|

시장보고서

상품코드

2065437

헬스케어 연합학습 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Federated Learning In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

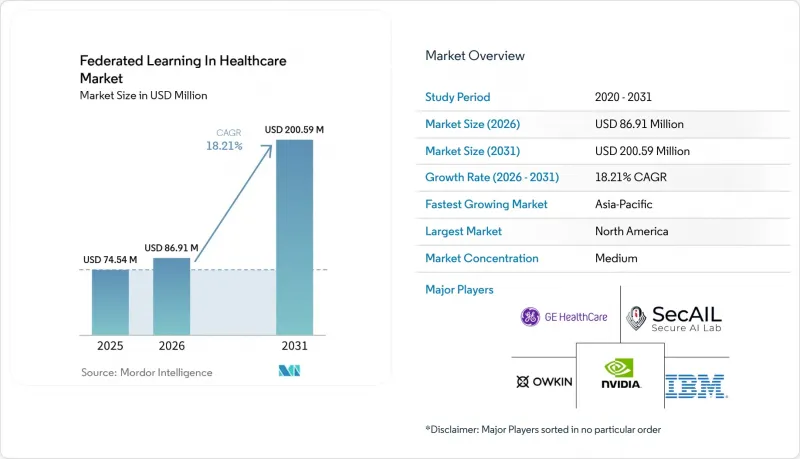

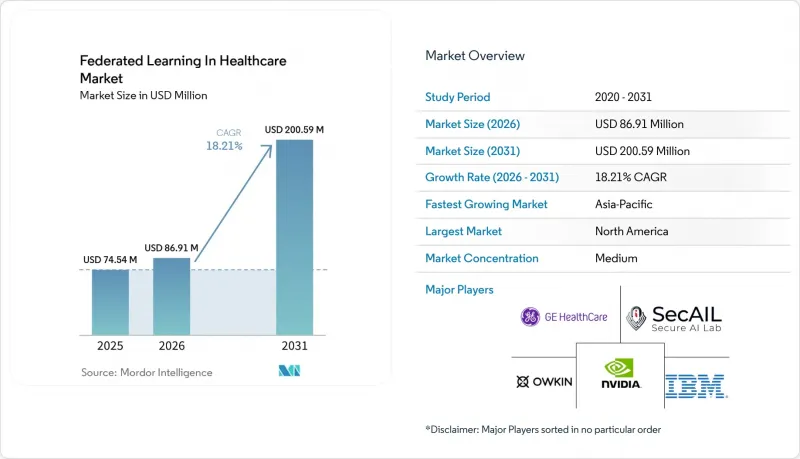

헬스케어 연합학습 시장 규모는 2025년에 7,454만 달러로 평가되었고, 2026년에 8,691만 달러로 추정되고, 2031년까지 2억 59만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 18.21%로 성장할 전망입니다.

본 보고서는 구성 요소별(소프트웨어 플랫폼, 인프라, 서비스), 도입 형태별(온프레미스, 클라우드 기반, 하이브리드), 용도별(신약 개발, 의료 영상, 전자건강기록(EHR) 분석, 원격 모니터링, 임상시험), 최종 사용자별(병원, 제약·바이오기술 기업 등), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카(MEA), 남미)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 헬스케어 연합학습 시장 동향 및 인사이트

개인정보 보호 규제에 힘입은 분산형 AI 도입

데이터 보호 관련 규정은 단순한 규정 준수 차원의 배경적 조치에서 헬스케어 연합학습(Federated Learning) 시장 전반에 걸친 핵심 아키텍처 결정으로 전환되고 있습니다. 미국과 유럽의 병원 및 의료 네트워크는 기관 간 및 국경을 초월한 원시 환자 데이터 전송을 피해야 한다는 압박을 점점 더 강하게 받고 있으며, 이로 인해 임상 현장에서 중앙 집중식 AI 훈련을 정당화하기가 어려워지고 있습니다. 『Scientific Reports』지에 게재된 2026년 연구에 따르면, 차분 프라이버시와 동형 암호화를 활용한 페더레이티드 프레임워크는 프라이버시 보호 기능이 없는 페더레이티드 기준 모델과 비교하여 멤버십 추론 위험을 20%에서 5%로 낮춘 것으로 나타났으며, 이는 유용성 측면에서 큰 타협 없이도 개인정보를 보호하는 모델 개발이 가능함을 입증하고 있습니다. 유럽의 정책은 이러한 전환을 더욱 촉진하고 있습니다. 왜냐하면 EHDS(유럽 헬스케어 데이터 전략)는 2차 이용 및 국경을 초월한 접근에 관한 공식적인 체계를 구축하고 있으며, 이는 원시 데이터의 통합보다는 분산형 분석과 더 자연스럽게 부합하기 때문입니다. 이로 인해 의료 서비스 제공업체들은 감사 가능성, 추적 가능성, 거버넌스 관리 기능을 이미 갖춘 플랫폼을 요구하게 되었으며, 소프트웨어 구매 주기가 수년 단위로 장기화되고 있습니다. 소규모 병원이나 지역 의료 시스템의 경우, 공급업체가 관리형 배포 모델을 통해 법적, 기술적, 업무 흐름상의 복잡성을 해소해 줄 수 있다면, 의료 분야의 연합 학습 시장은 특히 매력적입니다.

데이터 풀 없이 다기관 영상 진단 모델 확장

영상 진단은 헬스케어 연합학습 시장에서 가장 뚜렷한 초기 수요원 중 하나입니다. 이는 방사선과 및 병리학 데이터가 가치가 높지만, 공유하기 어렵기 때문입니다. 기존의 다기관 간 영상 진단 연계에서는 계약 체결, 책임 소재 검토, 그리고 현지 거버넌스 승인 단계에서 종종 지연이 발생하며, 그 결과 통합된 데이터를 활용한 모델 훈련이 지연되거나 중단되는 경우가 있습니다. 2026년 2월 『npj Digital Medicine』지에 게재된 연구에 따르면, 페더레이티드 러닝과 여러 거점 간을 이동하는 모델(트래블링 모델)의 접근 방식을 결합함으로써 오분류 편차가 34%에서 26%로 감소하는 동시에 균형 정확도도 향상된 것으로 밝혀졌습니다. 이는 분산형 훈련이 견고성과 공정성 모두를 향상시킬 수 있음을 보여줍니다. GE 헬스케어가 매사추세츠 종합병원 브라이햄 및 위스콘신 대학교 매디슨 캠퍼스와 공동으로 20만 건 이상의 다기관 영상 데이터를 활용해 학습시킨 3D MR 기반 모델에 대한 이 프로젝트는 의료 시스템이 영상 아카이브를 고립된 로컬 자산이 아닌 공유된 학습 인프라로 취급하기 시작했음을 보여줍니다. 이로 인해 여전히 단일 시설의 데이터 세트에 의존하고 있는 공급업체들에게는 진입 장벽이 높아지고 있습니다. 특히, 성능 격차가 금방 드러나기 쉬운 방사선과나 병리학 분야에서는 이러한 경향이 두드러집니다. 그 결과, 헬스케어 연합학습(Federated Learning) 시장에서는 개인정보 보호의 중요성은 물론, 원본 스캔 데이터를 공개하지 않고도 더 많은 의료 기관이 참여할 수 있게 됨에 따라 모델의 품질이 향상되었기 때문에 영상 진단을 중심으로 한 도입이 확대되고 있습니다.

비독립동분포(Non-IID) 임상 데이터의 불균일성과 모델의 드리프트

의료 분야의 연합 학습 시장에서 가장 뿌리 깊은 기술적 제약은 서로 다른 기관에서 수집된 임상 데이터 세트 간의 불일치입니다. 병원마다 영상 진단 프로토콜, 장비 공급업체, 코딩 관행, 환자 구성, 라벨 품질 등이 다르기 때문에 표준적인 집계 기법을 사용한다고 해서 반드시 모든 참여 기관에서 균일하게 일반화할 수 있는 모델을 얻을 수 있는 것은 아닙니다. 2025년 4월 『Nature Communications』지에 게재된 'Federated Tumor Segmentation Challenge' 조사에 따르면, 적응형 집계 알고리즘은 페더레이션 전체에서는 평균적으로 양호한 성능을 발휘하는 반면, 특정 의료기관에서는 여전히 유의미한 성능 저하가 나타나는 것으로 밝혀졌습니다. 이는 연방의 평균 성능이 국소적인 위험을 가려버릴 가능성이 있음을 의미하며, 임상팀이 단순히 강력한 통합 벤치마크뿐만 아니라 각 병원에서 신뢰할 수 있는 결과를 필요로 할 경우, 이는 심각한 문제가 됩니다. 2026년 초에 실시된 드리프트를 고려한 미세 조정 관련 연구는 더 나은 방향성을 제시하고 있지만, 의료 현장에서 시설 수준의 조정 민감도가 여전히 중요한 과제임을 밝혀내고 있습니다. 그 결과, 헬스케어 연합학습(Federated Learning) 시장에서는 장기적으로 시설별 모니터링, 재조정, 검증 워크플로를 유지할 수 있는 충분한 자원을 보유한 학술 기관이나 대규모 의료 시스템이 여전히 유리한 입지를 차지하고 있습니다.

부문별 분석

2022년, 소프트웨어 플랫폼은 구성 요소별 매출의 52.38%를 차지했으며, 이에 따라 이 부문은 헬스케어 분야의 연방 학습 시장에서 가장 큰 점유율을 확보했습니다. 수요를 견인한 주요 요인은 병원이 자체적으로 구축하는 것이 아니라 지원 서비스가 포함된 제품 형태로 조달할 수 있는 오케스트레이션, 모델 통합, 개인정보 보호 도구 및 거버넌스 기능에 대한 수요였습니다. 또한, 많은 의료 서비스 제공업체들이 사내에 고도의 연합 엔지니어링 팀을 구축하지 않고도 기존의 규정 준수 프로세스에 부합하는 턴키 환경을 원했기 때문에 조달 동향 역시 소프트웨어를 선호하는 경향을 보였습니다. NVIDIA FLARE, Flower, PySyft 등의 오픈소스 프레임워크는 기술적 접근성을 확대했지만, 한편으로는 워크플로우 통합, 모니터링, 감사 가능성, 도입 지원을 통해 차별화를 꾀하도록 상용 벤더에 대한 압박도 커지고 있습니다.

서비스는 가장 빠르게 성장하고 있는 구성 요소이며, 헬스케어 연합학습(Federated Learning) 서비스 시장 규모는 2026-2031년 연평균 성장률(CAGR) 19.16%로 확대될 것으로 전망됩니다. 이러한 추세는 많은 의료 기관이 소프트웨어를 구매할 수는 있지만, 설정, 검증, 거버넌스 매핑, 교육 및 운영, 그리고 지속적인 MLOps 지원에 대해서는 여전히 외부 지원이 필요하다는 사실을 반영하고 있습니다. 의료 분야의 구매자들은 단순히 소프트웨어 라이선스에 대한 접근 권한뿐만 아니라 책임감 있는 도입 성과를 요구하고 있기 때문에 관리형 제공의 중요성이 커지고 있습니다. 또한, 벤더들이 분산 환경 전반에 걸친 추론 라우팅, 모니터링, 페더레이션 관리를 점점 더 많이 지원하게 됨에 따라, 서비스의 범위가 도입 단계에서 실행 단계의 운영으로 전환되고 있는 것도 바로 이 때문입니다. 앞으로 헬스케어 분야의 페더레이티드 러닝 시장에서 서비스 제공업체들이 페더레이티드 AI를 완전히 독자적으로 운영하는 툴셋이 아닌 관리형 인프라로 취급하게 됨에 따라, 서비스 수익이 소프트웨어 수익과의 격차를 점차 좁혀갈 것으로 보입니다.

2025년에는 온프레미스 배포가 57.61%의 점유율을 차지했으며, 헬스케어 분야의 연방 학습 시장에서 주요 배포 형태로 자리 잡았습니다. 이 결과는 보호 대상 의료 정보를 기관 내부에 보관하고, 기존 PACS, 스토리지 및 로컬 GPU에 대한 투자를 새로운 AI 워크플로우로 확장하고자 하는 병원 측의 오랜 의향을 반영한 것입니다. 많은 대학 병원의 경우, 온프레미스 구축은 완전히 새로운 설비 투자 결정이라기보다는 기존의 영상 분석 및 연구 인프라의 자연스러운 연장선상에 있었습니다. 또한, 리스크 관리 담당자들도 내부 승인 절차가 간소화되고, 모델 개발 과정에서 제3자의 접근에 대한 우려가 줄어들기 때문에 현지에서 관리하는 것을 선호하는 경향이 있었습니다.

클라우드 기반 도입은 가장 빠르게 성장하고 있는 형태이며, 헬스케어 연합학습(Federated Learning) 시장 중 클라우드 기반 도입 규모는 2031년까지 연평균 성장률(CAGR) 18.83%로 확대될 것으로 전망됩니다. 이러한 성장은 병원이 데이터를 처리하는 동안 데이터를 보호하고, 공유 인프라 내 워크로드의 무결성을 검증할 수 있게 해주는 기밀 컴퓨팅 도구에 의해 뒷받침되고 있습니다. 또한 유럽에서는 헬스케어 데이터 접근에 관한 체계가 성숙해짐에 따라, 클라우드 상에 존재하는 안전한 처리 환경을 위한 규제 체계가 마련되고 있으며, 이를 통해 하이브리드형이나 원격 오케스트레이션 모델을 검토하는 서비스 제공업체의 정책적 불확실성이 줄어들고 있습니다. 따라서 클라우드 수준의 연동을 추구하면서도, 로컬에서의 계산 처리나 원시 데이터를 현장에 보관하고자 하는 멀티사이트 네트워크에서 하이브리드형 도입이 확산되고 있습니다. 헬스케어 연합학습(Federated Learning) 업계에서는 도입 방식의 선택이 더 이상 ‘클라우드 대 온프레미스’라는 이념적 대립의 문제가 아니라, 거버넌스, 규모, 통합 준비 상황에 가장 적합한 모델이 무엇인지에 초점이 맞추어지고 있습니다.

지역별 분석

2025년, 북미는 헬스케어 분야의 페더레이티드 러닝 시장에서 41.42%를 차지했으며, 지역별로는 가장 큰 점유율을 기록했습니다. 이 지역은 학술 의료 센터가 밀집해 있고, HIPAA에 기반한 확립된 거버넌스 프로세스가 갖춰져 있으며, 헬스케어 및 생명과학 분야의 연합형 플랫폼이 조기에 상용화되고 있다는 등의 장점이 있습니다. 미국은 강력한 AI 인프라, 기업용 소프트웨어의 적극적인 도입, 그리고 생의학 및 제약 분야에서 NVIDIA FLARE와 같은 주목할 만한 실제 운영 사례를 모두 갖추고 있어 여전히 핵심 수익원으로 자리 잡고 있습니다. 캐나다 역시 연구 주도형 협력 모델을 통해 기여하고 있지만, 멕시코의 경우 많은 의료 제공 환경에서 병원의 디지털화와 고급 분석 인프라가 아직 성숙 단계에 이르지 못해 도입은 초기 단계에 머물러 있습니다.

유럽에서는 정책 설계가 인프라 수요를 직접 형성하고 있기 때문에 헬스케어 분야의 연방 학습 시장에서 구조적 중요성이 커지고 있습니다. 규정(EU) 2025/327에 따라 유럽 건강 데이터 공간(European Health Data Space)이 구축되었으며, 각 회원국에 건강 데이터 접근 기관이 설치되고, 국경을 초월한 2차 활용을 위한 HealthData&EU가 공식적으로 제정되었습니다. 이에 따라, 페더레이티드 인프라는 향후 데이터 액세스 워크플로우에서 핵심적인 역할을 담당하게 될 것입니다. 독일은 ‘Gesundheitsdatennutzungsgesetz(의료 데이터 이용법)’ 및 연구 데이터 인프라와 상호 운용성의 역할에 관한 관련 노력을 바탕으로, 국내 준비 과정에서 다른 많은 국가들보다 신속하게 움직이고 있습니다. 이로 인해 유럽 시장의 특성은 북미와 달라졌습니다. 그 이유는 도입이 기업 주도로 이루어질 뿐만 아니라, 공공 규제 체계에 의해서도 형성되고 있기 때문입니다. 이러한 추세는 예측 기간 동안 거버넌스가 강화된 플랫폼, 안전한 처리 환경, 그리고 국경을 초월한 페더레이션 도구의 도입을 촉진할 것으로 예측됩니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역이며, 이 지역의 헬스케어 연합학습(Federated Learning) 시장 규모는 2031년까지 연평균 성장률(CAGR) 18.61%로 확대될 것으로 전망됩니다. 한국이 2026년 3월에 발표한 ‘국가 의료 데이터 스페이스’ 계획은 원시 데이터를 각 병원 내에 보관하면서도 안전한 다기관 간 AI 개발을 가능하게 한다는 점에서 공공 정책이 연방형 모델을 반영하기 시작했음을 보여줍니다. 대만도 주목할 만합니다. 해당 국가의 헬스케어 연합 학습 이니셔티브에서는 NVIDIA FLARE가 채택되고 있으며, 공통 오케스트레이션 계층이 선정된다면 정부 주도의 도입이 가속화될 수 있음이 밝혀졌습니다. 중국은 막대한 잠재력을 지니고 있지만, 현지 데이터 규제는 국내 관리를 유지하는 아키텍처를 우선시하고 있어, 광범위한 국경을 초월한 데이터 풀보다는 온프레미스 기반의 연동 방식을 지지하는 경향이 있습니다. 인도와 호주는 여전히 학술·의료 센터 및 암 연구 네트워크를 중심으로 한 초기 단계 시장에 머물러 있습니다. 한편, 중동 및 아프리카 수요는 GCC(걸프협력회의) 회원국들의 디지털 헬스 분야 지출에 의해 형성되고 있으며, 남미에서는 유럽식 데이터 보호 기준과 유사한 개인정보 보호 조건 하에서 브라질이 주도적인 역할을 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the federated learning in healthcare market size is projected to be USD 74.54 million in 2025, USD 86.91 million in 2026, and reach USD 200.59 million by 2031, growing at a CAGR of 18.21% from 2026 to 2031.

This report is Segmented by Component (Software Platforms, Infrastructure, Services), Deployment Mode (On-Premises, Cloud-Based, Hybrid), Application (Drug Discovery, Medical Imaging, EHR Analytics, Remote Monitoring, Clinical Trials), End User (Hospitals, Pharma & Biotech, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are in Value (USD).

Global Federated Learning In Healthcare Market Trends and Insights

Privacy Regulation-Driven Decentralized AI Adoption

Data protection rules have moved from background compliance work into core architecture decisions across the Federated learning in healthcare market. Hospitals and health networks in the United States and Europe are under rising pressure to avoid raw patient-data transfers across institutional and national boundaries, which makes centralized AI training harder to justify in clinical settings. A 2026 study in Scientific Reports showed that a federated framework using differential privacy and homomorphic encryption reduced membership-inference risk from 20% to 5% against non-private federated baselines, which supports the case for privacy-safe model development without a major utility tradeoff. European policy is pushing this shift further because the EHDS creates a formal structure for secondary use and cross-border access that aligns more naturally with distributed analytics than with raw data pooling. This is creating multi-year software buying cycles as providers look for platforms that already contain auditability, traceability, and governance controls. For smaller hospitals and regional systems, the Federated learning in healthcare market is especially attractive when vendors can absorb legal, technical, and workflow complexity through managed deployment models.

Multi-Institution Imaging Model Scaling Without Data Pooling

Imaging has become one of the clearest early demand centers in the Federated learning in healthcare market because radiology and pathology data are both valuable and difficult to share. Traditional multi-site imaging collaborations often slow down at contracting, liability review, and local governance approval, which can delay or stop pooled-data model training. A February 2026 study in npj Digital Medicine found that combining federated learning with a traveling-model approach across multiple sites reduced misclassification disparities from 34% to 26% while also improving balanced accuracy, which shows that distributed training can improve both robustness and fairness. GE HealthCare's work with Mass General Brigham and the University of Wisconsin-Madison on a 3D MR foundation model trained on more than 200,000 multi-site images shows that health systems are starting to treat imaging archives as shared training infrastructure rather than isolated local assets. That raises the bar for vendors that still depend on single-site datasets, especially in radiology and pathology, where performance gaps can become visible quickly. As a result, the Federated learning in healthcare market is seeing imaging-led adoption not only because privacy matters, but also because model quality now improves when more institutions can participate without surrendering raw scans.

Non-IID Clinical Data Heterogeneity and Model Drift

The most persistent technical restraint in the federated learning in healthcare market is the mismatch between clinical datasets collected at different sites. Hospitals vary in imaging protocols, device vendors, coding behavior, patient mix, and label quality, so standard aggregation methods do not always deliver a model that generalizes evenly across all participants. Research from the Federated Tumor Segmentation challenge, published in Nature Communications in April 2025, found that adaptive aggregation algorithms could perform well on average across a federation while still showing meaningful performance drops at specific institutions. That means average federation performance can mask local risk, which is a serious issue when clinical teams need dependable results at each hospital rather than only a strong pooled benchmark. Early 2026 work on drift-aware fine-tuning points in a better direction, but it also shows that site-level tuning sensitivity remains a live issue in medical settings. As a result, the federated learning in healthcare market still favors well-resourced academic centers and large health systems that can maintain per-site monitoring, recalibration, and validation workflows over time.

Other drivers and restraints analyzed in the detailed report include:

- Biopharma Demand for Privacy-Safe Collaborative Drug Discovery

- Cloud and Confidential Computing Stack Maturity

- Legacy EHR And PACS Integration Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software platforms held 52.38% of component revenue in 2025, which gave this layer the largest position in the Federated learning in healthcare market. The leading demand driver was the need for orchestration, model aggregation, privacy tooling, and governance functions that hospitals could procure as a supported product instead of assembling internally. Procurement behavior also favored software because many providers wanted a turnkey environment that could fit existing compliance processes without requiring a deep in-house federated engineering team. Open-source frameworks such as NVIDIA FLARE, Flower, and PySyft have widened technical access, but they have also increased pressure on commercial vendors to differentiate through workflow integration, monitoring, auditability, and implementation support.

Services is the fastest-growing component segment, with the federated learning in healthcare market size for services projected to expand at 19.16% CAGR between 2026 and 2031. That pace reflects the fact that many institutions can buy software, but still need outside help for configuration, validation, governance mapping, training operations, and ongoing MLOps support. Managed delivery is becoming more important because healthcare buyers want accountable deployment outcomes rather than only access to a software license. This is also why service scope is moving past implementation into runtime operations, as vendors increasingly support inference routing, monitoring, and federation management across distributed environments. Over time, the Federated learning in healthcare market is likely to see services narrow the distance with software revenue as providers treat federated AI as managed infrastructure rather than as a tool set they operate entirely on their own.

On-premises deployment held 57.61% share in 2025, which made it the leading mode in the federated learning in healthcare market. That result reflected long-standing hospital preferences for keeping protected health information inside institutional boundaries and extending existing PACS, storage, and local GPU investments into new AI workflows. For many academic medical centers, on-premises deployment was a natural continuation of earlier imaging analytics and research infrastructure rather than a completely new capital decision. Risk officers also tended to prefer local control because it simplified internal approval and reduced concern over third-party access during model development.

Cloud-based deployment is the fastest-growing mode, with the federated learning in healthcare market size for cloud-based deployment projected to expand at 18.83% CAGR through 2031. Growth is being supported by confidential computing tools that let hospitals protect data during active processing and verify workload integrity in shared infrastructure. Europe is also creating a regulatory pathway for cloud-resident secure processing environments as health data access frameworks mature, which lowers policy uncertainty for providers evaluating hybrid and remote orchestration models. Hybrid deployment is therefore gaining ground across multi-site networks that want cloud-level coordination while still keeping local computation and raw data on site. In the Federated learning in healthcare industry, deployment choices are becoming less about cloud versus local ideology and more about which model best matches governance, scale, and integration readiness.

Geography Analysis

North America held 41.42% of the federated learning in healthcare market share in 2025, which made it the largest regional contributor. The region benefits from a dense concentration of academic medical centers, established HIPAA-driven governance processes, and early commercial deployment of federated platforms in healthcare and life sciences. The US remains the core revenue center because it combines strong AI infrastructure, active enterprise software adoption, and visible production examples such as NVIDIA FLARE in biomedical and pharmaceutical settings. Canada is also contributing through research-led collaboration models, while Mexico remains earlier in adoption because hospital digitization and advanced analytics infrastructure are less mature across many provider environments.

Europe is gaining structural weight in the federated learning in healthcare market because policy design is directly shaping infrastructure demand. Regulation (EU) 2025/327 established the European Health Data Space, set up Health Data Access Bodies in each member state, and formalized HealthData@EU for cross-border secondary use, which makes federated infrastructure central to future data access workflows. Germany has moved faster than most peers in national preparation, building on the Gesundheitsdatennutzungsgesetz and related work around research data infrastructure and interoperability roles. This gives Europe a different market profile from North America because adoption is not only enterprise-led, it is also being shaped by public regulatory architecture. That dynamic should support procurement of governance-rich platforms, secure processing environments, and cross-border federation tools over the forecast period.

Asia-Pacific is the fastest-growing region, and the federated learning in healthcare market size for Asia-Pacific is projected to expand at 18.61% CAGR through 2031. South Korea's March 2026 plan for a national medical data space shows how public policy is starting to mirror the federated model by keeping raw data inside each hospital while enabling secure multi-institutional AI development. Taiwan is also notable because its national healthcare federated learning initiative uses NVIDIA FLARE, which shows that state-backed adoption can accelerate once a common orchestration layer is selected. China offers large potential, but local data rules favor architectures that preserve domestic control and often support on-premises federation rather than broader cross-border pooling. India and Australia remain earlier-stage markets centered on academic medical centers and cancer research networks, while the Middle East and Africa demand is being shaped by GCC digital health spending, and South America is led by Brazil under privacy conditions that resemble European-style data protection expectations.

- Duality Technologies Inc.

- FedML Inc.

- Flower Labs GmbH

- Fujitsu

- GE HealthCare Technologies Inc.

- Google LLC

- Health Catalyst

- IBM

- Intel

- Johnson & Johnson

- Koninklijke Philips

- Lifebit Biotech Ltd.

- Medtronic

- Microsoft

- NVIDIA

- Owkin

- Rhino Federated Computing

- Roche

- Secure AI Labs Inc.

- Siemens Healthineers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Privacy Regulation-Driven Decentralized AI Adoption

- 4.2.2 Multi-Institution Imaging Model Scaling Without Data Pooling

- 4.2.3 Biopharma Demand for Privacy-Safe Collaborative Drug Discovery

- 4.2.4 Cloud and Confidential Computing Stack Maturity

- 4.2.5 EHDS-Enabled Cross-Border Secondary-Use Pathways

- 4.2.6 Federated AI Registries and Algorithmic Vigilance Networks

- 4.3 Market Restraints

- 4.3.1 Non-IID Clinical Data Heterogeneity and Model Drift

- 4.3.2 Legacy EHR And PACS Integration Burden

- 4.3.3 Site-Level GPU, MLOps, and Networking Cost Burden

- 4.3.4 Model IP, Liability, And Contributor-Value Allocation Disputes

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Component

- 5.1.1 Software Platforms

- 5.1.2 Infrastructure Solutions

- 5.1.3 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud-Based

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Drug Discovery & Development

- 5.3.2 Medical Imaging & Diagnostics

- 5.3.3 Electronic Health Record & Clinical Data Analytics

- 5.3.4 Remote Patient Monitoring

- 5.3.5 Clinical Trial Optimization

- 5.4 By End User

- 5.4.1 Hospitals & Health Systems

- 5.4.2 Pharmaceutical & Biotechnology Companies

- 5.4.3 Research & Academic Institutions

- 5.4.4 Diagnostic Laboratories & Imaging Networks

- 5.4.5 Contract Research Organizations

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Duality Technologies Inc.

- 6.3.2 FedML Inc.

- 6.3.3 Flower Labs GmbH

- 6.3.4 Fujitsu Limited

- 6.3.5 GE HealthCare Technologies Inc.

- 6.3.6 Google LLC

- 6.3.7 Health Catalyst Inc.

- 6.3.8 IBM Corporation

- 6.3.9 Intel Corporation

- 6.3.10 Johnson & Johnson

- 6.3.11 Koninklijke Philips N.V.

- 6.3.12 Lifebit Biotech Ltd.

- 6.3.13 Medtronic plc

- 6.3.14 Microsoft Corporation

- 6.3.15 NVIDIA Corporation

- 6.3.16 Owkin

- 6.3.17 Rhino Federated Computing

- 6.3.18 Roche Holding AG

- 6.3.19 Secure AI Labs Inc.

- 6.3.20 Siemens Healthineers AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment