|

시장보고서

상품코드

2065432

HR용 AI 코파일럿 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI Copilot For HR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

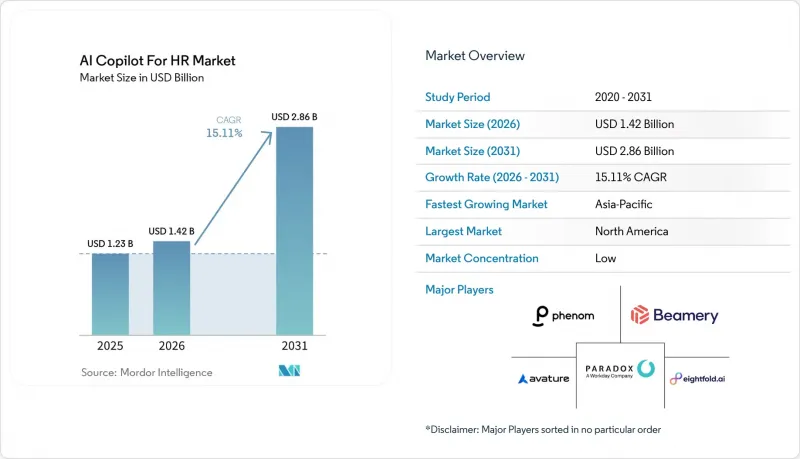

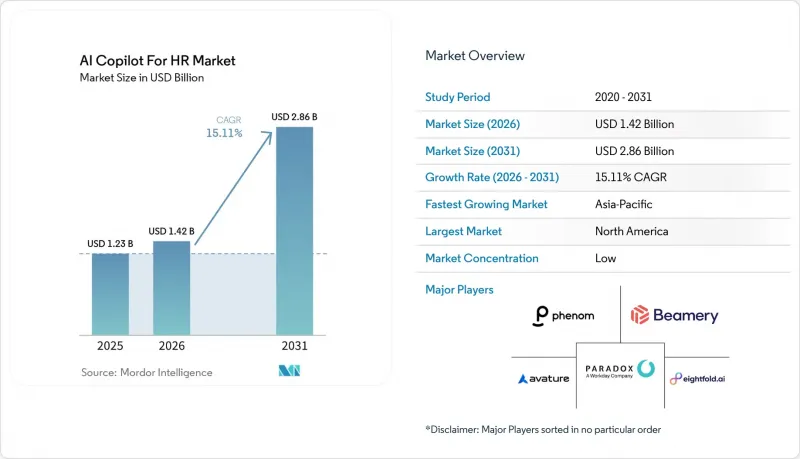

HR용 AI 코파일럿 시장 규모는 2025년 12억 3,000만 달러로 평가되었고, 2026년에는 14억 2,000만 달러로 추정되고, 2026-2031년 CAGR 15.11%로 성장을 지속할 전망이며, 2031년까지 28억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소별(소프트웨어 및 서비스), 용도별(급여 계산, 복리후생 및 인사 관리 등), 도입 형태별(클라우드 기반, 온프레미스형, 하이브리드형), 기업 규모별(대기업, 중소기업), 최종 사용자 산업 분야별(은행/금융서비스/보험 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 HR용 AI 코파일럿 시장 동향 및 인사이트

채용 건수의 자동화 및 채용까지 소요되는 기간 단축

생성형 도구의 등장으로 지원자들이 더 짧은 시간 내에 더 많은 지원 서류를 작성하고 제출할 수 있게 되면서, 채용 워크플로우를 수작업으로 관리하는 것이 점점 더 어려워지고 있습니다. Greenhouse에 따르면, 채용 담당자 1인당 지원 건수는 2023년 이후 412% 증가했으며, 이는 채용 팀이 직면한 선발 압박이 얼마나 급격히 커지고 있는지를 보여줍니다. 이러한 압박으로 인해 HR용 AI 코파일럿 시장은 채용 담당자의 개입을 최소화하면서 수행할 수 있는 자동화된 후보자 선별, 음성 기반 전형, 면접 일정 조정 및 후보자와의 커뮤니케이션 방향으로 나아가고 있습니다. 수요가 가장 높은 분야는 속도가 중요하고 채용 담당자의 대응 능력에 한계가 있는 직종, 특히 현장 업무나 시급제 채용입니다. 또한, 고용주들은 감사 추적 기록, 체계적인 평가, 후보자의 경험을 저해하지 않으면서 채용까지 걸리는 시간을 단축할 수 있는 도구를 원하고 있습니다. 따라서 기존 채용 시스템 내에서 선발, 검증, 워크플로우 조정을 연계할 수 있는 벤더가 더욱 뚜렷한 우위를 점하고 있습니다.

HR 헬프데스크에서 직원용 셀프 서비스형 코파일럿으로의 전환

티켓 기반의 인사 지원에서 대화형 직원 지원으로의 전환에 따라, 급여, 사내 규정, 휴가, 복리후생과 관련된 일상적인 문의에 대한 조직의 대응 방식이 변화하고 있습니다. 2025년 10월, Interact Software와 Leena AI는 직원들이 단일 인터페이스를 통해 HRIS, ITSM, ERP, CRM 시스템에 걸쳐 있는 지식에 접근하고 조치를 취할 수 있는 ‘에이전트형 직원 경험’ 솔루션을 발표했습니다. 이 모델은 HR용 AI 코파일럿 시장의 광범위한 추세와 부합하며, 구매자들은 HR 서비스 인력을 늘리는 대신 서비스 대기 시간을 단축해 주는 프런트엔드 어시스턴트를 점점 더 선호하는 추세입니다. 또한, 이러한 코파일럿은 직원들과의 상호작용과 관련된 데이터를 지속적으로 생성하므로, 고용주는 반복적으로 발생하는 정책상의 미비점, 관리직과의 마찰 요인, 서비스의 병목 현상 등을 조기에 파악할 수 있게 됩니다. 그 가치는 비용 관리에 그치지 않고, 대응 속도와 일관성은 직원들의 신뢰와도 직결되기 때문입니다. 그 결과, 각 벤더사는 보다 심층적인 워크플로우, 보다 광범위한 시스템 지원 범위, 그리고 사람이 직접 검토하는 단계로 명확하게 에스컬레이션되는 절차를 갖춘 셀프 서비스 도구를 개발하고 있습니다.

채용 결정에 따른 편향, 설명 가능성 및 감사 위험

고용 결정에는 법적, 평판, 거버넌스 측면에서 직접적인 영향이 따르기 때문에 편향의 위험은 여전히 AI의 광범위한 도입을 가로막는 주요 요인 중 하나입니다. 콜로라도주의 SB 26-189 법안은 2026년 5월 채용 결정 후의 투명성 요건을 추가하고 있으며, 이는 규제 당국의 기대가 채용 및 승진 결정이 이루어지는 실제 단계에 점점 더 가까워지고 있음을 보여줍니다. 이는 HR용 AI 코파일럿 시장의 구매자들이 감사 로그, 모델 문서, 검토 관리, 그리고 후보자 수준에서의 설명에 대해 더욱 까다로운 질문을 제기하고 있음을 의미합니다. 이에 대해 각 벤더사는 공식적인 거버넌스 프로그램이나 외부 규격 준수 등을 통해, 책임 있는 AI에 대한 인증 정보를 보다 명확히 제시함으로써 대응하고 있습니다. Eightfold AI는 자사의 면접 프로세스가 뉴욕시 지방법 제144호, 일리노이주 BIPA 및 ISO/IEC 42001을 준수하도록 구축함으로써, 제품의 신뢰성이 어떻게 상업적 경쟁의 한 요소로 자리 잡고 있는지를 보여주었습니다. 그 결과, 설명 가능성은 더 이상 법적 부가 사항이 아니라, 조달 및 도입 속도에 직접적인 영향을 미치는 요인이 되는 시장이 형성되고 있습니다.

부문별 분석

2025년 HR용 AI 코파일럿 시장 규모에서 소프트웨어가 72.89%의 점유율을 차지했습니다. 이는 구매자들이 여전히 독립형 자문 모델보다 플랫폼 주도형 도입을 훨씬 더 선호하고 있음을 보여줍니다. 가장 큰 수익원은 여전히 채용 및 HCM(인적 자원 관리) 워크플로우에 통합된 핵심 코파일럿 플랫폼, 인재 인텔리전스 엔진, 그리고 대화형 에이전트에 집중되어 있습니다. 시장의 이 부문은 반복 가능한 자동화, 통합 관리, 그리고 사용자에게 친숙한 시스템 내에서의 손쉬운 도입에 대한 기업 수요 덕분에 혜택을 보고 있습니다. 벤더들도 워크플로우와의 보다 긴밀한 통합을 통해 입지를 강화하고 있으며, 예를 들어 Eightfold AI와 Oracle Fusion Cloud Recruiting의 연동을 통해 기존 채용 환경 내에서 자율적인 면접을 실시할 수 있게 되었습니다.

서비스 분야는 2031년까지 연평균 성장률(CAGR) 17.04%로 확대될 것으로 예상되며, HR용 AI 코파일럿 시장에서 가장 두드러진 성장을 보일 것으로 전망됩니다. 이러한 성장의 배경에는 지속적인 기술 지원이나 변경 대응 없이 코파일럿을 기존의 ATS(채용 관리 시스템), 급여 계산, HR 서비스 및 직원 데이터 시스템에 연동하는 데 따르는 실무상의 어려움이 있습니다. 또한 기업은 초기 도입 후에도 서비스 수요를 유지하기 위해 이용 사례 설계, 프롬프트 거버넌스, 배포 계획, 직원 교육 및 도입 후 최적화에 관한 지원이 필요합니다. Gloat사가 2026년에 플랫폼을 출시한 것은 Microsoft 365 Copilot, Teams, Slack, Google Chat, Workday, SAP SuccessFactors, Oracle 등과의 연동을 통해 통합 범위가 얼마나 넓어졌는지를 보여주고 있으며, 이러한 복잡성이 HR용 AI 코파일럿 업계 전체에서 더 큰 서비스 역할을 뒷받침하고 있음을 알 수 있습니다.

2025년 HR용 AI 코파일럿 시장 규모 중 채용 및 인재 확보가 31.28%를 차지했으며, 이는 채용이 여전히 자동화와 측정 가능한 성과를 얻기 위한 가장 명확한 진입점임을 반영하고 있습니다. 이 도구를 통해 채용 심사 속도가 향상되고, 수작업으로 이루어지던 일정 조정이 줄어들며, 대규모 지원자 풀 전반에 걸쳐 채용 담당자의 업무 범위가 확대됨에 따라, 고용주는 그 가치를 신속하게 실감할 수 있습니다. Greenhouse사는 Ezra AI Labs 인수를 통해 2023년 이후 리크루터 1인당 지원 건수가 412% 증가했다고 보고했으며, 이는 채용 스택이 여전히 가장 큰 용도 영역인 이유를 보여줍니다. 채용 기간이나 채용 담당자의 생산성을 직접 추적할 수 있는 경우, 구매 결정의 정당성을 입증하기가 가장 쉬워지기 때문에 채용 분야는 HR용 AI 코파일럿 시장에서 계속해서 중심적인 위치를 차지하고 있습니다.

성과 관리는 2031년까지 연평균 성장률(CAGR) 15.99%로 확대될 것으로 예상되며, HR용 AI 코파일럿 시장에서 가장 빠르게 성장하는 분야가 될 것입니다. 이러한 성장은 지속적인 피드백, 평가 기준 조정 지원, 관리자의 지도, 그리고 분산형 팀 전체에 걸쳐 보다 일관된 평가 프로세스에 대한 수요와 밀접한 관련이 있습니다. 기업들이 정기적인 평가 주기에만 의존하지 않고, 목표, 역량 격차 및 역량 개발 활동에 대해 보다 명확한 가시성을 추구함에 따라, 이러한 활용 사례가 확대되고 있습니다. 학습·개발, 온보딩, 인재 계획, 인사 관리가 용도 구성의 나머지 부분을 계속 차지하고 있으며, 현재 많은 도입 사례에서 이러한 기능들이 연동됨으로써 채용, 성과, 개발 관련 데이터를 상호 간에 활용할 수 있게 되었습니다. 장기적으로는 이러한 광범위한 워크플로우 연동을 통해 용도 확장이 HR용 AI 코파일럿 업계 전반의 수익 확대에 있어 주요 원천이 될 것입니다.

지역별 분석

2025년, 북미는 36.55%의 점유율을 기록했으며, HR용 AI 코파일럿 시장에서 가장 높은 지역 점유율을 차지했습니다. 이 지역은 탄탄한 HR 기술 생태계, 기업용 소프트웨어에 대한 꾸준한 지출, 그리고 미국 내 지속적인 채용 수요의 혜택을 누리고 있습니다. 노동통계국의 보고에 따르면, 2026년 초에는 690만 건의 구인 공고가 있는 반면, 월간 채용 건수는 560만 건에 그치고 있어, 이에 따라 채용 효율 향상은 기업의 최우선 과제로 계속해서 중요한 위치를 차지하고 있습니다. 미국은 여전히 주요 수요 시장이지만, 캐나다와 멕시코에서도 관심이 높아지고 있어, 이중언어 구사자 및 현장 직원에 대한 채용 수요가 증가하고 있습니다. 주 차원의 규제로 인해 구매자에 대한 심사가 더욱 엄격해지고 있으며, 콜로라도주 등의 요건으로 인해 투명성과 심사 관행에 대한 관심이 높아지고 있습니다.

유럽은 HR용 AI 코파일럿 시장에 있어 여전히 중요한 지역이지만, 그 도입은 거버넌스 강화 및 직원 보호 체계 구축과 병행하여 진행되고 있습니다. EU AI법에 따르면, 2026년 8월 2일 이후 고용 의사결정 지원 도구가 고위험 범주로 분류됨에 따라, 문서화, 규정 준수 절차 및 인적 감독의 중요성이 강조되고 있습니다. 따라서 유럽 시장에서는 워크플로우 자동화 자체뿐만 아니라 설명 가능성, 지역 내 호스팅, 그리고 도입 관리가 중요하게 여겨지게 됩니다. 독일, 영국, 프랑스가 계속해서 해당 지역 수요를 주도하고 있지만, 직원 모니터링, 의사결정 지원, 혹은 국경을 넘는 데이터 활용이 관련된 경우, 해당 지역의 구매자들은 보다 신중한 태도를 보이고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 16.41%로 성장할 것으로 예상되며, HR용 AI 코파일럿 시장 규모 측면에서 가장 빠르게 성장하는 지역 부문이 될 것입니다. 인도는 전 세계 역량 센터의 확장에 힘입어 2031년까지 연평균 성장률(CAGR)이 12.2%를 나타낼 것으로 전망되며, 국가별 시장 중 가장 빠르게 성장하고 있는 시장입니다. 같은 정보원에 따르면, 불필요한 자격 요건 필터를 제거함으로써 인도에서는 후보자 풀을 11.4배, 인도네시아에서는 9.5배로 확대할 수 있는 것으로 나타났으며, 이는 AI 기반 선별 과정 및 다국어 지원 채용 도구의 도입을 뒷받침하는 근거가 되고 있습니다. 중국은 후보자 데이터의 거버넌스 및 감사 대응이 시스템 설계 단계에서 점점 더 중요해지고 있기 때문에 여전히 중요한 시장입니다. 한편, 일본과 한국에서는 자동화를 촉진하는 인력 부족 현상이 계속되고 있습니다. 남미, 중동 및 아프리카은 현재 수익 규모는 아직 작지만, 모바일 우선 인사 플랫폼, 각국의 AI 프로그램, 현지 언어 지원 기능의 향상으로 인해 도입 가능성이 높아지면서 도입이 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the aI copilot for HR market size is expected to grow from USD 1.23 billion in 2025 to USD 1.42 billion in 2026 and is forecast to reach USD 2.86 billion by 2031 at 15.11% CAGR over 2026-2031.

This report is Segmented by Component (Software, and Services), Application (Payroll, Benefits and HR Administration, and More), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Banking, Financial Services, and Insurance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI Copilot For HR Market Trends and Insights

Recruitment-Volume Automation and Time-To-Hire Compression

Recruitment workflows are becoming harder to manage manually as generative tools enable candidates to produce and submit more applications in less time. Greenhouse said applications per recruiter had risen 412% since 2023, which shows how sharply screening pressure has increased for hiring teams. This pressure is pushing the AI copilot for HR market toward automated shortlisting, voice-led screening, interview scheduling, and candidate communication that can run with less recruiter intervention. The strongest demand is coming from roles where speed matters and recruiter bandwidth is limited, especially in frontline and hourly hiring. Employers are also looking for tools that can compress time-to-hire without weakening audit trails, structured evaluation, or candidate experience. Vendors that can connect screening, validation, and workflow orchestration inside existing recruiting systems are therefore gaining a clearer advantage.

Shift from HR Helpdesks to Employee Self-Service Copilots

The move from ticket-based HR support to conversational employee assistance is changing how organizations handle routine questions on payroll, policies, leave, and benefits. In October 2025, Interact Software and Leena AI introduced an agentic employee experience offering that enabled employees to access knowledge and complete actions across HRIS, ITSM, ERP, and CRM systems through a single interface. That model fits a broader pattern in the AI copilot for HR market, where buyers increasingly prefer front-end assistants that reduce service queues instead of adding more HR service headcount. These copilots also generate a steady stream of employee interaction data, helping employers spot recurring policy gaps, manager friction points, and service bottlenecks earlier. The value is not limited to cost control because response speed and consistency matter to employee trust as well. As a result, vendors are building self-service tools with stronger workflow depth, broader system reach, and clearer escalation paths to human review.

Bias, Explainability, and Audit Exposure in Employment Decisions

Bias risk remains one of the main brakes on wider deployment because employment decisions carry direct legal, reputational, and governance consequences. Colorado's SB 26-189 added post-decision transparency requirements in May 2026, indicating that regulatory expectations are moving closer to the actual points of hiring and promotion decisions. This means buyers in the AI copilot for HR market are asking harder questions about audit logs, model documentation, review controls, and candidate-level explanation. Vendors are responding by making responsible AI credentials more visible, including through formal governance programs and support for external standards. Eightfold AI positioned its interview process to comply with NYC Local Law 144, Illinois BIPA, and ISO/IEC 42001, demonstrating how product trust is becoming part of commercial competition. The result is a market where explainability is no longer a legal footnote but a direct factor in procurement and rollout speed.

Other drivers and restraints analyzed in the detailed report include:

- Skills Intelligence, and Internal Mobility Orchestration

- Need for Multilingual Frontline Hiring and Support at Scale

- Sensitive HR Data Privacy and Cross-Border Governance Burdens

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 72.89% share of the AI copilot for HR market size in 2025, which shows how strongly buyers still prefer platform-led deployments over stand-alone advisory models. The largest revenue pool remains tied to core copilot platforms, talent intelligence engines, and conversational agents that sit inside recruiting and HCM workflows. This part of the market benefits from enterprise demand for repeatable automation, centralized administration, and easier user adoption inside familiar systems. Product vendors are also strengthening their position through tighter workflow integration, such as Eightfold AI's connection with Oracle Fusion Cloud Recruiting, which keeps autonomous interviewing inside established recruiting environments.

Services are projected to expand at 17.04% CAGR through 2031, making them the fastest-growing component in the AI copilot for HR market. The rise comes from the practical difficulty of connecting copilots to legacy ATS, payroll, HR service, and workforce data systems without ongoing technical and change support. Enterprises also need help with use-case design, prompt governance, rollout planning, employee training, and post-launch optimization to keep service demand active after the initial implementation. Gloat's 2026 platform launch showed how wide the integration surface has become, with connections across Microsoft 365 Copilot, Teams, Slack, Google Chat, Workday, SAP SuccessFactors, and Oracle, and that complexity supports a larger services role across the AI copilot for HR industry.

Recruitment and talent acquisition accounted for 31.28% of the AI copilot for HR market size in 2025, reflecting that hiring remains the clearest entry point for automation and measurable returns. Employers can see the value quickly when tools improve screening speed, reduce manual scheduling, and widen recruiter coverage across large applicant pools. Greenhouse linked its Ezra AI Labs acquisition to a 412% increase in applications per recruiter since 2023, which shows why the recruiting stack remains the largest application area. This keeps recruitment at the center of the AI copilot for HR market because buying decisions are often easiest to justify when time-to-fill and recruiter productivity can be tracked directly.

Performance management is projected to advance at 15.99% CAGR through 2031, making it the fastest-growing application in the AI copilot for HR market. Growth here is tied to demand for continuous feedback, calibration support, manager guidance, and more consistent evaluation processes across distributed teams. This use case is moving forward because enterprises want better visibility into goals, capability gaps, and development actions without depending only on periodic review cycles. Learning and development, onboarding, workforce planning, and HR administration continue to hold the rest of the application mix, and many deployments now connect these functions so hiring, performance, and development data can inform one another. Over time, this broader workflow connection should make application expansion a major source of revenue depth across the AI copilot for HR industry.

Geography Analysis

North America accounted for 36.55% share in 2025, giving it the largest regional position in the AI copilot for HR market. The region benefits from a deep HR technology ecosystem, strong enterprise software spending, and persistent hiring pressure in the United States. The Bureau of Labor Statistics reported 6.9 million open positions against 5.6 million monthly hires in early 2026, which kept recruiting efficiency high on the corporate agenda.The United States remains the main demand center, while Canada and Mexico are also seeing stronger interest, with bilingual and frontline hiring needs rising. State-level rules are adding another layer of buyer scrutiny, with requirements in places such as Colorado increasing attention on transparency and review practices.

Europe remains an important region for the AI copilot for HR market, but adoption is moving alongside tighter governance and stronger employee protection frameworks. The EU AI Act classifies employment decision-support tools as high risk from August 2, 2026, underscoring the importance of documentation, conformity processes, and human oversight. This makes Europe a market where explainability, regional hosting, and deployment controls can matter as much as workflow automation itself. Germany, the United Kingdom, and France continue to shape regional demand, but buyers across the region are moving more carefully when employee monitoring, decision support, or cross-border data use is involved.

Asia-Pacific is projected to grow at 16.41% CAGR through 2031, making it the fastest-growing regional slice of the AI copilot for HR market size. India is the fastest-growing country market, supported by the expansion of global capability centers and a 12.2% projected CAGR through 2031. The same source noted that removing unnecessary qualification filters can expand candidate pools by 11.4x in India and 9.5x in Indonesia, which strengthens the case for AI-led screening and multilingual hiring tools. China remains important because candidate data governance and audit readiness are becoming more central to deployment design, while Japan and South Korea continue to face labor scarcity that supports automation. South America, the Middle East, and Africa remain smaller in current revenue terms, but adoption is expanding as mobile-first HR platforms, national AI programs, and local-language capabilities improve deployment feasibility.

- Phenom People, Inc.

- Eightfold AI Inc.

- Beamery, Inc.

- Avature Limited

- Paradox, Inc.

- HumanlyHR Inc. d/b/a Humanly

- Textio, Inc.

- Leena AI Inc.

- Gloat Ltd.

- ZipStorm, Inc. (SeekOut)

- HireVue, Inc.

- Visier Solutions Inc.

- Retrain AI Inc.

- Draup, Inc.

- Wisq, Inc.

- Cleary Technologies, Inc.

- Riminder, societe par actions simplifiee (HrFlow.ai)

- Dovetail Software, Inc.

- AssessFirst SAS

- Explore & Beyond Inc. (Talentpilot)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Recruitment-Volume Automation and Time-to-Hire Compression

- 4.2.2 Shift From HR Helpdesks to Employee Self-Service Copilots

- 4.2.3 Skills Intelligence and Internal Mobility Orchestration

- 4.2.4 Need for Multilingual Frontline Hiring and Support at Scale

- 4.2.5 Compliance-by-Design Demand as AI Employment Rules Tighten

- 4.2.6 Workforce Data Layer Modernization Unlocking Embedded Copilots

- 4.3 Market Restraints

- 4.3.1 Bias, Explainability, and Audit Exposure in Employment Decisions

- 4.3.2 Sensitive HR Data Privacy and Cross-Border Governance Burdens

- 4.3.3 Fragmented HR Data and Legacy HCM Integration Bottlenecks

- 4.3.4 Entry-Level Hiring Distortion From AI-Generated Applications and Screening Noise

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Core AI Copilot Platforms

- 5.1.1.2 Talent Intelligence and Matching Engines

- 5.1.1.3 Conversational Agents and Workflow Orchestration

- 5.1.1.4 Analytics and Insights Modules

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration Services

- 5.1.2.2 Training and Change Management Services

- 5.1.2.3 Managed and Optimization Services

- 5.1.1 Software

- 5.2 By Application

- 5.2.1 Recruitment and Talent Acquisition

- 5.2.2 Employee Onboarding and Engagement

- 5.2.3 Performance Management

- 5.2.4 Learning and Development

- 5.2.5 Workforce Planning and Analytics

- 5.2.6 Payroll, Benefits and HR Administration

- 5.2.7 Other Applications

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Based

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-Sized Enterprises

- 5.5 By End-user Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 Banking, Financial Services, and Insurance

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Retail and E-commerce

- 5.5.5 Manufacturing

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Southeast Asia

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Phenom People, Inc.

- 6.4.2 Eightfold AI Inc.

- 6.4.3 Beamery, Inc.

- 6.4.4 Avature Limited

- 6.4.5 Paradox, Inc.

- 6.4.6 HumanlyHR Inc. d/b/a Humanly

- 6.4.7 Textio, Inc.

- 6.4.8 Leena AI Inc.

- 6.4.9 Gloat Ltd.

- 6.4.10 ZipStorm, Inc. (SeekOut)

- 6.4.11 HireVue, Inc.

- 6.4.12 Visier Solutions Inc.

- 6.4.13 Retrain AI Inc.

- 6.4.14 Draup, Inc.

- 6.4.15 Wisq, Inc.

- 6.4.16 Cleary Technologies, Inc.

- 6.4.17 Riminder, societe par actions simplifiee (HrFlow.ai)

- 6.4.18 Dovetail Software, Inc.

- 6.4.19 AssessFirst SAS

- 6.4.20 Explore & Beyond Inc. (Talentpilot)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment