|

시장보고서

상품코드

2065454

디지털 온보딩 플랫폼 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Digital Onboarding Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

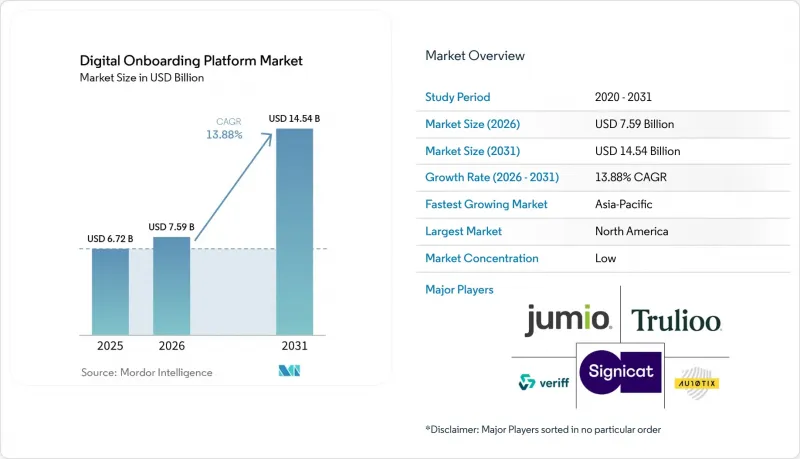

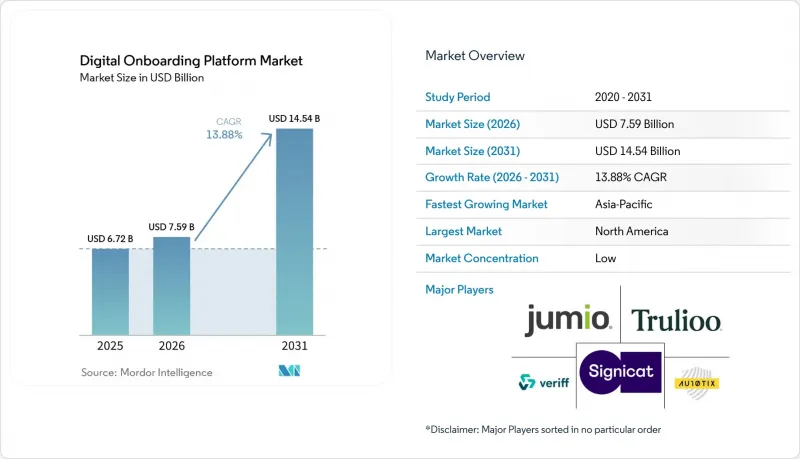

Mordor Intelligence에 의하면, 디지털 온보딩 플랫폼 시장 규모는 2025년에 67억 2,000만 달러로 평가되었고, 2026년에 75억 9,000만 달러로 추정되고, 2031년까지 145억 4,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 13.88%로 성장할 전망입니다.

본 보고서는 구성 요소별(소프트웨어 플랫폼, 서비스), 도입 모델별(클라우드 기반, 기타), 기업 규모별(대기업, 중소기업), 온보딩 프로세스 유형별(고객 온보딩, 기타), 최종 사용자 산업 분야별(은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 디지털 온보딩 플랫폼 시장 동향 및 인사이트

원격 및 모바일 우선 방식을 통한 계좌 개설 가속화

디지털 온보딩 플랫폼 시장에서 원격 온보딩은 현재 관리의 엄격함뿐만 아니라 완료까지 걸리는 속도 또한 중요한 평가 기준이 되고 있습니다. 이러한 변화는 은행 업계를 넘어 확산되고 있으며, 예를 들어 Aetna사는 2026년 2월, 400만 명의 회원을 대상으로 ‘디지털 퍼스트’ 방식의 복리후생 온보딩 서비스를 시작했습니다. 또한, Jumio사는 2026년 4월, 남미 전역에서 셀카 사진을 활용한 재사용 가능한 신원 확인 솔루션을 확대했습니다. 이는 재방문 사용자를 위해 마찰이 적은 재인증 절차에 공급업체가 투자하고 있음을 보여줍니다. 또한, Interac도 2026년 5월, Incode와의 제휴를 통해 딥페이크 및 인젝션 공격에 대한 방어 기능을 추가하고, 캐나다 내 디지털 온보딩 절차를 강화하기 시작했습니다. 모바일 사용자들은 긴 심사 대기 시간을 싫어하는 경향이 있기 때문에 각 통신사들은 신속한 정보 수집, 번거로움이 적은 절차, 즉각적인 라우팅을 실현할 수 있도록 온보딩 절차를 재설계하고 있습니다. 스마트폰에서 등록 절차가 시작되는 경우가 늘어남에 따라, 완료율은 계좌 수 증가, 등록 건수, 서비스 활성화와 점점 더 밀접한 관련을 맺고 있습니다.

부문별 분석

2025년, 클라우드 기반 도입은 디지털 온보딩 플랫폼 시장 점유율의 71.29%를 차지했으며, 주요 도입 모델이 되었습니다. 구매자가 클라우드를 선호한 이유는 초기 인프라 요구 사항을 줄이고, 생체 인증의 상용화까지 걸리는 기간을 단축할 수 있기 때문입니다. 또한, 클라우드 모델에서는 벤더가 생체 인증, 부정 행위 감지, 서류 검증을 위한 모델 업데이트를 다수의 고객에게 동시에 배포할 수 있게 됩니다. 이는 공격 수법이 기존의 소프트웨어 릴리스 주기보다 훨씬 빠르게 변화하고 있는 환경에서 중요한 요소입니다. 또한, 다른 곳에서 대규모 레거시 시스템을 유지하고 있는 기관이라 하더라도 클라우드 도입이 여전히 매력적이었던 이유를 설명하는 한 가지 요인이기도 합니다.

하이브리드 도입은 2031년까지 연평균 성장률(CAGR) 14.73%로 확대될 것으로 예측되며, 이는 많은 구매자들이 온프레미스 시스템에서 완전히 철수하기보다는 과도기적인 접근 방식을 취하고 있음을 보여줍니다. 이러한 경향은 기관이 클라우드의 속도를 필요로 하면서도 기밀성이 높은 신원 확인 데이터, 암호화 제어 또는 승인 기록을 로컬 경계 내에 보관해야 하는 경우에 가장 두드러집니다. IBM이 2026년 5월에 ‘IBM Sovereign Core’를 출시한 것은 공급업체가 관할 구역에 제한된 클라우드 운영을 통해 이러한 중간적 접근 방식을 어떻게 지원하려 하고 있는지를 여실히 보여주고 있습니다. 디지털 온보딩 플랫폼 시장에서 하이브리드 방식은 일시적인 타협안이 아니라 전략적인 운영 모델로 자리 잡고 있습니다. 온프레미스 배포는 높은 수준의 보안이 요구되는 이용 사례에서 여전히 틈새 시장으로서의 중요성을 유지하고 있지만, 현재의 성장 대부분은 클라우드 오케스트레이션과 관리형 로컬 데이터 처리를 결합한 아키텍처에 집중되어 있습니다.

2025년에는 대기업이 시장의 63.41%를 차지했으며, 디지털 온보딩 플랫폼 시장에서 가장 큰 지출층이 되었습니다. 이러한 우위는 계약 규모, 여러 국가에 걸친 규정 준수 요건, 그리고 직원, 고객, 제3자에 걸쳐 더욱 복잡해진 온보딩 업무량에서 기인합니다. 또한 대기업들은 공식적인 아이덴티티 오케스트레이션 프로젝트를 추진하기 위해 필요한 예산과 거버넌스 체계를 갖추고 있었기 때문에 조기에 도입을 추진했습니다. 이러한 시스템의 도입은 대개 여러 워크플로우에 걸쳐 있으며, 공급업체와의 관계도 광범위하게 뻗어 있기 때문에 타사로 전환하기가 어렵습니다. 이것이 바로 새로운 구매자층이 시장에 진입하고 있음에도 불구하고, 여전히 대기업 계정이 수익의 상당 부분을 차지하고 있는 이유 중 하나입니다.

중소기업(SME) 시장은 2031년까지 연평균 성장률(CAGR) 16.87%를 나타낼 것으로 예측되며, 디지털 온보딩 플랫폼 시장에서 신원 오케스트레이션이 하위 시장으로 확대되고 있는 것으로 나타났습니다. 이러한 변화는 임베디드 파이낸스, 파트너 온보딩, 그리고 그동안 중소기업이 자체적으로 처리하지 않았던 규정 준수 업무의 소프트웨어 주도형 분산화와 관련이 있습니다. Modern Treasury와 Persona는 2026년 4월, 비즈니스 온보딩 및 규정 준수를 강화하기 위한 제휴를 발표했습니다. 이는 결제 업무에서 보다 간편한 API 기반의 KYB(고객 확인) 워크플로가 요구되고 있음을 반영한 것입니다. 또한, Veriff가 2026년 2월에 Vespia를 인수한 것도, 개인 인증에서 300개 이상의 관할 구역에 걸친 실시간 기업 인증으로 사업을 확대함으로써 이러한 방향성을 뒷받침하고 있습니다. 규제 대상 서비스가 수직형 소프트웨어 및 플랫폼 생태계를 통해 보급됨에 따라, 디지털 온보딩 플랫폼 시장에서 중소규모 기업은 더 이상 ‘예외적인 사례’가 아니라 중요한 구매자로 자리매김하고 있습니다.

지역별 분석

2025년, 북미는 디지털 온보딩 플랫폼 시장 점유율의 39.73%를 차지했으며 계속해서 최대 지역 부문으로서의 위상을 유지했습니다. 미국은 규제 대상 금융기관, 기업용 인사(HR) 소프트웨어에 대한 수요, 그리고 신원 확인 및 부정 행위 감지 분야의 탄탄한 공급업체 기반이 어우러져 여전히 중심적인 위치를 차지하고 있습니다. FinCEN이 2026년 4월에 발표한 AML(자금세탁방지) 및 CFT(테러자금조달방지) 개혁안에 따라, 각 기관은 기존의 온보딩 관리 체제가 결과 중심의 위험 기반 유효성 기준을 충족할 수 있는지 재검토해야 하는 상황에 놓여 있습니다. 캐나다에서는 Interac이 2026년 5월 Incode와의 제휴를 발표하고, Interac Verified 솔루션에 iBeta 레벨 3 인증을 받은 생체 인증, 딥페이크 감지 및 인젝션 공격 방어 기능을 추가했습니다. 이는 보다 견고한 디지털 온보딩 인프라에 대한 국가 차원의 투자를 보여주는 것입니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 19.13%를 기록하며 성장할 것으로 예상되며, 디지털 온보딩 플랫폼 시장에서 가장 빠르게 성장하는 지역 부문이 될 전망입니다. 이러한 성장은 모바일 우선 사용자층, 확대되는 핀테크 생태계, 그리고 디지털 ID 인프라와 상업용 온보딩 프로세스 간의 연계 강화에 힘입어 이루어지고 있습니다. 일본에서는 LIQUID eKYC가 IC 칩 기반의 신원 확인을 통해 세븐은행의 외국인 대상 계좌 개설 절차를 지원함으로써, 일부 사용자층의 수기 서류 입력에 대한 의존도를 낮췄습니다. 모바일 이용, 신원 확인 인프라, 플랫폼 주도형 서비스 제공이 결합됨에 따라 아시아태평양은 새로운 온보딩 모델 도입에 있어 여전히 가장 활발한 지역 중 하나로 자리매김하고 있습니다.

2025년, 유럽은 시장의 큰 비중을 차지했으며, 독일과 영국이 주요 하위 시장으로 자리 잡고 있습니다. 독일은 2026년, ‘Digitales-Identitaten-Gesetz(디지털 ID법)’을 통해 유럽 디지털 ID 지갑의 법적 체계를 마련하고, 국내 지갑 도입의 다음 단계를 뒷받침했습니다. 보다 광범위한 유럽 디지털 ID 프레임워크는 온보딩 플랫폼이 지갑 기반 ID 교환 및 상호 운용 가능한 신뢰 서비스를 어떻게 준비해야 하는지에 대한 방향성도 제시하고 있습니다. 남미에서는 재사용 가능한 ID 모델의 보급에 따라 그 중요성이 커지고 있으며, 2026년 4월에는 Jumio가 해당 지역 전역으로 셀카 인증 도입을 확대했습니다. 중동 및 아프리카는 절대적인 규모로 볼 때 여전히 작지만, 공급업체들이 제품의 현지화를 추진하고 각국 정부가 디지털 신분증 도입을 확대함에 따라 도입은 계속해서 진전되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the digital onboarding platform market size is projected to be USD 6.72 billion in 2025, USD 7.59 billion in 2026, and reach USD 14.54 billion by 2031, growing at a CAGR of 13.88% from 2026 to 2031.

This report is Segmented by Component (Software Platforms, and Services), Deployment Model (Cloud-Based, and More), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Onboarding Process Type (Customer Onboarding, and More), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Digital Onboarding Platform Market Trends and Insights

Acceleration of Remote and Mobile-First Account Opening

Remote onboarding is now judged by completion speed as much as by control strength in the digital onboarding platform market. That shift is spreading beyond banking, as Aetna launched a digital-first benefits onboarding experience for 4 million members in February 2026. Jumio expanded its reusable identity solution to include selfies across South America in April 2026, which shows vendor investment in repeat verification journeys with less friction for returning users. Interac also moved to strengthen national digital onboarding flows in Canada in May 2026 through a collaboration with Incode that adds deepfake and injection-attack defenses. Mobile users are less willing to tolerate long review queues, so providers are redesigning onboarding journeys for fast capture, low friction, and immediate routing. As more enrollment journeys begin on phones, completion rates are increasingly tied to account growth, enrollment volume, and service activation.

Other drivers and restraints analyzed in the detailed report include:

- Tightening KYC, AML, and Customer Due Diligence Mandates

- Rising Synthetic Identity, Deepfake, and Account Opening Fraud

- Shift to Cloud-Native and API-First Onboarding Orchestration

- Regulatory Fragmentation and Biometric Privacy Compliance Burden

- Legacy Core-System Integration Complexity and Implementation Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based deployment captured 71.29% of the digital onboarding platform market share in 2025, making it the leading deployment model. Buyers favored cloud because it lowers upfront infrastructure needs and shortens the path to live verification. The cloud model also enables vendors to distribute model updates for liveness checks, fraud detection, and document verification to many customers simultaneously. That matters in environments where attack methods are changing more quickly than traditional software release cycles. It also helps explain why cloud deployment remained attractive even for institutions that still maintain large legacy estates elsewhere.

Hybrid deployment is projected to expand at a 14.73% CAGR through 2031, showing that many buyers are building bridges rather than making full exits from on-premises systems. That pattern is strongest where institutions need cloud speed but must keep sensitive identity data, encryption controls, or approval records within local boundaries. IBM's May 2026 launch of IBM Sovereign Core highlights how suppliers are trying to support that middle path with jurisdiction-bound cloud operations. In the digital onboarding platform market, hybrid is becoming a strategic operating model rather than a temporary compromise. On-premises deployment still holds niche relevance for high-security use cases, but most growth is now centered on architectures that mix cloud orchestration with controlled local data handling.

Large enterprises accounted for 63.41% of the market in 2025, making them the largest spending cohort in the digital onboarding platform market. Their lead came from larger contract values, multi-country compliance requirements, and more complex onboarding volumes across employees, customers, and third parties. Large organizations were also earlier adopters because they had the budget and governance structures needed to justify formal identity orchestration projects. Their deployments often span several workflows, which makes vendor relationships broader and harder to displace. That helps explain why enterprise accounts still account for a large share of revenue, even as newer buyer groups enter the market.

SMEs are projected to grow at a 16.87% CAGR through 2031, showing that identity orchestration is moving downmarket within the digital onboarding platform market. This shift is tied to embedded finance, partner onboarding, and software-led distribution of compliance tasks that smaller firms did not previously handle themselves. Modern Treasury and Persona announced a partnership in April 2026 to strengthen business onboarding and compliance, reflecting the need for easier API-based KYB workflows in payment operations. Veriff's February 2026 acquisition of Vespia also supports this direction by expanding from individual verification into real-time business verification across more than 300 jurisdictions. As regulated services spread through vertical software and platform ecosystems, smaller businesses are becoming meaningful buyers rather than edge cases in the digital onboarding platform market.

Geography Analysis

North America held 39.73% of the digital onboarding platform market share in 2025, keeping it as the largest regional segment. The United States remained central because it combined regulated financial institutions, enterprise HR software demand, and a deep vendor base in identity verification and fraud detection. FinCEN's April 2026 AML and CFT reform proposal is pushing institutions to review whether legacy onboarding controls can meet a more outcome-focused standard of risk-based effectiveness. In Canada, Interac announced a May 2026 collaboration with Incode to add iBeta Level 3-validated liveness, deepfake detection, and injection-attack defense to Interac Verified solutions, signaling national-level investment in stronger digital onboarding infrastructure.

Asia-Pacific is projected to grow at a 19.13% CAGR through 2031, making it the fastest-growing regional segment in the digital onboarding platform market. Growth is being supported by mobile-first users, expanding fintech ecosystems, and stronger links between digital identity infrastructure and commercial onboarding flows. In Japan, LIQUID eKYC supported Seven Bank's foreign account opening process through IC chip-based identity verification, reducing dependence on manual document capture for some user groups. That combination of mobile use, identity infrastructure, and platform-led service delivery continues to make Asia-Pacific one of the most active regions for the adoption of new onboarding models.

Europe held a significant share of the market in 2025, with Germany and the United Kingdom as major sub-markets. Germany advanced its legal framework for the European Digital Identity Wallet in 2026 through the Digitales-Identitaten-Gesetz, supporting the next phase of national wallet deployment. The broader European Digital Identity framework is also shaping how onboarding platforms prepare for wallet-based identity exchange and interoperable trust services. South America is gaining relevance as reusable identity models spread, with Jumio extending selfie across the region in April 2026. The Middle East and Africa remained smaller in absolute terms, but adoption continued to improve as vendors localized their products and governments expanded digital identity efforts.

- Jumio Corporation

- Trulioo Information Services Inc.

- Signicat AS

- Veriff OU

- Au10tix Ltd.

- IDnow GmbH

- Sum and Substance Ltd.

- Shufti Pro Limited

- Persona Identities, Inc.

- Socure Inc.

- First Mile Group, Inc. d/b/a Alloy

- Mitek Systems, Inc.

- Ondato UAB

- UAB iDenfy

- PXL Vision AG

- Innovatrics, s.r.o.

- Incode Technologies, Inc.

- ID.me, LLC

- Intellicheck, Inc.

- HyperVerge Technologies Private Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening KYC, AML, and Customer Due Diligence Mandates

- 4.2.2 Acceleration of Remote and Mobile-First Account Opening

- 4.2.3 Rising Synthetic Identity, Deepfake, and Account Opening Fraud

- 4.2.4 Shift to Cloud-Native and API-First Onboarding Orchestration

- 4.2.5 Emergence of Reusable Digital Identity Wallets and Verifiable Credentials

- 4.2.6 Embedded Finance and Platform-Led Multi-Party Onboarding Demand

- 4.3 Market Restraints

- 4.3.1 Regulatory Fragmentation and Biometric Privacy Compliance Burden

- 4.3.2 Legacy Core-System Integration Complexity and Implementation Cost

- 4.3.3 Gray-Zone Review Queues From AI Spoof Edge Cases and Model Governance

- 4.3.4 Data Localization and Sovereign Cloud Requirements

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software Platforms

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By Onboarding Process Type

- 5.4.1 Customer Onboarding

- 5.4.2 Employee Onboarding

- 5.4.3 Vendor and Supplier Onboarding

- 5.4.4 Partner and Merchant Onboarding

- 5.5 By End User Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecom

- 5.5.4 Retail and E-commerce

- 5.5.5 Industrial Manufacturing

- 5.5.6 Government and Public Sector

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Netherlands

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Jumio Corporation

- 6.4.2 Trulioo Information Services Inc.

- 6.4.3 Signicat AS

- 6.4.4 Veriff OU

- 6.4.5 Au10tix Ltd.

- 6.4.6 IDnow GmbH

- 6.4.7 Sum and Substance Ltd.

- 6.4.8 Shufti Pro Limited

- 6.4.9 Persona Identities, Inc.

- 6.4.10 Socure Inc.

- 6.4.11 First Mile Group, Inc. d/b/a Alloy

- 6.4.12 Mitek Systems, Inc.

- 6.4.13 Ondato UAB

- 6.4.14 UAB iDenfy

- 6.4.15 PXL Vision AG

- 6.4.16 Innovatrics, s.r.o.

- 6.4.17 Incode Technologies, Inc.

- 6.4.18 ID.me, LLC

- 6.4.19 Intellicheck, Inc.

- 6.4.20 HyperVerge Technologies Private Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment