMed's January 2025 partnership with Siemens Healthineers for liver disease screening reflects continued modality-specific investment in ultrasound workflows.

Oncology represented 33.24% of revenue in 2025, giving it the largest application position in the US diagnostic imaging services market. That leadership reflects the longitudinal structure of cancer care, where patients often move through staging, restaging, treatment response monitoring, and recurrence surveillance across several modalities. The segment also benefits from the way screening expansion feeds downstream advanced imaging, especially when suspicious findings generate follow-up CT, MRI, ultrasound, or nuclear imaging. Oncology volumes therefore support both baseline utilization and higher-value cross-sectional procedures across provider networks. Radiology Partners' October 2025 launch of Mammo Enhance Heart also shows how screening infrastructure can be used to widen clinical value capture from existing imaging touchpoints.

Neurology and Spine is the fastest-growing application, with the US diagnostic imaging services market size for this segment expected to rise at a 7.52% CAGR through 2031. MRI demand is a major driver because stroke workup, multiple sclerosis follow-up, degenerative spine disease, and cognitive decline assessment all depend on repeated imaging over time. Cardiology imaging remains an important adjacent volume stream, but the ASNC-reported Tc-99m pyrophosphate shortage in early 2025 showed how nuclear cardiology can be disrupted by supply issues outside provider control. Orthopedics and musculoskeletal imaging continue to provide high-frequency demand because aging patients and outpatient joint procedures support recurring diagnostic needs. Women's Health and Obstetrics also stand to gain from expanded screening and supplemental follow-up pathways, while General Imaging remains a dependable base because emergency departments and primary care referrals continue to generate broad study volume.

List of Companies Covered in this Report:

- Akumin

- Capitol Imaging Services

- CommonSpirit Health

- Envision Radiology

- HCA Healthcare

- LucidHealth

- Lumexa Imaging

- MedQuest Imaging

- Outpatient Imaging Affiliates

- Radiology Partners

- RadNet

- RAYUS Radiology

- Rezolut

- Shared Medical Services

- SimonMed Imaging

- Solis Mammography

- Tenet Healthcare

- The US Oncology Network

- Touchstone Medical Imaging

- vRad

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Chronic-Disease Imaging Volumes

- 4.2.2 Screening-Led Early Diagnosis Demand

- 4.2.3 Outpatient Imaging Migration and Site-Neutral Economics

- 4.2.4 AI-Enabled Workflow and Scan Productivity

- 4.2.5 Virtual Direct Supervision for Contrast Imaging

- 4.2.6 Theranostics-Led PET/CT Mix Upgrade

- 4.3 Market Restraints

- 4.3.1 Radiologist and Technologist Shortages

- 4.3.2 Reimbursement and Margin Pressure

- 4.3.3 Prior-Authorization Friction in Advanced Imaging

- 4.3.4 Isotope and Imported-Equipment Input Volatility

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Modality

- 5.1.1 X-ray

- 5.1.2 Computed Tomography

- 5.1.3 Magnetic Resonance Imaging

- 5.1.4 Ultrasound

- 5.1.5 Mammography

- 5.1.6 Nuclear Imaging

- 5.2 By Application

- 5.2.1 Oncology

- 5.2.2 Cardiology

- 5.2.3 Neurology and Spine

- 5.2.4 Orthopedics and Musculoskeletal

- 5.2.5 Women's Health and Obstetrics

- 5.2.6 General Imaging

- 5.3 By Site of Care

- 5.3.1 Hospital-based Imaging Departments

- 5.3.2 Freestanding Imaging Centers

- 5.3.3 Community Diagnostic Centers and Polyclinic Hubs

- 5.3.4 Mobile Imaging Units

- 5.4 By Delivery Model

- 5.4.1 Owned and Operated Networks

- 5.4.2 Hospital Joint Ventures

- 5.4.3 Managed Services and Outsourcing Contracts

- 5.4.4 Teleradiology-enabled Networks

- 5.5 By Payor

- 5.5.1 Commercial and Employer-sponsored Plans

- 5.5.2 Medicare

- 5.5.3 Medicaid

- 5.5.4 Self-pay

- 5.5.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Akumin

- 6.3.2 Capitol Imaging Services

- 6.3.3 CommonSpirit Health

- 6.3.4 Envision Radiology

- 6.3.5 HCA Healthcare

- 6.3.6 LucidHealth

- 6.3.7 Lumexa Imaging

- 6.3.8 MedQuest Imaging

- 6.3.9 Outpatient Imaging Affiliates

- 6.3.10 Radiology Partners

- 6.3.11 RadNet

- 6.3.12 RAYUS Radiology

- 6.3.13 Rezolut

- 6.3.14 Shared Medical Services

- 6.3.15 SimonMed Imaging

- 6.3.16 Solis Mammography

- 6.3.17 Tenet Healthcare

- 6.3.18 The US Oncology Network

- 6.3.19 Touchstone Medical Imaging

- 6.3.20 vRad

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment