|

시장보고서

상품코드

2065444

미국의 전기 치료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Electrotherapy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

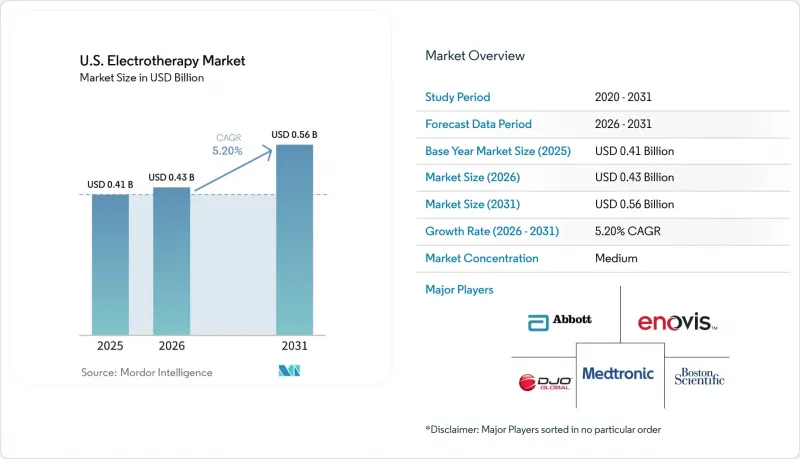

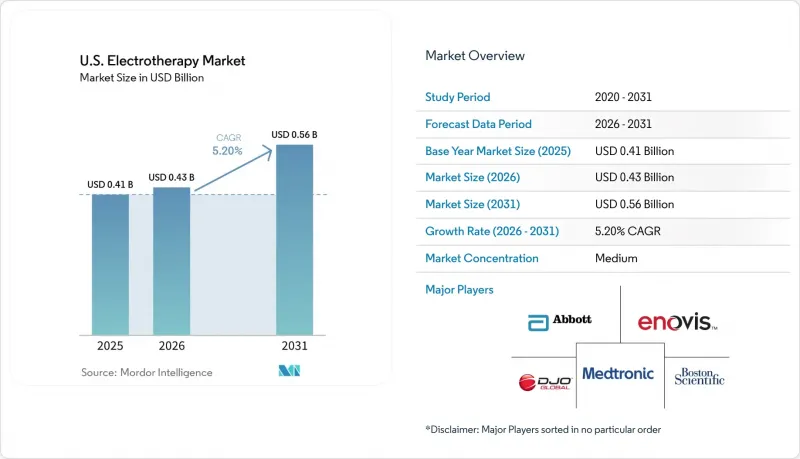

미국의 전기 치료 시장 규모는 2025년 4억 1,000만 달러로 평가되었습니다. 2026년에는 4억 3,000만 달러로 확대되어 2031년까지 5억 6,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 5.20%로 성장할 전망입니다.

본 보고서는 치료법 유형(TENS, IFT, NMES/FES 등), 용도(통증 관리, 신경근 기능 장애 등), 최종 사용자(병원, 통증 클리닉, 물리치료 센터, 외래수술센터(ASC) 등), 처방 형태(처방약, 일반의약품, 하이브리드형 재택 치료)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 전기 치료 시장 동향 및 인사이트

만성 통증의 부담과 노화에 따른 통증 발생률

만성 통증은 계속해서 미국의 전기 치료 시장의 주요 성장 동인으로 작용하고 있으며, 2025년에는 성인의 24.3%(약 6,000만 명)가 만성 통증을 경험했습니다. 그중 8.9%는 일상생활에 지장을 줄 정도의 심각한 만성 통증에 시달리고 있었습니다. 고령층이 가장 큰 영향을 받고 있으며, 65세 이상에서는 유병률이 36.0%인 반면, 젊은 층에서는 12.3%에서 28.7%에 그치고 있습니다. 퇴행성 관절염이나 척추 퇴행성 질환과 같은 질환들은 약물 사용을 최소화하는 통증 관리에서 전기 치료이 수행하는 역할을 부각시키고 있습니다. 이 시장은 외래 재활, 재택 간호, 만성 질환 관리 등 다양한 분야에 걸친 안정적인 수요 기반의 혜택을 누리고 있습니다.

통증 관리의 전 과정에서 오피오이드 사용을 자제하는 치료법의 선호

비오피오이드계 통증 치료로의 전환에 따라, 병원, 외래 진료 시설, 전문의 채널에 걸친 미국의 전기 치료 시장이 확대되고 있습니다. 'NOPAIN법'은 2027년까지 비오피오이드계 치료에 대한 메디케어 지급을 지원함으로써, 의료기기를 활용한 통증 관리의 경제적 타당성을 높이고 있습니다. ‘PAIN법 대체 법안’은 메디케어 파트 D의 사전 승인 장벽을 낮추고, 비약물 요법을 장려하고 있습니다. 만성 요통에 대한 말초신경 자극 요법에 대한 전문의들의 지지가 이 요법의 도입을 더욱 촉진하고 있으며, 일반 소비자용 기기보다 부가가치가 높은 처방 시스템이 주목을 받고 있습니다.

상환 관련 마찰, 사전 승인 및 LCD 제한

상환 절차의 복잡성은 미국의 전기 치료 시장에서 여전히 단기적인 주요 과제로 남아 있습니다. 애리조나주, 뉴저지주, 텍사스주 등에서 2026년 1월 1일부터 시행되는 ‘WISeR 모델’은 전기 신경 자극 기기에 대해 AI를 활용한 사전 승인을 도입함으로써 업무 부담을 가중시키고 판매 주기를 장기화시키고 있습니다. 2024년 1월에 시행된 TENS용 CMS LCD L33802 등, 더욱 엄격해진 규정 준수 요건은 이미 공급업체들의 부담을 가중시키고 있습니다. 대기업들은 규모와 자원을 활용해 이러한 변화에 효과적으로 대응하고 있지만, 중소 공급업체들은 큰 행정적 난관에 직면해 있습니다. 메디케어 이용자가 많은 주요 시장인 텍사스주에서는 이러한 추가 심사가 수익에 미치는 영향이 더욱 커지고 있습니다.

부문별 분석

2025년, TENS 치료용 기기는 치료 유형별 구성에서 32.55%의 점유율을 차지하며 미국의 전기 치료 시장을 주도했습니다. 이러한 우위는 처방약 및 일반의약품의 유통 경로를 불문하고 널리 구할 수 있다는 점에 기인하며, 진료소, 약국, 소매점 및 직접 구매를 통해 접근성을 높이고 있습니다. FDA의 510(k) 승인 절차는 여전히 활발하게 진행되고 있으며, ‘OTC 4채널 충전식 TENS 기기’ 및 Zynex Medical사의 ‘TensWave’ 등의 승인을 통해 처방전이 필요한 TENS 제품 포트폴리오가 확대되었습니다. 간섭파 요법 및 미약전류 요법은 물리치료에서 그 역할을 유지한 반면, PENS 및 골성장 자극 요법은 여전히 전문적인 영역에 머물렀습니다.

신경근 전기 자극(NMES)은 2031년까지 연평균 성장률(CAGR) 6.80%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 치료법이 될 전망입니다. 재택 사용 승인을 바탕으로, 뇌졸중 재활, 척수 손상 회복, 수술 후 근재교육 분야에서 도입이 확대되고 있습니다. 척수 자극 및 천골 신경 조절과 같은 고부가가치 이식형 기기가 여전히 매출의 대부분을 차지하는 반면, 체표형 기기가 판매량 증가를 주도하고 있습니다.

2025년에는 통증 관리가 용도 구성의 42.88%를 차지하며 미국의 전기 치료 시장을 주도했습니다. 이는 처방전이 필요한 TENS(경피적 전기 신경 자극 요법), 말초 신경 자극 및 척수 자극 치료가 외래 통증 클리닉이나 척추 전문 진료소에 집중되어 있음을 반영합니다. 골유합 및 척추 고정술에 대한 지원은 고위험 사례에서의 임상적 필요성에 힘입어 안정적인 수요를 유지했습니다. 한편, 상처 관리 및 피부과 용도는 보험 급여와 관련된 문제로 인해 여전히 제한적인 상황에 머물렀습니다.

신경근 기능 장애 및 재활 시장은 뇌졸중, 척수 손상, 외상성 뇌손상의 발생률 증가에 힘입어 2031년까지 연평균 성장률(CAGR) 6.35%로 성장할 것으로 전망됩니다. 보스턴 사이언티피크의 액소닉스 인수로 인해, 골반 기능 장애 치료 분야에서 해당 기업의 입지가 강화되었으며, 사업 포트폴리오에 고성장 부문이 추가되었습니다. 통증 관리가 여전히 핵심을 이루는 한편, 재활 및 골반 신경 조절이 주목을 받고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the u.S. electrotherapy market size is expected to increase from USD 0.41 billion in 2025 to USD 0.43 billion in 2026 and reach USD 0.56 billion by 2031, growing at a CAGR of 5.20% over 2026-2031.

This report is Segmented by Therapy Type (TENS, IFT, NMES/FES, and More), Application (Pain Management, Neuromuscular Dysfunction, and More), End User (Hospitals, Pain Clinics, PT Centers, Ascs, and More), and Prescription Type (Prescription, OTC, and Hybrid Direct-To-Home). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Electrotherapy Market Trends and Insights

Chronic Pain Burden and Aging-Related Pain Incidence

Chronic pain remains a significant driver for the United States electrotherapy market, with 24.3% of adults, approximately 60 million people, experiencing chronic pain in 2025. Among them, 8.9% faced high-impact chronic pain that disrupted daily activities. Older adults were most affected, with a 36.0% prevalence among those aged 65 and above, compared to 12.3% to 28.7% in younger groups. Conditions like osteoarthritis and spinal degeneration highlight the role of electrotherapy in drug-sparing pain management. The market benefits from a stable demand base across outpatient rehabilitation, homecare, and chronic disease management settings.

Opioid-Sparing Treatment Preference Across Pain Care Pathways

The shift toward non-opioid pain treatments is strengthening the United States electrotherapy market across hospitals, outpatient facilities, and specialist channels. The NOPAIN Act supports Medicare payments for non-opioid treatments through 2027, enhancing the financial case for device-based pain management. The Alternatives to PAIN Act reduces prior authorization barriers under Medicare Part D, favoring non-drug therapies. Specialist endorsements for peripheral nerve stimulation in chronic back pain further drive adoption, with higher-value prescription systems gaining traction over consumer devices.

Reimbursement Friction, Prior Authorization, and LCD Limits

Reimbursement complexities remain a key short-term challenge for the United States electrotherapy market. The WISeR Model, effective January 1, 2026, in states like Arizona, New Jersey, and Texas, introduces AI-assisted prior authorization for electrical nerve stimulators, increasing operational burdens and extending sales cycles. Stricter compliance requirements, such as the CMS LCD L33802 for TENS implemented in January 2024, have already added to suppliers' challenges. Larger manufacturers manage these changes more effectively due to scale and resources, while smaller suppliers face significant administrative hurdles. Texas, a critical Medicare-heavy market, amplifies the revenue impact of these added reviews.

Other drivers and restraints analyzed in the detailed report include:

- Home-Based Rehabilitation and Portable Device Adoption

- Higher Outpatient Musculoskeletal and Post-Surgical Rehab Volume

- Mixed Clinical Evidence Across Some Indications and Modalities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, TENS therapy devices held a 32.55% share of the therapy type mix, leading the United States electrotherapy market. Their dominance was driven by broad availability across prescription and over-the-counter channels, enhancing access through clinics, pharmacies, retail outlets, and direct purchases. The FDA's 510(k) pathway remained active, with clearances like the OTC 4-Channel Rechargeable TENS Unit and Zynex Medical's TensWave expanding the prescription TENS portfolio. Interferential and microcurrent therapies retained their roles in physiotherapy, while PENS and bone growth stimulation remained specialized.

Neuromuscular electrical stimulation (NMES) is projected to grow at a 6.80% CAGR through 2031, making it the fastest-growing therapy type. Its adoption is increasing in stroke rehabilitation, spinal cord injury recovery, and post-surgical muscle re-education, supported by home-use clearances. High-value implantables like spinal cord stimulation and sacral neuromodulation continue to dominate revenue, while surface devices drive higher unit sales.

Pain management accounted for 42.88% of the application mix in 2025, leading the United States electrotherapy market. This reflects the concentration of prescription TENS, peripheral nerve stimulation, and spinal cord stimulation in outpatient pain clinics and spine practices. Bone healing and spinal fusion support maintained stable demand, driven by clinical necessity in high-risk cases, while wound care and dermatological applications remained limited due to reimbursement challenges.

The market for neuromuscular dysfunction and rehabilitation is forecast to grow at a 6.35% CAGR through 2031, driven by rising incidences of stroke, spinal cord injuries, and traumatic brain injuries. Boston Scientific's acquisition of Axonics strengthened its position in pelvic dysfunction therapy, adding a high-growth segment to the application mix. Pain management remains the anchor, while rehabilitation and pelvic neuromodulation are gaining traction.

List of Companies Covered in this Report:

- Abbott Laboratories

- Axonics, Inc.

- BioWave Corporation

- Boston Scientific

- BTL Industries, Inc.

- DJO Global

- Electronic Waveform Lab, Inc. (H-Wave)

- EMS Physio Ltd.

- Enovis Corporation

- Gymna Group NV

- Medtronic

- Mettler Electronics

- NeuroMetrix

- OMRON Healthcare, Inc.

- Orthofix

- Richmar

- RS Medical, Inc.

- TensCare Ltd.

- Utah Medical Products

- Zynex, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Chronic Pain Burden and Aging-Related Pain Incidence

- 4.2.2 Opioid-Sparing Treatment Preference Across Pain Care Pathways

- 4.2.3 Home-Based Rehabilitation and Portable Device Adoption

- 4.2.4 Higher Outpatient Musculoskeletal and Post-Surgical Rehab Volumes

- 4.2.5 Faster Coverage Visibility for Breakthrough Stimulation Platforms

- 4.2.6 Remote Programming and Adherence Analytics Improving Home-Use Scalability

- 4.3 Market Restraints

- 4.3.1 Mixed Clinical Evidence Across Some Indications and Modalities

- 4.3.2 Reimbursement Friction, Prior Authorization, and LCD Limits

- 4.3.3 Competition From Physical Therapy, Drugs, Injections, Surgery, and Other Modalities

- 4.3.4 Crowded Low-End Device Supply and Compliance Burden

- 4.4 Value/Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of new entrants

- 4.7.2 Bargaining power of suppliers

- 4.7.3 Bargaining power of buyers

- 4.7.4 Threat of substitutes

- 4.7.5 Intensity of rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Therapy Type

- 5.1.1 Transcutaneous Electrical Nerve Stimulation (TENS)

- 5.1.2 Interferential Therapy (IFT)

- 5.1.3 Neuromuscular Electrical Stimulation (NMES) / Functional Electrical Stimulation (FES)

- 5.1.4 Microcurrent Therapy

- 5.1.5 Percutaneous Electrical Nerve Stimulation (PENS)

- 5.1.6 Spinal Cord Stimulation (SCS)

- 5.1.7 Peripheral Nerve Stimulation (PNS)

- 5.1.8 Sacral Neuromodulation (SNM)

- 5.1.9 Bone Growth Stimulation

- 5.2 By Application

- 5.2.1 Pain Management

- 5.2.2 Neuromuscular Dysfunction and Rehabilitation

- 5.2.3 Bone Healing and Spinal Fusion Adjunct Therapy

- 5.2.4 Urinary and Fecal Incontinence / Pelvic Floor Dysfunction

- 5.2.5 Other Indications

- 5.3 By End User

- 5.3.1 Hospitals and Health Systems

- 5.3.2 Pain Management and Spine Clinics

- 5.3.3 Physical Therapy and Rehabilitation Centers

- 5.3.4 Ambulatory Surgery Centers and Outpatient Orthopedic Clinics

- 5.3.5 Homecare and Self-Administered Care

- 5.3.6 Others

- 5.4 By Prescription Type

- 5.4.1 Prescription Devices

- 5.4.2 Over-the-Counter Devices

- 5.4.3 Hybrid Physician-Enabled Direct-to-Home Devices

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Axonics, Inc.

- 6.3.3 BioWave Corporation

- 6.3.4 Boston Scientific Corporation

- 6.3.5 BTL Industries, Inc.

- 6.3.6 DJO, LLC

- 6.3.7 Electronic Waveform Lab, Inc. (H-Wave)

- 6.3.8 EMS Physio Ltd.

- 6.3.9 Enovis Corporation

- 6.3.10 Gymna Group NV

- 6.3.11 Medtronic plc

- 6.3.12 Mettler Electronics Corp.

- 6.3.13 NeuroMetrix, Inc.

- 6.3.14 OMRON Healthcare, Inc.

- 6.3.15 Orthofix Medical Inc.

- 6.3.16 Richmar

- 6.3.17 RS Medical, Inc.

- 6.3.18 TensCare Ltd.

- 6.3.19 Utah Medical Products, Inc.

- 6.3.20 Zynex, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment