|

시장보고서

상품코드

2064543

GPU 및 AI 서버용 전원 공급 모듈(VRM) 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Power Delivery Module (VRM) For GPU And AI Servers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

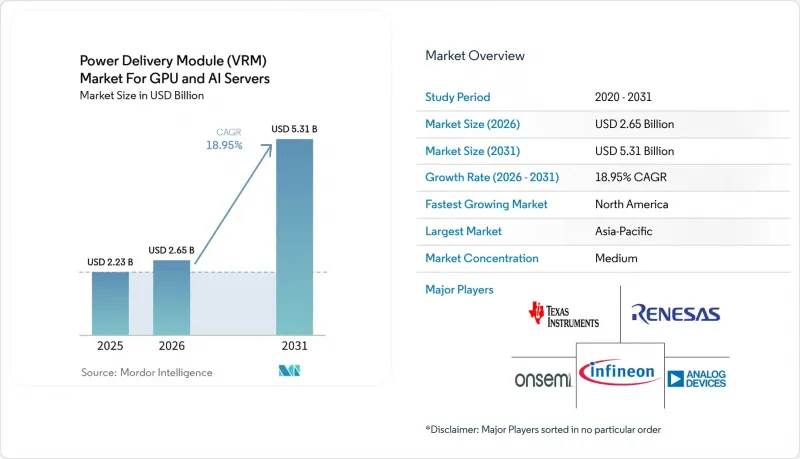

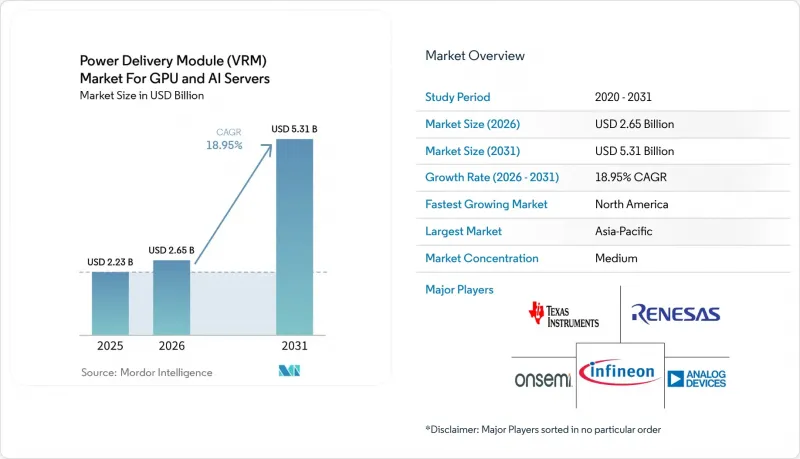

Mordor Intelligence에 의하면, GPU 및 AI 서버용 전원 공급 모듈(VRM) 시장 규모는 2024년 17억 8,000만 달러로 평가되었고, 2025년에는 22억 3,000만 달러로 확대되었으며, 2031년까지 53억 1,000만 달러에 이를 것으로 예측되고, 2026-2031년 CAGR 18.95%로 성장할 전망입니다.

본 보고서는 VRM의 유형별(다상 디지털, 아날로그 등), 상 수별(6 이하, 7-12, 13-20, 20 이상), 전력 용량별(저전력(100A 미만), 중전력(100-300A), 기타), 구성 요소별(파워 스테이지, PWM 컨트롤러 등), 최종 용도별(GPU 카드, AI/HPC 서버 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 GPU 및 AI 서버용 전원 공급 모듈(VRM) 시장 동향 및 인사이트

하이퍼스케일 데이터센터에서의 GPU 가속기 수요 증가

2025년, 컴퓨팅 패브릭이 대규모 언어 모델과 추천 엔진으로 전환되는 가운데, 하이퍼스케일 사업자들은 300만 대 이상의 GPU 가속기를 도입했습니다. NVIDIA H200 및 AMD MI300X 그래픽 카드는 각각 최대 1,000와트를 소비하므로, VRM은 리플 10밀리볼트 미만으로 서브볼트 레일에서 1,200암페어를 공급해야 합니다. 직접 수냉식 랙을 통해 100kW를 초과하는 전력 밀도가 가능해짐에 따라, 기판의 점유 면적을 줄여주는 통합형 전력 모듈의 도입이 촉진되고 있습니다. 현재 하이퍼스케일러는 상 전류, 온도, 효율에 관한 실시간 텔레메트리 데이터를 필요로 하고 있으며, 이러한 사양은 디지털 다상 컨트롤러에 유리하게 작용하고 있습니다. 이러한 사업자들은 기존의 유통 경로를 우회하여, 24-36개월공급 계약에 따라 용도 특화형 모듈의 공동 개발을 더욱 적극적으로 추진하고 있습니다.

3D 적층 HBM 메모리로의 전환이 과도 부하 요건을 높입니다.

2024년 하반기부터 양산이 시작된 HBM3E에는 1마이크로초당 200암페어의 과도 단계가 도입되었습니다. 또한, HBM4 프로토타입의 경우 2027년까지 스택당 전력 소비량이 50와트를 초과할 것으로 예측됩니다. 이에 대해 VRM 공급업체는 결합 인덕터와 적응형 전압 제어를 채택하여 출력 임피던스를 40% 낮춤으로써 이에 대응하고 있습니다. 2025년 3월, 텍사스 기기의 6-페이즈 레퍼런스 설계는 500암페어에서 15밀리볼트의 과도 응답을 달성했습니다. GPU 다이와 메모리 사이의 수직 거리가 줄어들면서 임피던스 허용 범위가 더욱 엄격해져, VRM을 기판에서 20mm 이내로 배치할 수밖에 없게 되었습니다. 기판에 수직으로 장착된 수직형 파워 모듈은 루프 인덕턴스를 50% 저감하지만, 전용 기계적 고정 장치와 열 인터페이스가 필요합니다.

고성능 파워 스테이지공급망 부족

기판 공급업체들이 수익성이 높은 치플렛을 우선시한 탓에, 2026년 초에는 DrMOS 및 스마트 파워 스테이지의 리드타임이 26주까지 늘어났습니다. Vishay는 가동률 95%를 기록하며, 2025년 하반기까지의 수주 잔고를 보고했습니다. 2025년 10월 Onsemi의 Vcore 인수는 갈륨 질화물 웨이퍼의 생산 능력을 확보하기 위한 것으로, 공급을 안정화하기 위한 수직 통합의 움직임을 보여줍니다. 인피니온은 추가 실리콘 카바이드 웨이퍼 생산을 위해 8억 유로(9억 400만 달러)를 배정했으나, 신규 팹이 완전 가동되는 시점은 2027년 하반기가 될 전망입니다. 부족 현상이 가장 심각한 것은 1상당 100암페어를 초과하는 영역이며, 이 경우 방열 여유를 확보하기 위해 구리 클립 본딩이 필요합니다. VRM 설계자는 대체 공급업체의 인증을 받거나 펌웨어를 개정해야 하므로, 개발 주기가 최대 9개월까지 연장될 것입니다.

부문별 분석

다상·디지털 제어 장치가 전원 공급 모듈(VRM) 시장 점유율을 주도하며, 2025년에는 매출의 61%를 차지했습니다. 이 장치들은 펌웨어 업데이트가 가능한 제어 루프와 PMBus 텔레메트리 같은 고급 기능을 갖추고 있어, 하이퍼스케일러의 차량 군 모니터링 시스템에 최적화되어 있기 때문에 선호되고 있습니다. 펌웨어 업데이트 기능을 통해 변화하는 요구 사항에 대한 적응성이 확보되고, PMBus 텔레메트리를 통한 실시간 모니터링 및 제어가 가능하기 때문에 이러한 장치는 대규모 운영 환경에서 높은 효율성과 신뢰성을 발휘합니다. 통합형 파워 모듈은 2025년 시점에서 시장 점유율은 낮지만, 예측 기간 동안 19.74%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 이러한 성장은 설계를 간소화하고 개발 기간을 단축하는 소형 드롭인 솔루션에 대한 서버 제조업체 수요 증가에 힘입은 것입니다.

전원 공급 모듈(VRM) 분야에서 통합 모듈 시장 점유율은 보다 콤팩트하고 효율적인 레이아웃을 가능하게 하는 48볼트 중간 버스 및 수냉식 랙 등의 기술 발전에 힘입어 꾸준히 증가하고 있습니다. Vicor와 같은 공급업체들은 이러한 추세의 최전선에 서서, 컨트롤러, 파워 스테이지, 결합 인덕터를 단일 패키지에 통합한 혁신적인 솔루션을 제공합니다. 이번 통합을 통해 기판 면적이 약 40% 줄어들어, 제조업체 입장에서는 공간 절약이라는 큰 이점을 얻을 수 있습니다. 엣지 디바이스의 경우 아날로그 컨트롤러가 여전히 비용 효율성이 뛰어나지만, 장기적인 추세는 디지털 또는 하이브리드 설계로 전환되고 있습니다. 이러한 첨단 설계는 낮은 지연 시간과 강화된 텔레메트리 기능을 결합한 균형 잡힌 접근 방식을 제공하며, 이는 정밀한 전력 관리 및 모니터링이 필요한 현대의 용도에 필수적입니다.

2025년에는 13-20페이즈 솔루션이 매출의 43%를 차지했으며, 최대 700와트의 전력을 필요로 하는 가속기의 표준으로 자리 잡았습니다. 이러한 솔루션은 고성능 컴퓨팅 시스템의 전력 수요를 충족시키기 위해 널리 채택되고 있습니다. 그러나 20단계 이상의 부문은 향후 몇 년 동안 1,200와트를 넘어설 것으로 예상되는 GPU 전력 수요 증가에 힘입어 연평균 성장률(CAGR) 19.63%로 성장할 것으로 전망됩니다.

이 부문의 전원 공급 모듈(VRM) 시장의 성장은 결합 인덕터의 발전에 힘입어 이루어지고 있습니다. 이를 통해 콤팩트한 6-페이즈 실적 내에서 12-페이즈에 상응하는 성능을 구현할 수 있습니다. 이러한 혁신을 통해 기판상의 공간을 최적화하면서, 보다 효율적인 전력 공급이 가능해집니다. 또한, 전류 감지 기술을 통합한 스마트 파워 스테이지는 배선 혼잡을 줄여주고, 24상 및 32상 레이아웃 설계를 효율화하는 데 도움이 됩니다. 고상수 컨트롤러와 수직 실장 솔루션을 효과적으로 통합할 수 있는 공급업체는 이러한 기술이 진화하는 시장의 요구 사항에 부합하기 때문에 차세대 GPU 출시로 인한 수요를 최대한 활용할 수 있는 유리한 위치에 있습니다.

지역별 분석

아시아태평양은 대만 반도체 제조 회사(TSMC)의 패키징 기술 발전과 중국의 엑사스케일 훈련 클러스터 개발에 힘입어 2025년 매출의 58%를 차지했습니다. 일본의 Rapidus 이니셔티브는 2027년까지 2나노미터 로직 생산을 실현하기 위해 9,200억 엔(62억 달러)의 자금을 확보했습니다. 이에 따라 0.6V 미만의 전압 조정기 모듈(VRM)에 대한 수요가 크게 증가할 것으로 예측됩니다. 한국의 ‘K-Chips법’은 국내 전원 관리 IC 생산 라인에 26조 원(195억 달러)을 투자하고 있으며, SK하이닉스나 삼성 등 주요 기업의 사업 확장을 뒷받침하고 있습니다. 한편, 인도의 150억 달러 규모의 보조금 프로그램은 조립 투자를 유치하고 있지만, 컨트롤러용 실리콘의 대부분은 여전히 대만이나 미국에서 조달되고 있습니다.

북미에서는 반도체 제조 역량의 국내화를 촉진하는 ‘CHIPS법’을 주된 요인으로 하여, 2031년까지 연평균 성장률(CAGR) 20.95%라는 가장 높은 성장이 예상됩니다. 인텔이 200억 달러를 투자하는 애리조나주의 제조 시설에는 2026년 말까지 전력 관리용 생산 라인이 도입될 예정이며, 한편, 울프스피드가 노스캐롤라이나주에 건설하는 65억 달러 규모의 실리콘 카바이드(SiC) 공장은 2026년에 가동을 시작할 전망입니다. 또한, Microsoft Azure나 Amazon Web Services와 같은 클라우드 서비스 제공업체들은 2027년까지 각각 50만 대 이상의 GPU를 도입할 계획이며, 그 결과 VRM 수요는 500메가와트를 넘어설 것으로 예측됩니다.

유럽 시장 점유율은 해당 지역에 GPU 생산 능력이 부족하기 때문에 여전히 제한적입니다. 그러나 430억 유로(486억 달러) 규모의 ‘유럽 칩 법’에 따라 독일과 네덜란드 등 여러 국가에 전력 관리 설계 허브를 설립하는 데 적극적인 자금 지원이 이루어지고 있습니다. 반면, 중동 및 아프리카 및 남미 시장은 여전히 발전 초기 단계에 있으며, 정부 주도의 AI 연구 클러스터를 지원하기 위해 수입 VRM에 크게 의존하고 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the power delivery module (VRM) market size is expected to increase from USD 1.78 billion in 2024 to USD 2.23 billion in 2025 and reach USD 5.31 billion by 2031, growing at an 18.95% CAGR over 2026-2031.

This report is Segmented by VRM Type (Multiphase Digital, Analog, and More), Phase Count (<=6, 7-12, 13-20, and 20+), Current Capacity (Low <<100A, Mid 100-300A, and More), Component (Power Stages, PWM Controllers, and More), End Application (GPU Cards, AI/HPC Servers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Insights and Trends of Power Delivery Module (VRM) Market For GPU And AI Servers

Growing Demand for GPU Accelerators in Hyperscale Data Centers

Hyperscale operators deployed more than 3 million GPU accelerators in 2025 as compute fabrics shifted toward large language models and recommendation engines. Each NVIDIA H200 or AMD MI300X card draws up to 1,000 watts, forcing VRMs to deliver 1,200 amperes at sub-volt rails with ripple below 10 millivolts. Direct liquid-cooled racks enable power densities above 100 kilowatts, encouraging the use of integrated power modules that compress board footprint. Hyperscalers now require real-time telemetry for phase current, temperature, and efficiency, a specification that favors digital multiphase controllers. These operators increasingly co-develop application-specific modules under 24- to 36-month supply agreements, bypassing traditional distribution channels.

Transition Toward 3D Stacked HBM Memory Raising Transient Load Requirements

HBM3E, in volume since late 2024, introduces transient steps of 200 amperes per microsecond; HBM4 prototypes will push per-stack power past 50 watts by 2027. VRM suppliers respond with coupled inductors and adaptive voltage positioning, lowering output impedance by 40%. A Texas Instruments six-phase reference design achieved a 15-millivolt transient response at 500 amperes in March 2025. The vertical distance between the GPU die and the memory is shrinking, tightening impedance budgets and forcing VRM placement within 20 millimeters of the substrate. Vertical power modules mounted perpendicular to the board reduce loop inductance by 50%, but they demand custom mechanical fixtures and thermal interfaces.

Supply Chain Tightness for High-Performance Power Stages

Lead times for DrMOS and smart power stages stretched to 26 weeks in early 2026 as substrate suppliers prioritized high-margin chiplets. Vishay reported 95% utilization and a backlog into late 2025. Onsemi's October 2025 acquisition of Vcore secured gallium nitride wafer capacity, illustrating vertical integration moves to stabilize supply. Infineon earmarked EUR 800 million (USD 904 million) for additional silicon-carbide wafers, though new fabs will not reach full output until late 2027. Shortages are most acute above 100 amperes per phase, where copper-clip bonding is needed for thermal headroom. VRM designers must qualify alternate vendors and revise firmware, extending development cycles by up to 9 months.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Mandates from Cloud Service Providers

- Adoption of Advanced FinFET Nodes Lowering Core Voltages

- Thermal Management Challenges Above 800 A Rails

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Multiphase, digitally controlled units led the Power Delivery Module (VRM) market share, accounting for 61% of revenue in 2025. These units are preferred due to their advanced features, including firmware-updatable control loops and PMBus telemetry, which are well-suited for hyperscaler fleet monitoring systems. The ability to update firmware ensures adaptability to evolving requirements, while PMBus telemetry provides real-time monitoring and control, making these units highly efficient and reliable for large-scale operations. Integrated power modules, although representing a smaller market share in 2025, are projected to experience the fastest CAGR of 19.74% during the forecast period. This growth is driven by server builders' increasing preference for compact, drop-in solutions that simplify design and reduce development time.

The market share of integrated modules in the Power Delivery Module (VRM) sector is steadily increasing, supported by advancements such as 48-volt intermediate buses and liquid-cooled racks, which enable tighter, more efficient layouts. Vendors like Vicor are at the forefront of this trend, offering innovative solutions that integrate controllers, power stages, and coupled inductors into a single package. This integration reduces board area by approximately 40%, providing significant space-saving benefits for manufacturers. While analog controllers remain cost-effective for edge devices, the long-term trend is shifting toward digital or hybrid designs. These advanced designs offer a balanced approach, combining low latency with enhanced telemetry capabilities, which are critical for modern applications requiring precise power management and monitoring.

Thirteen- to 20-phase solutions accounted for 43% of the revenue in 2025, establishing themselves as the standard for accelerators requiring up to 700 watts of power. These solutions are widely adopted because they meet the power demands of high-performance computing systems. However, the 20-plus phase tier is projected to grow at a compound annual growth rate (CAGR) of 19.63%, driven by the increasing power requirements of GPUs, which are expected to surpass 1,200 watts in the coming years.

The growth of the Power Delivery Module (VRM) market in this tier is supported by advancements in coupled inductors, which enable 12-phase performance within a compact six-phase footprint. This innovation allows for more efficient power delivery while optimizing space on circuit boards. Additionally, smart power stages with integrated current sensing technology help reduce routing congestion and streamline the design of 24- and 32-phase layouts. Suppliers who can effectively integrate high-phase controllers with vertical packaging solutions are well positioned to capitalize on demand for next-generation GPU launches, as these technologies align with evolving market requirements.

Geography Analysis

Asia-Pacific generated 58% of 2025 revenue, driven by Taiwan Semiconductor Manufacturing Company's advancements in packaging technologies and China's development of exascale training clusters. Japan's Rapidus initiative secured JPY 920 billion (USD 6.2 billion) in funding to achieve 2-nanometer logic production by 2027, which is expected to create significant demand for sub-0.6-volt Voltage Regulator Modules (VRMs). South Korea's K-Chips Act is channeling KRW 26 trillion (USD 19.5 billion) into domestic power-management IC production lines, facilitating expansions by major players such as SK hynix and Samsung. Meanwhile, India's USD 15 billion subsidy program is attracting assembly investments; however, the majority of controller silicon is still sourced from Taiwan and the United States.

North America is anticipated to experience the fastest Compound Annual Growth Rate (CAGR) of 20.95% through 2031, primarily due to the CHIPS Act, which is incentivizing the localization of semiconductor manufacturing capacity. Intel's USD 20 billion Arizona fabrication facility is set to include a power-management production line by late 2026, while Wolfspeed's USD 6.5 billion silicon carbide (SiC) plant in North Carolina is expected to begin operations in 2026. Additionally, cloud service providers such as Microsoft Azure and Amazon Web Services are planning to deploy over 500,000 GPUs each by 2027, resulting in a projected VRM demand exceeding 500 megawatts.

Europe's market share remains limited due to the region's lack of GPU manufacturing capabilities. However, the EUR 43 billion (USD 48.6 billion) European Chips Act is actively funding the establishment of power-management design hubs in countries like Germany and the Netherlands. In contrast, the markets in the Middle East, Africa, and South America are still in their early stages of development, relying heavily on imported VRMs to support government-sponsored AI research clusters.

- Texas Instruments Incorporated

- Renesas Electronics Corporation

- Infineon Technologies AG

- onsemi

- Analog Devices, Inc.

- Monolithic Power Systems, Inc.

- Rohm Co., Ltd.

- STMicroelectronics N.V.

- Vicor Corporation

- Delta Electronics, Inc.

- Bel Fuse Inc. (Bel Power Solutions)

- Advanced Energy Industries, Inc.

- Murata Manufacturing Co., Ltd.

- Vishay Intertechnology, Inc.

- Coilcraft, Inc.

- TDK Corporation

- Lite-On Technology Corporation

- Foxconn Interconnect Technology Ltd.

- FSP Technology Inc.

- XP Power Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand For GPU Accelerators In Hyperscale Data Centers

- 4.2.2 Energy-Efficiency Mandates From Cloud Service Providers

- 4.2.3 Transition Toward 3D Stacked HBM Memory Raising Transient Load Requirements

- 4.2.4 Adoption Of Advanced FinFET Nodes Lowering Core Voltages

- 4.2.5 AI Inference At The Edge Driving Compact High-Current VRMs

- 4.2.6 Government Incentives For Domestic Semiconductor Supply Chains

- 4.3 Market Restraints

- 4.3.1 Supply Chain Tightness For High-Performance Power Stages

- 4.3.2 Board Space Constraints In Dense GPU Card Layouts

- 4.3.3 Thermal Management Challenges Above 800 A Rails

- 4.3.4 Limited Standardization Across Server OEM VRM Specifications

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By VRM Type

- 5.1.1 Multiphase VRMs (Digital-controlled)

- 5.1.2 Analog VRMs

- 5.1.3 Integrated Power Modules

- 5.1.4 Hybrid VRMs

- 5.2 By Phase Count

- 5.2.1 <=6 Phases

- 5.2.2 7-12 Phases

- 5.2.3 13-20 Phases

- 5.2.4 20+ Phases

- 5.3 By Current Handling Capacity

- 5.3.1 Low Power (<100 A)

- 5.3.2 Mid Power (100-300 A)

- 5.3.3 High Power (300-800 A)

- 5.3.4 Ultra High Power (800 A+)

- 5.4 By Component Type

- 5.4.1 Power Stages (DrMOS / SPS)

- 5.4.2 PWM Controllers

- 5.4.3 Inductors (Chokes)

- 5.4.4 Capacitors

- 5.5 By End Application

- 5.5.1 GPU Accelerator Cards

- 5.5.2 AI / HPC Servers

- 5.5.3 AI Training Systems

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Rest of the World

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Texas Instruments Incorporated

- 6.4.2 Renesas Electronics Corporation

- 6.4.3 Infineon Technologies AG

- 6.4.4 onsemi

- 6.4.5 Analog Devices, Inc.

- 6.4.6 Monolithic Power Systems, Inc.

- 6.4.7 Rohm Co., Ltd.

- 6.4.8 STMicroelectronics N.V.

- 6.4.9 Vicor Corporation

- 6.4.10 Delta Electronics, Inc.

- 6.4.11 Bel Fuse Inc. (Bel Power Solutions)

- 6.4.12 Advanced Energy Industries, Inc.

- 6.4.13 Murata Manufacturing Co., Ltd.

- 6.4.14 Vishay Intertechnology, Inc.

- 6.4.15 Coilcraft, Inc.

- 6.4.16 TDK Corporation

- 6.4.17 Lite-On Technology Corporation

- 6.4.18 Foxconn Interconnect Technology Ltd.

- 6.4.19 FSP Technology Inc.

- 6.4.20 XP Power Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment