|

시장보고서

상품코드

2065453

미국의 케타민 클리닉 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Ketamine Clinics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

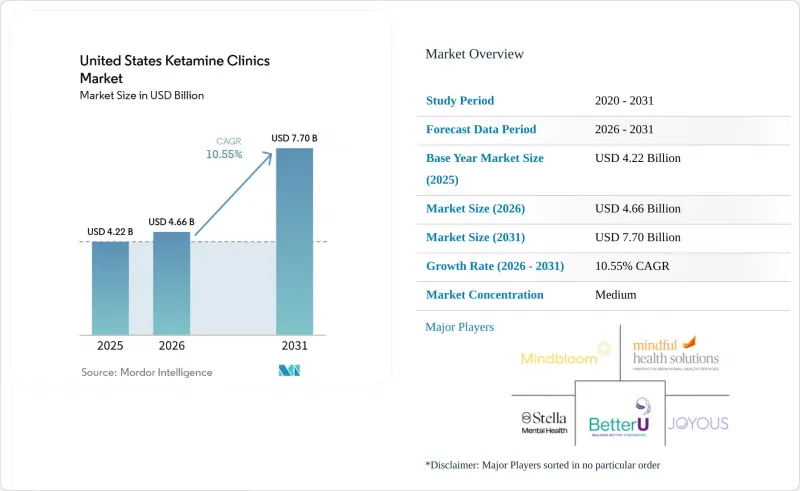

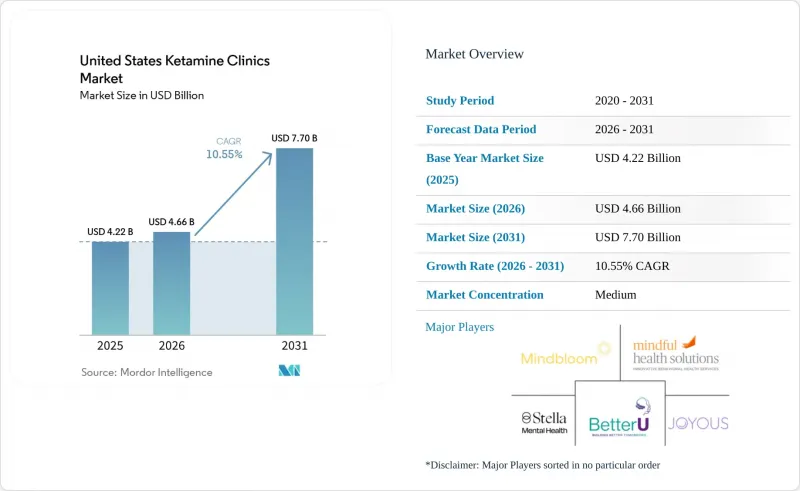

미국의 케타민 클리닉 시장 규모는 2025년에 42억 2,000만 달러로 평가되었고, 2026년 46억 6,000만 달러로 추정되고, 2031년까지 77억 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 10.55%를 나타낼 전망입니다.

본 보고서는 임상 적응증별(우울증, 불안 장애, PTSD, 강박 장애, 약물 사용 장애, 만성 통증, 기타), 치료 형태별(대면, 온라인, 하이브리드), 투여 경로별(정맥 내, 근육 내, 비강 내 에스케타민, 설하/경구, 피하)로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

미국의 케타민 클리닉 시장 동향 및 인사이트

치료 저항성 우울증으로 인한 부담 증가

치료 저항성 우울증(TRD)은 치료를 받고 있는 우울증 환자 집단에서 상당한 비중을 차지하며, 높은 의료적·사회적 비용을 수반하기 때문에 미국 케타민 클리닉 시장에서 여전히 가장 확실한 수요의 주축으로 자리 잡고 있습니다. 미국에서 약물 치료를 받고 있는 주요 우울 장애(MDD) 성인 890만 명 중 280만 명이 치료 저항성 우울증(TRD)으로 진행되고 있으며, 이 그룹은 약물 치료를 받고 있는 MDD와 관련된 연간 927억 달러의 비용 부담 중 438억 달러를 차지했습니다. 중증도의 차이는 의료 서비스 이용 현황에도 나타나고 있으며, TRD 환자의 평균 입원 비용은 6,464달러인 반면, 비-TRD 환자는 1,734달러이며, 우울증 에피소드의 지속 일수도 TRD 환자가 1,000일 이상인 반면, 비-TRD 환자는 452일에 그치고 있습니다. 이러한 비용 추세를 바탕으로, 케타민 클리닉은 의뢰처나 보험사에 대해 더욱 설득력 있는 주장을 펼칠 수 있게 됩니다. 왜냐하면, 이 논의가 단순한 증상 완화에 그치지 않고, 피할 수 있는 입원이나 장기화되는 질병 부담에까지 미치기 때문입니다. 또한 CDC 보고서에 따르면, 2023년 미국 성인의 11.4%가 우울증 치료제를 처방받았으며, 지역이나 장애 유무에 따라 차이가 나타납니다. 이는 미국 전역에 걸쳐 치료를 받지 못했거나 불충분한 치료를 받고 있는 환자층이 여전히 상당수 존재한다는 견해를 뒷받침하는 것입니다. 미국의 케타민 클리닉 시장이 확대됨에 따라 새로운 적응증이 주목을 받게 되더라도, 이러한 구조적인 수요 조건으로 인해 우울증을 주원인으로 하는 의뢰 건수는 높은 수준을 유지할 것으로 전망됩니다.

기존 항우울제를 대체할 수 있는 즉효성 있는 치료법

미국의 케타민 클리닉 시장은 일반적인 경구용 항우울제와 급성 고통을 겪고 있는 환자들의 요구 사이에서 발생하는 실질적인 격차 덕분에 계속해서 혜택을 보고 있습니다. 기존 항우울제의 전체적인 유효율은 37%이며, 뚜렷한 임상적 개선이 나타나기까지 4-6주가 소요되는 경우가 많기 때문에 더 신속하게 효과를 볼 수 있는 치료법에 있어 중요한 치료 기회가 생겨나고 있습니다. 2025년 1월 SPRAVATO 단독 요법의 승인을 뒷받침한 3상 임상시험에서 4주 시점에 환자의 22.5%가 관해를 달성한 반면, 위약군에서는 7.6%에 그쳤으며, 첫 투여 후 24시간 이내에 측정 가능한 증상 개선이 관찰되었습니다. 이러한 속도는 중증 증상을 보이는 환자가 초기 반응을 몇 주 동안 기다릴 수 없는 경우가 많기 때문에 임상적으로 중요할 뿐만 아니라, 조기에 반응을 보인 환자는 더 신속하게 유지 요법으로 전환할 수 있으므로 운영상으로도 중요합니다. PMC에 게재된 2024년 연구에서도 3개월 시점에서 우울증, 불안 장애, PTSD의 모든 영역에서 큰 치료 효과가 확인되었으며, 6개월 시점에서는 효과가 다소 줄어들었으나 지속되었고, 참가자의 50%에서 75%에게서 유의미한 임상적 개선이 나타났습니다. 그 결과, 미국의 케타민 클리닉 시장은 기존의 투약 주기보다 빠르게 효과를 발휘하는 대안을 찾는 정신과 의사 및 1차 진료 의사들로부터 점점 더 많은 주목을 받고 있습니다.

적응증 외 케타민 요법에 대한 보험 적용 범위 제한

보험 적용에 따른 불균형은 여전히 미국의 케타민 클리닉 시장에 있어 가장 중요한 구조적 걸림돌로 남아 있습니다. 실무상의 차이는 분명합니다. 스프라바토(Spravato)는 FDA의 공식 승인 절차를 거쳤기 때문에 보험 급여 제도에 부합하기 쉬운 반면, 정신과 용도로 사용되는 정맥 내(IV), 근육 내(IM), 설하 및 피하 투여용 케타민은 여전히 환자 본인 부담으로 인한 경제적 부담을 겪기 쉬운 상황에 놓여 있습니다. 이러한 구분에 따라 두 가지의 병행되는 비즈니스 모델이 등장하고 있습니다. 하나는 감독 하에 보험 환급 대상이 되는 에스케타민 치료로 이어지는 모델이고, 다른 하나는 적응증 외 치료에 대한 환자의 직접 지불로 이어지는 모델입니다. 그 결과, 환자 수요나 의사의 관심이 높더라도 주로 적응증 외 투여 방식에 의존하는 사업자의 경우, 대상 환자층이 좁아지게 됩니다. 또한, 이는 경쟁 행태에도 영향을 미칩니다. 왜냐하면 대규모 사업자는 급여 내용의 검증, 사전 승인 지원, 그리고 보험 적용 환자의 부담을 경감하는 계약에 더 많은 금액을 투자할 수 있기 때문입니다. 모든 투여 형태에 대한 보험 적용이 확대되기 전까지는 미국의 케타민 클리닉 시장은 환자의 소득 수준, 비용 부담 주체, 클리닉의 운영 모델에 따라 고르지 않은 성장세를 이어갈 것으로 보입니다.

부문별 분석

2025년, 미국 케타민 클리닉 시장 점유율의 44.31%를 우울증이 차지했으며, 이는 주요 임상 적응증인 동시에 현재 사업자들에게 있어 주된 수익원이 되고 있습니다. 이 부문은 미국 내 치료 저항성 우울증(TRD) 시장 규모에 힘입어 성장하고 있습니다. 해당 국가에서는 약물 치료를 받고 있는 주요 우울 장애(MDD) 환자 중 280만 명의 성인이 치료 저항성 질환을 앓고 있습니다. 또한, 미국 국립정신건강연구소(NIMH)의 보고에 따르면, 2,100만 명의 성인이 주요 우울 장애를 경험하고 있으며, 기존의 약물 치료가 효과를 보이지 않은 후 단계적인 개입을 위한 폭넓은 의뢰 기반이 존재한다는 점도 이 부문을 뒷받침하는 요인이 되고 있습니다. 2025년 1월 SPRAVATO 단독 요법의 승인으로, 그동안 일부 정신과 의사와 환자들에게 진료 의뢰 결정을 복잡하게 만들었던 실질적인 장벽이 제거되었습니다. 미국의 케타민 클리닉 업계에서 클리닉이 인접한 정신과 진단을 수용하는 범위를 확대하고 있는 상황에서도, 우울증은 여전히 의사의 의뢰 행위의 중심을 차지하고 있습니다.

만성 통증 시장은 2026-2031년 연평균 성장률(CAGR) 11.38%로 가장 빠른 성장세를 보일 것으로 예상되며, 이는 미국의 케타민 클리닉 시장이 당초의 주요 대상이었던 우울증을 넘어 확대되고 있음을 보여줍니다. 스탠퍼드 대학교는 2025년 1월, 프로포폴 진정 하에서 우울증을 동반한 만성 통증에 대한 정맥 내 케타민의 유효성을 평가하는 4상 임상시험을 시작했으며, 2026년 말까지 연구 방법론적으로 더욱 체계화된 근거가 추가될 전망입니다. 또한, 『Frontiers in Pain Research』지에 게재된 2025년 사례 시리즈에서는 저용량 케타민과 생물심리사회적 보조 요법을 병용함으로써 임상적으로 유의미한 통증 완화가 확인되었을 뿐만 아니라, 필요한 투여량을 줄일 수 있는 방안도 제시되었습니다. 불안 장애, PTSD, 강박 장애(OCD), 약물 사용 장애는 여전히 규모는 작지만 중요한 환자 집단을 차지하고 있으며, 2024년 PMC 조사는 단일 진단에 기반한 보고서에서는 간과되기 쉬운 요구 사항을 다중 적응증 프로토콜을 통해 파악할 수 있다는 견해를 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the united states ketamine clinics market size was valued at USD 4.22 billion in 2025 and is estimated to grow from USD 4.66 billion in 2026 to reach USD 7.70 billion by 2031, at a CAGR of 10.55% during the forecast period (2026-2031).

This report is Segmented by Clinical Indication (Depression, Anxiety Disorders, PTSD, OCD, Substance Use Disorders, Chronic Pain, Other), Therapy Modality (On-Site, Online, Hybrid), and Route of Administration (Intravenous, Intramuscular, Intranasal Esketamine, Sublingual/Oral, Subcutaneous). The Market Forecasts are Provided in Terms of Value (USD).

United States Ketamine Clinics Market Trends and Insights

Rising Treatment-Resistant Depression Burden

Treatment-resistant depression remains the clearest demand anchor for the US ketamine clinics market because the condition sits inside a large treated depression population and carries high medical and social cost. Among 8.9 million medication-treated adults with MDD in the United States, 2.8 million progress to TRD, and that group accounts for USD 43.8 billion of the USD 92.7 billion yearly burden associated with medicated MDD. The severity gap is also visible in care utilization, since TRD patients recorded average hospitalization costs of USD 6,464 versus USD 1,734 for non-TRD patients and experienced depressive episodes lasting more than 1,000 days versus 452 days. This cost profile gives ketamine clinics a stronger case when they approach referral sources or payers, because the discussion is no longer limited to symptom relief and extends to avoidable hospital use and prolonged disease burden. The CDC also reported that 11.4% of U.S. adults took prescription medication for depression in 2023, with variation by region and disability status, which supports the view that untreated or poorly treated populations remain sizable across the country. As the US ketamine clinics market expands, these structural demand conditions should keep depression-led referrals elevated even as additional indications gain traction.

Rapid-Acting Alternative to Conventional Antidepressants

The US ketamine clinics market continues to benefit from the practical gap between standard oral antidepressants and the needs of patients in acute distress. Conventional antidepressants show an overall response rate of 37% and often need 4 to 6 weeks before clear clinical improvement becomes visible, which leaves a meaningful treatment window for faster-acting care. In the Phase 3 study behind the January 2025 SPRAVATO monotherapy approval, 22.5% of patients achieved remission at week 4 compared with 7.6% on placebo, and measurable symptom improvement appeared within 24 hours of the first dose. That speed matters clinically because patients with severe symptoms often cannot wait several weeks for an initial response, and it matters operationally because earlier responders can move into maintenance schedules more quickly. A 2024 study published in PMC also found large treatment effects across depression, anxiety, and PTSD at 3 months, with durable though smaller effects at 6 months and meaningful clinical improvement in 50% to 75% of participants. As a result, the US ketamine clinics market is drawing more interest from psychiatrists and primary care physicians who want options that work faster than the conventional medication cycle.

Limited Insurance Coverage for Off-Label Ketamine Therapy

Insurance asymmetry remains the most important structural brake on the US ketamine clinics market. The practical divide is clear, Spravato has a formal FDA-approved pathway that fits reimbursement structures more easily, while IV, IM, sublingual, and subcutaneous ketamine for psychiatric use are still much more exposed to self-pay economics. That split creates two parallel business models, one tied to supervised, reimbursable esketamine care and another tied to direct patient payment for off-label treatment. The result is a narrower addressable pool for operators that rely mainly on off-label formats, even when patient demand and physician interest are strong. This also shapes competitive behavior because scale operators can invest more heavily in benefit verification, prior authorization support, and contracts that reduce friction for covered patients. Until reimbursement becomes broader across formats, the US ketamine clinics market will keep growing unevenly across patient income groups, payer types, and clinic models.

Other drivers and restraints analyzed in the detailed report include:

- Growing Psychiatrist and Patient Acceptance of Interventional Psychiatry

- Expansion of Multi-Site Clinics and Hybrid Care Pathways

- Protocol Heterogeneity and Limited Long-Term Evidence

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Depression accounted for 44.31% of the US ketamine clinics market share in 2025, making it the leading clinical indication and the main revenue base for current operators. The segment is supported by the scale of TRD in the United States, where 2.8 million adults develop treatment-resistant disease within the medicated MDD population. It is also supported by the broader prevalence pool, since NIMH reported that 21 million adults experienced a major depressive episode, which leaves a wide referral base for stepped-up intervention after conventional drug failure. The January 2025 SPRAVATO monotherapy approval removed a practical barrier that had previously complicated referral decisions for some psychiatrists and patients. Within the US ketamine clinics industry, this keeps depression at the center of physician referral behavior even as clinics broaden their intake across adjacent psychiatric diagnoses.

Chronic pain is projected to record the fastest growth at 11.38% CAGR from 2026 to 2031, which shows that the US ketamine clinics market is expanding beyond its original depression focus. Stanford University began a Phase 4 study in January 2025 to evaluate IV ketamine for chronic pain with comorbid depression under propofol sedation, which should add more methodologically structured evidence by late 2026. A 2025 case series in Frontiers in Pain Research also showed clinically meaningful pain reduction from low-dose ketamine combined with biopsychosocial adjunct therapies, while suggesting a pathway to lower required dosing. Anxiety disorders, PTSD, OCD, and substance use disorders still represent smaller but meaningful pools, and the 2024 PMC study supports the view that multi-indication protocols can capture needs that single-diagnosis reporting misses.

List of Companies Covered in this Report:

- Actify Neurotherapies

- Avesta Ketamine and Wellness

- Better U

- Cambridge Biotherapies

- Capitol Ketamine & Wellness

- Complete Ketamine Solutions

- Ember Health

- Hopemark Health

- Joyous

- Keta Medical Center

- Ketamine Clinics Los Angeles

- Ketamine Wellness NY

- Klarisana

- Mindbloom

- Mindful Health Solutions

- Numinus

- Nushama

- NY Ketamine Infusions

- Revitalist Clinic

- Stella Mental Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Treatment-Resistant Depression Burden

- 4.2.2 Rapid-Acting Alternative to Conventional Antidepressants

- 4.2.3 Growing Psychiatrist and Patient Acceptance of Interventional Psychiatry

- 4.2.4 Expansion Of Multi-Site Clinics and Hybrid Care Pathways

- 4.2.5 SPRAVATO Monotherapy Label Expansion Simplifying Treatment Workflows

- 4.2.6 Telehealth Prescribing Flexibilities Sustaining Hybrid Patient Acquisition

- 4.3 Market Restraints

- 4.3.1 Limited Insurance Coverage for Off-Label Ketamine Therapy

- 4.3.2 Protocol Heterogeneity and Limited Long-Term Evidence

- 4.3.3 FDA Scrutiny of Compounded Ketamine Increasing Compliance Burden

- 4.3.4 Prior Authorization and REMS Chair-Time Limiting Spravato Throughput

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Clinical Indication

- 5.1.1 Depression

- 5.1.2 Anxiety Disorders

- 5.1.3 PTSD

- 5.1.4 OCD

- 5.1.5 Substance Use Disorders

- 5.1.6 Chronic Pain

- 5.1.7 Other Indications

- 5.2 By Therapy Modality

- 5.2.1 On-Site Therapy

- 5.2.2 Online Therapy

- 5.2.3 Hybrid Therapy

- 5.3 By Route of Administration

- 5.3.1 Intravenous

- 5.3.2 Intramuscular

- 5.3.3 Intranasal Esketamine

- 5.3.4 Sublingual / Oral

- 5.3.5 Subcutaneous

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Actify Neurotherapies

- 6.3.2 Avesta Ketamine and Wellness

- 6.3.3 Better U

- 6.3.4 Cambridge Biotherapies

- 6.3.5 Capitol Ketamine & Wellness

- 6.3.6 Complete Ketamine Solutions

- 6.3.7 Ember Health

- 6.3.8 Hopemark Health

- 6.3.9 Joyous

- 6.3.10 Keta Medical Center

- 6.3.11 Ketamine Clinics Los Angeles

- 6.3.12 Ketamine Wellness NY

- 6.3.13 Klarisana

- 6.3.14 Mindbloom

- 6.3.15 Mindful Health Solutions

- 6.3.16 Numinus

- 6.3.17 Nushama

- 6.3.18 NY Ketamine Infusions

- 6.3.19 Revitalist Clinic

- 6.3.20 Stella Mental Health

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment