|

시장보고서

상품코드

2065440

디지털 맘모그래피 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Digital Mammography - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

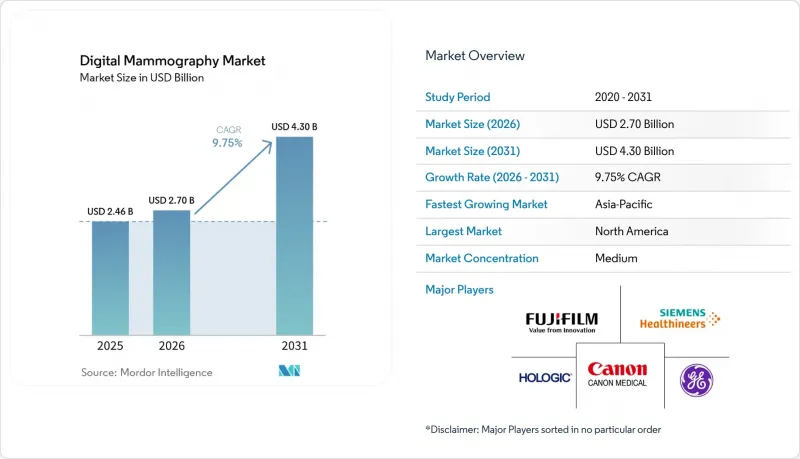

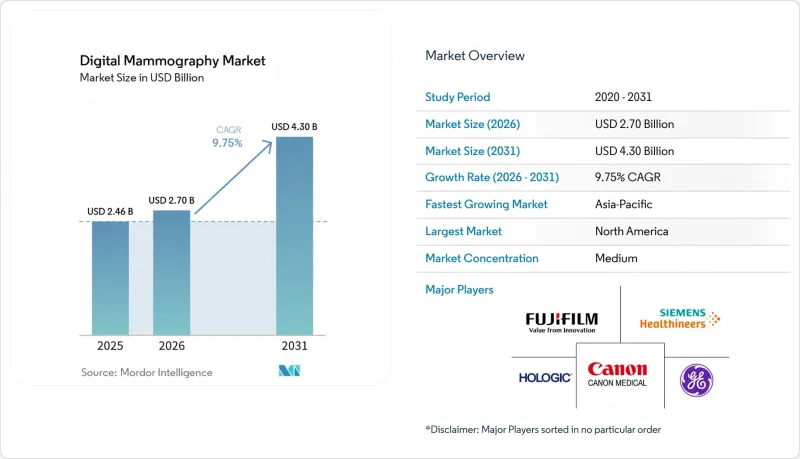

Mordor Intelligence에 의하면, 디지털 맘모그래피 시장 규모는 2025년 24억 6,000만 달러로 평가되었고, 2026년에는 27억 달러로 추정되고, 2026-2031년 CAGR 9.75%로 성장을 지속할 전망이며, 2031년에는 43억 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형별(디지털 시스템, 3D 유방 토모신테시스 시스템 등), 기술별(2D FFDM, 3D DBT 등), 용도별(선별 검사, 진단 등), 최종 사용자별(병원, 영상진단센터 등), 지역별(북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카)로 분류되어 있습니다. 예측치는 금액(달러)으로 표시되어 있습니다.

세계의 디지털 맘모그래피 시장 동향 및 인사이트

USPSTF가 40세부터 검진 대상을 확대함에 따라 수요의 구조적 하한선이 확립되었습니다.

2024년 4월, 미국 예방의료서비스작업반(USPSTF)은 2년마다 실시하는 유방촬영술 검진 대상 연령을 40세에서 74세 여성으로 확대함으로써, 디지털 맘모그래피 시장 수요에 큰 변화를 가져왔습니다. 40세부터 검진을 시작하면, 기존에 50세부터 시작하던 방식에 비해 20% 더 많은 생명을 구할 가능성이 있으며, 백인 여성보다 유방암 사망률이 40% 더 높은 흑인 여성에게 있어 그 혜택은 더욱 커집니다. B등급 평가를 받음에 따라, 고용주의 건강보험 플랜은 첫날부터 전액 보장을 제공해야 할 의무가 있으며, 이는 ‘저렴한 의료법(ACA)’에 따라 40대 여성의 정기 검진을 장려하는 효과가 있습니다. 유방 조직이 치밀한 경우가 많은 젊은 연령대의 검진 대상자들은 디지털 유방 토모신테시스(DBT) 및 AI를 활용한 워크플로우의 운영적 가치를 높여, 시장에 안정적인 최소 수요 수준을 창출하고 있습니다.

고소득 시장에서 2D에서 3D DBT로의 교체 주기가 가속화되고 있습니다.

디지털 맘모그래피 시장은 2D 풀필드 디지털 맘모그래피 시스템의 지속적인 업데이트 주기에 힘입어 성장하고 있습니다. 2025년 3월 기준으로, 미국의 인증 시설 8,963곳 중 8,266곳이 최소 1대의 인증 DBT 장비를 보유하고 있었으나, 인증 2D 장비 1만 3,759대는 여전히 DBT 장비 1만 2,780대를 소폭 상회하고 있어, 대폭적인 업그레이드의 여지가 있음을 여실히 보여주고 있습니다. DBT는 재검사 횟수를 줄이고 판독 효율을 높일 수 있기 때문에 조직 검진에서 점점 더 선호되고 있습니다. 완전한 교체가 아닌 모듈식 업그레이드를 제공하는 공급업체는 특히 자본 계획을 대폭 재검토하지 않고 현대화를 추진하려는 공공 의료기관이나 지역 병원에서 유리한 입장에 있습니다.

자본 예산의 경쟁으로 인해 멀티모달리티로의 업그레이드 주기가 둔화되고 있습니다.

수요는 호조를 보이고 있음에도 불구하고, 디지털 맘모그래피 시장은 의료 시스템 내 자본 배분이라는 과제에 직면해 있습니다. 유방촬영술 플랫폼은 제한된 예산을 두고 CT, MRI, PET/CT와 경쟁하고 있으며, 의료 제공업체들이 부채 관리, 인프라 업그레이드, 서비스 확대에 주력함에 따라 이러한 추세는 2024년 이후 더욱 강화되고 있습니다. DBT 플랫폼의 수명 주기 비용이 높기 때문에 조달 결정은 임상적 선호도보다는 보험 급여 제도의 명확성이나 다년간의 예산에 좌우되는 경향이 있습니다. 지방이나 신흥 지역의 의료기관에서는 방음 시설, 전력 안정성, PACS 연결과 같은 추가 비용이 스캐너 가격을 초과하는 경우가 많아, 업그레이드 속도가 둔화되고 있습니다. 수요는 여전히 견조하지만, 이러한 요인으로 인해 교체 주기가 길어지면서 업그레이드는 장기적인 계획에 포함되게 되었습니다.

부문별 분석

2025년에는 디지털 시스템이 제품 유형별 매출에서 압도적인 60.45%의 점유율을 차지했습니다. 이러한 변화는 특히 첨단 영상 진단 시스템 분야에서 디지털 유방촬영 시장이 아날로그 방식이나 개조 중심의 구성에서 결정적으로 전환되고 있음을 보여줍니다. 2차원(2-D) 플랫폼이 여전히 많은 도입 실적을 차지하고 있음에도 불구하고, 성숙한 시장에서의 교체 수요는 견조한 추세를 보이고 있습니다. C

3D 유방 토모신테시스 시스템은 급속히 부상하고 있으며, 2031년까지 연평균 성장률(CAGR) 11.25%로 성장할 것으로 전망됩니다. 이러한 기세는 임상적 유효성의 입증, 정책적 지원, 그리고 확고한 조달 근거에 의해 뒷받침되고 있습니다. 2025년 3월 기준 FDA 자료에 따르면, 미국에서는 1만 2,780대의 인증된 DBT 장비가 가동 중이지만, 이는 여전히 1만 3,759대의 인증된 2D 디지털 장비 수를 밑돌고 있습니다. 이러한 차이는 현재 진행 중인 업그레이드 주기를 여실히 보여주고 있습니다. 의료기관들은 특히 고밀도 유방을 가진 환자층에서 재촬영 횟수가 줄어들고 성능이 향상될 것으로 예상에 따라 DBT에 대한 관심을 높이고 있습니다.

2025년, 2D 풀필드 디지털 맘모그래피은 기술 매출의 50.9%라는 큰 비중을 차지했으며, 단기적인 검사에서는 여전히 기존 디지털 시스템에 대한 의존도가 지속되고 있음이 드러나고 있습니다. 이러한 확고한 입지는 지역 및 지방 시설에서의 광범위한 도입 실적은 물론, 다양한 시장에서 2D 검사의 운영에 대한 익숙함과 보험 환급 제도에 의해 뒷받침되고 있습니다. 동시에, AI를 활용한 CAD(컴퓨터 지원 진단) 및 이미지 트리아지를 통해 2D 및 DBT의 하드웨어 성능이 향상되어, 즉시 하드웨어를 업그레이드하지 않고도 성능을 개선할 수 있게 되었습니다.

광자 계수형 디지털 유방촬영기는 꾸준한 성장세를 보일 것으로 예상되며, 2031년까지 연평균 성장률(CAGR)은 10.45%로 전망되어 가장 빠르게 발전하고 있는 기술 부문으로 꼽히고 있습니다. 그 매력은 선량 효율과 스펙트럼 이미징을 중시한 검출기 아키텍처에 있습니다. 이를 통해 작은 침윤성 유방암이나 비침윤성 유관암의 검출 감도가 향상되어, 특히 젊은 연령층의 선별 검진이나 고해상도 조영 워크플로우에서 중요한 역할을 합니다. 국제적으로도 관심이 높아지고 있으며, 유럽과 아시아의 일부 시장에서 초기 도입 및 임상 적용이 진행되고 있는 점으로 미루어 볼 때, 단순한 시험 단계에 그치는 관심을 넘어서는 단계로 접어들고 있음을 알 수 있습니다.

지역별 분석

북미는 연방 정부의 꾸준한 자금 지원에 힘입어 2025년 전 세계 매출의 61.11%를 차지했습니다. 북미는 확립된 유방암 검진 프로그램, 견고한 보험 보상 체계, 그리고 3D 토모신테시스 및 AI 지원 진단과 같은 첨단 기술의 급속한 보급에 힘입어 디지털 맘모그래피 시장에서 가장 큰 점유율을 차지하고 있습니다. 특히 미국에서는 FDA의 승인 및 보험 적용에 따라 병원과 영상진단센터가 아날로그 시스템에서 디지털 시스템으로의 전환을 촉진하고 있습니다. 높은 인지도와 정부의 이니셔티브이 시장의 우위를 더욱 공고히 하고 있지만, 소규모 진료소의 경우 장비 비용이 여전히 과제로 남아 있습니다.

유럽은 성숙한 시장이며, 독일, 프랑스, 영국 등 각국의 국가 검진 프로그램의 지원을 받아 디지털 맘모그래피이 널리 보급되어 있습니다. 이 지역에서는 조기 발견과 품질 기준이 중시되고 있으며, 체계적인 보상 정책을 통해 의료 서비스 접근성을 확보하고 있습니다.

중동은 디지털 맘모그래피의 신흥 시장이며, 사우디아라비아와 아랍에미리트(UAE) 등 여러 국가들이 최신 진단 인프라에 막대한 투자를 하고 있습니다. 이러한 성장의 원동력은 유방암 발병률 증가, 정부 주도의 인식 제고 캠페인, 그리고 국제적인 의료 제공업체들과의 제휴입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the digital mammography market size is expected to grow from USD 2.46 billion in 2025 to USD 2.70 billion in 2026 and is forecast to reach USD 4.30 billion by 2031 at 9.75% CAGR over 2026-2031.

This report is Segmented by Product Type (Digital Systems, 3-D Breast Tomosynthesis Systems, and More), Technology (2-D FFDM, 3-D DBT, and More), Application (Screening, Diagnostic, and More), End User (Hospitals, Diagnostic Imaging Centers, and More), and Geography (North America, Europe, Asia-Pacific, Latin America, MEA). Forecasts are Provided in Terms of Value (USD).

Global Digital Mammography Market Trends and Insights

USPSTF Age-40 Screening Expansion Adds a Structural Volume Floor

In April 2024, the U.S. Preventive Services Task Force (USPSTF) extended biennial screening mammography to women aged 40 to 74, marking a significant shift in demand for the digital mammography market. Starting screenings at age 40 could save 20% more lives compared to the previous starting age of 50, with a larger benefit for Black women, who face a 40% higher mortality rate from breast cancer than White women. With a Grade B rating, employer health plans must provide first-dollar coverage, encouraging women in their 40s to undergo routine screenings under the Affordable Care Act. Younger screening cohorts, often with dense breast tissue, increase the operational value of Digital Breast Tomosynthesis (DBT) and AI-enhanced workflows, creating a stable volume floor for the market.

2-D to 3-D DBT Replacement Cycle Accelerates Across High-Income Markets

The digital mammography market is driven by an ongoing replacement cycle among 2-D full-field digital mammography systems. As of March 2025, 8,266 of 8,963 certified facilities in the United States had at least one accredited DBT unit, while 13,759 accredited 2-D units still slightly outnumbered 12,780 DBT units, highlighting significant upgrade potential. DBT is increasingly preferred for organized screenings due to its ability to reduce recalls and improve reading efficiency. Vendors offering modular upgrades instead of full replacements are well-positioned, especially in public systems and community hospitals seeking modernization without overhauling capital plans.

Capital Budget Competition Slows Multi-Modality Upgrade Cycles

Despite favorable demand, the digital mammography market faces capital allocation challenges within health systems. Mammography platforms compete with CT, MRI, and PET/CT for limited budgets, a trend that has intensified since 2024 as providers manage debt, infrastructure upgrades, and service expansions. The high lifecycle costs of DBT platforms make procurement decisions reliant on reimbursement clarity and multi-year budgets rather than clinical preferences. Facilities in rural and emerging areas experience slower upgrades due to additional costs like room shielding, power stability, and PACS connectivity, which often exceed the scanner price. While demand remains strong, these factors extend replacement cycles and push upgrades into long-term planning.

Other drivers and restraints analyzed in the detailed report include:

- Dense-Breast Notification and Follow-Up Imaging Push Drives Incremental Scan Volume

- AI-Enabled Throughput and Recall Reduction Redefines Radiologist Capacity

- Breast-Imaging Workforce Shortage Creates a Structural Capacity Ceiling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Digital Systems dominated the product-type revenue, claiming a substantial 60.45% share. This shift underscores the digital mammography market's decisive pivot away from its analog roots and retrofit-heavy configurations, especially in advanced imaging systems. Despite a significant installed base still featuring 2-D platforms, replacement demand remains robust in mature markets. C

3-D Breast Tomosynthesis Systems are on a rapid ascent, projected to grow at an 11.25% CAGR through 2031. Their momentum is bolstered by clinical validation, policy backing, and sound procurement rationale. As of March 2025, FDA data highlighted 12,780 accredited DBT units in the U.S., still trailing behind the 13,759 accredited 2-D digital units. This gap underscores the ongoing upgrade cycle. Facilities are increasingly drawn to DBT for its promise of fewer recalls and enhanced performance, especially in dense-breast demographics.

In 2025, 2-D Full-Field Digital Mammography accounted for a significant 50.9% of technology revenue, underscoring the continued reliance on legacy digital systems for near-term procedures. This stronghold is bolstered by a widespread installed base in community and rural facilities, coupled with the operational familiarity and reimbursement of 2-D procedures in various markets. Concurrently, AI-driven CAD and image triage are enhancing both 2-D and DBT hardware performance, allowing for improvements without immediate hardware upgrades.

Photon-counting Digital Mammography is set to chart a robust trajectory, with projections indicating a 10.45% CAGR through 2031, marking it as the most rapidly advancing technology segment. Its allure lies in its detector architecture, which champions dose efficiency and spectral imaging. This ensures heightened sensitivity for detecting small invasive cancers and ductal carcinoma in situ, making it particularly relevant for younger screening demographics and sophisticated contrast workflows. Internationally, there's a burgeoning interest, with early installations and clinical applications in several European and Asian markets signaling a shift from mere trial-stage curiosity.

Geography Analysis

North America accounted for 61.11% of global revenue in 2025, driven by robust federal funding. North America holds the largest share of the digital mammography market, driven by well-established breast cancer screening programs, strong reimbursement frameworks, and rapid adoption of advanced technologies like 3D tomosynthesis and AI-assisted diagnostics. The U.S., in particular, benefits from FDA approvals and insurance coverage that encourage hospitals and imaging centers to upgrade from analog to digital systems. High awareness levels and government initiatives further reinforce market dominance, though equipment costs remain a challenge for smaller clinics.

Europe represents a mature market with widespread adoption supported by national screening programs in countries such as Germany, France, and the UK. The region emphasizes early detection and quality standards, with structured reimbursement policies ensuring accessibility.

The Middle East is an emerging market for digital mammography, with countries like Saudi Arabia and the UAE investing heavily in modern diagnostic infrastructure. Growth is fueled by rising breast cancer incidence, government-backed awareness campaigns, and partnerships with international healthcare providers.

- Canon

- CureMetrix, Inc.

- DeepHealth, Inc.

- Delphinus Medical Technologies, Inc.

- Densitas, Inc.

- FUJIFILM

- GE Healthcare

- General Medical Merate

- Hologic

- iCAD, Inc.

- Konica Minolta

- Lunit

- Metaltronica

- Onsite Women's Health, LLC

- Planmed

- RadNet, Inc.

- ScreenPoint Medical B.V.

- Siemens Healthineers

- Therapixel SA

- Volpara Health Technologies Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 USPSTF Age-40 Screening Expansion

- 4.2.2 2D-To-DBT Replacement Cycle

- 4.2.3 Dense-Breast Notification and Follow-Up Imaging Push

- 4.2.4 AI-Enabled Throughput and Recall Reduction

- 4.2.5 2026 No-Cost Completion Imaging Under ACA Plans

- 4.2.6 Rural Access and Mobile Deployment Economics

- 4.3 Market Restraints

- 4.3.1 Capital Budget Pressure for Multi-Modality Upgrades

- 4.3.2 Breast-Imaging Radiologist and Technologist Shortage

- 4.3.3 MQSA Audit and Record-Transfer Compliance Burden

- 4.3.4 Tariff and Service-Parts Volatility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Digital Systems

- 5.1.2 3-D Breast Tomosynthesis Systems

- 5.1.3 Contrast-Enhanced Mammography Systems

- 5.1.4 Computed-Radiography Retrofit Kits

- 5.2 By Technology

- 5.2.1 2-D Full-Field Digital Mammography

- 5.2.2 3-D Digital Breast Tomosynthesis

- 5.2.3 AI-enabled CAD and Image Triage

- 5.2.4 Photon-counting Digital Mammography

- 5.3 By Application

- 5.3.1 Screening

- 5.3.2 Diagnostic

- 5.3.3 Interventional and Biopsy Guidance

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Diagnostic Imaging Centers

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Office-based and Specialty Breast Centers

- 5.4.5 Mobile Screening Programs

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Canon Medical Systems Corporation

- 6.3.2 CureMetrix, Inc.

- 6.3.3 DeepHealth, Inc.

- 6.3.4 Delphinus Medical Technologies, Inc.

- 6.3.5 Densitas, Inc.

- 6.3.6 FUJIFILM Healthcare

- 6.3.7 GE HealthCare

- 6.3.8 General Medical Merate S.p.A.

- 6.3.9 Hologic, Inc.

- 6.3.10 iCAD, Inc.

- 6.3.11 Konica Minolta, Inc.

- 6.3.12 Lunit Inc.

- 6.3.13 Metaltronica S.p.A.

- 6.3.14 Onsite Women's Health, LLC

- 6.3.15 Planmed Oy

- 6.3.16 RadNet, Inc.

- 6.3.17 ScreenPoint Medical B.V.

- 6.3.18 Siemens Healthineers AG

- 6.3.19 Therapixel SA

- 6.3.20 Volpara Health Technologies Limited

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment